Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

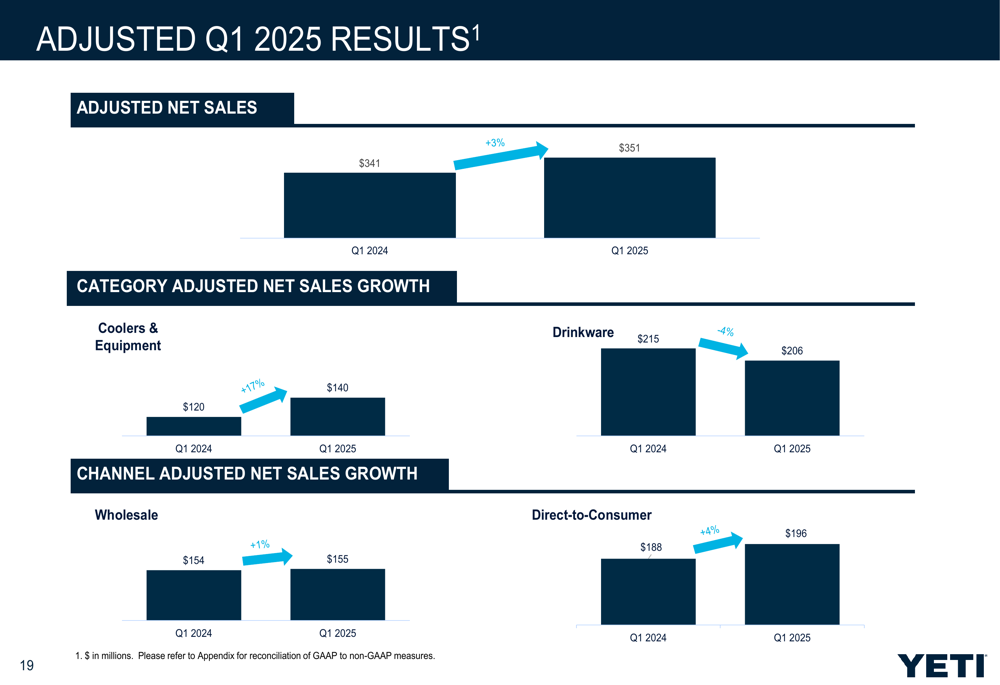

YETI Holdings Inc (NYSE:YETI) presented its first quarter 2025 results on May 8, revealing modest overall growth but a significant downward revision to its full-year outlook. The outdoor product manufacturer reported a 3% year-over-year increase in adjusted net sales to $351 million, while adjusted earnings per share declined 9% to $0.31. The company’s stock, which had risen 2.12% to $27.93 in the previous session, was trading down 4.19% in premarket activity, reflecting investor concerns about the reduced guidance.

Quarterly Performance Highlights

YETI’s Q1 2025 performance showed divergent trends across product categories. The Coolers & Equipment segment demonstrated robust growth of 17% year-over-year, reaching $140 million and accounting for 40% of total sales. However, this strength was partially offset by a 4% decline in the larger Drinkware segment, which fell to $206 million and represented 59% of sales.

As shown in the following chart of quarterly sales by product category:

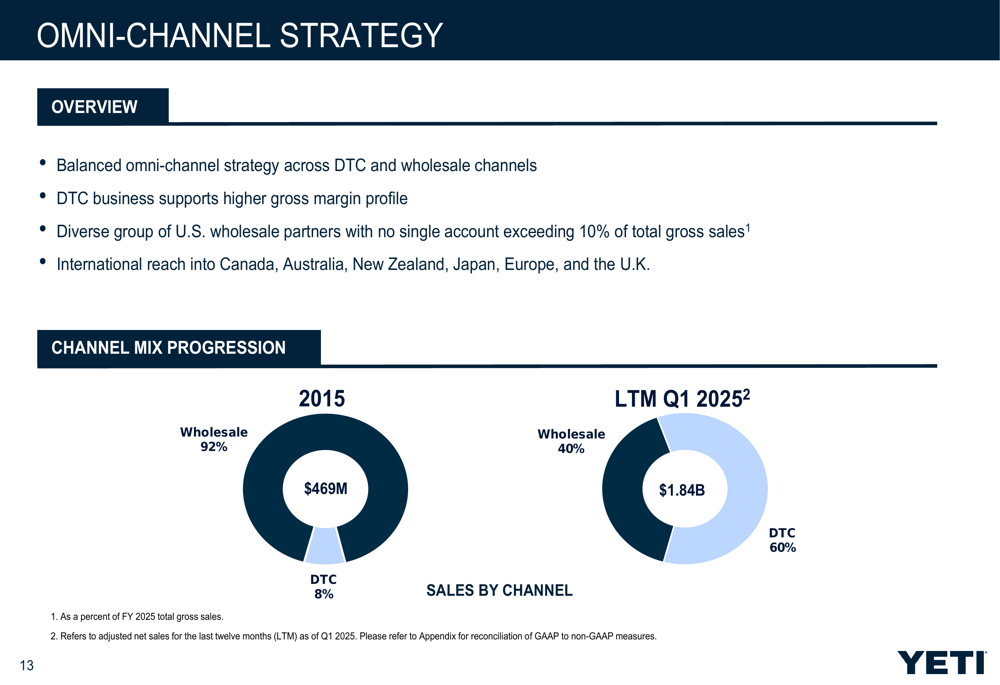

The company’s channel strategy continues to evolve, with Direct-to-Consumer (DTC) sales increasing 4% to $196 million, while Wholesale sales grew marginally by 1% to $155 million. This reflects YETI’s ongoing shift toward higher-margin direct sales, which now account for 60% of total revenue compared to just 8% in 2015.

The company’s omni-channel evolution is illustrated in this breakdown:

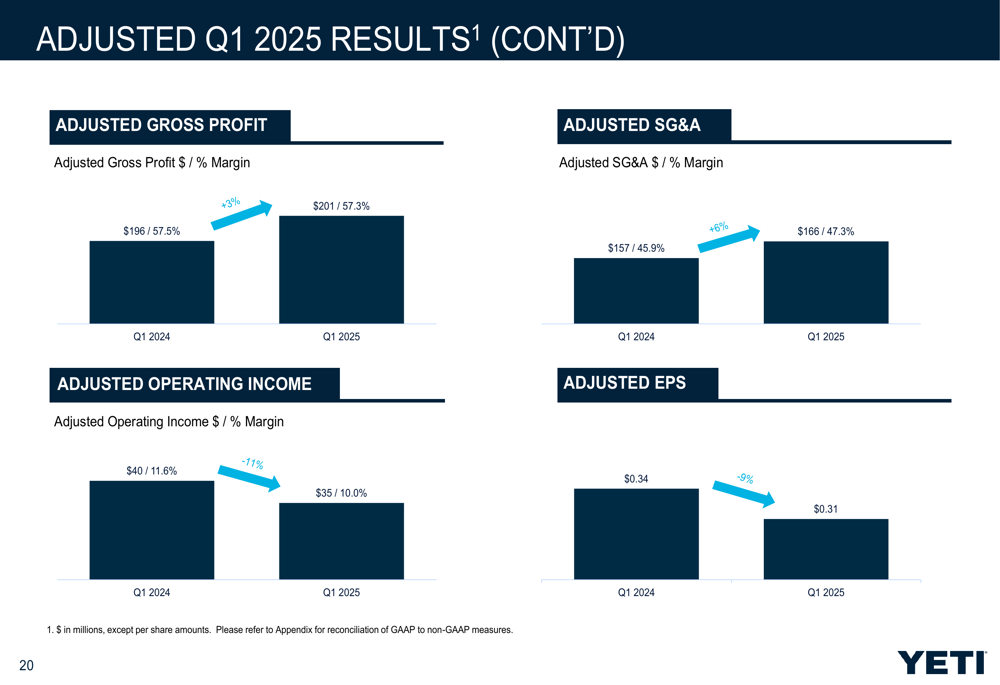

From a profitability perspective, YETI faced margin pressure during the quarter. Adjusted operating income declined 11% to $35 million, with operating margin contracting to 10.0% from 11.6% in the prior year period. Adjusted gross profit increased 3% to $201 million, but gross margin slightly decreased to 57.3% from 57.5%.

The following chart details these profitability metrics:

Strategic Initiatives

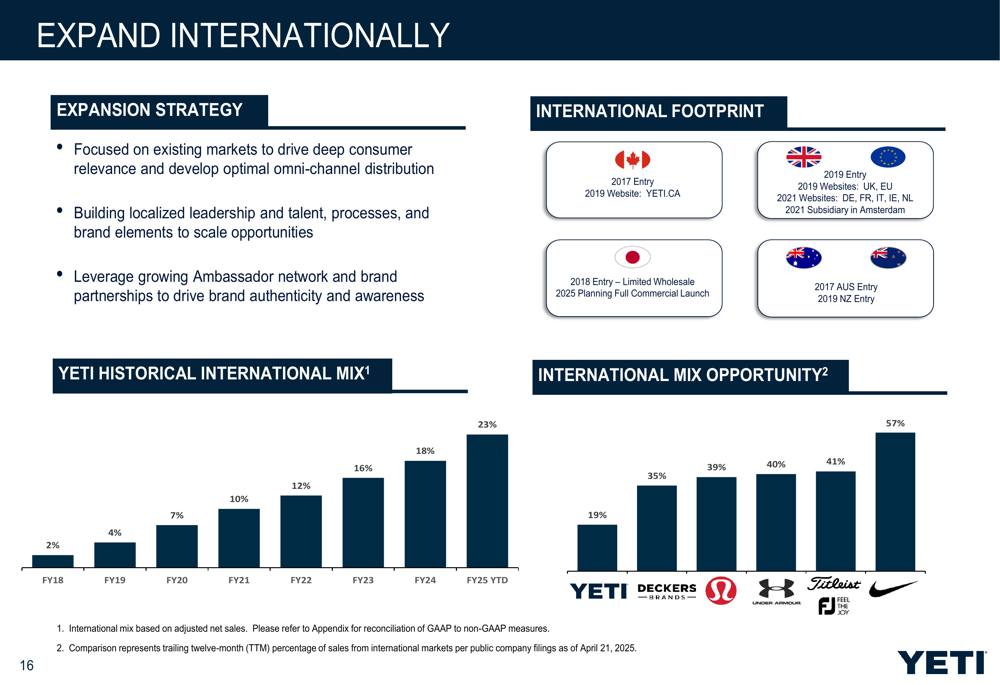

Despite near-term challenges, YETI continues to execute on its long-term strategic priorities, focusing on expanding its customer base, introducing new products, accelerating direct-to-consumer sales, and growing internationally.

The company’s strategic roadmap is outlined below:

International expansion remains a particular bright spot, with sales growing 22% year-over-year and now representing 23% of total revenue, up from just 2% in fiscal 2018. YETI is focused on deepening its presence in existing markets while building localized leadership and brand elements to scale opportunities.

The company’s international strategy and growth trajectory are illustrated here:

YETI is also making progress on diversifying its supply chain, particularly reducing its dependence on China for manufacturing. The company now expects 90% of U.S. Drinkware capacity to be outside China by the end of 2025, with less than 5% of total cost of goods sold exposed to U.S. tariffs on Chinese imports going forward.

Forward-Looking Statements

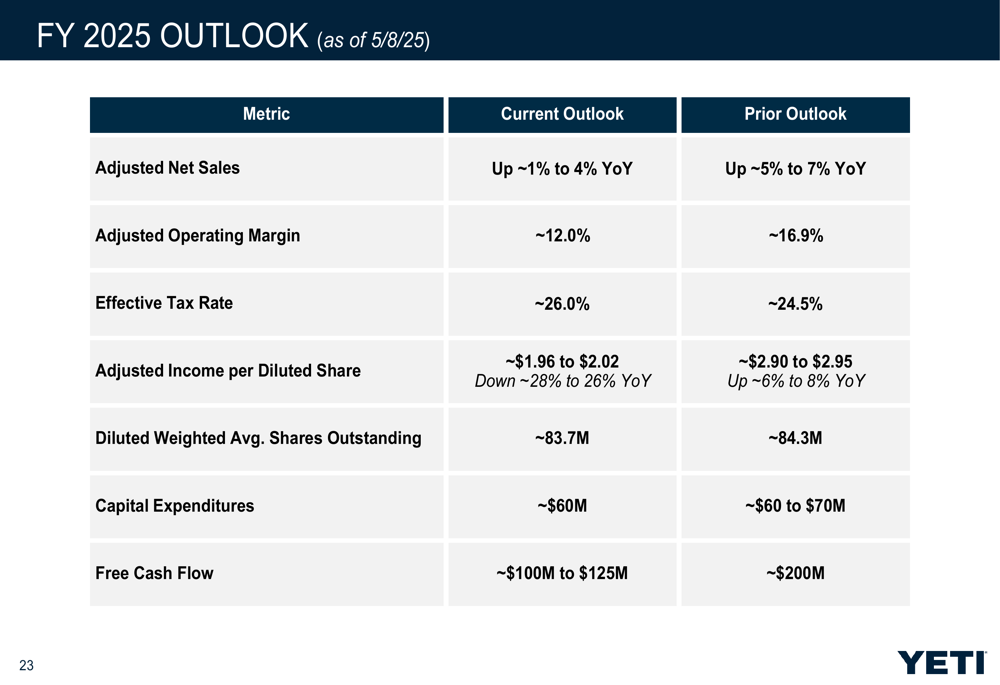

In a concerning development for investors, YETI significantly reduced its full-year 2025 outlook. The company now expects sales growth of just 1-4%, down from its previous guidance of 5-7%. Adjusted operating margin is projected at approximately 12.0%, a substantial reduction from the previous forecast of 16.9%. Similarly, adjusted earnings per share are now expected to be $1.96-$2.02, compared to the previous range of $2.90-$2.95.

The revised guidance is detailed in the following comparison:

This downward revision suggests YETI is facing more significant headwinds than previously anticipated, potentially including competitive pressures, shifting consumer preferences, or broader economic challenges affecting discretionary spending.

Conclusion

YETI’s Q1 2025 results present a mixed picture. While the company continues to make progress on its long-term strategic initiatives, particularly international expansion and the shift toward direct-to-consumer sales, the significant downward revision to full-year guidance raises concerns about near-term growth prospects.

The strength in Coolers & Equipment and international markets demonstrates the company’s ability to diversify its revenue streams, but weakness in the core Drinkware segment and overall margin pressure point to challenges ahead. Investors will likely focus on whether YETI can maintain its brand strength and premium positioning while navigating what appears to be a more difficult operating environment than previously expected.

Looking at YETI’s historical performance, the company has demonstrated consistent growth from 2018 through 2024, increasing adjusted net sales from $779 million to $1.84 billion while improving its balance sheet by reducing debt from $333 million to $78 million. This track record suggests the company has the financial foundation to weather current challenges while continuing to invest in long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.