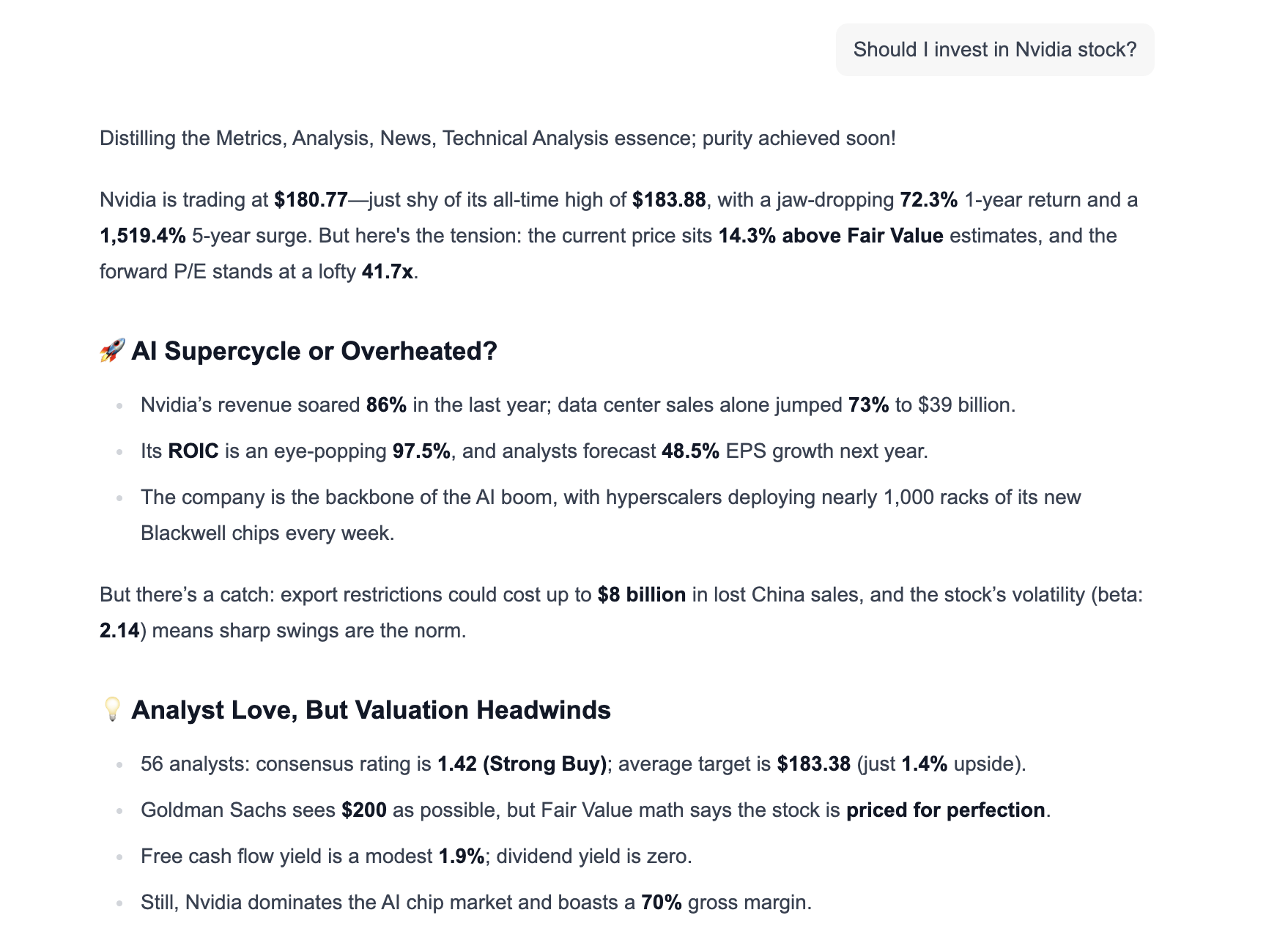

Deere and Tractor Supply shares fall after Trump criticizes farm equipment prices

Investing is tough, especially when dealing with individual company stocks, because risk can shift on a dime and your portfolio could drop 25% in a matter of weeks if you’re not careful.

The hard part about some of these problematic positions is that they’re not obviously bad companies or just overall crazy risks. Instead, there are five big positions that I see routinely needing to be fixed, and I want to point those out here. Almost all of these problems stem from the fact that investors are chasing returns.

Position #1: NVIDIA - The Valuation Concern

You need to understand that buying into a stock or position that’s gone up 100% in the last couple of months is literally the worst time to be jumping into that stock. People have FOMO (fear of missing out) and think that since something’s been going up, it will continue going up. But that is actually the most risky time to jump into something.

The Problem: With a market cap over $4 trillion, NVIDIA’s (NASDAQ:NVDA) price-to-earnings (PE) ratio is seen as dangerously high. Its valuation is fueling concerns about overheating in AI mega caps, and strategists warn of a sharp correction if earnings fail to meet sky-high expectations.

Why It’s Risky Now: NVIDIA’s current price is based entirely on expected future returns. If it doesn’t hit exactly what’s expected or better, this stock could easily tumble. The real challenge lies in the math: for you to double your $1,000 investment to $2,000, the company would need to go from its current $4 trillion valuation to an $8 trillion market cap.

Consider this: in the entire world, there are only 11 companies with valuations over $1 trillion and only three above $3 trillion. While it’s possible that a single company may reach $8 trillion, it’s highly unlikely. Meanwhile, statistically, investors double their money approximately every seven years by investing in the basic S&P 500 - something that has happened like clockwork for over 70 years.

The Bottom Line: If you already hold NVIDIA from previous purchases, it’s not necessarily a bad stock - it’s actually an amazing company. But I’m seeing too many people starting new positions now at its literal all-time high. There are simply many better stocks that could provide better returns in a shorter period.

Making Smarter Investment Decisions with the Right Tools

Before diving into the next position, I want to share a resource that’s been invaluable for my investment research: When you subscribe as an InvestingPro member - now available for less than $9 a month - you get access to ProPicks AI, which uses artificial intelligence to analyze the market and provides a list of top investment opportunities.

What I love about ProPicks AI is that it saves me a tremendous amount of time. Instead of spending hours researching stocks, I can check their picks and make informed decisions in minutes.

Another one of my favorite tools is their Warren AI feature — a Gen AI tool completely directed to financial markets that can massively leverage your investment research.

For this analysis, I straight up asked it whether I should invest in NVIDIA stock. It provided solid pros and cons and ultimately agreed with my earlier assessment: NVIDIA is a global AI powerhouse with world-beating growth, but much of that optimism is already priced in.

As it puts it, "For investors, this is where legend meets lofty expectations - sky-high potential, sky-high risks."

Below’s a screenshot of the AI’s response. Click here to access the fulsome response:

As an Investing Pro member, you don’t only get access to ProPicks AI, but a whole suite of powerful tools. For example, there’s an ideas section where you can examine and copy the strategies of legendary investors like Warren Buffett.

The best part is that Investing.com is running a summer sale of 50% off, and I’ve managed to secure an even better discount for readers - an additional 15% off, but only until the end of August when using this link.

This offer is available for a limited time, so don’t miss out if you’re serious about improving your investment research process.

Position #2: International ETFs - Wrong Timing, Right Idea

The Current Situation: The overall US stock market has been shaky, while international markets have been crushing the US in 2025. The S&P 500 is up around 6-7% this year, while international markets are up 16-18%. This performance has been largely fueled by a weaker US dollar - when the dollar weakens, international stock values increase for US investors. The US dollar index is down 10.7% versus a basket of major global currencies.

The Problem: While six-month performance favors international stocks, the US-based S&P 500 has meaningfully outperformed developed international stocks over three, five, and 10-year periods. What I’m seeing is people selling portions of the S&P 500 or Nasdaq 100 to buy international funds today at their all-time high while they’re beating the US market. This is exactly the wrong time to make this move.

The Better Strategy: Educate yourself on whether international exposure is important for your long-term portfolio. If you decide it is, wait until the scales get back into alignment. Wait until we work through current geopolitical, tariff, and trade issues, then add cheaper-priced international exposure.

Position #3: Urban Air Mobility Speculation - Managing Your Risk Allocation

The Opportunity (SO:FTCE11B): Companies like Joby Aviation (NYSE:JOBY) and Archer Aviation are pioneering the urban air mobility sector, developing electrical vertical takeoff and landing aircraft designed to revolutionize short-distance travel. Both aim to transform 30-90 minute commutes into 10-20 minute flights.

The Promise: These companies have impressive backing:

- Joby Aviation partners with Delta, Toyota (NYSE:TM), Uber (NYSE:UBER), and the Air Force

- Archer works with United Airlines, Stellantis (NYSE:STLA), Enduro, and Palantir (NASDAQ:PLTR)

- Substantial funding: $1.4 billion in cash for Joby and $2 billion total raised by Archer

The Risks:

- Joby burns about $500 million annually

- Archer has no top-line revenue with quarterly losses of about $100 million

- Regulatory uncertainty and FAA compliance questions

- Intense competition from companies like Lilium and Whisk

- Short seller criticism

The Real Problem: What I’m seeing in portfolios isn’t just speculation in one or two companies - it’s speculation in five or 10 companies, representing 30-40% of entire portfolios. More often than not, these speculative plays don’t pan out.

My Recommendation: Keep speculative investments to no more than 10% of your entire portfolio.

Position #4: Crypto-Adjacent Companies - Direct vs. Indirect Exposure

The Landscape: Bitcoin is becoming more valuable and acceptable in our increasingly digital financial world. However, I’m seeing too many clients with excessive exposure to companies like Coinbase (NASDAQ:COIN) and MicroStrategy Incorporated (NASDAQ:MSTR).

The Risks:

- These companies have been propelled by crypto mania but face regulatory and market headwinds.

- MicroStrategy is tethered to Bitcoin and could collapse if crypto prices drop.

- Coinbase is vulnerable to tightening crypto regulations.

My Preference: I prefer Bitcoin itself over companies trying to build strategies around Bitcoin. If I want exposure to crypto-related companies while mitigating risk, I’d rather hold growth-style ETFs like QQQM, SCHG, or VUG. These funds house companies like Coinbase or MicroStrategy, among many other growth companies, so if they do well, I make money. Still, if they perform poorly, it doesn’t decimate my entire portfolio.

Position #5: Excessive Cash and Defensive Holdings - Opportunity Cost

The Context: During the market volatility this year, especially the significant drop in April, people were happy to have portions of their portfolios in stabilized funds like bonds or cash equivalents. The sting of that dip still lingers and should be respected.

The Problem: What I’m seeing in portfolios that are lagging overall is way too much money in defensive areas or excessive cash on the sidelines.

The Missed Opportunity: During that April dip, I advised buying even heavier. Those who followed this advice instead of keeping money on the sidelines have seen monster returns:

- S&P 500 (SPY): From around $500 in April to about $623 in mid-July (20-24% gain)

- NASDAQ 100 (QQQ/QQQM): From about $460 in early April to $554 (28% gain)

Year-to-Date 2025 Performance:

- S&P 500: Up about 7%

- NASDAQ Composite: Up 6.6%

- Dow Jones Industrial Average: Up 4.3%

- Bonds: Up 3.2%

The Strategy: Yes, bonds kept portfolios safe during the downturn, and at that point, they served their purpose. But the key was to take cash or money from the sidelines and invest it during the dip. Bonds can be important for retirees or those living off their portfolios, but if you’re young with years for growth, having too much money sitting on the sidelines will make your portfolio significantly lag.

Watch the full video of this discussion here:

***

Disclaimer: I’m not a financial adviser, but I am an expert in finance and investing who teaches this at the university level. This content is for educational purposes and should not be considered personalized financial advice.