Nvidia developing new China-specific AI chip, more powerful than H20 - report

The S&P 500 has powered to new heights in 2025, recently closing at a record 6,468. This leg up is driven by a potent combination of upbeat earnings revisions and a blowout second-quarter reporting season. Crucially, the rally is rooted in improving fundamentals rather than pure multiple expansion. Still, market breadth remains narrow, with fewer individual stocks making new highs compared to the index.

Earnings Revisions and Corporate Confidence on the Rise

Earnings estimates are being revised upward at the fastest pace since late 2021, reflecting broad-based optimism. But this isn’t just analyst enthusiasm, companies are lifting their own forward guidance too. The ratio of positive-to-negative guidance has hit a four-year high, especially on near-term forecasts, which has propelled momentum. Full-year 2025 earnings growth is now pegged at 10.3%, with Q3 expected to grow around 8% year over year.

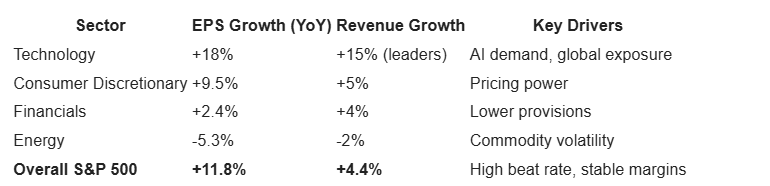

Q2 Earnings: A Blowout Season

With nearly all S&P 500 companies reporting, second-quarter earnings growth landed at 11.8% year over year, nearly triple the original 4% expectation. It marks the third consecutive quarter of double-digit growth. A remarkable 82% of companies beat estimates, one of the highest beat rates on record. Revenue rose 4.4%, led by technology and consumer discretionary. Importantly, margins held firm at 12.1%, defying fears of erosion, thanks to corporate agility in managing costs, adapting supply chains, and passing through price increases.

Tariff Resilience and Currency Tailwinds

U.S. companies have shown resilience to tariffs by passing costs to consumers and optimizing operations. Smaller firms may still face margin pressure if trade measures escalate, but most large-cap exporters have benefited from the dollar’s 12% depreciation, which has added an estimated 2 to 3% to EPS. That said, constant-currency revenue growth has decelerated, exposing a more moderate underlying pace.

Mega-Cap Tech: Still Carrying the Load

The Magnificent 7 delivered 26% EPS growth and beat consensus by 12%. Their 2026 capex forecasts now total $461 billion, driven by intensifying AI infrastructure investments. However, while their estimates have ticked higher, the rest of the S&P 500 has seen modest cuts, reinforcing concentration risks. Tech sector earnings are forecast to grow 16.9% in 2025, a step down from recent years due to tougher comps.

Outlook: Choppiness Ahead, But Upside Intact

The alignment of revisions, corporate guidance, and strong earnings beats has shifted this rally from a multiple-driven one to earnings-led. Third-quarter earnings are expected to grow 8%, with full-year growth at 10.3%. But markets could see choppiness into the Jackson Hole symposium and the September Fed meeting. If Powell doesn’t reinforce the rate-cut narrative, a temporary pullback may emerge.

Still, I maintain my year-end target of 6,500 and continue to see 7,000 as achievable by mid-2026, especially as AI investments transition from cost centers to monetized platforms. Investors should remain diversified beyond mega-caps and watch Fed commentary closely to navigate any near-term volatility.