Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Zymeworks Inc . (NASDAQ:ZYME) presented its corporate strategy and pipeline developments in May 2025, highlighting the company’s focus on multifunctional therapeutics for cancer, autoimmune, and inflammatory diseases. Despite reporting a net loss of $122.7 million for fiscal year 2024 and only marginal revenue growth to $76.3 million, Zymeworks is advancing multiple clinical and preclinical candidates while maintaining a strong cash position of approximately $324 million.

The biopharmaceutical company, currently valued at around $902 million, saw its stock close at $11.34 on May 8, 2025, near its fair value according to analysts, who have set price targets ranging from $12 to $30. The presentation comes at a critical time for Zymeworks as it transitions from research and development to commercialization with its first FDA-approved drug.

Pipeline Development

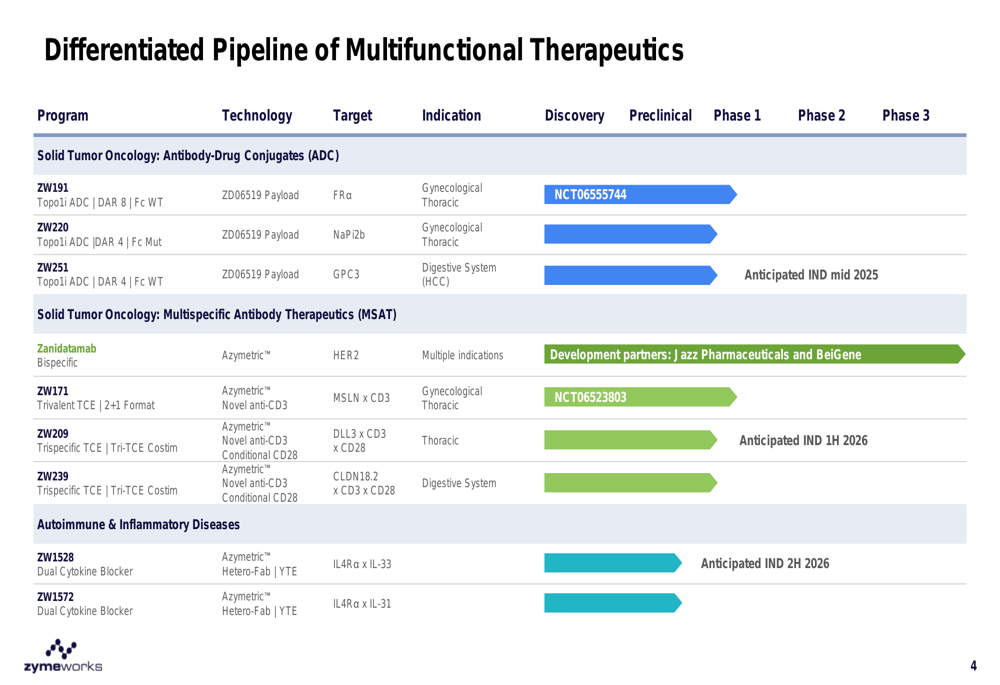

Zymeworks has built a diverse pipeline of multifunctional therapeutics spanning oncology and autoimmune/inflammatory diseases. The company’s portfolio includes six wholly-owned candidates across multiple modalities, with two assets already in Phase 1 clinical trials.

As shown in the following comprehensive pipeline overview, Zymeworks is developing antibody-drug conjugates (ADCs) and multispecific antibody therapeutics (MSATs) targeting various indications:

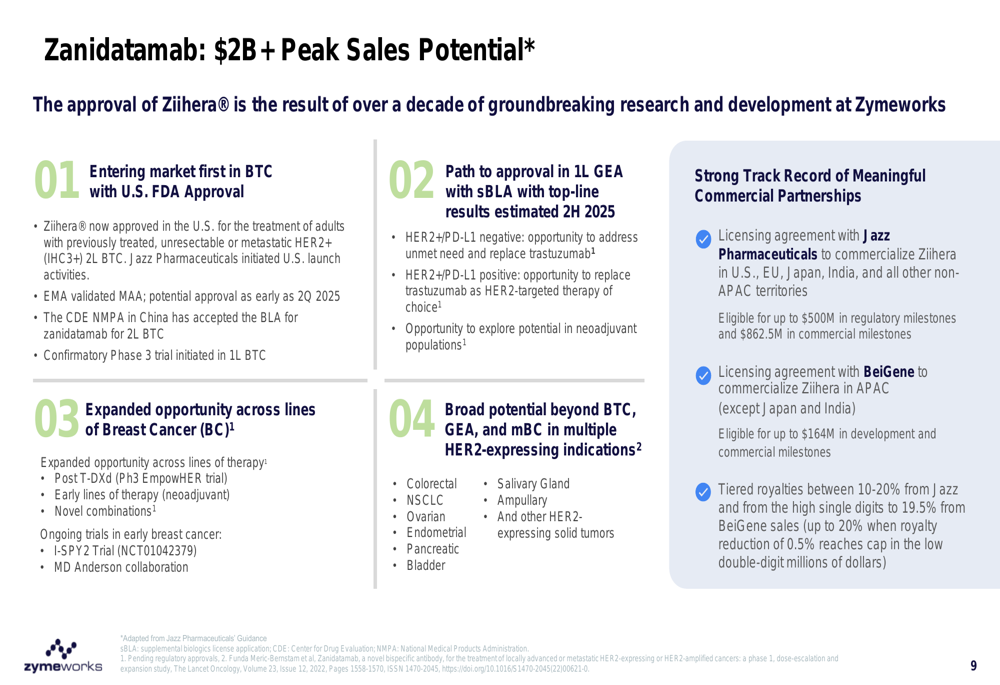

The company’s lead asset, Zanidatamab (Ziihera®), received FDA approval in November 2024 for previously treated, unresectable or metastatic HER2-positive (IHC3+) biliary tract cancer. This milestone represents the first internally developed drug to reach commercialization for Zymeworks, with Jazz Pharmaceuticals (NASDAQ:JAZZ) handling the U.S. launch activities.

"We remain focused on advancing our next generation of wholly owned therapeutics," said Leonie Patterson, CFO, during the recent earnings call, emphasizing the company’s commitment to pipeline progression despite financial challenges.

Commercial Opportunities

Zanidatamab represents a significant commercial opportunity for Zymeworks, with potential peak sales exceeding $2 billion across multiple indications. The company has secured valuable partnerships with Jazz Pharmaceuticals and BeiGene (NASDAQ:ONC) to commercialize the drug globally.

The following slide details the commercial potential and partnership structure for Zanidatamab:

Under these agreements, Zymeworks is eligible to receive up to $500 million in regulatory milestones and $862.5 million in commercial milestones from Jazz Pharmaceuticals, plus tiered royalties between 10-20%. The BeiGene partnership covers Asia-Pacific territories (excluding Japan and India) and includes up to $164 million in development and commercial milestones, with royalties ranging from high single digits to 19.5%.

Beyond biliary tract cancer, Zanidatamab is being evaluated in gastroesophageal adenocarcinoma (GEA), with top-line Phase 3 results expected in the second half of 2025. Additional opportunities in breast cancer and other HER2-expressing tumors could further expand the drug’s market potential.

Key Clinical Assets

Zymeworks is advancing several wholly-owned candidates through clinical development, with ZW171 and ZW191 currently in Phase 1 trials.

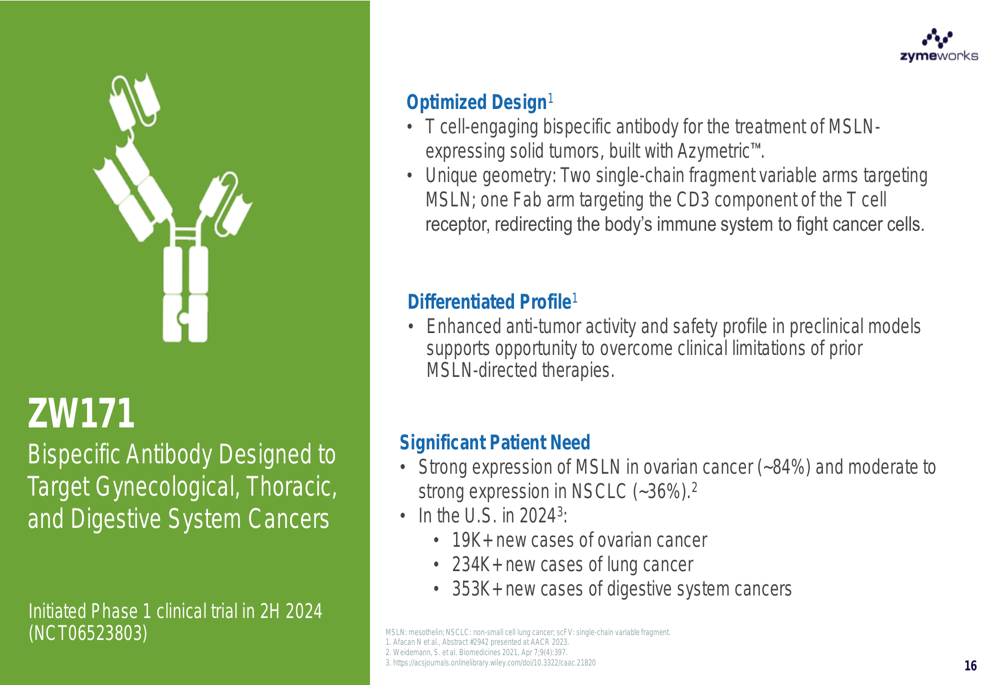

ZW171 is a bispecific antibody targeting mesothelin-expressing solid tumors, including ovarian cancer and non-small cell lung cancer. The molecule’s design aims to overcome limitations of previous mesothelin-directed therapies:

The global Phase 1 study for ZW171 (NCT06523803) is currently enrolling approximately 160 patients, with dose escalation followed by expansion cohorts in ovarian cancer, NSCLC, and a basket cohort of other mesothelin-expressing tumors.

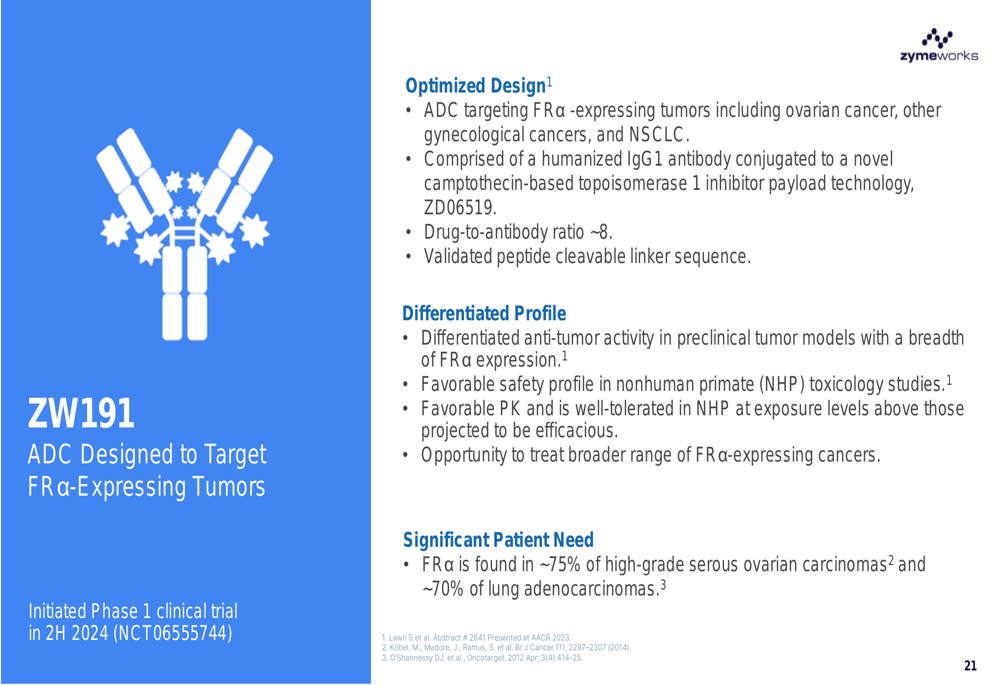

Similarly, ZW191 is an antibody-drug conjugate targeting folate receptor alpha (FRα)-expressing tumors:

ZW191 utilizes Zymeworks’ proprietary topoisomerase inhibitor payload technology (ZD06519) and is designed to target a broad range of FRα-expressing cancers, including ovarian, endometrial, and non-small cell lung cancer. The Phase 1 study (NCT06555744) is enrolling approximately 145 patients.

Technology Platforms

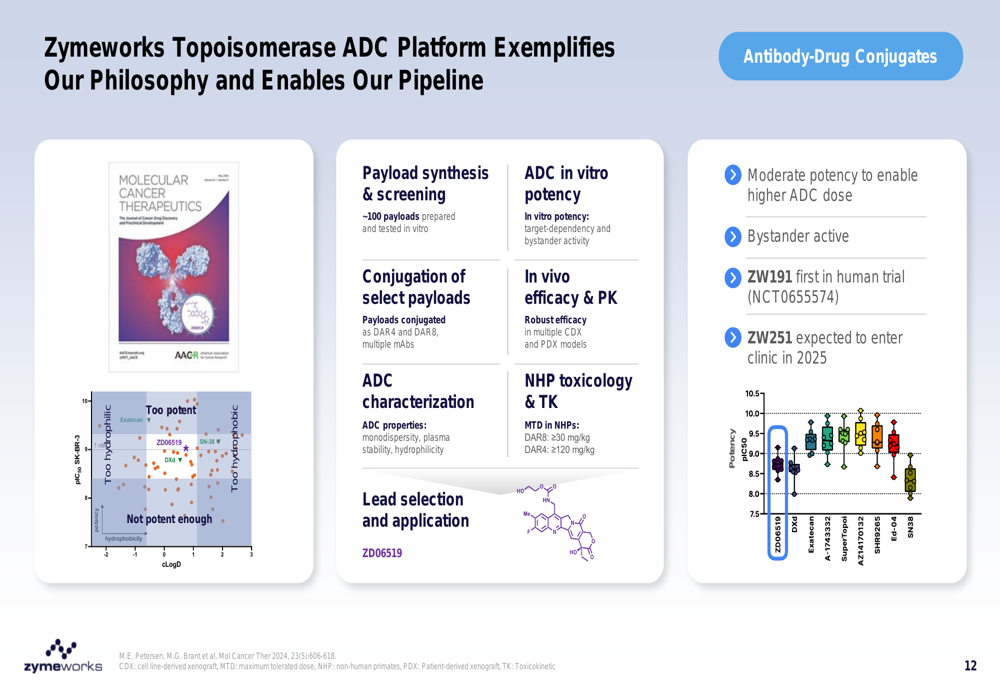

Underpinning Zymeworks’ pipeline is its proprietary technology platforms, including the Azymetric™ platform for multispecific antibodies and a novel topoisomerase inhibitor ADC platform.

The following slide details the company’s ADC technology:

This platform has enabled the development of multiple clinical candidates, including ZW191 and ZW251, with the latter expected to enter clinical trials in 2025 for hepatocellular carcinoma. The technology offers several advantages, including moderate potency to enable higher ADC dosing and bystander activity to target heterogeneous tumors.

Financial Position and Outlook

Despite the promising pipeline, Zymeworks continues to face financial challenges. The company reported a net loss of $122.7 million for fiscal year 2024, or $1.62 per diluted share, with revenue increasing only marginally to $76.3 million from $76.0 million in 2023.

However, the company maintains a strong cash position of $324.2 million as of December 31, 2024, which is expected to sustain operations into the second half of 2027. This runway provides Zymeworks with flexibility to advance its pipeline while pursuing additional partnerships.

The company’s recent accomplishments and near-term milestones highlight its strategic priorities:

Looking ahead, Zymeworks plans to submit an Investigational New Drug (IND) application for ZW251 by mid-2025, with additional INDs for ZW209 and ZW1528 planned for 2026. The company will continue to invest in its T-cell engager and antibody-drug conjugate platforms while exploring opportunities in autoimmune and inflammatory diseases.

Challenges and Opportunities

While Zymeworks has made significant progress with its pipeline and first product approval, the company faces several challenges. Continued net losses could affect investor confidence, and the marginal revenue growth may not meet market expectations. Additionally, the competitive landscape in oncology and biopharmaceuticals remains intense.

However, the approval and commercialization of Zanidatamab represent a significant milestone and potential revenue driver. The company’s strong cash position provides runway for continued pipeline advancement, and its differentiated technology platforms offer opportunities for both internal development and additional partnerships.

As CEO Ken Galbraith emphasized during the earnings call, the company’s goal is to "advance breakthrough therapies, expanding our collaborations and unlocking new opportunities for growth." With multiple clinical programs advancing and a clear strategic focus, Zymeworks is positioning itself to capitalize on its scientific expertise despite current financial challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.