Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Yara International ASA (OTC:YARIY) (OB:YAR) reported strong second-quarter 2025 results on July 18, showcasing significant financial improvements amid favorable market conditions in the global fertilizer industry. The Norwegian fertilizer producer continues to benefit from its strategic focus on premium products, operational efficiency, and cost reduction initiatives.

The company’s performance comes against a backdrop of supportive nitrogen market fundamentals, with strong demand from key markets like India and constrained exports from China. These market dynamics have helped maintain healthy pricing for Yara’s products, particularly for its premium nitrate and NPK offerings.

Quarterly Performance Highlights

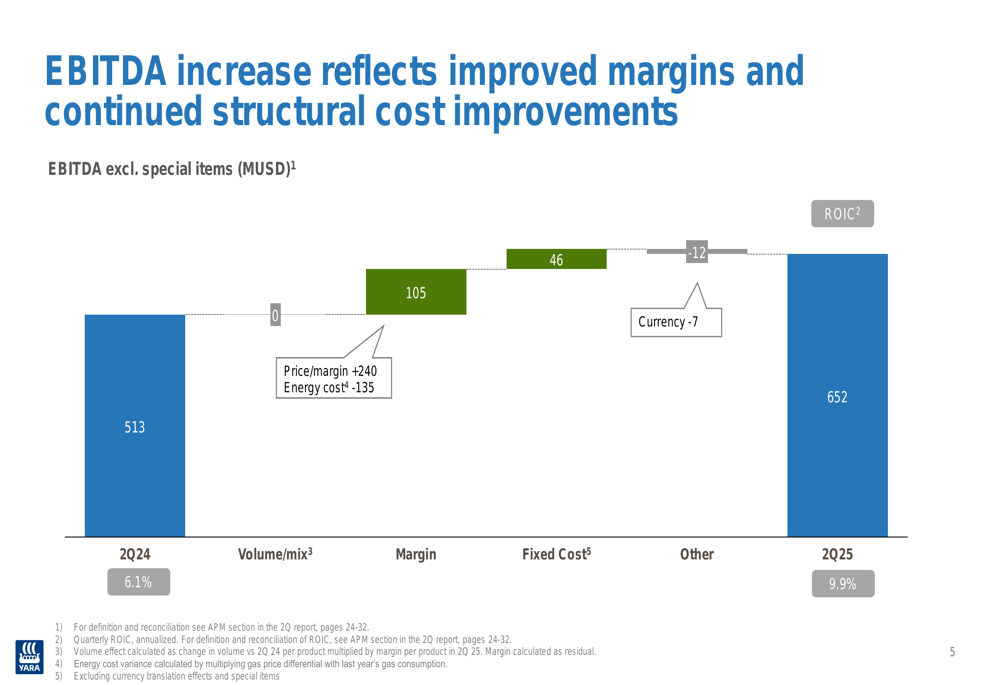

Yara delivered impressive financial results in Q2 2025, with EBITDA excluding special items reaching 652 million USD, a 27% increase from 513 million USD in the same period last year. This improvement was primarily driven by enhanced commercial performance, record-high production levels, and supportive market fundamentals.

The company’s adjusted earnings per share for the first half of 2025 reached 1.92 USD, a substantial increase from 0.64 USD in the previous year. Return on invested capital (ROIC) on a 12-month rolling basis improved to 7.0%, up from 5.6% in Q2 2024.

As shown in the following breakdown of EBITDA growth factors:

The EBITDA improvement was primarily driven by margin improvements (+105 million USD) and fixed cost reductions (+46 million USD), with smaller contributions from volume/mix changes (+5 million USD). These gains were partially offset by currency effects (-7 million USD) and other factors (-12 million USD).

Segment Performance Analysis

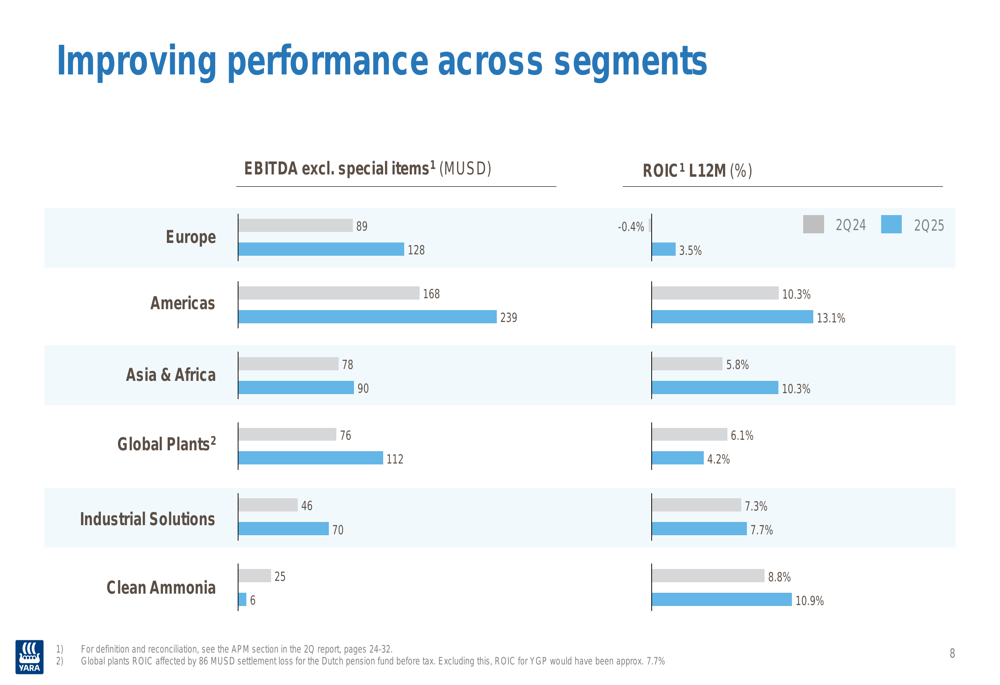

Yara reported improved performance across most of its business segments, with particularly strong results in the Americas and Europe regions. The company’s segmented approach continues to provide resilience and balanced growth opportunities across different markets.

The following chart illustrates the performance improvements across Yara’s business segments:

The Americas segment showed the strongest absolute improvement, with EBITDA increasing from 168 to 239 million USD and ROIC rising from 10.3% to 13.1%. Europe also demonstrated significant recovery, with EBITDA climbing from 89 to 128 million USD and ROIC turning positive at 3.5% from -0.4% a year earlier.

Asia & Africa, Global Plants, and Industrial Solutions segments all posted solid gains, while Clean Ammonia was the only segment to report a decrease in EBITDA, dropping from 25 to 6 million USD, though its ROIC improved from 8.8% to 10.9%.

Operational Excellence and Cost Management

Yara’s operational performance has been bolstered by increased asset productivity and continued focus on sustainability. The company has managed to slightly increase its finished product production while simultaneously reducing its greenhouse gas emission intensity.

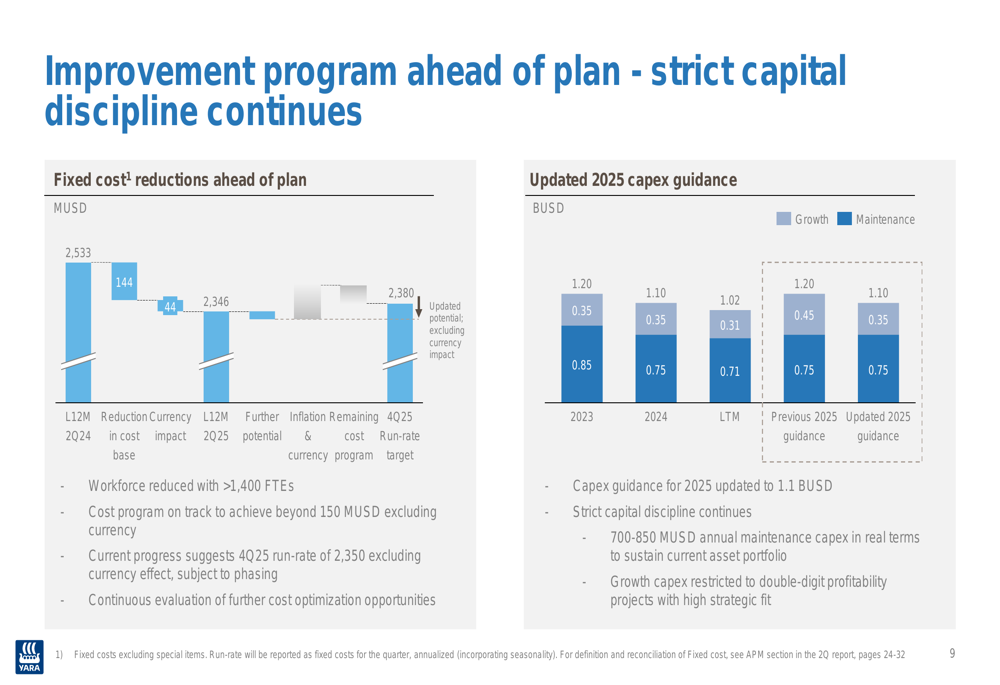

The company’s improvement program is ahead of schedule, as demonstrated in the following chart:

Fixed costs have been reduced from 2,533 million USD in Q2 2024 to 2,346 million USD in Q2 2025, representing significant progress toward the company’s cost reduction targets. Additionally, Yara has updated its 2025 capital expenditure guidance to 1.1 billion USD, comprising 0.75 billion USD for maintenance and 0.35 billion USD for growth initiatives.

Total (EPA:TTEF) crop nutrition deliveries increased from 6,100 kilotonnes in Q2 2024 to 6,273 kilotonnes in Q2 2025, with the Americas region showing the strongest growth. European full-season deliveries were up 5%, outperforming the broader fertilizer industry’s 1% growth.

Financial Position and Capital Allocation

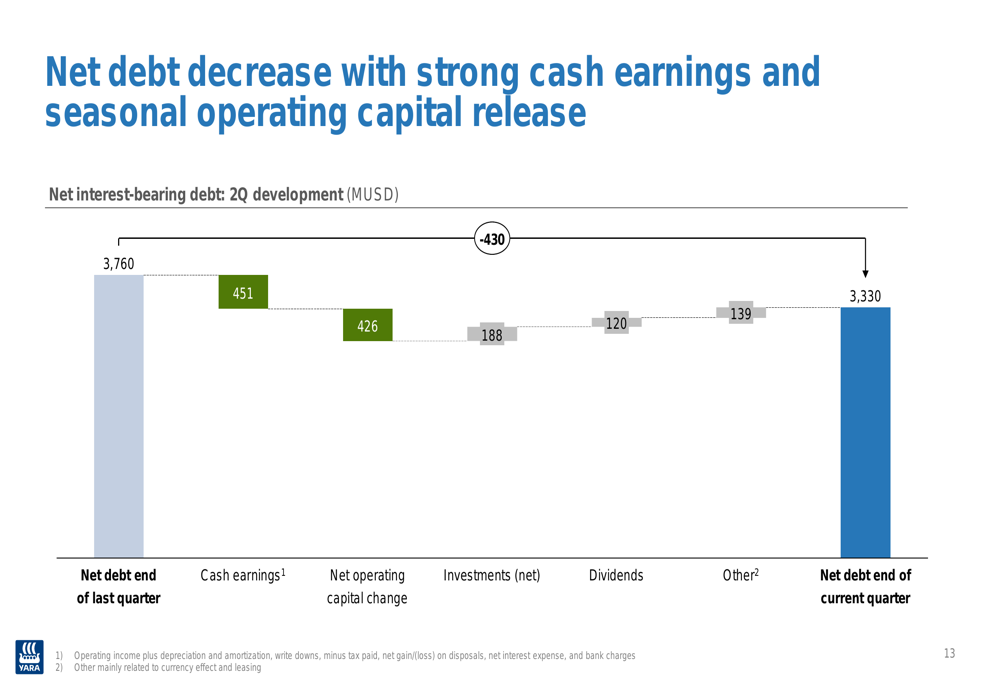

Yara has strengthened its financial position during the quarter, with net debt decreasing by 430 million USD to 3,330 million USD. This improvement was driven by strong cash earnings and a seasonal release of operating capital.

The following waterfall chart illustrates the factors contributing to the net debt reduction:

Strong cash earnings of 451 million USD and positive net operating capital change of 426 million USD were the main contributors to debt reduction. These positive factors were partially offset by investments (188 million USD), dividends (120 million USD), and other items (139 million USD).

The company’s strong cash flow generation provides flexibility for future investments while maintaining its commitment to shareholder returns.

Strategic Initiatives and Outlook

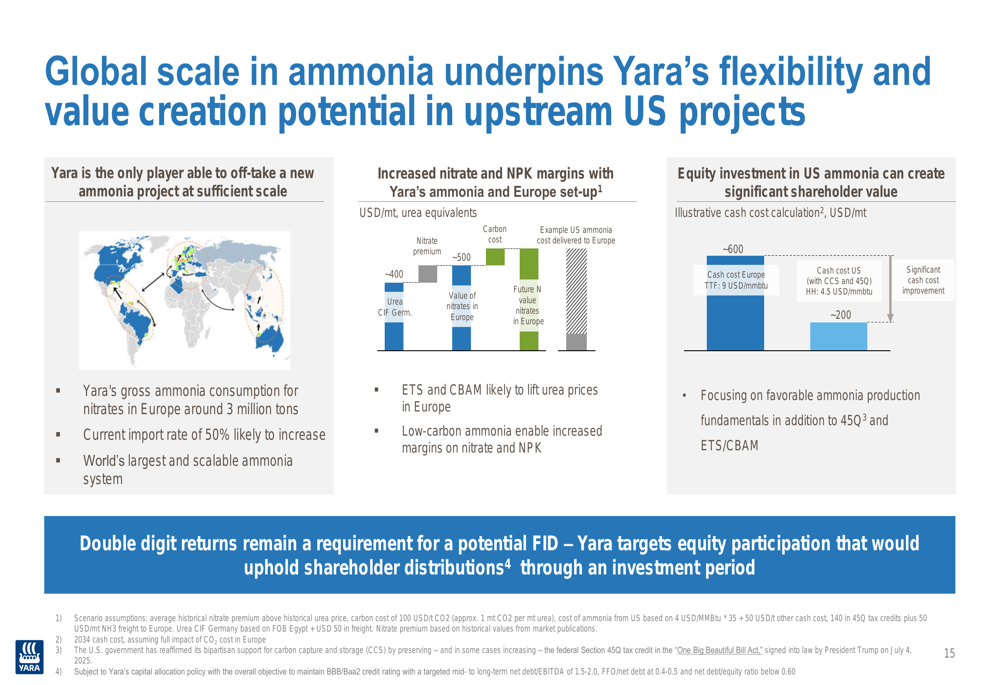

Yara is leveraging its global scale in ammonia production to create value through potential upstream US projects. The company’s unique position as the only player able to off-take a new ammonia project at sufficient scale provides strategic advantages.

The following illustration highlights Yara’s global ammonia strategy and US opportunities:

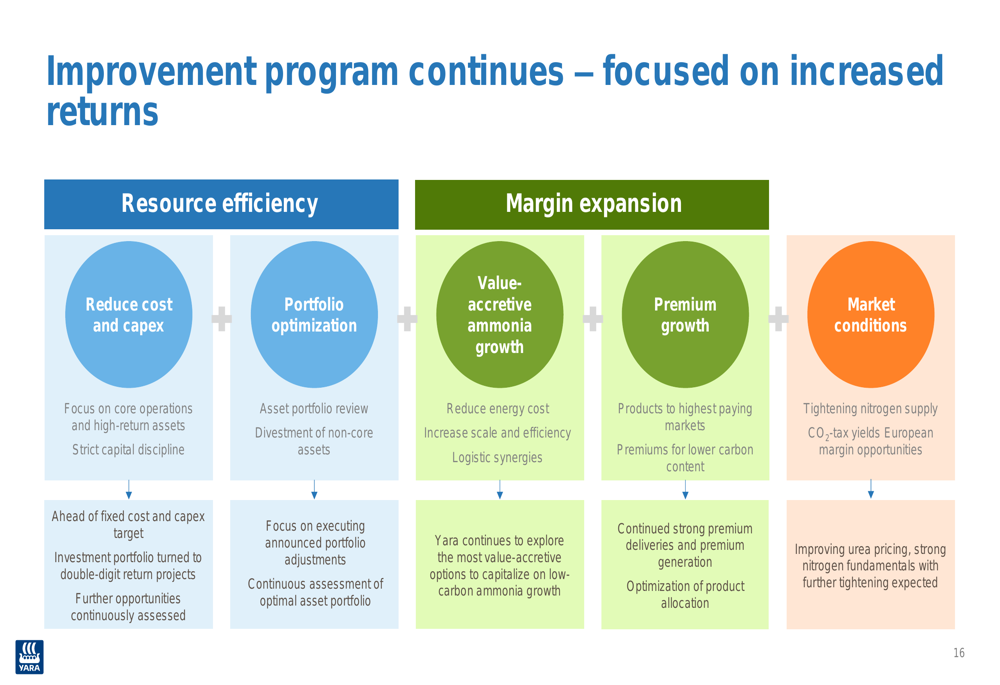

The company is focusing on favorable ammonia production fundamentals, including low-carbon initiatives that can enhance margins on nitrate and NPK products. Yara’s improvement program continues to target increased returns through resource efficiency, margin expansion, and capitalizing on favorable market conditions.

Yara’s ongoing strategic initiatives are summarized in this framework:

Looking ahead, Yara remains committed to its core operations while pursuing value-accretive growth opportunities, particularly in premium products and low-carbon ammonia. The company’s disciplined approach to capital allocation and operational excellence positions it well to navigate market fluctuations while delivering sustainable shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.