U.S. stocks surge; investors buoyed by progress towards ending government shutdown

Introduction & Market Context

Aalberts Industries NV ( AMS (VIE:AMS2):AALB) presented its first half-year 2025 results on July 24, 2025, revealing challenging market conditions that have prompted the company to adjust its full-year outlook. The industrial technology company reported a 3.2% organic revenue decline and reduced EBITA margins, leading to a significant market reaction with shares dropping 14.07% to €27.24, approaching its 52-week low of €24.64.

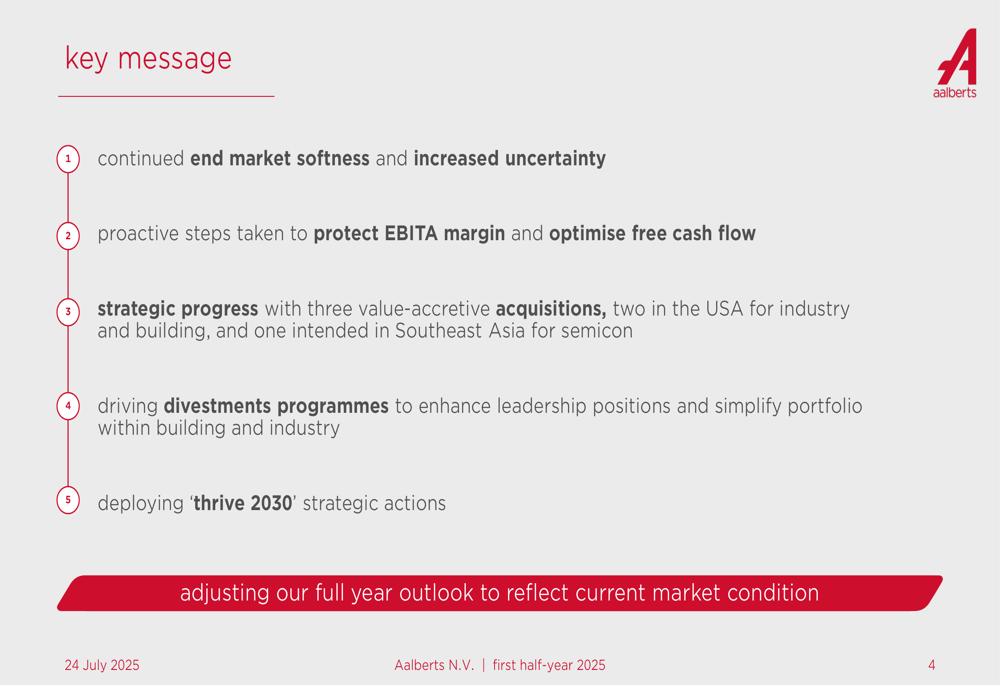

CEO Stéphane Simonetta highlighted "continued end market softness and increased uncertainty" as key factors affecting performance, while emphasizing the company’s proactive measures to protect margins and optimize cash flow. The results presentation comes amid ongoing challenges in European industrial markets and semiconductor sector weakness.

As shown in the following key messages slide, Aalberts is focusing on strategic acquisitions and operational improvements to navigate the difficult environment:

Quarterly Performance Highlights

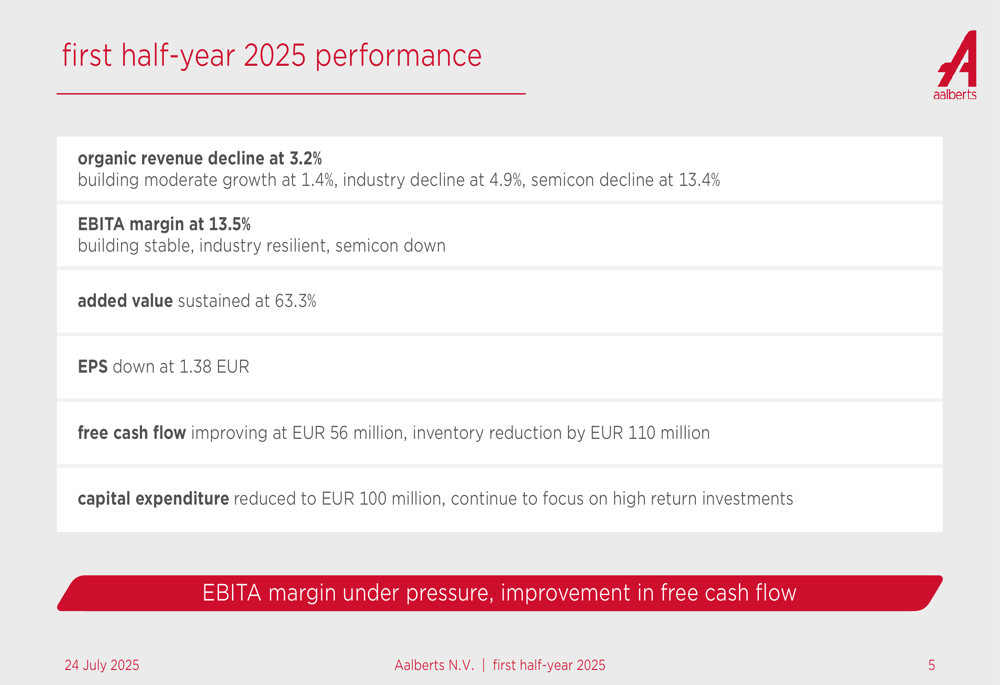

Aalberts reported first half-year 2025 revenue of €1,557 million, representing a 3.2% organic decline compared to the same period in 2024. The company’s EBITA margin fell to 13.5% from 15.0% in the previous year, while earnings per share decreased to €1.38.

Despite revenue challenges, the company improved its free cash flow to €56 million (up from €48 million in 1H2024) and achieved a significant inventory reduction of €110 million. Capital expenditure was reduced by 14% to €100 million as the company focused on high-return investments.

The following slide illustrates these key financial metrics:

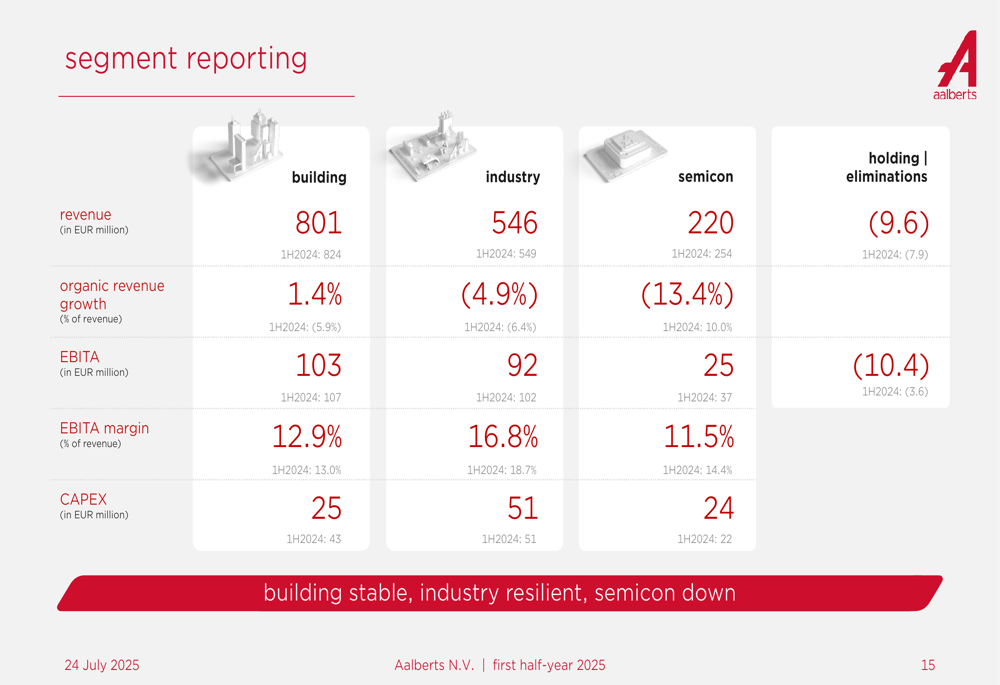

Performance varied significantly across Aalberts’ three business segments. The building segment showed moderate growth with a 1.4% organic revenue increase and stable EBITA margin of 12.9%. The industry segment experienced a 4.9% organic revenue decline but maintained a resilient EBITA margin of 16.8%. The semiconductor segment faced the most significant challenges with a 13.4% organic revenue decline and EBITA margin pressure.

The detailed segment breakdown is illustrated in the following slide:

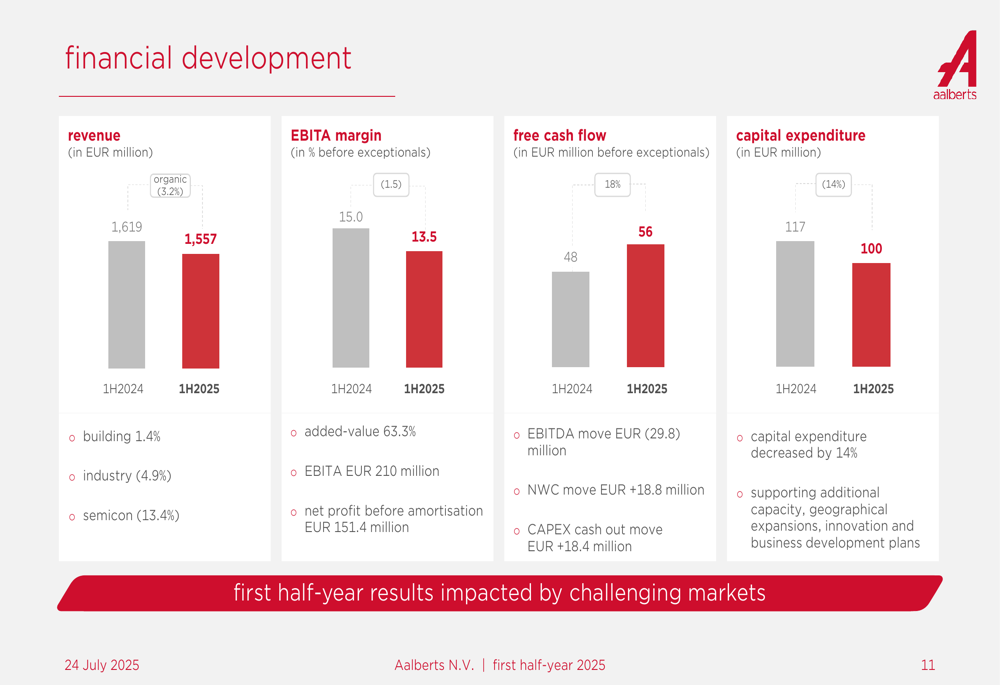

A closer examination of financial development shows the bridge between 2024 and 2025 performance:

Strategic Initiatives

Despite market headwinds, Aalberts continues to execute its "thrive 2030" strategy, focusing on portfolio optimization through both acquisitions and divestments. The company completed three value-accretive acquisitions during the period: Paulo (industrial heat treatment provider), Geo-Flo (pumping solutions for HVAC systems), and announced its intention to acquire Grand Venture Technology (GVT) in Southeast Asia to strengthen its semiconductor segment.

The company’s strategic framework is outlined in the following slide:

Aalberts is also implementing a divestment program for activities with low market attractiveness, targeting €400-500 million in revenue within the building and industry segments. This portfolio rationalization aims to enhance leadership positions and simplify the company’s structure.

The acquisition strategy is detailed in this slide:

Operational excellence initiatives remain a priority, with Aalberts reporting progress in four key areas: footprint optimization (including a major site closure in the UK), inventory reduction (€110 million reduction, DIO at 87 days), operations productivity (approximately €10 million in savings), and capital expenditure reduction (14% decrease).

These operational improvements are illustrated in the following slide:

Forward-Looking Statements

Based on current market conditions, Aalberts has adjusted its full-year 2025 outlook. The company does not expect organic revenue growth improvement in the second half of the year and has revised its full-year EBITA margin outlook to 13-14%.

Management emphasized continued focus on protecting EBITA margins and optimizing free cash flow through several short-term actions, including:

- Pursuing organic growth initiatives

- Continuing operational excellence programs with an annual benefit of €30 million

- Further cost-out excellence

- Inventory optimization to reduce DIO to below 90 days

- Lean capital expenditure within €200-225 million

- Portfolio optimization through divestments

The company’s outlook is summarized in this slide:

Balance Sheet and Financial Position

Despite challenging market conditions, Aalberts maintains a solid balance sheet with net debt of €971 million and a leverage ratio of 1.6. The company reported equity of €2,456 million, representing a solvability ratio of 55.7%. Return on capital employed (ROCE) stands at 13.3%, while net working capital has been reduced to €770 million (89 days).

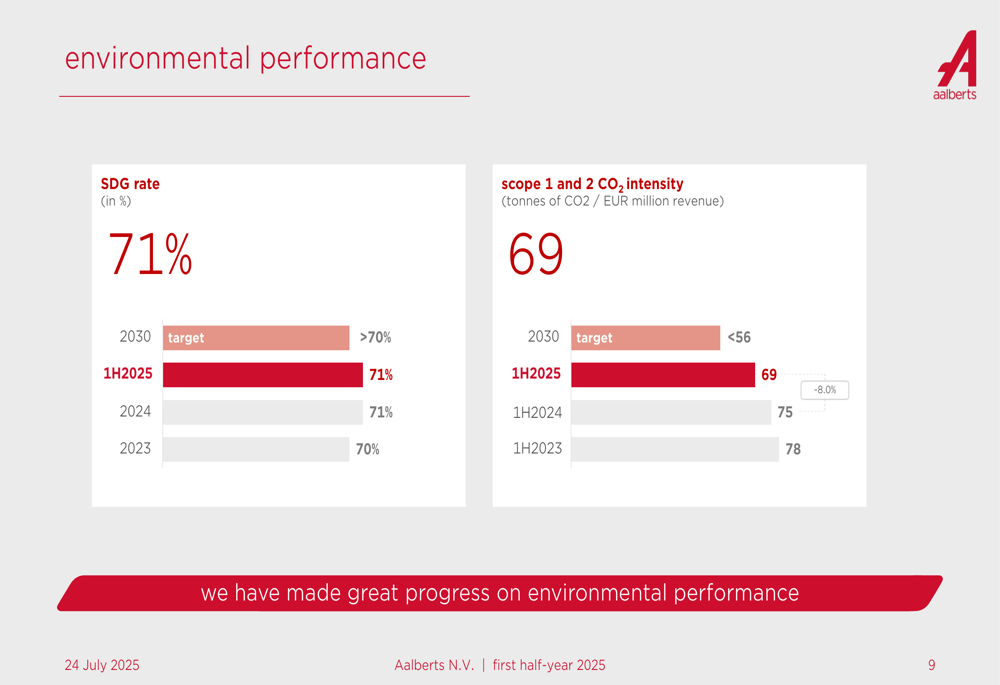

The company continues to make progress on its environmental commitments, with its SDG rate at 71% (ahead of the 2030 target of >70%) and scope 1 and 2 CO2 intensity improving to 69 tonnes of CO2 per €1 million revenue (down from 75 in 1H2024).

As shown in the following slide, Aalberts’ environmental performance continues to improve:

Aalberts’ management emphasized that despite current challenges, the company’s strong balance sheet supports its long-term "thrive 2030" strategy, enabling continued strategic investments while navigating the current market downturn. However, investors appear concerned about the near-term outlook, as reflected in the significant stock price decline following the results announcement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.