Intellia presents positive data for hereditary angioedema treatment

Xylem Inc. (NYSE:XYL) reported strong third-quarter results on October 28, 2025, with revenue growth across all segments and significant margin expansion leading to a full-year guidance increase. The water technology company’s stock rose 2.14% in pre-market trading following the announcement.

Quarterly Performance Highlights

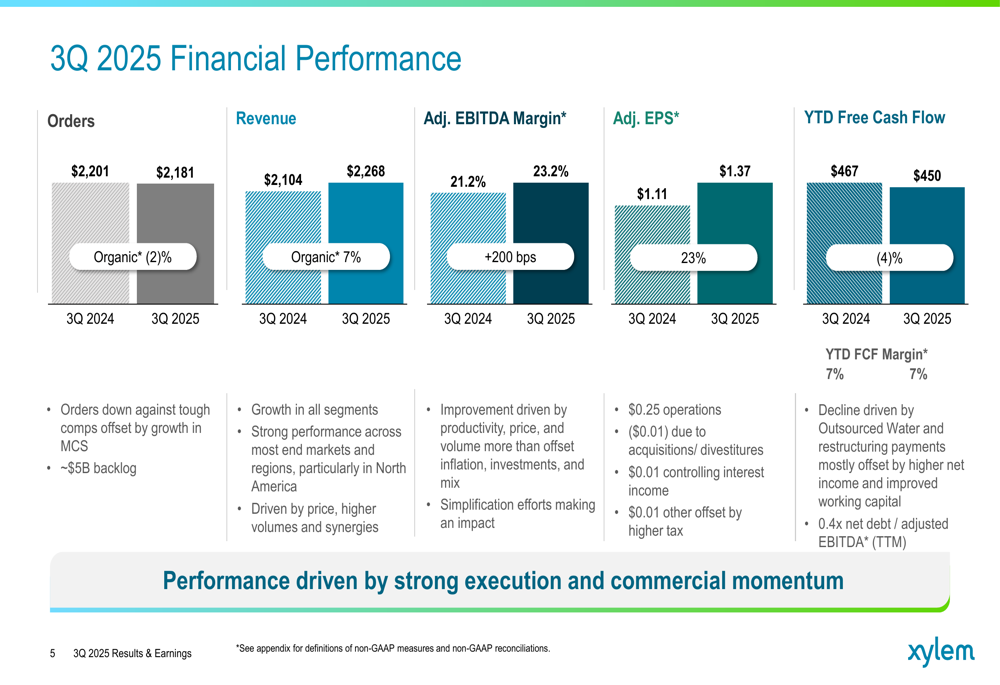

Xylem delivered solid financial results in the third quarter, with revenue reaching $2.27 billion, representing 8% overall growth and 7% organic growth compared to the same period last year. The company’s adjusted earnings per share increased by 23% to $1.37, exceeding analyst expectations of $1.23.

"We exceeded targets through commercial and operational momentum," the company stated in its presentation, highlighting "revenue growth across all segments and most end markets with double-digit growth in MCS and WSS."

Particularly impressive was the company’s profitability improvement, with adjusted EBITDA margin expanding by 200 basis points year-over-year to reach a record 23.2%. This margin expansion was attributed to productivity improvements, favorable pricing, and increased volumes more than offsetting inflation, investments, and mix challenges.

As shown in the following chart of Xylem’s quarterly financial performance:

Orders were slightly down at $2.18 billion, representing a 2% organic decline against what the company described as "tough comps," though this was partially offset by growth in the Measurement and Control Solutions segment. The company maintains a robust backlog of approximately $5 billion.

Segment Performance Analysis

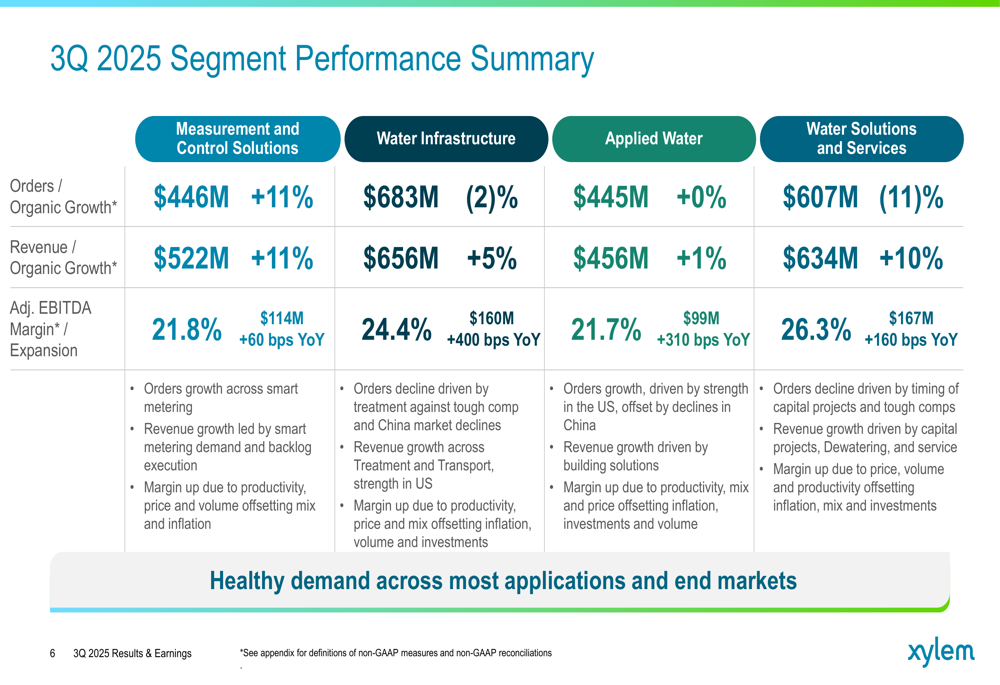

All four of Xylem’s business segments delivered revenue growth in the quarter, though with varying degrees of strength in orders and profitability.

The Measurement and Control Solutions segment was a standout performer, with 11% organic growth in both orders and revenue, driven by strong demand for smart metering solutions. The segment’s adjusted EBITDA margin expanded by 60 basis points year-over-year to 21.8%.

The Water Infrastructure segment saw 5% organic revenue growth despite a 2% decline in orders, which the company attributed to treatment against tough comparisons and market declines in China. This segment achieved the most significant margin improvement, with adjusted EBITDA margin expanding by 400 basis points to 24.4%.

The following segment performance breakdown illustrates these trends:

The Applied Water segment delivered modest 1% organic revenue growth with flat orders, while its adjusted EBITDA margin improved substantially by 310 basis points to 21.7%, driven primarily by building solutions.

The Water Solutions and Services segment achieved 10% organic revenue growth despite an 11% decline in orders, which the company attributed to timing of capital projects and tough comparisons. This segment maintained the highest adjusted EBITDA margin at 26.3%, representing a 160 basis point improvement.

Strategic Initiatives

Xylem highlighted its ongoing simplification efforts as a key driver of profitable growth. The company is implementing the 80/20 methodology across its business segments, which is helping to drive margin improvement through operational efficiency.

"80/20 progress driving margin improvement," the company noted, adding that "enhanced customer experience resulting in deeper relationships" has been another benefit of this approach.

During the earnings call, CEO Matthew Pine emphasized the importance of this methodology, stating, "80/20 is moving from a tool set to more of a critical piece on how we run the business."

The company also announced the divestiture of its International Metering business, enabling greater focus on the North American meter market. CFO Bill Grogan highlighted the growth potential in this area, noting, "We’re still less than 50% there [on AMI adoption]."

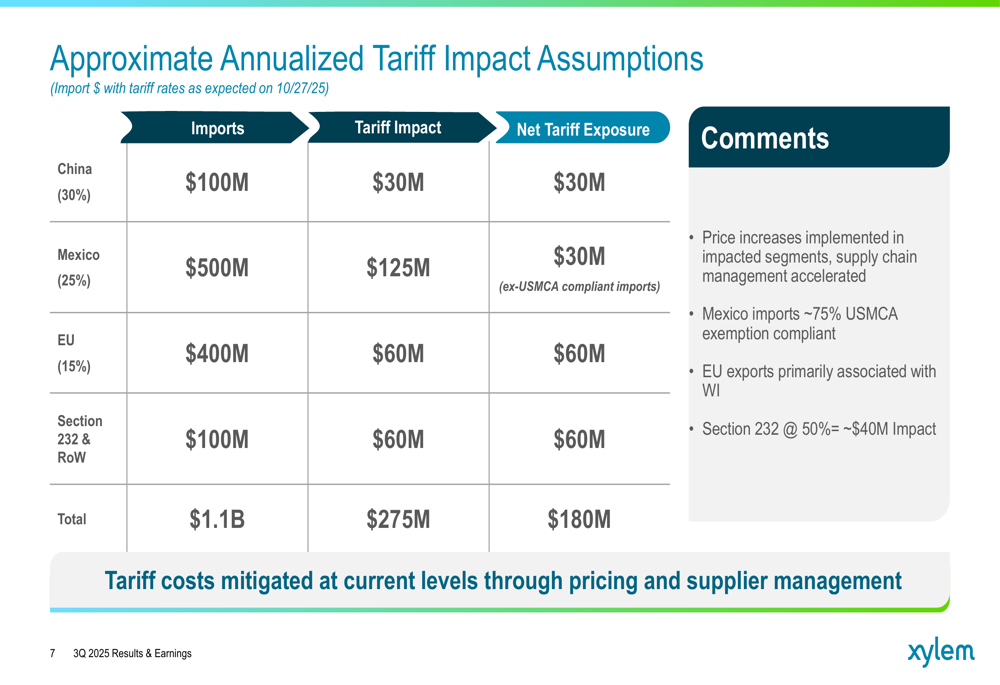

Xylem is also actively managing the impact of tariffs on its business. The company provided a detailed breakdown of its tariff exposure and mitigation strategies:

Forward-Looking Statements

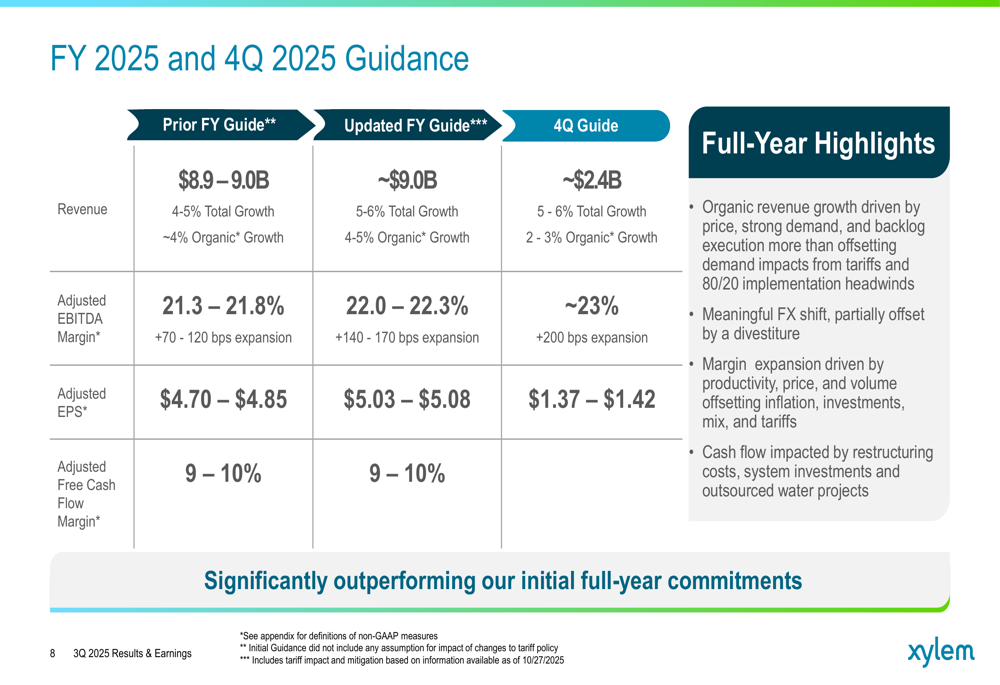

Based on its strong year-to-date performance and positive outlook, Xylem raised its full-year guidance across key metrics. The company now expects:

- Revenue of approximately $9.0 billion, representing 5-6% total growth and 4-5% organic growth

- Adjusted EBITDA margin of 22.0-22.3%, an expansion of 140-170 basis points

- Adjusted EPS of $5.03-$5.08, up from the previous guidance of $4.70-$4.85

For the fourth quarter specifically, Xylem projects:

- Revenue of approximately $2.4 billion, representing 5-6% total growth and 2-3% organic growth

- Adjusted EBITDA margin of approximately 23%, a 200 basis point expansion

- Adjusted EPS of $1.37-$1.42

The following guidance table provides a comprehensive view of these updates:

The company cited several factors supporting its updated outlook, including "organic revenue growth driven by price, strong demand, and backlog execution more than offsetting demand impacts from tariffs and 80/20 implementation headwinds."

Conclusion and Market Position

Xylem appears well-positioned for continued growth despite some macroeconomic challenges. The company’s focus on operational efficiency, strategic portfolio management, and pricing discipline has enabled it to deliver strong results and raise guidance.

"Strongly positioned to drive sustainable growth and value creation," the company concluded in its presentation.

The market responded positively to these results, with Xylem’s stock rising 2.14% in pre-market trading to $152.60, approaching its 52-week high of $152.84. With a current market capitalization of approximately $35.82 billion, Xylem maintains a robust financial health score according to various metrics, with particularly strong scores in growth and profitability.

However, investors should note potential challenges, including market headwinds in China, continued reliance on the North American market, and the impact of economic uncertainties such as potential government shutdowns. The company’s moderate debt levels and healthy current ratio of 1.9x provide some cushion against these risks.

The following key takeaways summarize Xylem’s current position:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.