Michael Burry warns of $176 billion depreciation understatement by tech giants

Aalberts Industries NV (AMS:AALB) reported a 3.2% organic revenue decline in its first half of 2025 results presentation, reflecting challenging market conditions while maintaining strategic focus on acquisitions and operational excellence. The company’s stock closed at €27.70 following the July 24 earnings release, down 1.59% as investors reacted to the mixed results and tempered outlook.

Executive Summary

Aalberts faced continued end market softness and increased uncertainty during the first half of 2025, prompting management to take proactive steps to protect margins and optimize free cash flow. Despite these challenges, the company continued its strategic expansion with three value-accretive acquisitions and maintained its divestment program to enhance leadership positions.

"We continue to take action to protect our EBITA margin, optimize our free cash flow, while at the same time we will continue to deploy and invest for the long term," said CEO Stéphane Simonetta during the presentation.

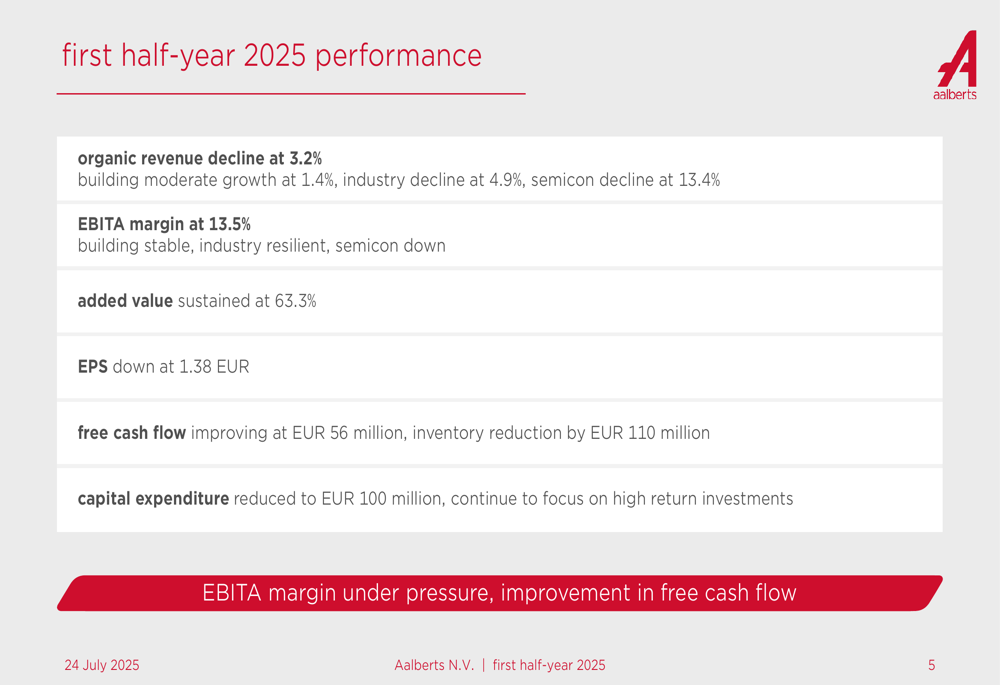

The company’s key financial metrics reflect these challenging conditions:

Financial Performance Highlights

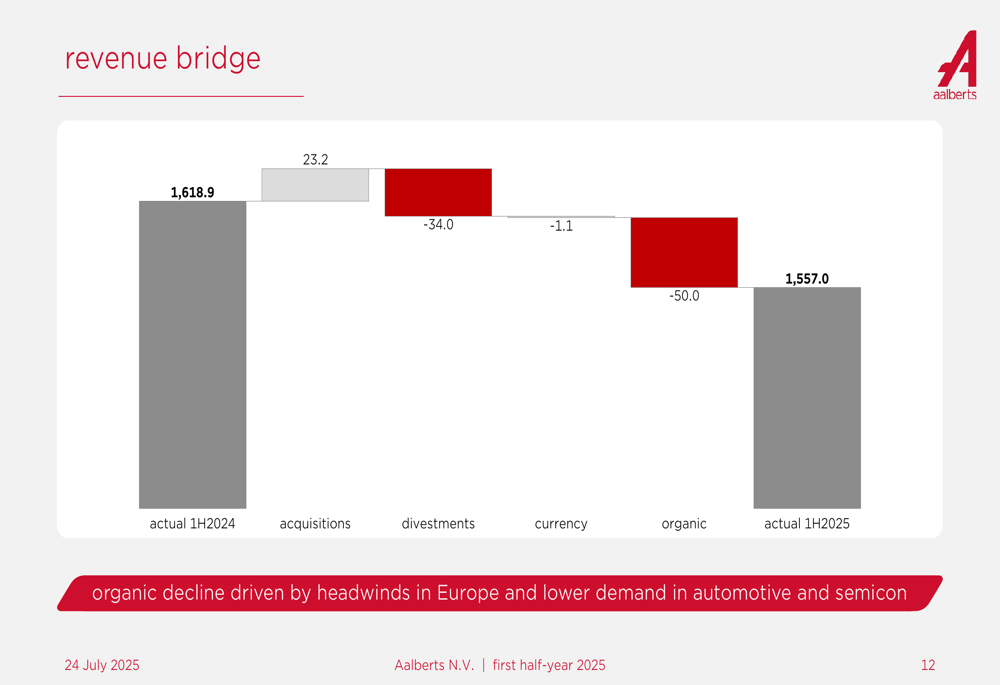

Aalberts reported first-half revenue of €1,557 million, down from €1,619 million in the same period of 2024. The 3.2% organic revenue decline was partially offset by a €23.2 million contribution from acquisitions, while divestments reduced revenue by €34 million.

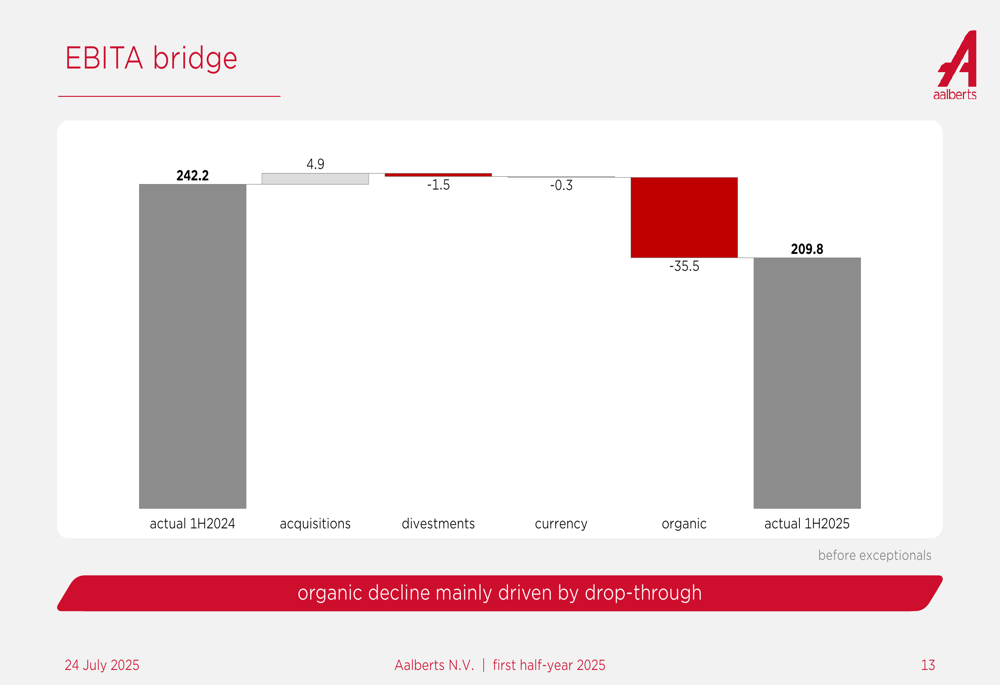

EBITA margin decreased to 13.5% from 15.0% in the previous year, though the company highlighted its efforts to protect margins through operational excellence initiatives. Free cash flow improved to €56 million from €48 million in H1 2024, supported by inventory reduction of €110 million and reduced capital expenditure of €100 million (down from €117 million).

The financial development bridge clearly illustrates the factors impacting revenue performance:

Similarly, the EBITA bridge shows how organic decline significantly impacted profitability despite positive contributions from acquisitions:

Segment Performance

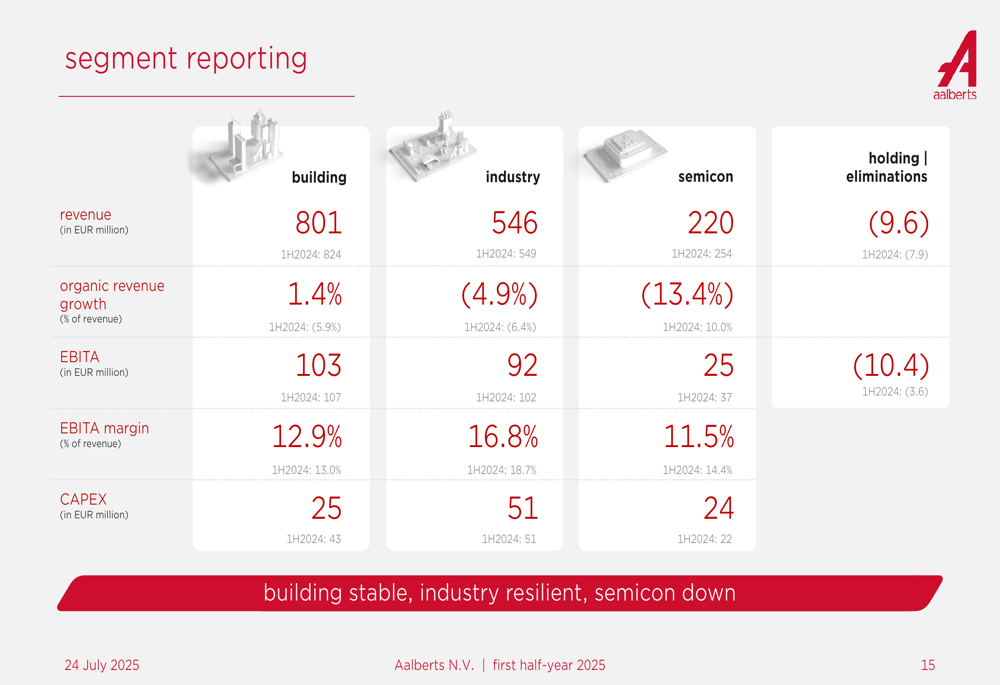

Aalberts’ performance varied significantly across its three main segments:

The Building segment showed moderate growth with 1.4% organic revenue increase, driven by strength in America and APAC regions. However, European markets remained challenging, with Germany and France continuing to be soft and slowdowns observed in Benelux and Eastern Europe. The segment maintained a stable EBITA margin of 12.9%.

The Industry segment experienced a 4.9% organic revenue decline, though it maintained a strong EBITA margin of 16.8%. Growth areas included aerospace, power generation, and defense, while automotive markets remained soft. The integration of Paulo, acquired in May 2025, is on track and expected to be accretive to both growth and margins.

The Semicon segment faced the steepest challenges with a 13.4% organic revenue decline, though it sustained an EBITA margin of 11.5%. The company noted that Q2 performance was better than Q1 in this segment.

The segment breakdown provides a clear view of each division’s performance metrics:

Strategic Initiatives

Despite market headwinds, Aalberts continued to execute its ’thrive 2030’ strategic plan, focusing on portfolio optimization through both acquisitions and divestments. The company completed two acquisitions in the United States (Geo-Flo for the building segment and Paulo for the industry segment) and announced its intention to acquire Grand Venture Technology (GVT) in Southeast Asia to strengthen its semiconductor business.

The intended acquisition of GVT would expand Aalberts’ semiconductor footprint in Southeast Asia. GVT is headquartered in Singapore with six production sites, 1,800 employees, and generated revenue of approximately SGD 160 million in 2024.

According to CFO Frans den Houter, "We really want full control over the company," highlighting the strategic importance of the planned GVT acquisition. The earnings call revealed that a shareholder vote on this acquisition is expected in September, with closing anticipated by year-end.

Simultaneously, Aalberts is driving a divestment program to enhance leadership positions and simplify its portfolio within the building and industry segments. The company is evaluating business units based on market attractiveness and ability to win, with potential divestments of €400-500 million expected.

The company also emphasized its operational excellence initiatives, which delivered significant results in H1 2025:

Outlook and Guidance

Based on current market dynamics and uncertainties, Aalberts adjusted its full-year outlook. The company does not expect organic revenue growth improvement in the second half of 2025 and adjusted its EBITA margin guidance to 13-14%.

For the short term, Aalberts outlined several key focus areas to navigate the challenging environment:

Market Context

Aalberts’ stock price fell by 1.59% following the earnings announcement, closing at €27.70. With a market capitalization of $3.42 billion and a beta of 1.3, the company faces ongoing investor scrutiny regarding its ability to navigate current market challenges.

Despite these challenges, the company maintains impressive gross profit margins of 62.93%, and according to some market analysis, the stock appears undervalued at current levels. The company’s balance sheet remains solid with a leverage ratio of 1.6 and solvability of 55.7%.

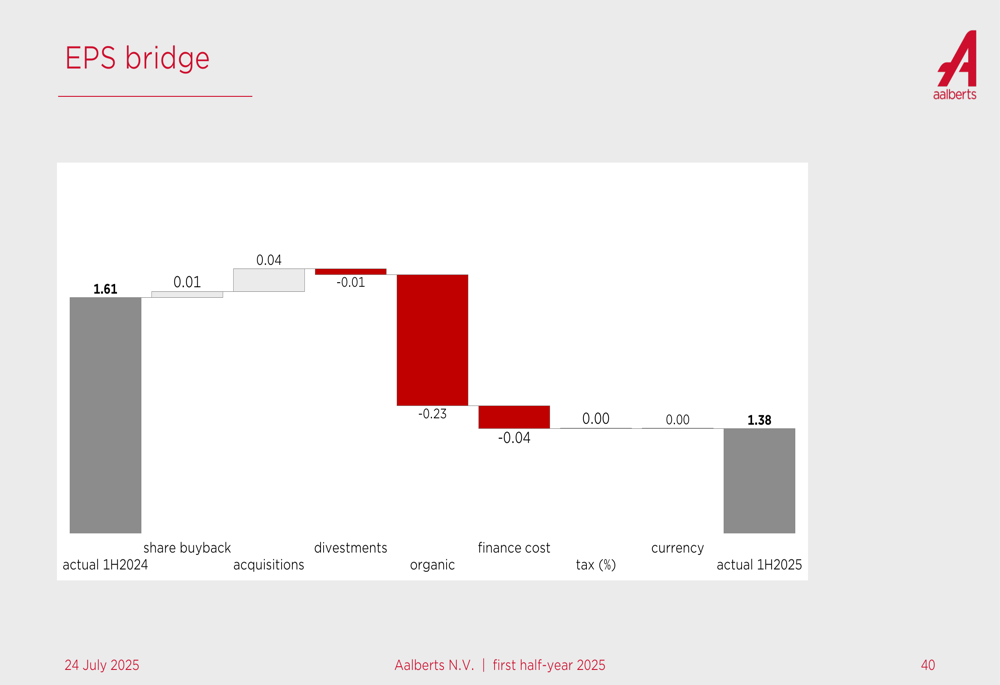

The EPS bridge shows the various factors contributing to the decline in earnings per share from €1.61 to €1.38:

As Aalberts continues to navigate market softness while pursuing its strategic initiatives, investors will be closely watching whether the company’s operational excellence and portfolio optimization efforts can offset the challenging market conditions and deliver improved performance in the second half of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.