Gold prices tick higher on fresh US tariff threats, Fed rate cut hopes

Introduction & Market Context

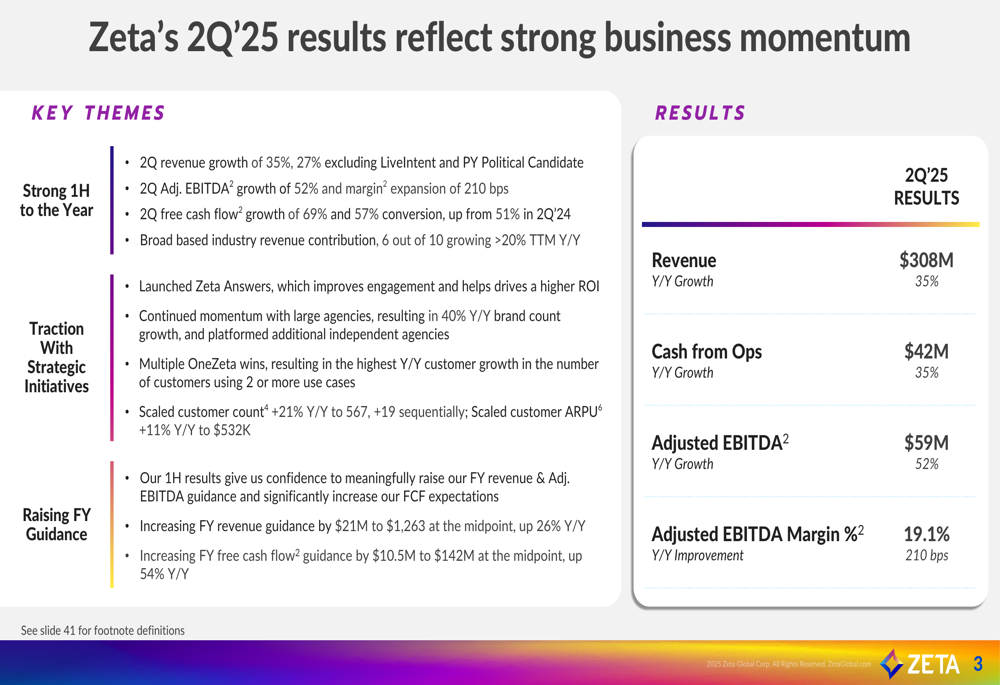

Zeta Global Holdings Corp (NYSE:ZETA) released its Q2 2025 earnings presentation on August 5, 2025, showcasing strong performance that exceeded expectations. The marketing technology company’s stock closed at $15.80 on the day of the announcement, with aftermarket trading showing a 1.27% increase to $16.00, indicating positive investor reception of the results.

The company’s performance comes amid a challenging environment for marketing technology providers, with Zeta positioning itself as a consolidator in the fragmented marketing landscape through its integrated platform approach.

Quarterly Performance Highlights

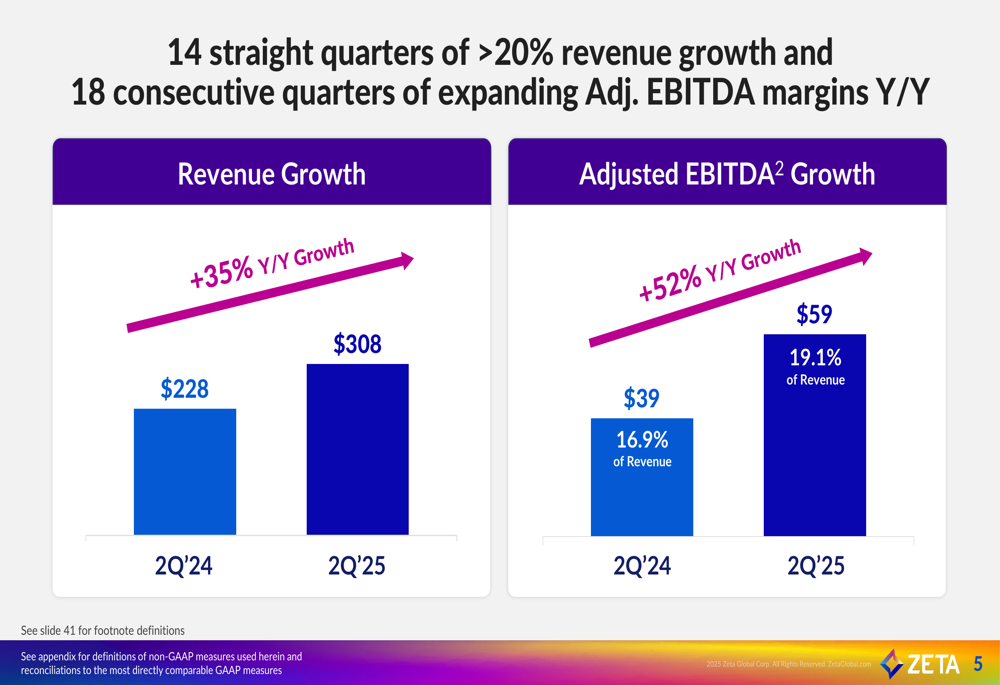

Zeta reported impressive Q2 2025 results, with revenue reaching $308 million, representing a 35% year-over-year increase. Even when excluding the LiveIntent acquisition and political candidate revenue, organic growth remained strong at 27% year-over-year.

As shown in the following chart of quarterly performance metrics, Zeta achieved significant improvements across all key financial indicators:

Adjusted EBITDA grew by 52% year-over-year to $59 million, with margin expanding by 210 basis points to 19.1%. Free cash flow showed even stronger growth, increasing 69% year-over-year to $33.6 million, with conversion improving from 51% in Q2’24 to 57% in Q2’25.

The company’s consistent growth trajectory is further illustrated in this revenue and adjusted EBITDA chart:

Detailed Financial Analysis

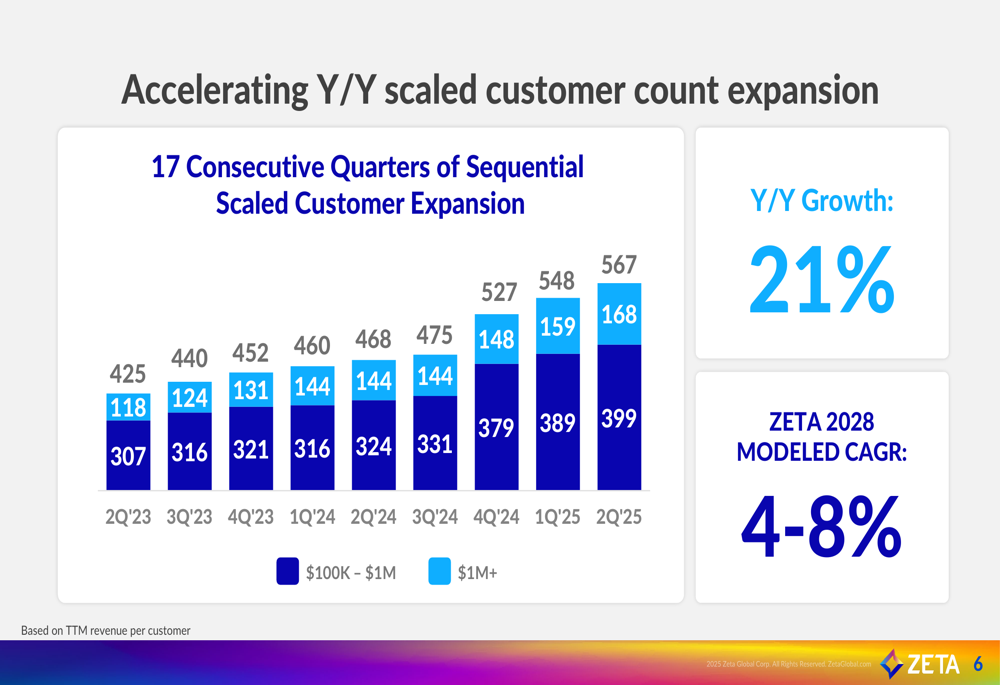

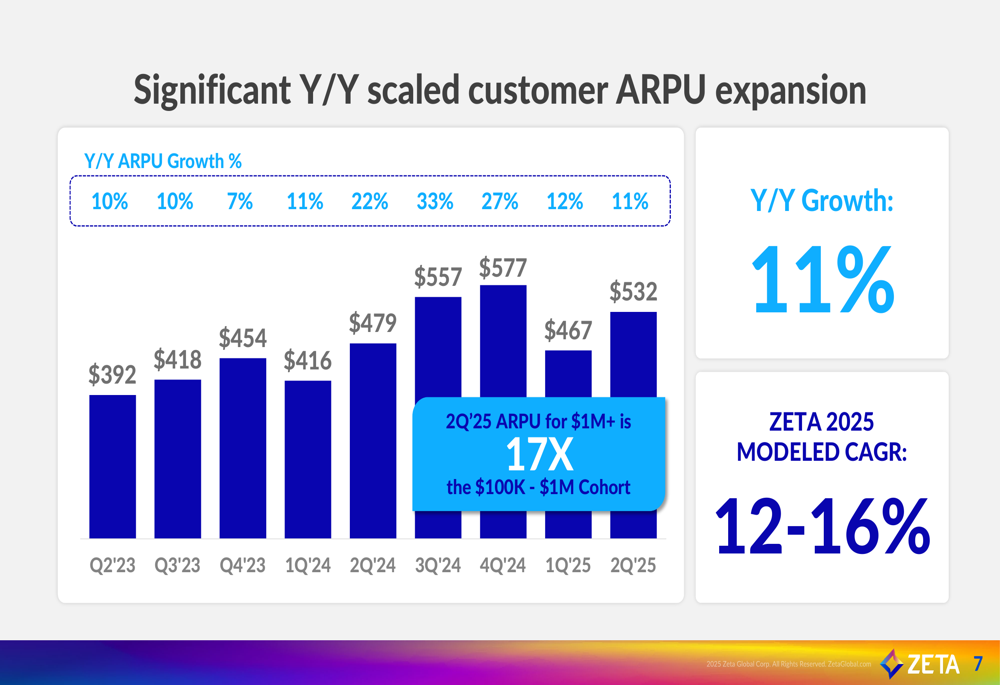

Zeta’s customer metrics showed robust growth, with scaled customer count (those spending at least $100,000 annually) increasing 21% year-over-year to 567, adding 19 new customers sequentially. Average revenue per user (ARPU) for scaled customers grew 11% year-over-year to $532,000.

The company’s customer expansion is visualized in the following chart showing 17 consecutive quarters of sequential growth:

Particularly noteworthy is the revenue leverage Zeta achieves as customers increase their spending. Customers in the greater than $1 million spending category generated quarterly ARPU of $1,578,000 in Q2’25, which is 17 times higher than the $91,000 ARPU for customers spending between $100,000 and $1 million.

The following chart illustrates Zeta’s consistent ARPU expansion over time:

Customer longevity also drives higher ARPU, with scaled customers who have been with Zeta for more than three years generating an average of $2.6 million in annual revenue, compared to $0.9 million for customers of less than one year. Approximately 90% of Zeta’s revenue comes from customers who have been with the company for more than one year.

Forward Guidance

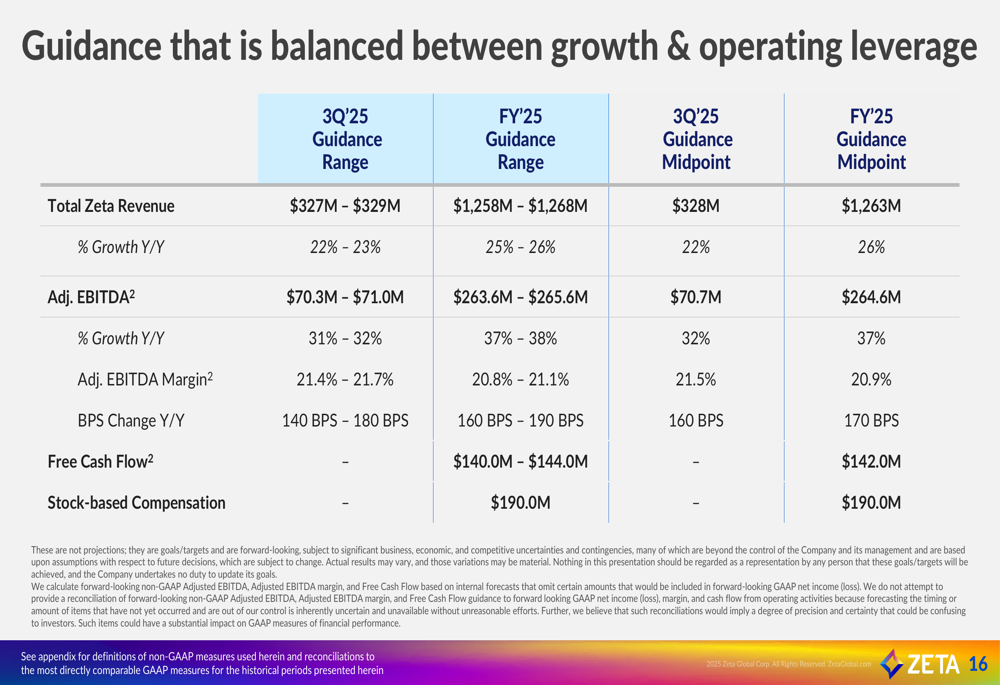

Based on strong first-half performance, Zeta raised its full-year 2025 guidance. The company now expects:

- Revenue of $1,258 million to $1,268 million (midpoint:$1,263 million), up $21 million from previous guidance and representing 26% year-over-year growth

- Adjusted EBITDA of $263.6 million to $265.6 million (midpoint:$264.6 million), with margin expansion of 170 basis points year-over-year

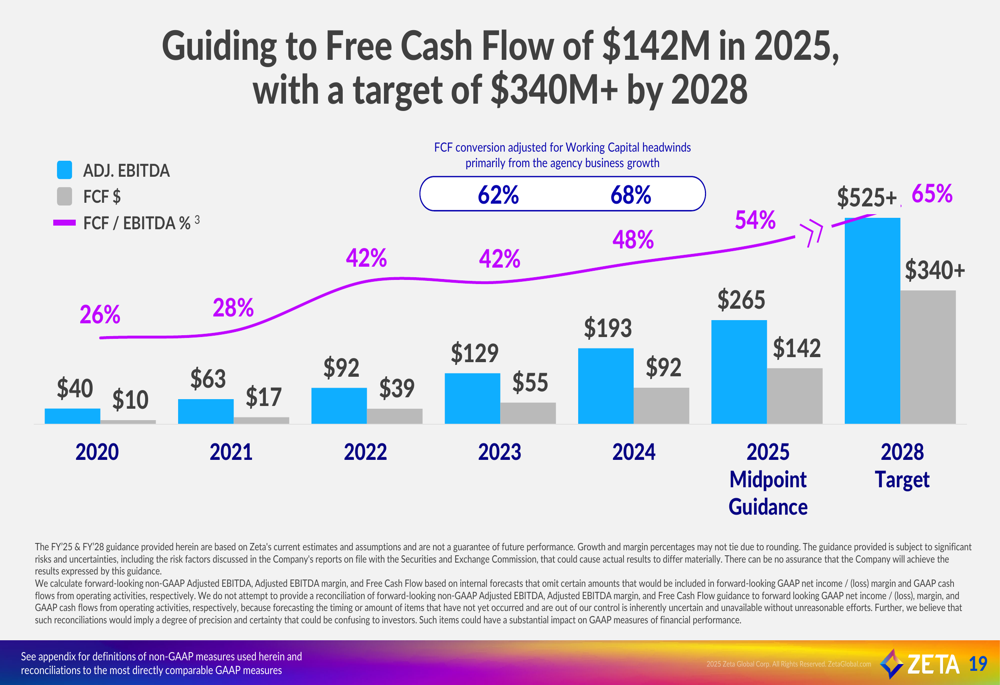

- Free cash flow of $140 million to $144 million (midpoint:$142 million), up $10.5 million from previous guidance and representing 54% year-over-year growth

The detailed guidance breakdown is presented in the following table:

For Q3 2025, Zeta expects revenue of $327 million to $329 million (22-23% growth) and adjusted EBITDA of $70.3 million to $71.0 million (31-32% growth) with margins expanding by 140-180 basis points year-over-year.

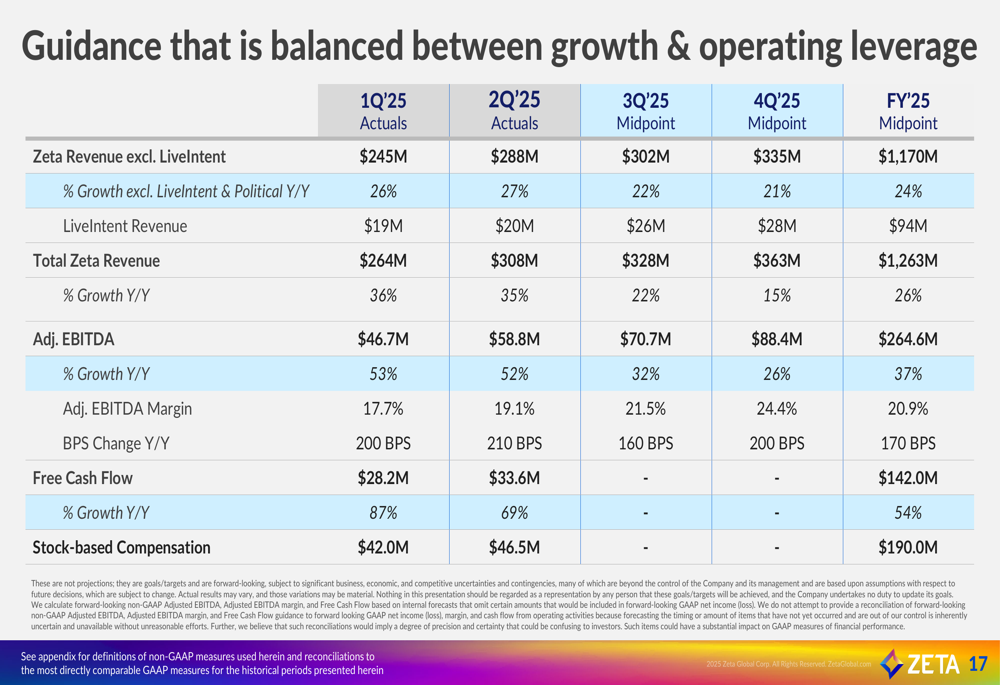

The quarterly progression of guidance shows consistent improvement throughout the year:

Long-Term Strategy (Zeta 2028)

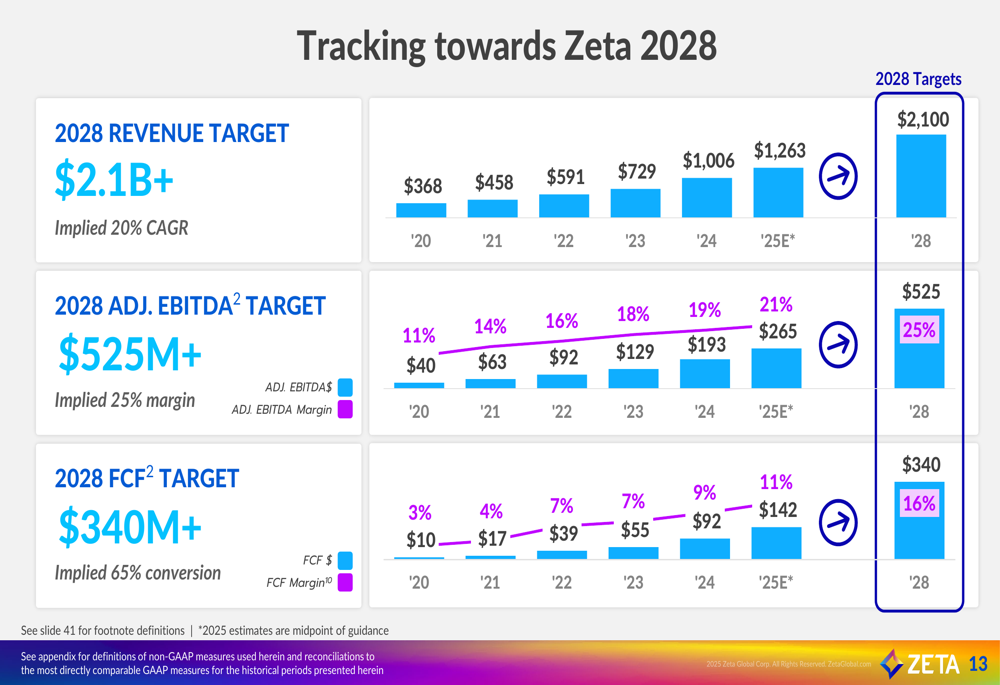

Zeta reaffirmed its long-term targets for 2028, which include:

- Revenue of $2.1 billion+ (implied 20% CAGR from 2025)

- Adjusted EBITDA of $525 million+ (implied 25% margin)

- Free cash flow of $340 million+ (implied 65% conversion)

The company’s progress toward these targets is illustrated in the following chart:

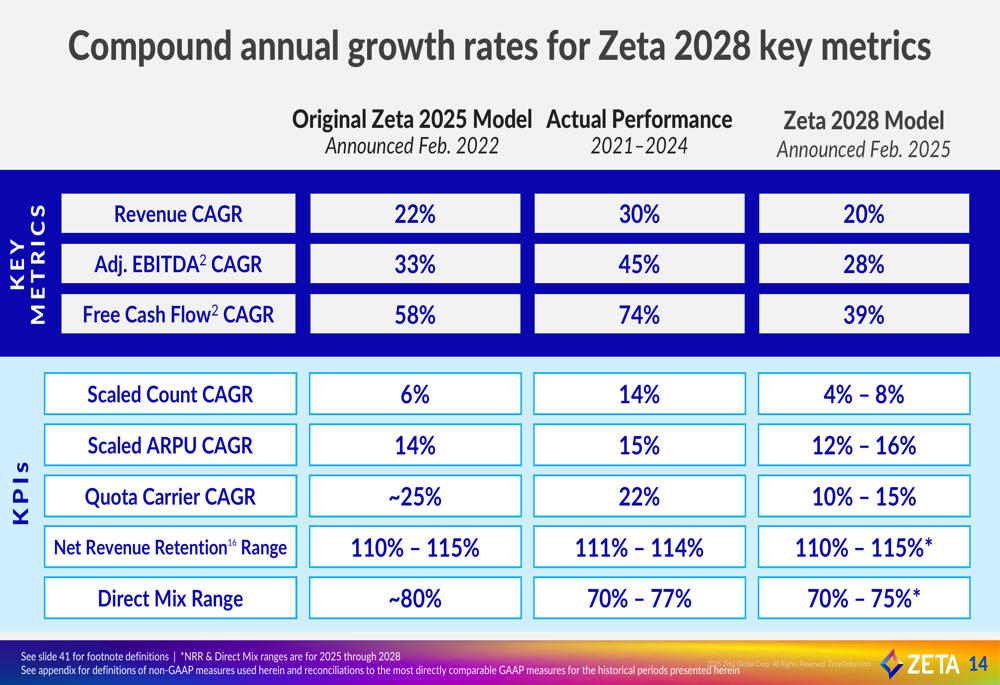

Zeta’s performance against its previous long-term targets (Zeta 2025) has been strong, with the company exceeding its original projections across key metrics. The comparison between original targets, actual performance, and new 2028 targets is detailed below:

The company also highlighted its improving capital efficiency, with free cash flow conversion expected to increase from 48% in 2024 to 54% in 2025, targeting 65% by 2028:

Competitive Positioning

Zeta emphasized its strengthening market position, noting that it serves 44% of the Fortune 100 companies, including 11 of the 17 largest Consumer & Retail companies and 5 of the 10 largest Insurance companies in the world.

The company was named a leader in the latest Forrester Wave report, scoring the highest possible rating in 13 of 22 categories. This recognition reinforces Zeta’s competitive advantage in the marketing technology landscape.

Zeta’s strategy focuses on consolidating the fragmented marketing technology stack by integrating data management, marketing automation, and engagement capabilities into a single platform. The company positions itself at the intersection of data, media, and technology, addressing a U.S. total addressable market of $83 billion growing at 12-14% annually.

Financial Efficiency Improvements

In addition to strong operational performance, Zeta highlighted significant improvements in financial efficiency. Stock-based compensation is projected to decline from 57% of revenue in 2021 to 15% in 2025, while share count dilution is expected to decrease from approximately 15% in FY’24 to 4-6% in FY’25 and 3-4% in FY’26.

These improvements, combined with increasing free cash flow conversion, suggest that Zeta is transitioning toward a more mature financial profile while maintaining strong growth rates.

Conclusion

Zeta Global’s Q2 2025 results demonstrate continued momentum across key financial and operational metrics. With 14 consecutive quarters of 20%+ revenue growth and 18 consecutive quarters of expanding adjusted EBITDA margins, the company has established a consistent track record of performance.

The raised guidance for 2025 and reaffirmed long-term targets for 2028 reflect management’s confidence in Zeta’s growth trajectory and competitive positioning. As the company continues to expand its customer base and increase ARPU, while simultaneously improving financial efficiency, it appears well-positioned to capitalize on the growing demand for integrated marketing technology solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.