ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

5N Plus Inc. (TSX:VNP) presented its third quarter 2025 earnings results on November 4, showcasing a period of exceptional financial performance. The specialty semiconductor and performance materials company reported its highest quarterly revenue in a decade, significantly beating analyst expectations and driving the stock price up 3.49% to close at $20.76, near its 52-week high of $20.88.

The company's strong performance comes amid growing demand in the terrestrial renewable energy and space power sectors, where 5N Plus has established a strong competitive position. The quarterly results demonstrated the company's ability to translate revenue growth into substantially improved profitability.

Quarterly Performance Highlights

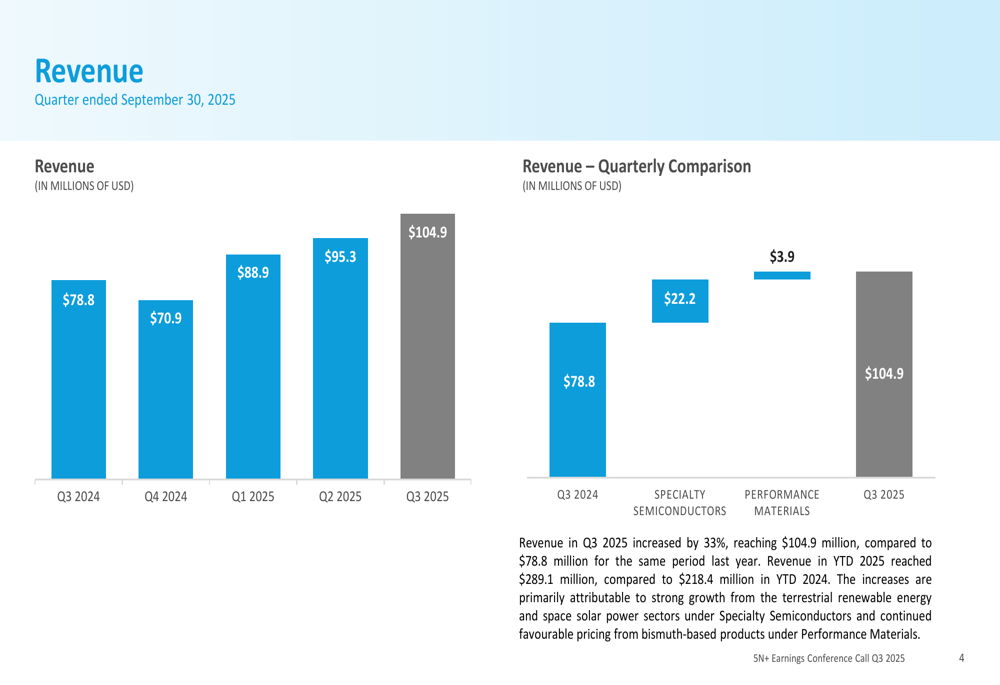

5N Plus reported Q3 2025 revenue of $104.9 million, representing a 33% increase compared to $78.8 million in the same period last year. This figure exceeded analyst expectations of $94.56 million by 10.93%. The revenue growth trend has been consistent over the past five quarters, as illustrated in the following chart:

Net earnings for Q3 2025 reached $18.2 million, nearly tripling the $6.4 million reported in Q3 2024. This translated to earnings per share of $0.20, substantially outperforming the forecasted $0.0925 by 116.22%.

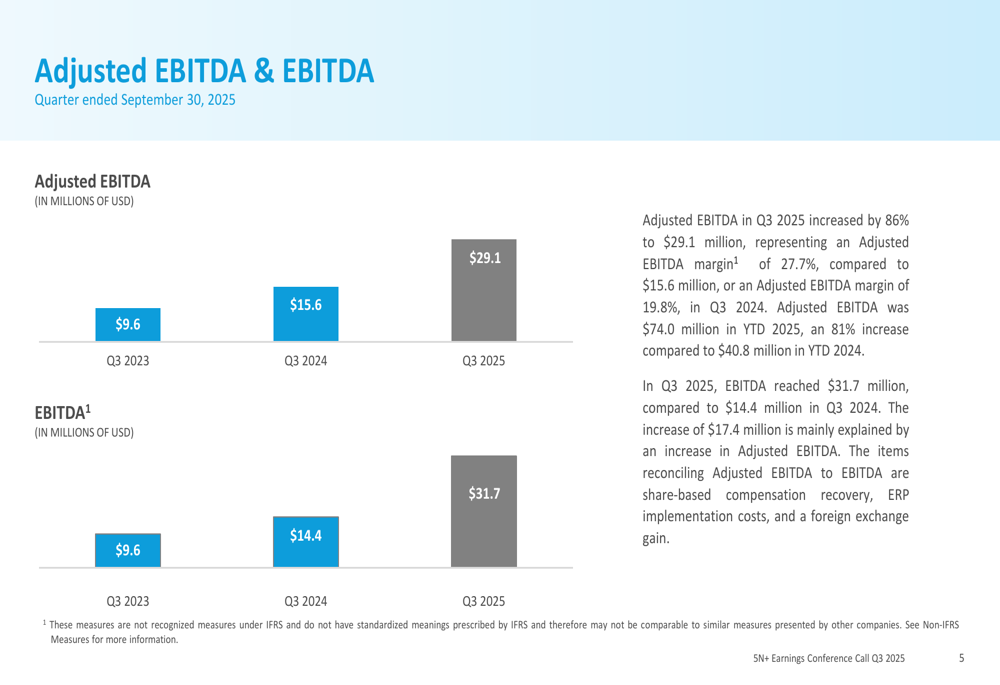

The company's adjusted EBITDA saw an even more dramatic improvement, increasing 86% year-over-year to $29.1 million, compared to $15.6 million in Q3 2024. This represents an adjusted EBITDA margin of 27.7%, up from 19.8% in the prior year period. The following chart illustrates this significant growth:

Adjusted gross margin increased by 58% to $38.7 million, with the adjusted gross margin percentage improving to 36.9% in Q3 2025 from 31.1% in Q3 2024. This margin expansion reflects improved operational efficiency and favorable product mix.

Detailed Financial Analysis

The company's financial health has strengthened considerably over the past year. Net debt decreased to $63.3 million as of September 30, 2025, compared to $100.1 million at the end of 2024, representing a reduction of nearly 37%. The net-debt-to-EBITDA ratio improved to 0.74x, indicating a stronger balance sheet and enhanced financial flexibility.

Year-to-date performance has been equally impressive, with revenue reaching $289.1 million for the first nine months of 2025, compared to $218.4 million in the same period of 2024. Adjusted EBITDA for the year-to-date period increased by 81% to $74.0 million, compared to $40.8 million in the first nine months of 2024.

The company's key financial metrics are summarized in the following comprehensive overview:

5N Plus has maintained a healthy backlog, which stood at $357.5 million as of September 30, 2025, representing 311 days of annualized revenue. This represents a 14-day increase from the previous quarter and provides strong visibility into future revenue streams.

Strategic Position & Outlook

The strong quarterly performance has prompted 5N Plus to revise its 2025 EBITDA guidance upward from $65-70 million to $85-90 million, reflecting confidence in continued strong demand and operational efficiency. The company is particularly well-positioned in the semiconductor compound supply market and is preparing for increased demand in 2026 through capacity expansions.

During the earnings call, CEO Gerard Vajrak highlighted the significance of the quarter, stating: "This quarter marks another financial milestone for 5N Plus, with our strongest quarterly revenue in a decade, record adjusted gross margin, and a new high for quarterly adjusted EBITDA."

The company's management also emphasized 5N Plus's unique market position as one of the few businesses in its sector that can both source critical minerals and recycle or refine secondary materials. This capability provides a competitive advantage, particularly as supply chain resilience becomes increasingly important in the semiconductor and advanced materials industries.

Looking forward, 5N Plus is focused on opportunities in medical imaging and defense sectors, in addition to its established presence in renewable energy and space power. The company's M&A strategy is targeting mature, EBITDA-generating assets that can complement its existing portfolio.

While the outlook remains positive, potential challenges include geopolitical tensions affecting critical mineral supplies, increasing competition in renewable energy sectors, and macroeconomic factors that could impact investment in clean energy infrastructure.

The company's strong financial position, growing backlog, and strategic market positioning suggest continued momentum into 2026, with the potential for further margin expansion and debt reduction as operational efficiencies continue to improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.