Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Zoom Video Communications Inc (NASDAQ:ZM) presented its Q1 FY26 earnings results on May 21, 2025, showcasing modest overall growth while highlighting accelerating enterprise segment performance and significant AI adoption. The company’s stock rose 1.13% to $83.20 in after-hours trading, following a 1.22% decline during regular trading hours.

The videoconferencing pioneer continues its strategic transformation from a pandemic darling to an integrated workplace platform, with particular emphasis on AI-powered solutions and enterprise customer expansion. This quarter’s results demonstrate Zoom’s ability to maintain steady growth despite the challenging post-pandemic normalization period.

Quarterly Performance Highlights

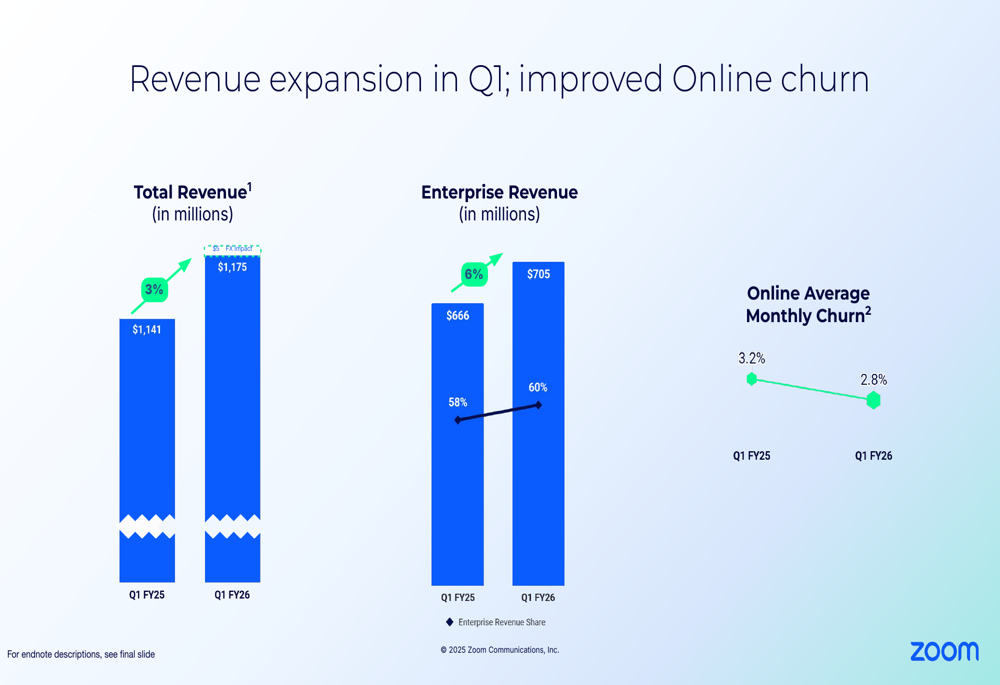

Zoom reported Q1 FY26 total revenue of $1,175 million, representing a 3% year-over-year increase. The enterprise segment continued to outperform, with revenue reaching $705 million, up 6% year-over-year and now accounting for 60% of total revenue.

As shown in the following revenue and churn metrics:

The company also demonstrated improved customer retention, with online average monthly churn decreasing from 3.2% in Q1 FY25 to 2.8% in Q1 FY26. This improvement reflects Zoom’s efforts to enhance product value and customer experience.

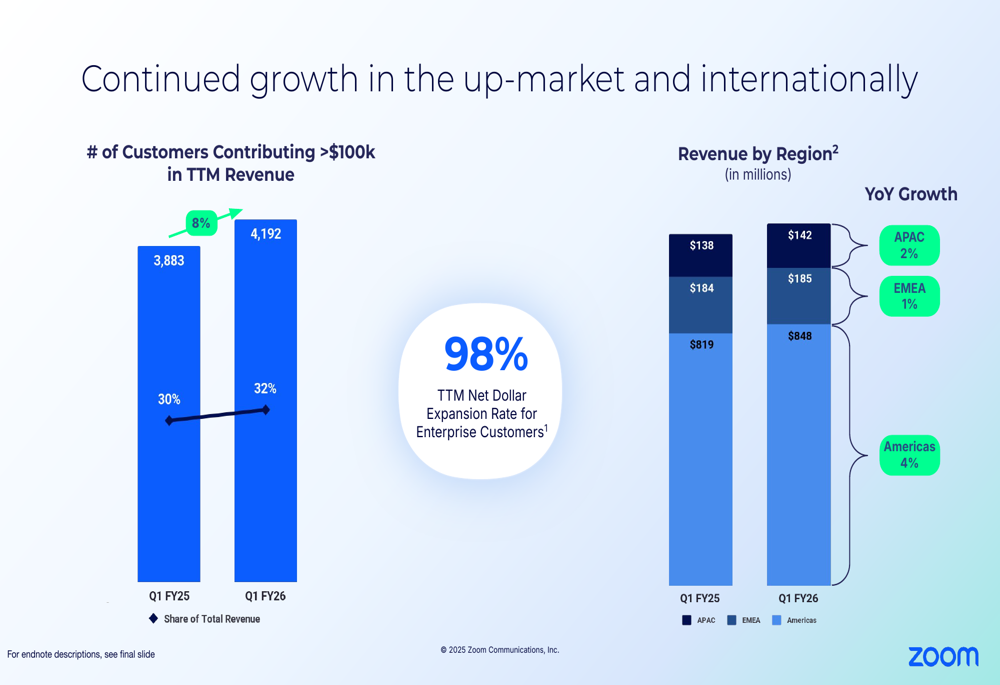

Zoom’s focus on larger customers continues to yield results, with 4,192 customers contributing more than $100,000 in trailing twelve-month revenue, an 8% increase year-over-year. These high-value customers now represent 32% of total trailing twelve-month revenue.

As illustrated in this breakdown of customer growth and international performance:

From a regional perspective, Americas revenue grew 4% year-over-year to $848 million, while EMEA and APAC regions showed more modest growth of 1% and 2%, reaching $185 million and $142 million respectively.

AI Innovation and Product Strategy

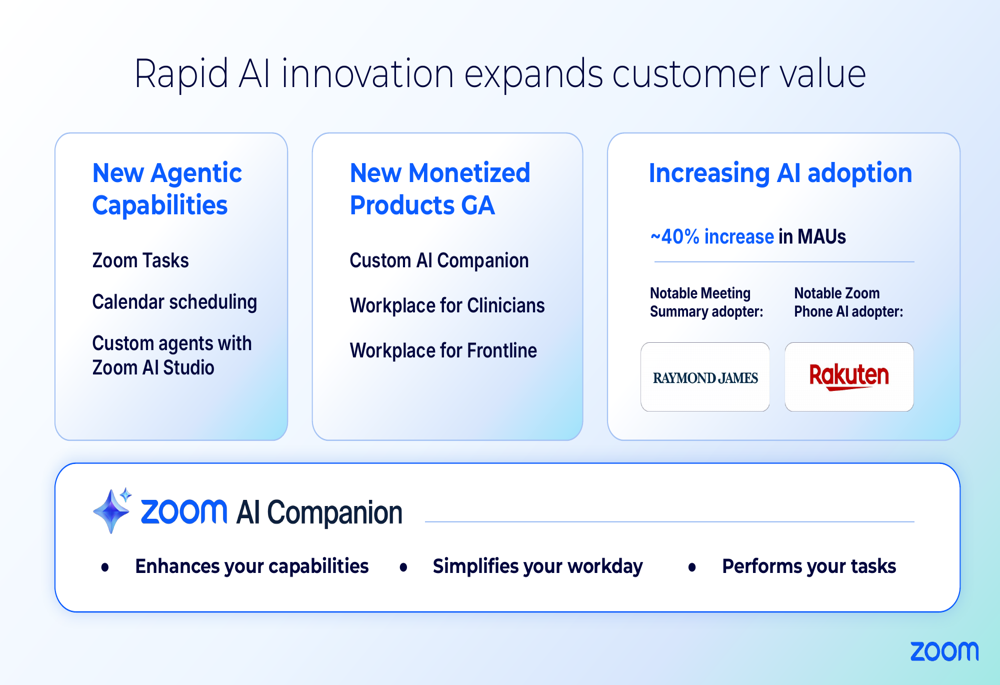

Zoom’s strategic focus on AI innovation was a central theme of the presentation, with the company highlighting new agentic capabilities and monetized AI products. The company reported a 40% increase in monthly active users for its AI features, demonstrating strong customer adoption.

The following slide details Zoom’s AI innovation strategy and key product developments:

New AI capabilities include Zoom Tasks, Calendar Scheduling, and Custom agents with Zoom AI Studio. The company has also launched several monetized AI products, including Custom AI Companion, Workplace for Clinicians, and Workplace for Frontline (NYSE:FRO).

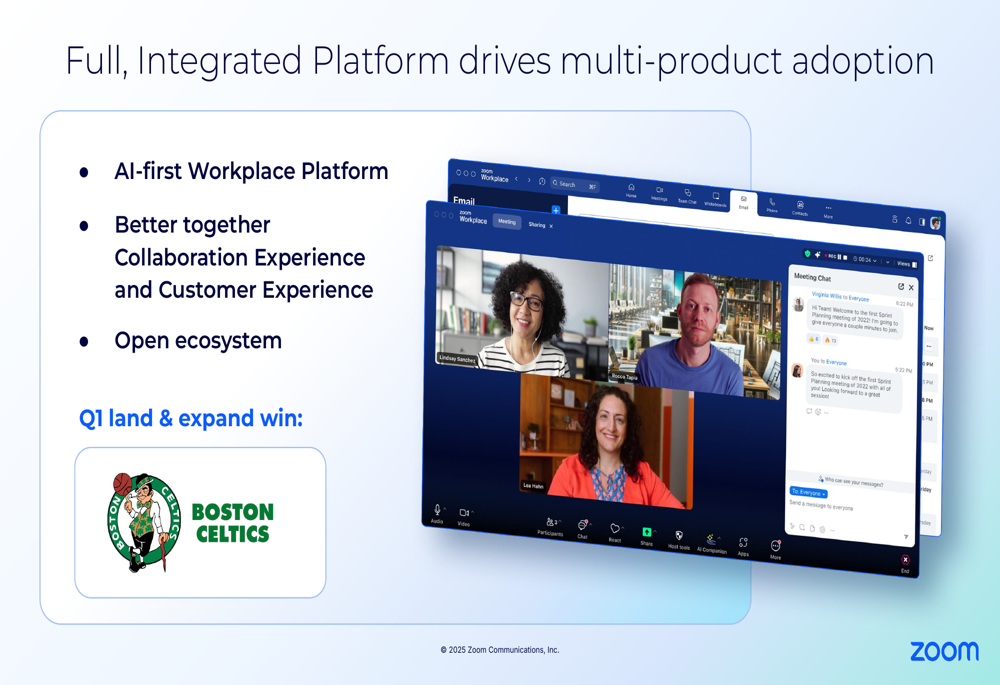

Zoom’s integrated platform approach aims to drive multi-product adoption among customers. The presentation highlighted a Q1 land and expand win with the Boston Celtics, showcasing the company’s ability to cross-sell additional products to existing customers.

As shown in this overview of Zoom’s integrated platform strategy:

Department-Specific Growth

Particularly impressive growth was reported in Zoom’s department-specific solutions. The Contact Center customer base increased 65% year-over-year, with Zoom Virtual Agent securing its largest deal to date. Revenue Accelerator licenses grew 72% year-over-year, while Workvivo customers more than doubled with 106% year-over-year growth.

The following slide illustrates the strong performance across department-specific solutions:

Notable customer wins in Q1 included Mimecast (NASDAQ:MIME) for Customer Experience, Goosehead Insurance for Revenue Accelerator, and the Boston Celtics for Workvivo. The company also announced Meta (NASDAQ:META) as a migration partner, potentially opening new customer acquisition channels.

Zoom is also strengthening its go-to-market strategy with the appointment of Kim Storin as the new Chief Marketing Officer and by expanding channel partnerships, including a new strategic partnership with Bell.

Financial Analysis and Outlook

Zoom delivered solid profitability with Q1 FY26 GAAP operating income at 20.6% of revenue and non-GAAP operating income at 39.8%. GAAP diluted EPS grew 17% year-over-year to $0.81, while non-GAAP diluted EPS increased 6% to $1.43.

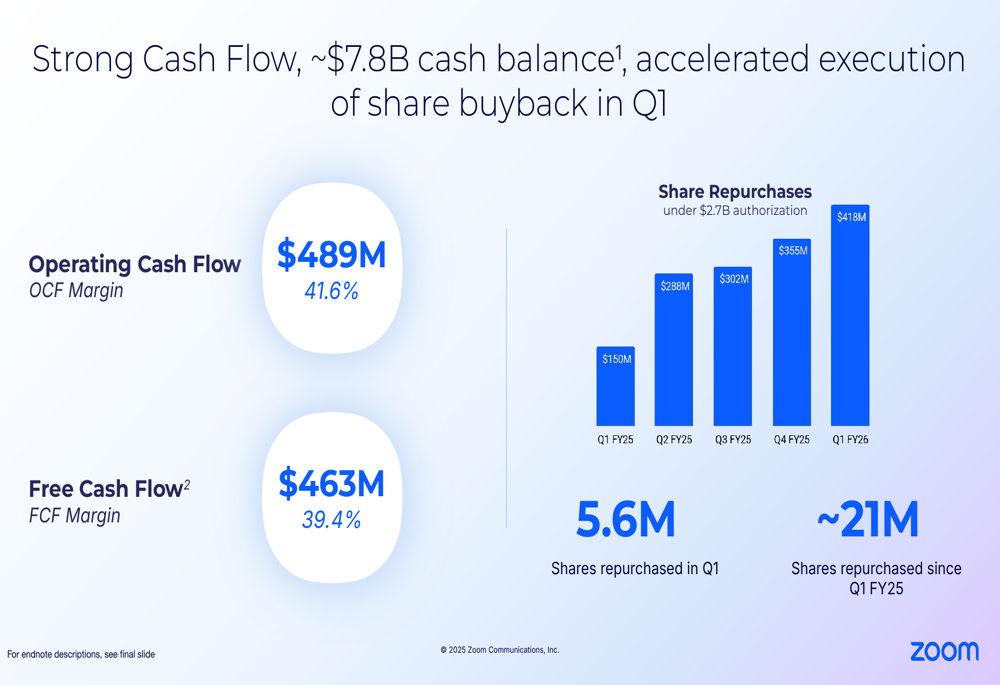

The company generated robust free cash flow of $463 million, representing a 39.4% free cash flow margin. This strong cash generation supported an aggressive share repurchase program, with $418 million used to buy back 5.6 million shares during Q1 FY26.

As illustrated in this cash flow and share repurchase overview:

Forward-looking indicators showed positive momentum, with total remaining performance obligations (RPO) reaching $3,877 million, up 6% year-over-year. Current RPO grew 8%, suggesting healthy near-term revenue visibility.

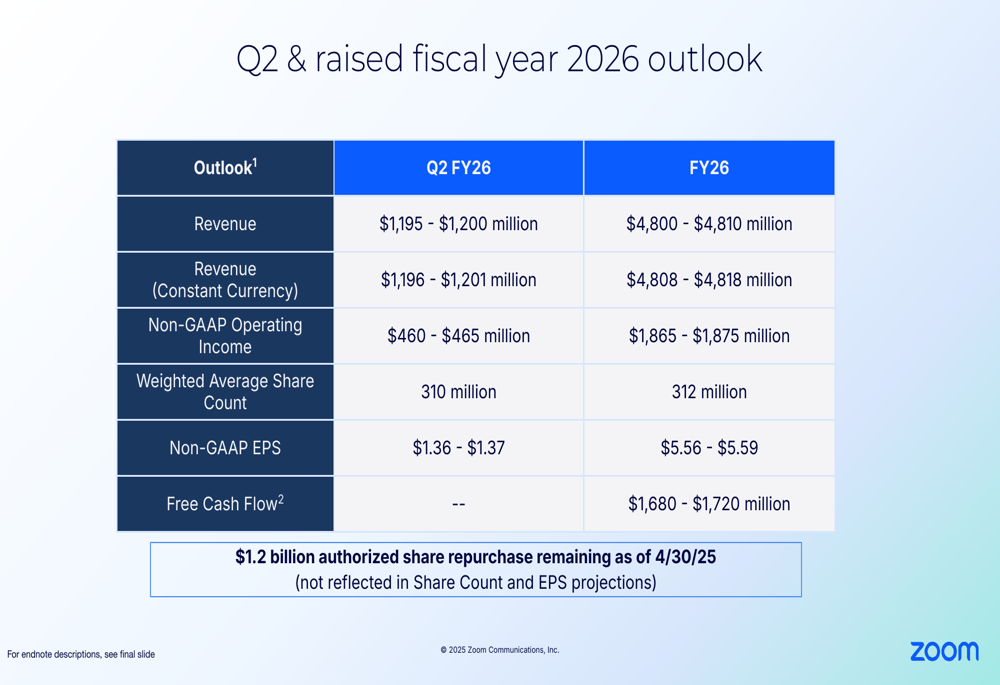

Based on these strong results, Zoom raised its fiscal year 2026 outlook. The company now projects full-year revenue between $4,800 million and $4,810 million, representing approximately 3% growth. Non-GAAP operating income is expected to be between $1,865 million and $1,875 million, with non-GAAP EPS projected at $5.56 to $5.59.

The following guidance overview details Zoom’s updated outlook:

For Q2 FY26, Zoom expects revenue between $1,195 million and $1,200 million, with non-GAAP operating income of $460 million to $465 million and non-GAAP EPS of $1.36 to $1.37.

The company continues to prioritize shareholder returns through its share repurchase program, with $1.2 billion remaining in its authorized repurchase capacity as of April 30, 2025.

Zoom’s Q1 FY26 results demonstrate the company’s successful execution of its strategic priorities, with AI innovation, enterprise customer growth, and department-specific solutions driving performance. While overall revenue growth remains modest, the raised full-year outlook suggests management’s confidence in accelerating momentum through the remainder of fiscal 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.