Bitcoin price today: dips below $112k, near 6-wk low despite Fed cut bets

Introduction & Market Context

Zelluna ASA (OSE:ZLNA) presented its second quarter 2025 business update on August 20, highlighting progress with its TCR-NK cell therapy platform amid a challenging financial environment. The company’s stock has continued to struggle, trading at 13.5 NOK, down from 13.8 NOK after Q1 results and representing a significant decline from its 52-week high of 35 NOK.

CEO Namir Hassan and CFO Hans Vassgård Eid emphasized the company’s strategic positioning in the rapidly evolving cell therapy market, where recent high-value acquisitions have validated early-stage platforms. The presentation highlighted AbbVie (NYSE:ABBV)’s recent acquisition of Capstan, an early Phase I in vivo CAR-T company, for approximately $2.1 billion as evidence of strong market appetite for innovative cell therapy approaches.

Strategic Positioning and Technology Platform

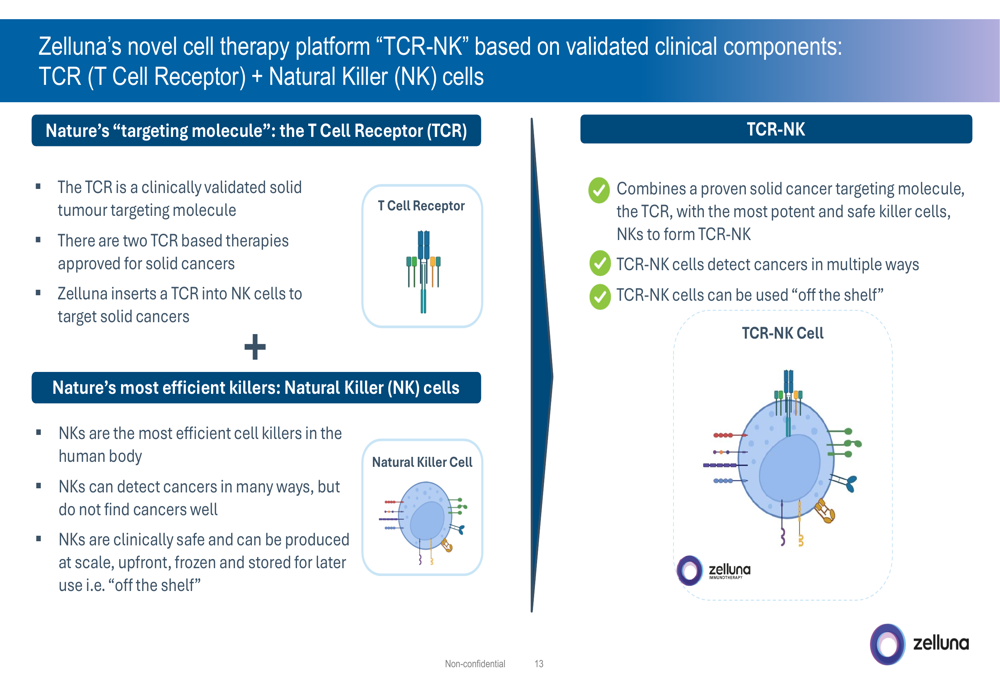

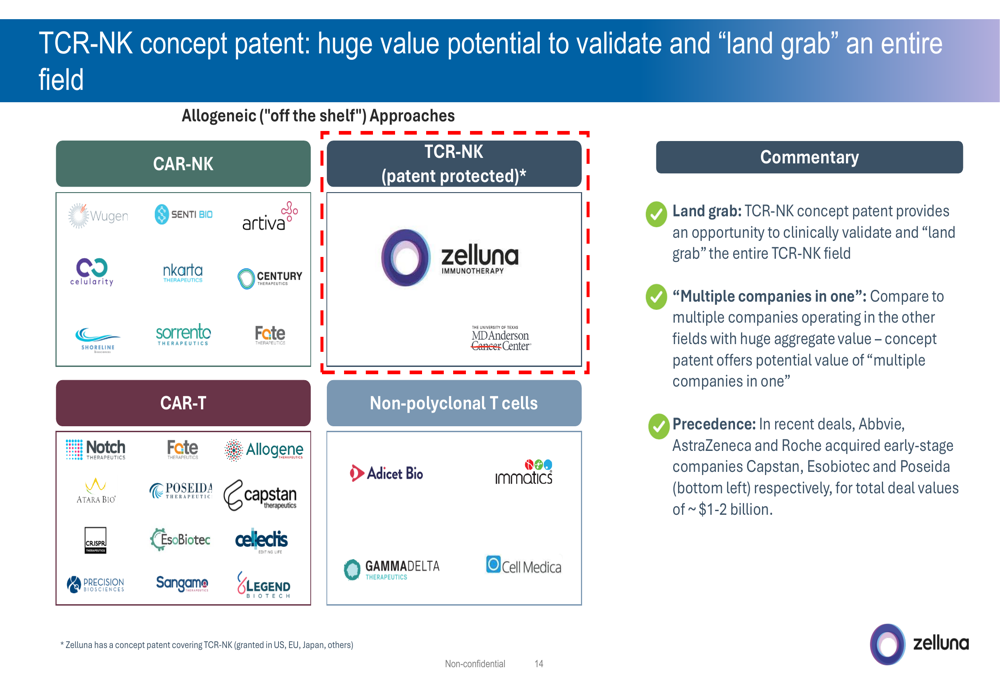

Zelluna’s core value proposition centers on its TCR-NK (T Cell Receptor + Natural Killer cells) platform, which the company claims combines clinically validated targeting molecules with efficient killer cells for solid tumor treatment. A key competitive advantage highlighted in the presentation is Zelluna’s concept patent covering the entire TCR-NK therapeutic field, granted in the US, EU, Japan, and other markets.

The company positioned this patent protection as analogous to "owning the CAR-T space," drawing parallels to the aggregate value of approved CAR-T products.

As shown in the diagram above, Zelluna’s approach combines T Cell Receptors (TCRs), which can target solid tumors, with Natural Killer (NK) cells, which the company describes as efficient cell killers that can be produced at scale as "off-the-shelf" therapies. This contrasts with current cell therapies that have primarily succeeded in liquid cancers but face challenges with solid tumors.

The competitive landscape illustration demonstrates Zelluna’s unique position in the allogeneic cell therapy market. The company emphasized that recent deals by major pharmaceutical companies like AbbVie, AstraZeneca (NASDAQ:AZN), and Roche acquiring early-stage cell therapy companies for $1-2 billion validate their strategic approach.

Pipeline Development and Clinical Timeline

Zelluna maintained that its lead program, ZI-MA4-1, remains on track for IND/CTA filing in the second half of 2025, with first patient dosing expected in the first half of 2026. The company reported several advances toward this goal, including:

- Completion of preclinical work

- Initiation of GMP production of clinical material in July

- Submission of a scientific advice briefing package to the UK MHRA in July

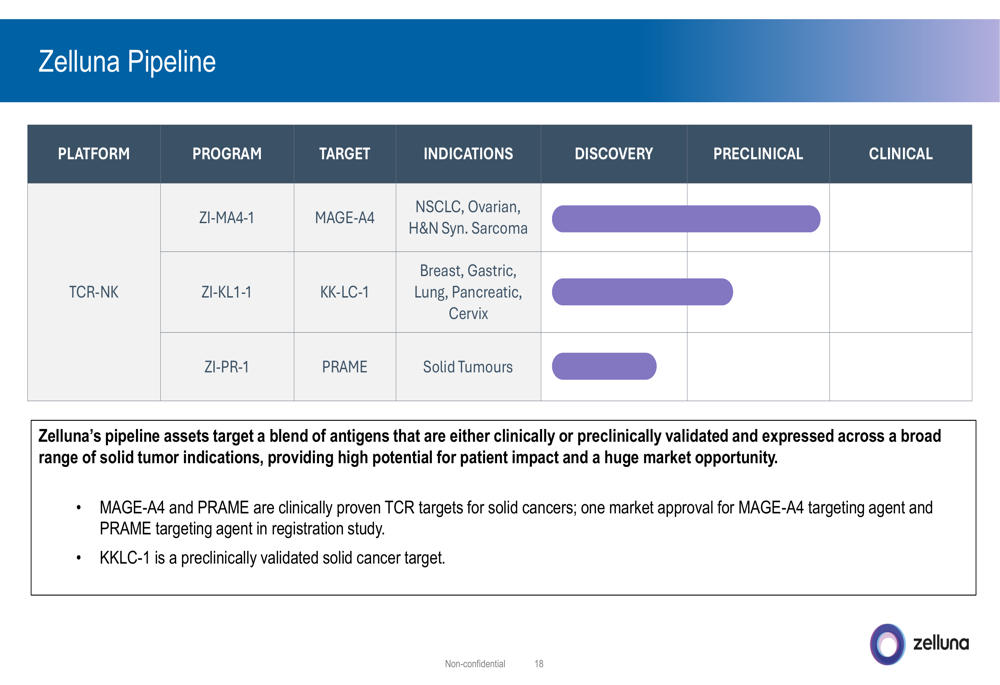

The company’s pipeline targets multiple cancer-associated antigens across various solid tumor indications:

The pipeline chart shows Zelluna’s three main programs. The lead candidate ZI-MA4-1 targets MAGE-A4 for non-small cell lung cancer, ovarian cancer, head and neck cancer, and synovial sarcoma. Two earlier-stage programs target KK-LC-1 and PRAME antigens across multiple solid tumor types.

Professor Fiona Thistlethwaite was quoted in the presentation expressing optimism about ZI-MA4-1: "I am genuinely excited to see the progress of ZI-MA4-1 into the clinic. I am optimistic that the dual killing mechanism of the NK cells and tumour antigen directed TCR will provide us with the step-change that we need in the solid tumour setting."

The presentation also noted that the company’s UV1 cancer vaccine program had produced "disappointing results" in three completed Phase II trials, and would be "wrapped up," though topline results for two ongoing trials (LUNGVAC and DOVACC) are expected during 2025.

Financial Performance and Cash Position

Zelluna’s financial situation presents significant challenges. The company reported:

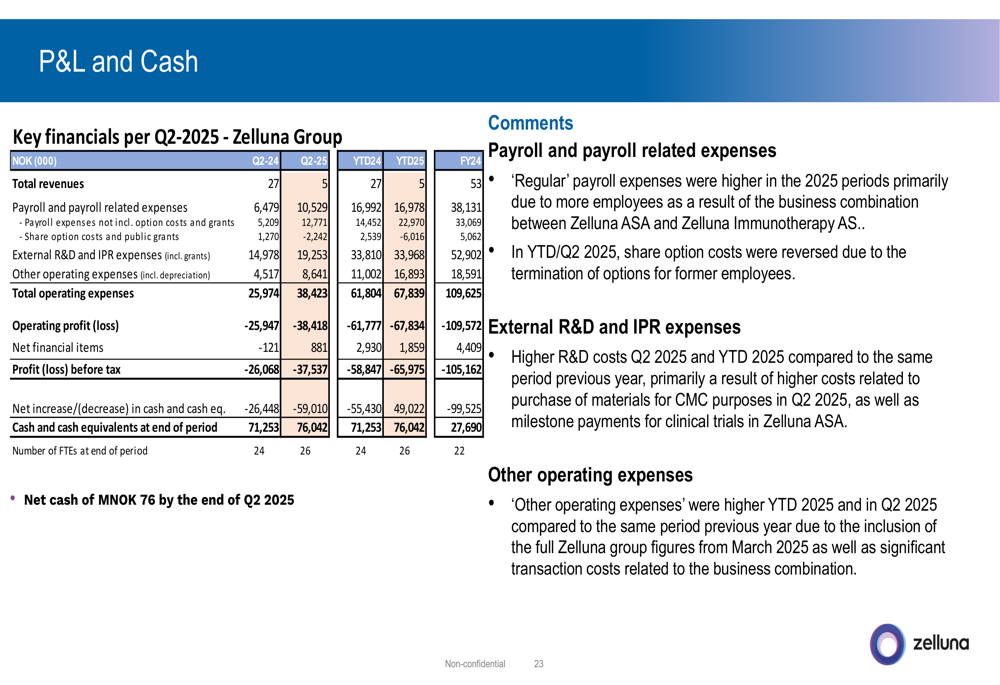

- Cash position of MNOK 76 (approximately $7 million) at the end of Q2 2025, down substantially from the MNOK 135 reported at the end of Q1

- Operating loss (EBIT) of MNOK -38 for Q2 2025 and MNOK -68 year-to-date

- Profit before tax of MNOK -38 for Q2 and MNOK -66 year-to-date

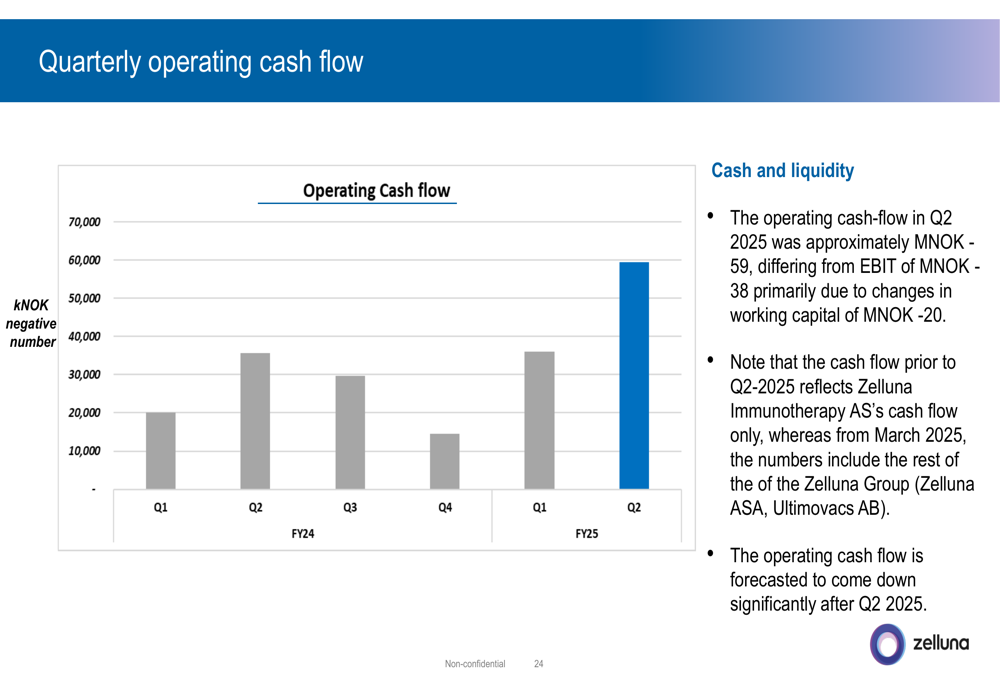

- Operating cash flow of approximately MNOK -59 in Q2, the highest quarterly burn rate to date

The financial table above shows deteriorating performance across most metrics compared to the same period last year. Total (EPA:TTEF) operating expenses increased to MNOK 38.4 in Q2 2025 from MNOK 26.0 in Q2 2024, driven by higher payroll expenses, R&D costs, and other operating expenses.

The quarterly operating cash flow chart illustrates the concerning trend of accelerating cash burn, reaching MNOK -59 in Q2 2025. However, management emphasized that this rate is expected to "come down significantly after Q2 2025."

Despite these challenges, the company maintains that its current cash position provides a runway into Q2 2026, which would cover the planned IND/CTA submission and initial clinical activities. The company also noted that it completed a reverse share split (10:1) effective April 1, 2025, and issued 227,096 new shares at NOK 26 per share on May 27, 2025.

Forward-Looking Statements and Milestones

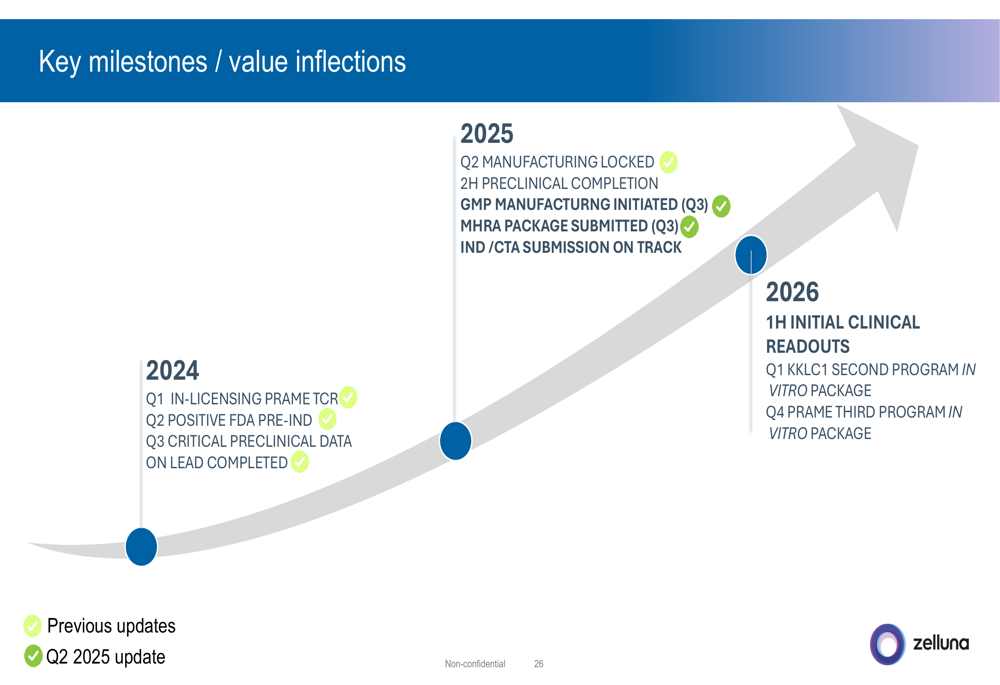

Zelluna outlined its key upcoming milestones and value inflection points:

As shown in the timeline above, Zelluna has completed several milestones in 2024-2025, including positive FDA pre-IND feedback, completion of critical preclinical data, and initiation of GMP manufacturing. The company’s near-term focus is on:

1. Receiving MHRA feedback (expected September 2025)

2. Submitting IND/CTA application (H2 2025)

3. Initial clinical readouts (H1 2026)

4. Advancing second (KKLC1) and third (PRAME) programs

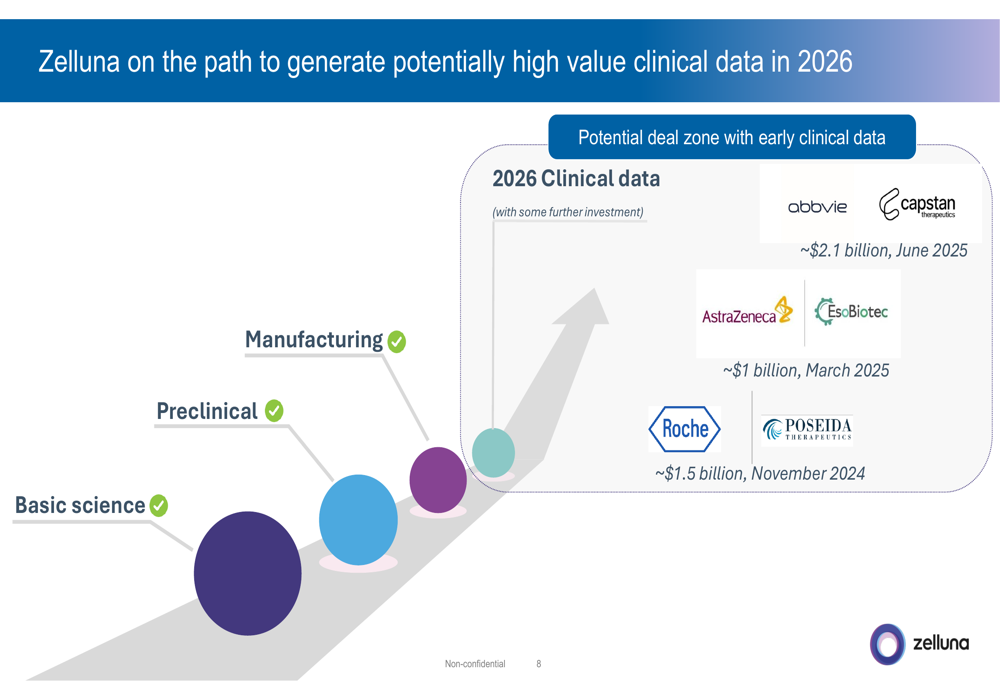

The company emphasized that early clinical data in this sector has driven high-value deals, pointing to recent acquisitions in the $1-2 billion range for early-stage cell therapy companies.

This timeline illustrates Zelluna’s path to potentially high-value clinical data in 2026, with benchmark deals shown for context. The company positions itself in the "potential deal zone with early clinical data" by 2026.

While Zelluna maintains an optimistic outlook on its technology platform and clinical timeline, the accelerating cash burn and declining stock price suggest investors remain cautious about the company’s prospects. The next few quarters will be critical as Zelluna attempts to advance its lead candidate toward the clinic while managing its financial resources.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.