Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Ziff Davis Inc (NASDAQ:ZD) presented its second quarter 2025 results on August 6, 2025, revealing accelerated revenue growth and a return to organic growth after several challenging quarters. The digital media and internet company, which operates across technology, gaming, health, connectivity, and cybersecurity segments, saw its stock rise 3.96% to close at $30.99 on the day of the announcement, suggesting positive market reception to the results.

The Q2 performance marks a significant improvement from the company’s Q1 2025 results, where Ziff Davis missed earnings expectations with an adjusted EPS of $1.14 against a forecast of $1.28. The latest quarterly performance indicates the company may be turning a corner after experiencing stock price pressure, with shares having fallen over 42% in the six months prior to Q1 earnings.

Quarterly Performance Highlights

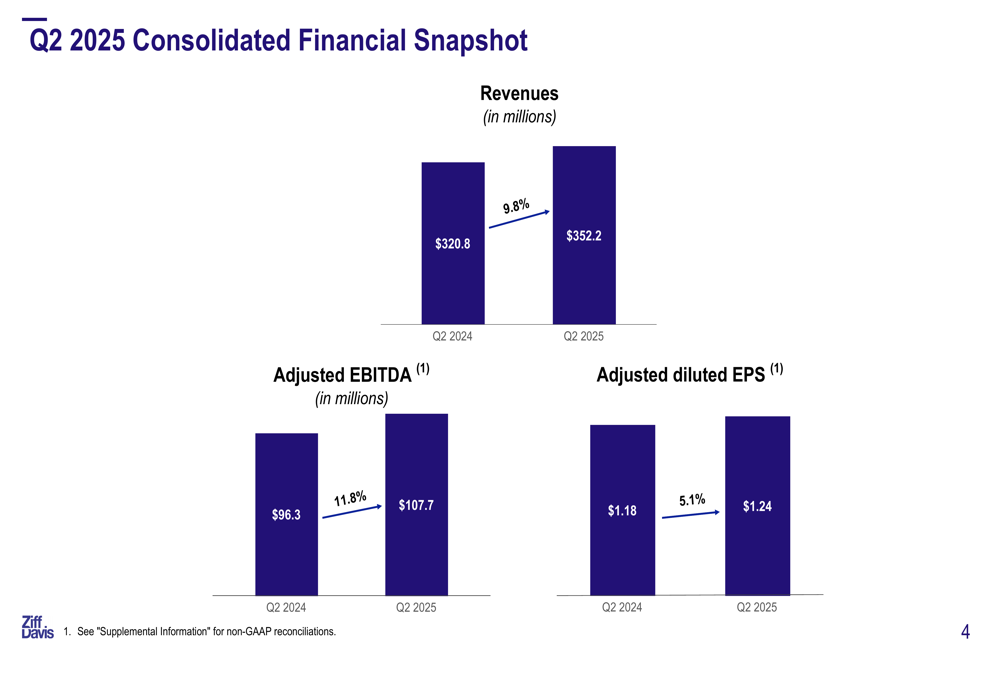

Ziff Davis reported substantial growth across key financial metrics for Q2 2025. Revenue increased by 9.8% year-over-year to $352.2 million, up from $320.8 million in Q2 2024. Adjusted EBITDA grew by 11.8% to $107.7 million, while adjusted diluted EPS rose 5.1% to $1.24 from $1.18 in the same period last year.

As shown in the following consolidated financial snapshot from the company’s presentation:

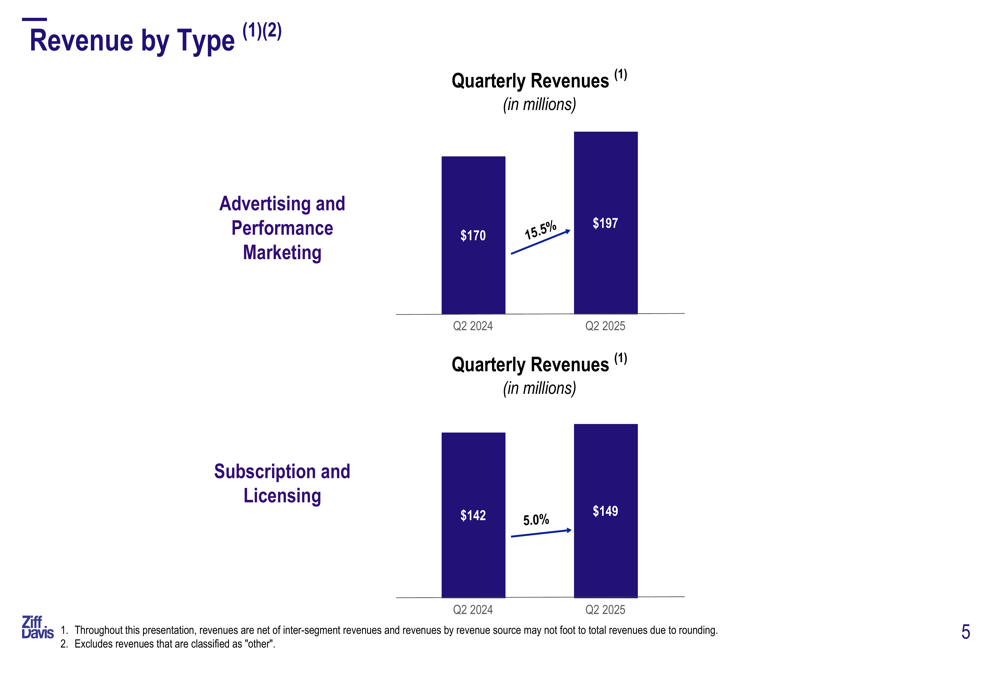

The company’s revenue growth was primarily driven by its Advertising and Performance Marketing segment, which saw a 15.5% increase to $197 million compared to $170 million in Q2 2024. The Subscription and Licensing segment also contributed positively with a 5.0% increase to $149 million from $142 million in the prior year period.

The following chart illustrates this revenue breakdown by type:

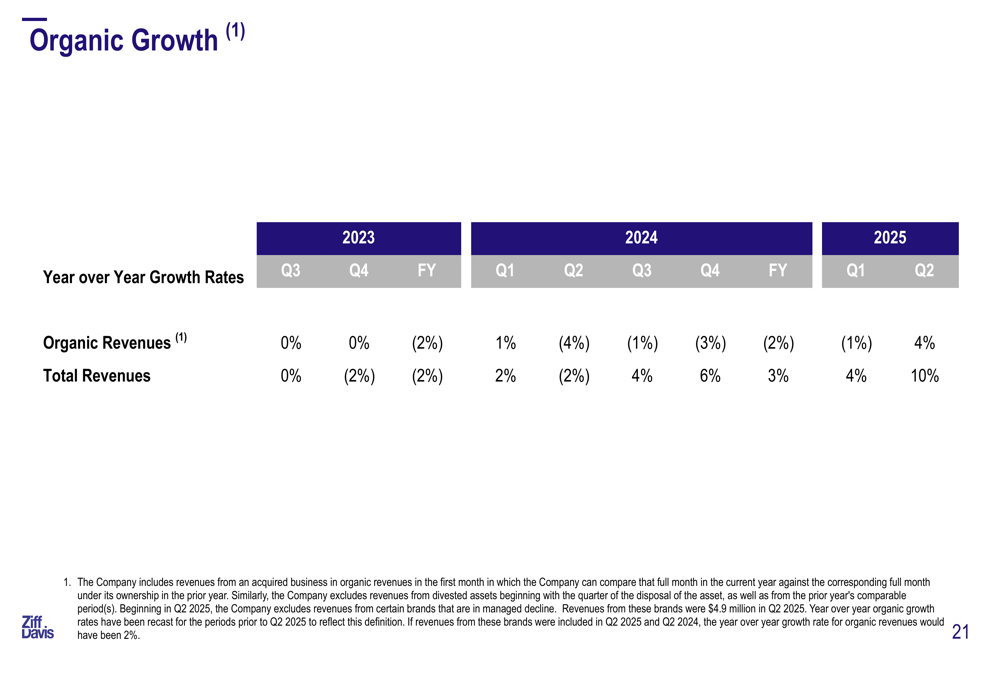

Notably, Ziff Davis achieved 4% organic revenue growth in Q2 2025, marking a significant turnaround from the -4% organic growth experienced in Q2 2024. This improvement suggests the company’s strategic initiatives are gaining traction after several quarters of flat or negative organic growth.

The organic growth trend is illustrated in this chart from the presentation:

Segment Performance Analysis

Ziff Davis operates across five business segments, with most showing strong performance in Q2 2025:

The Health & Wellness segment was the largest contributor to revenue, growing 15.7% to $99.5 million with an adjusted EBITDA margin of 33.6%. This segment benefited from increased advertising and performance marketing revenue, which rose to $82.5 million.

The Technology & Shopping segment saw revenue increase by 11.3% to $80.8 million, although its adjusted EBITDA margin decreased slightly to 22.6% from 23.9% in the prior year.

The Connectivity segment demonstrated strong growth with revenue up 14.2% to $57.4 million and adjusted EBITDA increasing by 12.4%, maintaining a robust margin of 47.3%.

The Gaming & Entertainment segment achieved 7.5% revenue growth to $46.2 million, with an impressive improvement in adjusted EBITDA margin from 28.6% to 32.9%.

The only segment showing a slight decline was Cybersecurity & Martech, where revenue decreased by 0.9% to $68.3 million. However, this segment still improved its adjusted EBITDA margin from 32.1% to 34.2%.

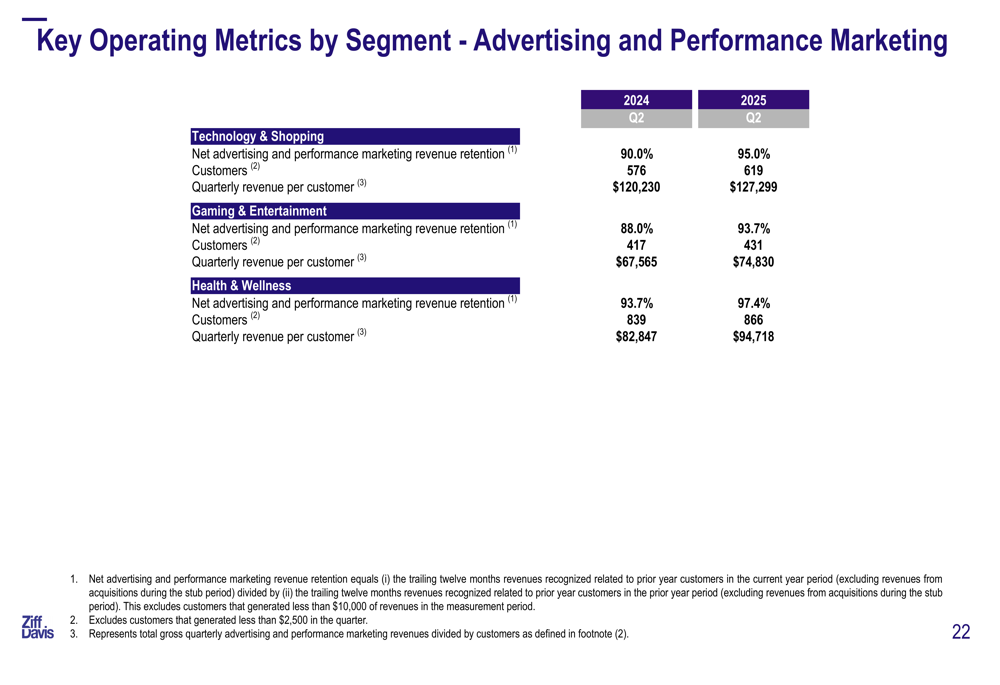

The company’s advertising and performance marketing metrics showed improvement across segments, with increased customer counts and higher revenue per customer:

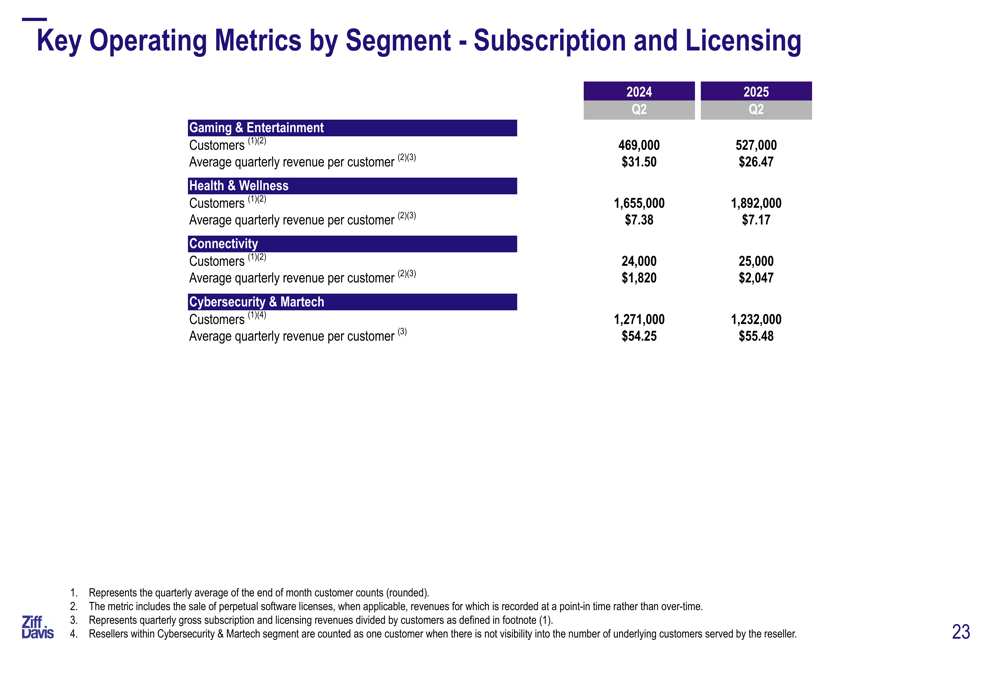

Similarly, the subscription and licensing business showed growth in customer numbers across most segments:

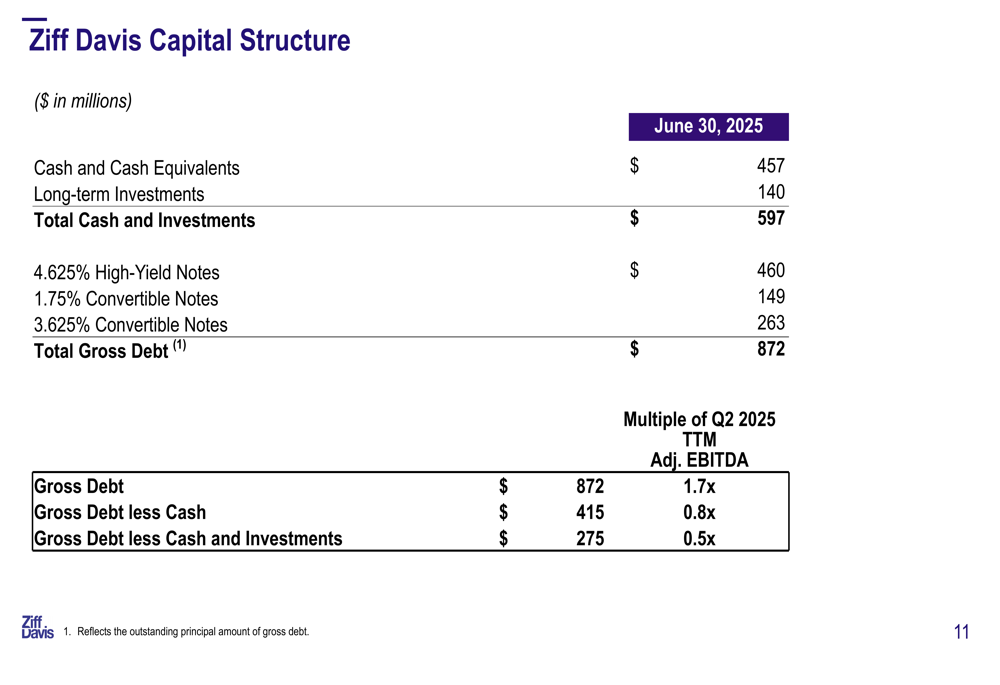

Financial Position and Capital Structure

Ziff Davis maintains a strong financial position with $457 million in cash and cash equivalents and $140 million in long-term investments, totaling $597 million in available capital. The company’s total gross debt stands at $872 million, resulting in a net debt position of $275 million when accounting for cash and investments.

The company’s leverage ratio remains conservative at 0.5x adjusted EBITDA (when considering gross debt less cash and investments), providing significant financial flexibility for potential acquisitions or share repurchases.

The following chart details the company’s capital structure:

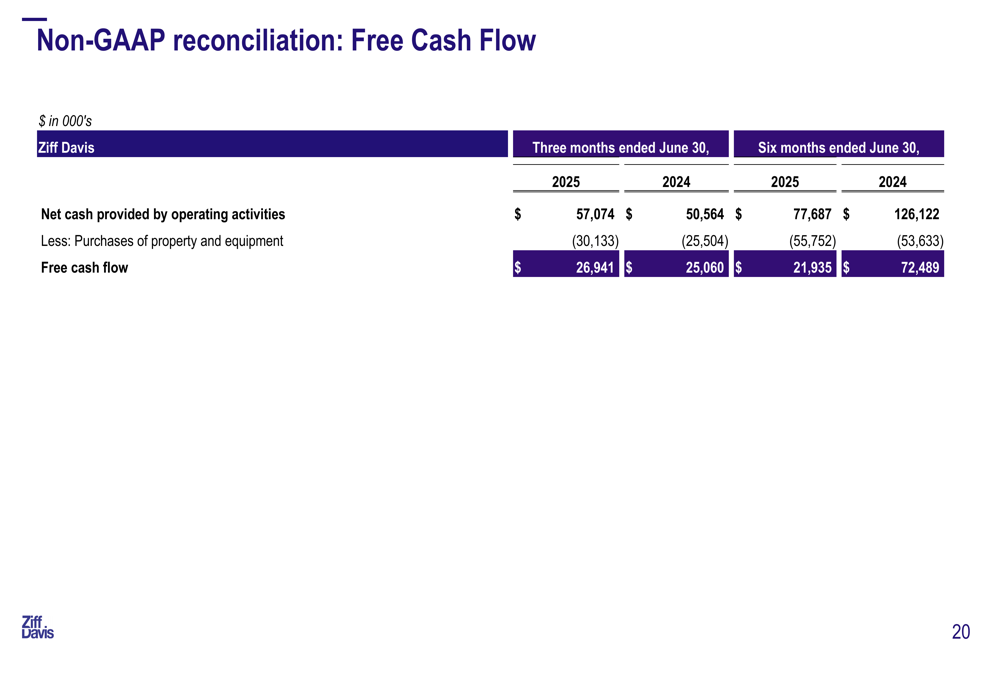

Free cash flow for the quarter was $26.9 million, a slight increase from $25.1 million in Q2 2024. However, for the six months ended June 30, 2025, free cash flow decreased to $21.9 million from $72.5 million in the prior year period, primarily due to changes in working capital.

As shown in the free cash flow reconciliation:

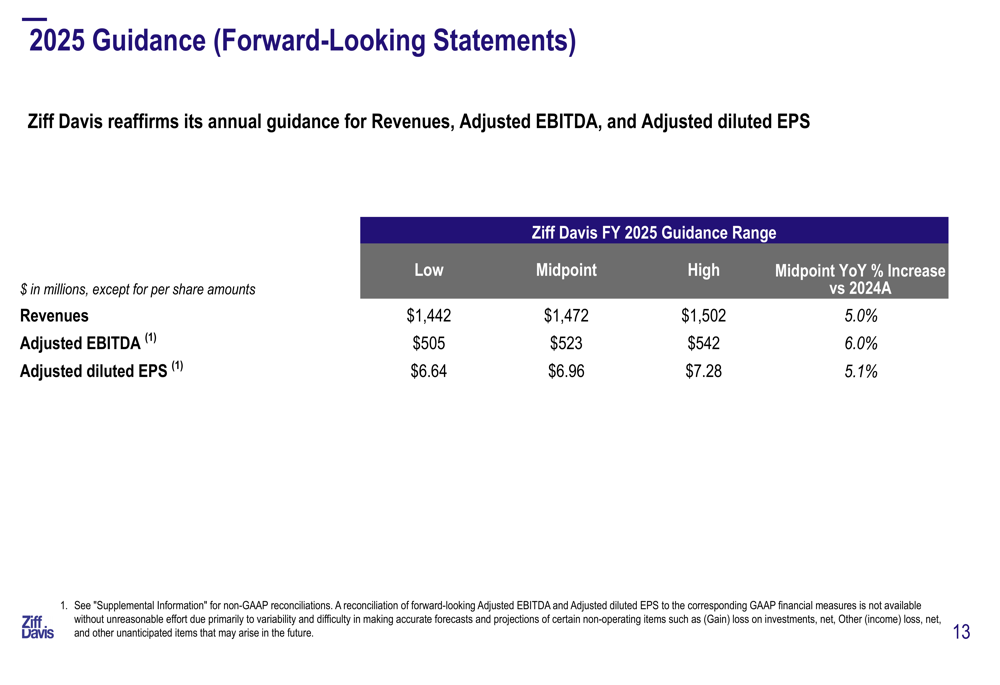

Forward-Looking Statements and Guidance

Ziff Davis reaffirmed its full-year 2025 guidance, projecting revenues between $1,442 million and $1,502 million (5.0% year-over-year growth at the midpoint), adjusted EBITDA between $505 million and $542 million (6.0% growth), and adjusted diluted EPS between $6.64 and $7.28 (5.1% growth).

The maintained guidance suggests management confidence in the company’s ability to sustain the improved performance seen in Q2 throughout the remainder of the year, despite the previous challenges in Q1.

The detailed guidance is presented in the following table:

The company’s return to organic growth in Q2 2025 after several quarters of flat or negative performance provides a positive signal for future quarters. With strong performance across most segments and improving customer metrics, Ziff Davis appears to be executing effectively on its growth strategy.

The solid balance sheet with low leverage also positions the company well for potential strategic acquisitions to further enhance its portfolio of digital properties and services, continuing the "nice M&A cadence" that CEO Vivek Shah referenced during the Q1 earnings call.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.