106%+ returns, 97% win rate: A fresh list of AI-picked stock is out NOW

Introduction & Market Context

Marsh McLennan (NYSE:MMC), a global leader in risk, strategy, and people, presented its fourth quarter 2024 investor presentation on January 30, 2025, highlighting what the company described as "another great year." The professional services firm, which operates through four market-leading businesses – Marsh, Guy Carpenter, Mercer, and Oliver Wyman – reported total revenue of $24.5 billion for 2024, maintaining its position as a dominant player in insurance brokerage and consulting services.

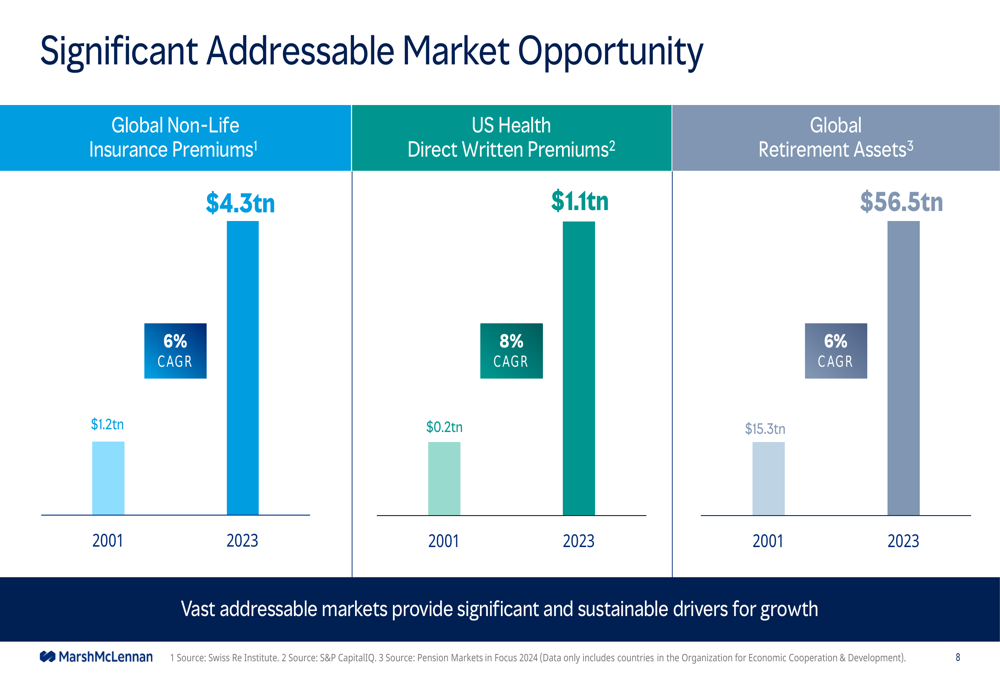

The company operates in a favorable market environment with significant addressable opportunities. Global non-life insurance premiums reached $4.3 trillion in 2023, growing at a 6% CAGR since 2001. Similarly, U.S. health direct written premiums expanded to $1.1 trillion (8% CAGR since 2001), while global retirement assets grew to $56.5 trillion (6% CAGR since 2001).

As shown in the following chart of addressable market opportunities:

Executive Summary

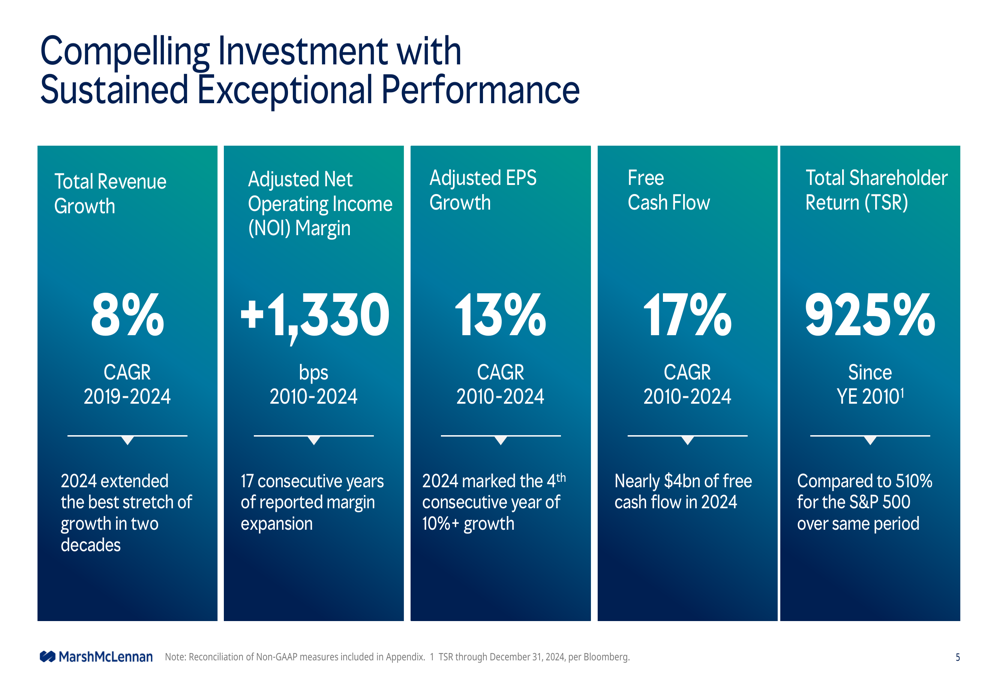

Marsh McLennan delivered exceptional financial performance in 2024, extending what it called "the best stretch of growth in two decades." The company achieved 8% compound annual revenue growth from 2019 to 2024, while expanding its adjusted operating margin by 1,330 basis points since 2010 to reach 26.8% in 2024. This marked the 17th consecutive year of reported margin expansion.

The company's adjusted earnings per share reached $8.80 in 2024, representing a 13% CAGR since 2010 and the fourth consecutive year of double-digit growth. Free cash flow generation was particularly strong at nearly $4 billion in 2024, translating to a 16% FCF margin and a 17% CAGR since 2010.

These performance metrics are illustrated in the following slide:

The company's diversified business model spans both services and geographies. By business unit, revenue distribution was: Marsh (52%), Mercer (24%), Guy Carpenter (10%), and Oliver Wyman (14%). Geographically, the U.S. accounted for 48% of revenue, followed by EMEA (33%), Asia Pacific (11%), Canada (4%), and Latin America & Caribbean (4%).

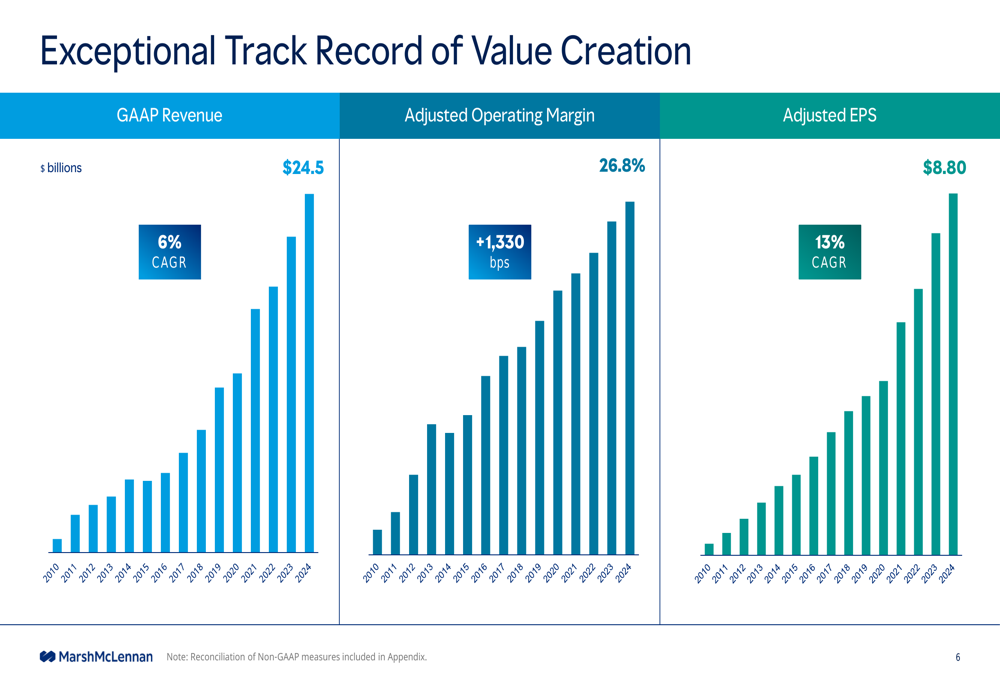

The company's exceptional track record of value creation is clearly demonstrated in these key financial metrics:

Detailed Financial Analysis

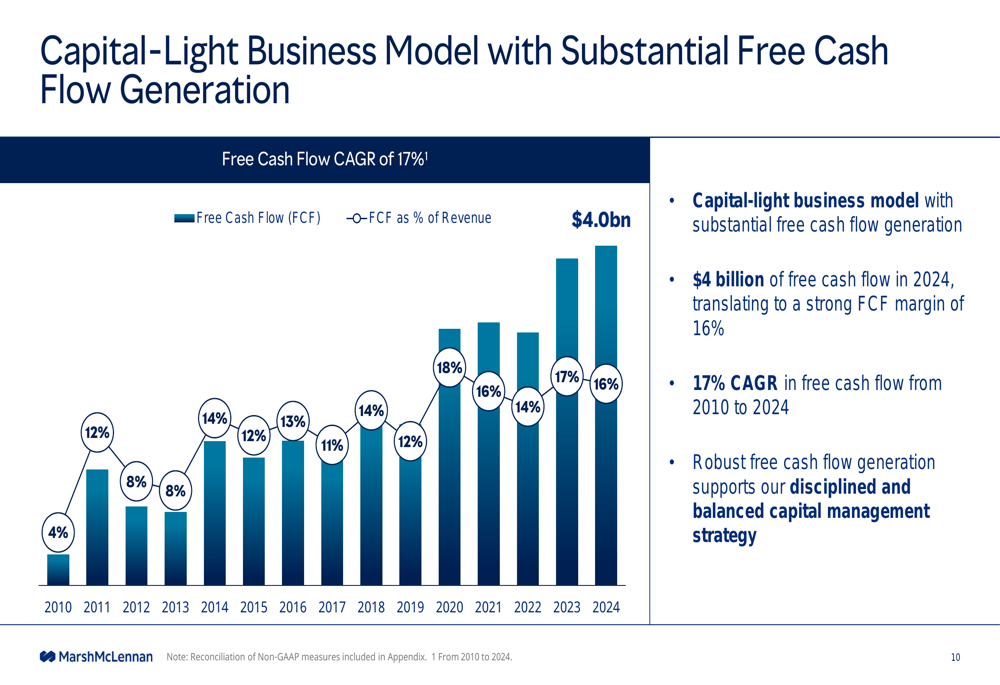

Marsh McLennan's capital-light business model continues to generate substantial free cash flow, reaching nearly $4 billion in 2024. This represents a 17% compound annual growth rate since 2010 and provides significant flexibility for capital allocation.

The company's operating leverage has been consistent over time, with underlying revenue growth outpacing underlying adjusted expense growth. This has fueled margin expansion, with "other operating expenses as percentage of revenue" decreasing from 24.2% in 2014 to 19.0% in 2024, representing 520 basis points of improvement.

The company's free cash flow growth is illustrated in the following chart:

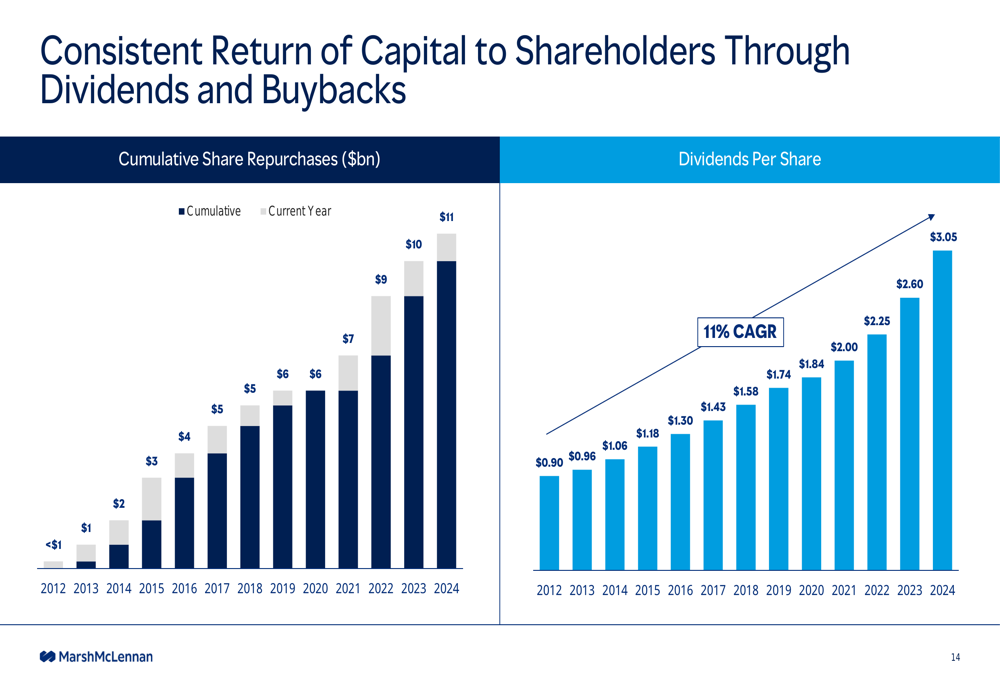

Marsh McLennan has maintained a balanced and disciplined capital management strategy, focusing on five core components: balancing efficiency and flexibility of capital structure, driving growth through organic investment, targeting dividend increases and share count reduction each year, deploying capital for acquisitions, and returning excess capital through share repurchases.

This approach has resulted in consistent returns to shareholders. Dividends per share increased from $0.90 in 2012 to $3.05 in 2024, representing an 11% CAGR. Cumulative share repurchases grew from less than $1 billion in 2012 to $11 billion by 2024.

The company's commitment to shareholder returns is shown in the following slide:

Strategic Initiatives

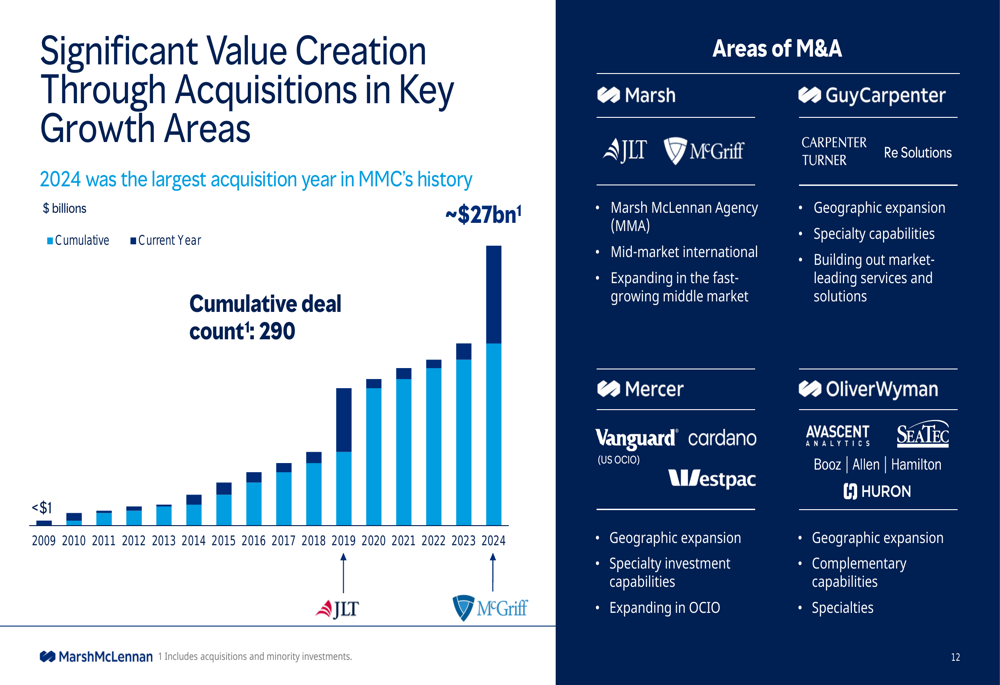

Acquisitions have been a cornerstone of Marsh McLennan's growth strategy. The company reported that 2024 was its largest acquisition year in history, with a cumulative deal count of 290 and total value of approximately $27 billion. These acquisitions have been strategically focused on key growth areas across all four business units.

The Marsh McLennan Agency (MMA) has been central to the company's M&A strategy, growing to approximately $5 billion in revenue. The recent addition of McGriff to MMA is expected to further boost its revenue and capabilities in the middle market segment.

The company's acquisition strategy is illustrated in this chart:

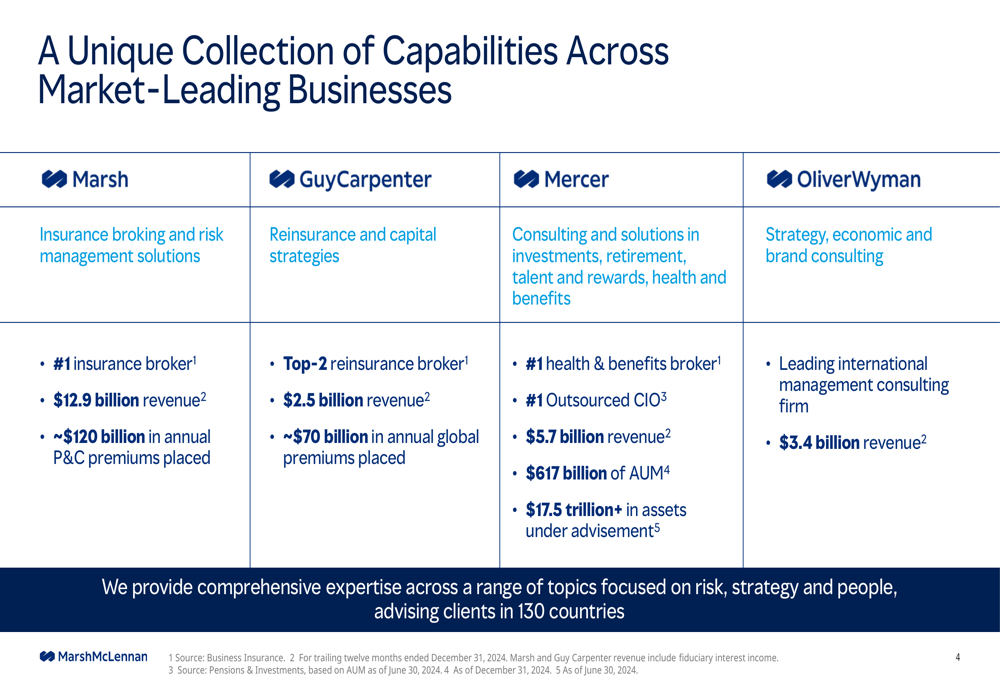

Marsh McLennan has positioned itself as a unique collection of market-leading businesses, each with significant scale and leadership positions:

- Marsh: #1 insurance broker with $12.9 billion in revenue and approximately $120 billion in annual P&C premiums placed

- Guy Carpenter: Top-2 reinsurance broker with $2.5 billion in revenue and approximately $70 billion in annual global premiums placed

- Mercer: #1 health & benefits broker and #1 Outsourced CIO with $5.7 billion in revenue, $617 billion of AUM, and over $17.5 trillion in assets under advisement

- Oliver Wyman: Leading international management consulting firm with $3.4 billion in revenue

This unique collection of businesses is detailed in the following slide:

The company has also emphasized innovation as a driver of growth, developing solutions that deliver meaningful client impact. Examples include Sentrisk™ and Blue[i] from Marsh, CatStop+ from Guy Carpenter, and various specialized offerings from Mercer and Oliver Wyman.

Forward-Looking Statements

Looking ahead, Marsh McLennan expressed confidence in its ability to deliver continued outstanding performance. The company highlighted several factors supporting this outlook:

1. Solid demand for advice and solutions driven by macro complexity

2. Innovation to serve clients in new and emerging areas of focus

3. Favorable business mix shift towards higher growth areas

4. Further upside from collaboration across businesses

5. Consistent investments in talent

Management indicated that the company's outlook contemplates continued revenue growth and margin expansion. The company also noted significant opportunities for further margin improvement through enhanced efficiency, including boosting service delivery in centers of excellence, leveraging horizontal capabilities, and increasing the use of technology and automation.

Marsh McLennan's capital-light business model, combined with its strong recurring revenue base and proven track record as a disciplined acquirer, positions the company well for continued success across economic cycles. With vast addressable markets providing significant and sustainable growth drivers, the company appears well-positioned to build on its 17-year streak of margin expansion and deliver continued value to shareholders.

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.