Palantir launches Chain Reaction AI infrastructure platform with CenterPoint and NVIDIA

Introduction & Market Context

Anheuser-Busch InBev (NYSE:BUD) presented its second quarter 2025 results on July 31, 2025, reporting EBITDA growth of 6.5% and margin expansion despite volume challenges in key markets. However, the stock fell 11.23% following the presentation, closing at $51.56, suggesting investors were concerned about the 1.9% decline in total volumes, particularly in Brazil and China.

The brewing giant maintained its full-year outlook of 4-8% organic EBITDA growth, continuing its focus on premiumization, digital transformation, and financial discipline. This follows the company’s strong Q1 2025 performance, which saw EBITDA growth of 7.9%, indicating a slight deceleration in the second quarter.

Quarterly Performance Highlights

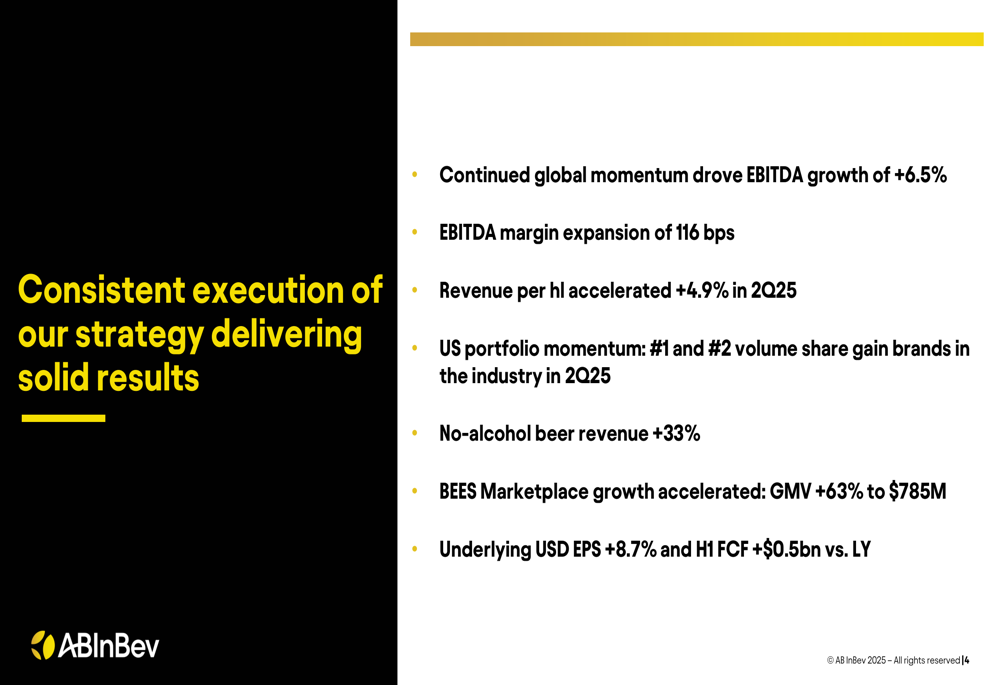

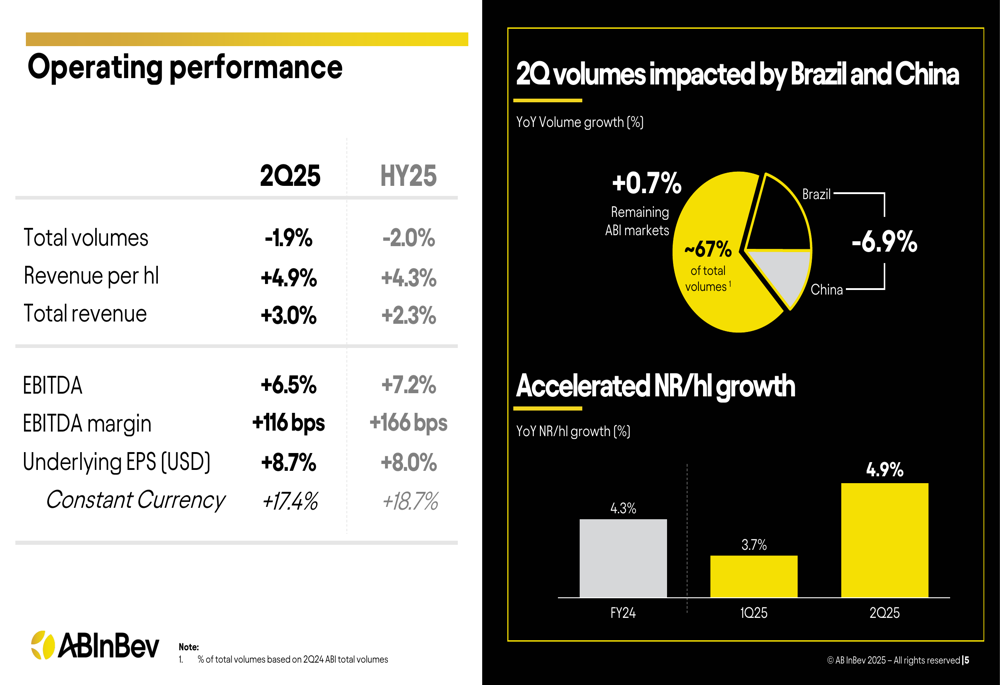

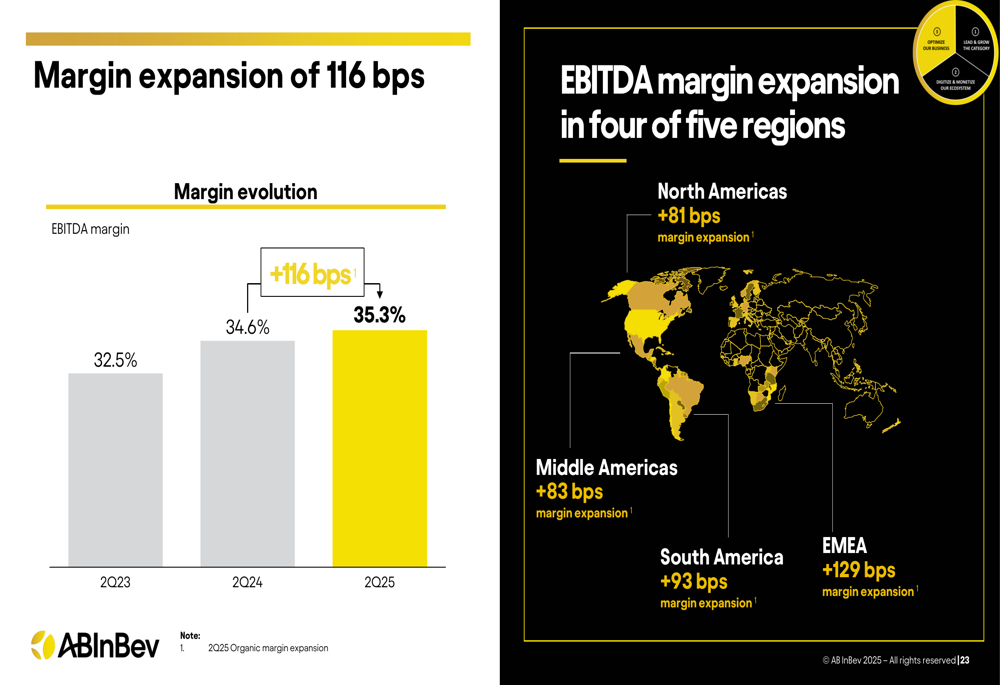

AB InBev reported solid financial results for Q2 2025, with EBITDA growing 6.5% and EBITDA margin expanding by 116 basis points to 35.3%. Revenue increased by 3.0%, driven by a 4.9% improvement in revenue per hectoliter, which accelerated from 3.7% in Q1 2025. Underlying EPS grew 8.7% to $0.98, while first-half free cash flow improved by $0.5 billion compared to last year.

As shown in the following key results summary:

The company’s volume performance was mixed, with total volumes declining 1.9% in Q2 2025. This was primarily impacted by weakness in Brazil (-6.9%) and China, while approximately 67% of total volumes from remaining markets grew by 0.7% year-over-year. The following chart illustrates this performance breakdown:

Regional Performance Analysis

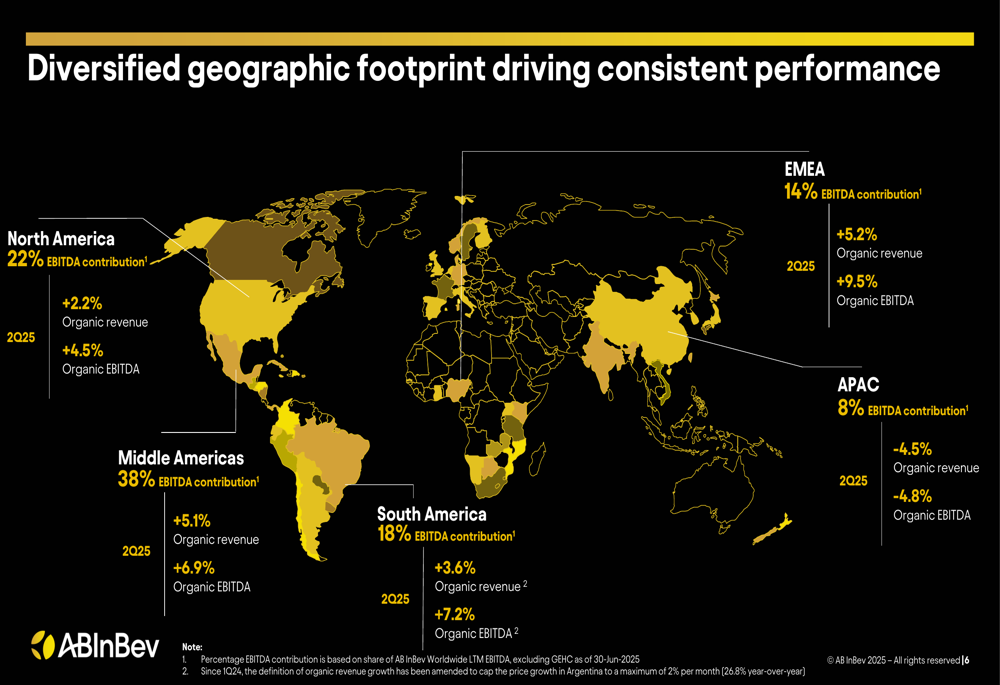

AB InBev’s geographic diversification helped offset challenges in specific markets. North America delivered 4.5% EBITDA growth with volumes up 0.3%, driven by strong performance of Michelob Ultra and Busch Light, which were the #1 and #2 volume share gainers in the U.S. beer industry.

Middle Americas continued its momentum with 6.9% EBITDA growth and 1.1% volume growth, led by Mexico and Colombia. South America saw EBITDA growth of 7.2% despite a 4.9% volume decline, with Brazil underperforming a soft industry impacted by adverse weather.

EMEA was a standout performer with 9.5% EBITDA growth and 0.9% volume growth, with market share gains in 5 of 6 key European markets. In contrast, APAC struggled with EBITDA declining 4.8% and volumes down 6.6%, primarily due to continued weakness in China.

The following map illustrates the company’s diversified geographic footprint and regional performance:

Strategic Initiatives

AB InBev continues to execute its three-pillar strategy focused on leading and growing the category, digitizing and monetizing its ecosystem, and optimizing its business:

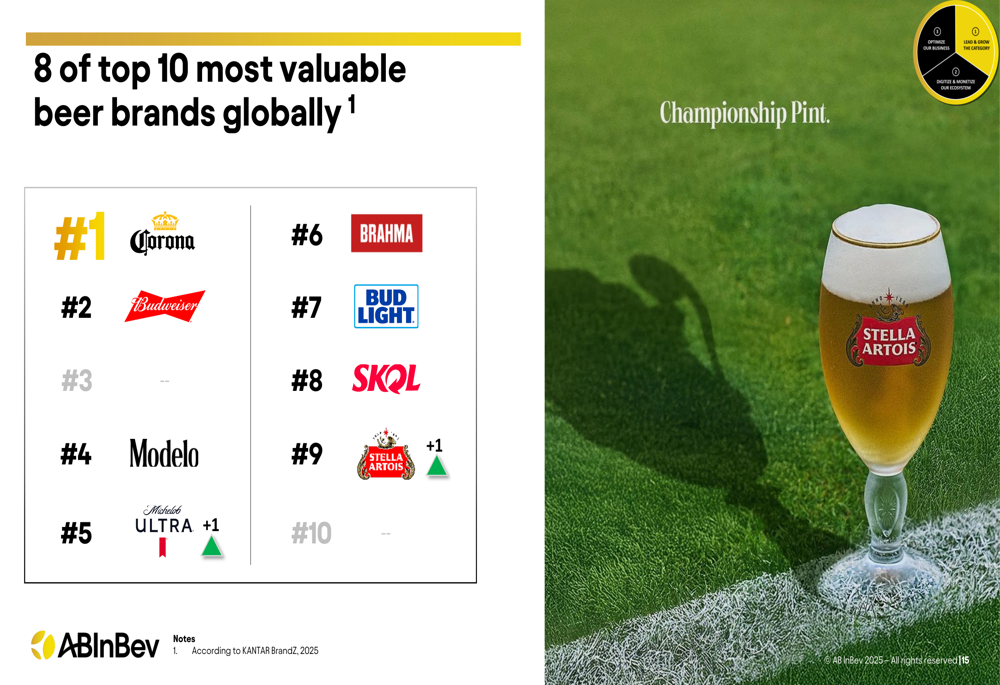

The company’s brand portfolio remains strong, with 8 of the top 10 most valuable beer brands globally according to KANTAR BrandZ 2025. Corona leads as the most valuable beer brand, followed by Budweiser:

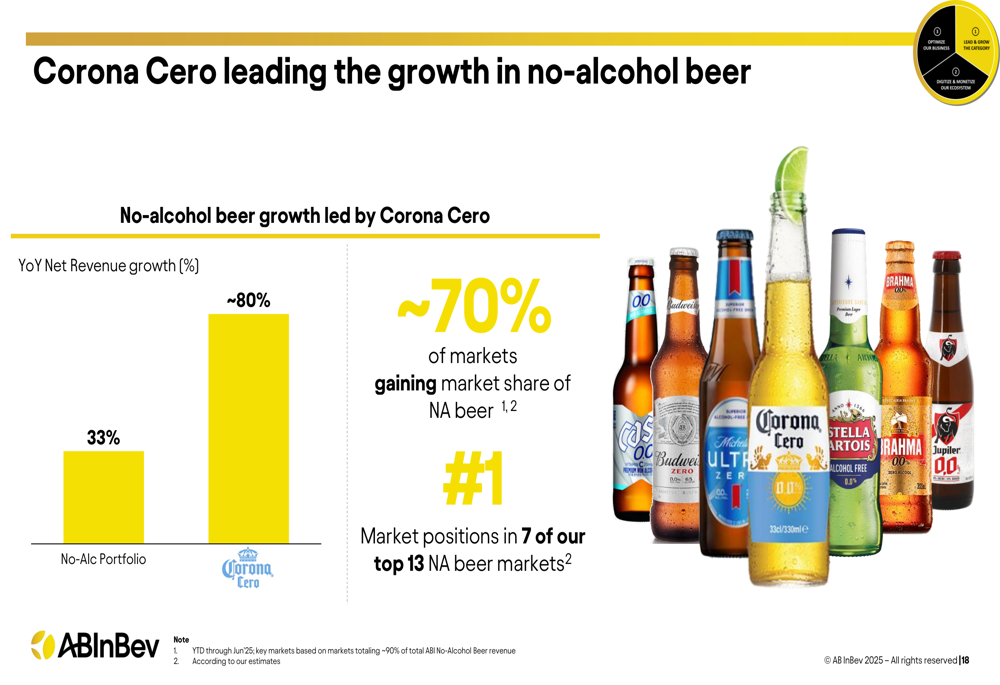

A key growth area is the no-alcohol beer segment, which saw 33% revenue growth, led by Corona Cero with approximately 80% net revenue growth year-over-year:

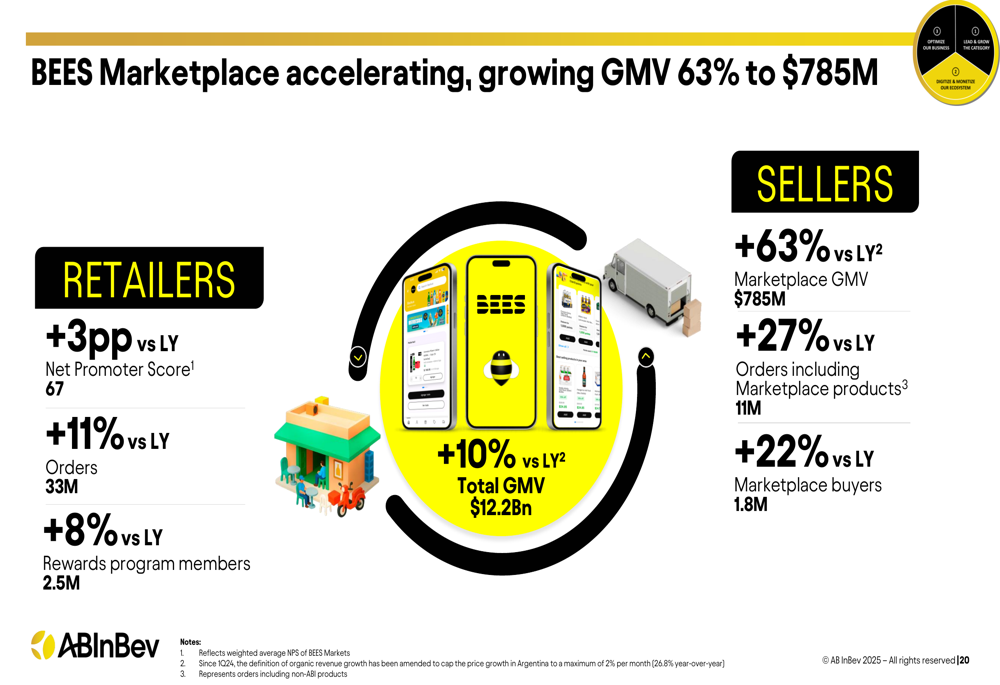

AB InBev’s digital transformation continues to accelerate, with the BEES Marketplace growing its Gross Merchandise Value (GMV) by 63% to $785 million. The platform’s Net Promoter Score increased 3 percentage points year-over-year to 67, with 33 million orders (up 11%) and 2.5 million rewards program members (up 8%):

Financial Position & Outlook

The company has maintained its focus on margin expansion, with EBITDA margin improving from 32.5% in Q2 2023 to 35.3% in Q2 2025:

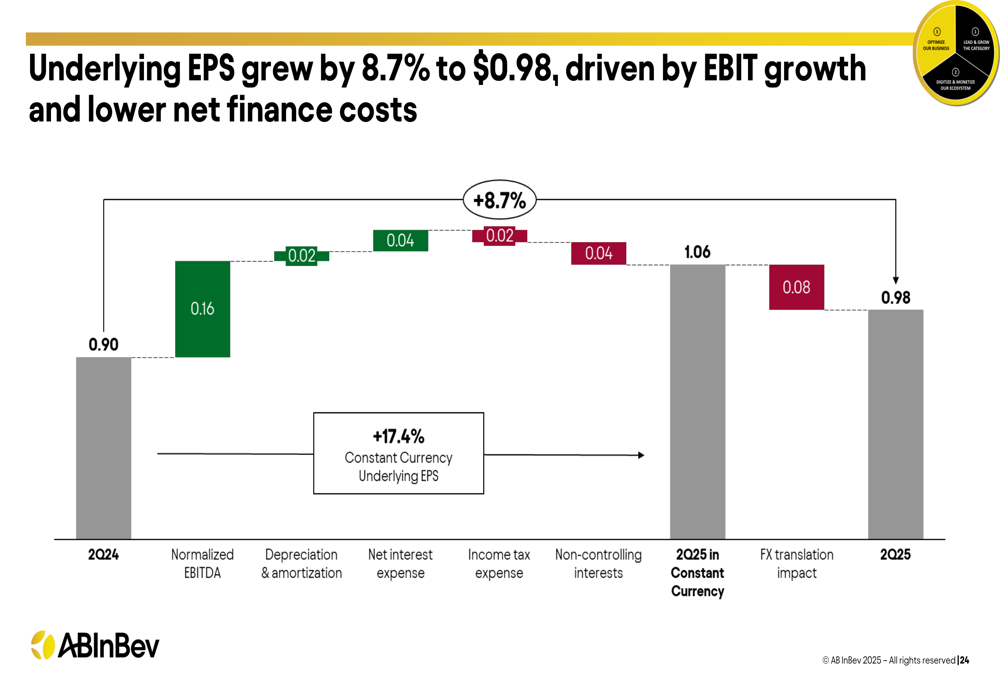

Underlying EPS grew 8.7% to $0.98, driven by EBIT growth and lower net finance costs, though partially offset by foreign exchange translation impacts:

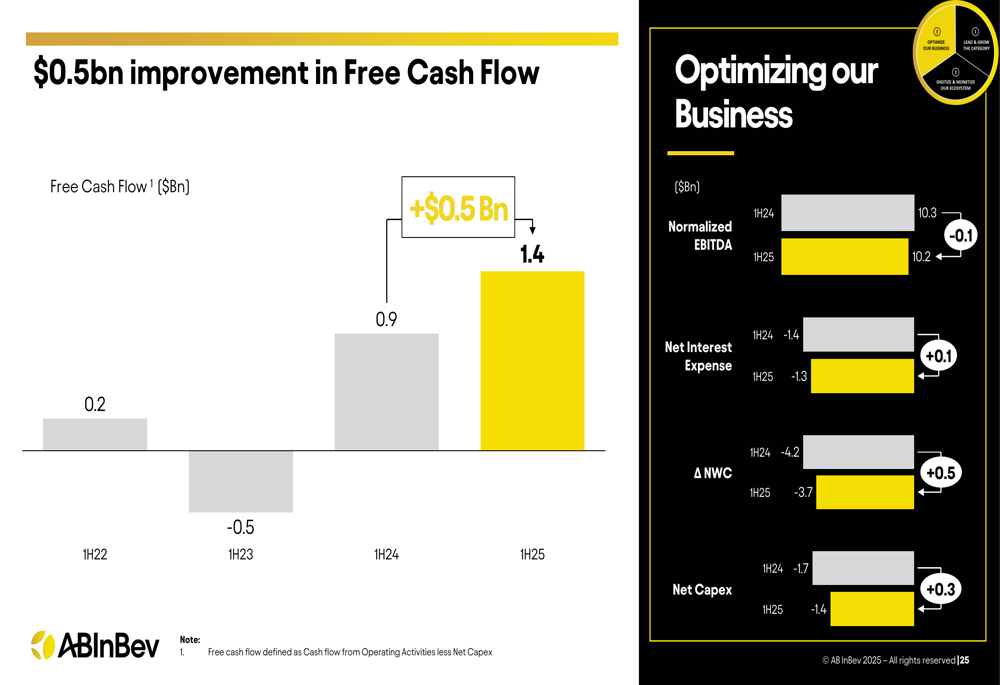

Free cash flow improved by $0.5 billion in the first half of 2025 compared to the same period last year, reaching $1.4 billion:

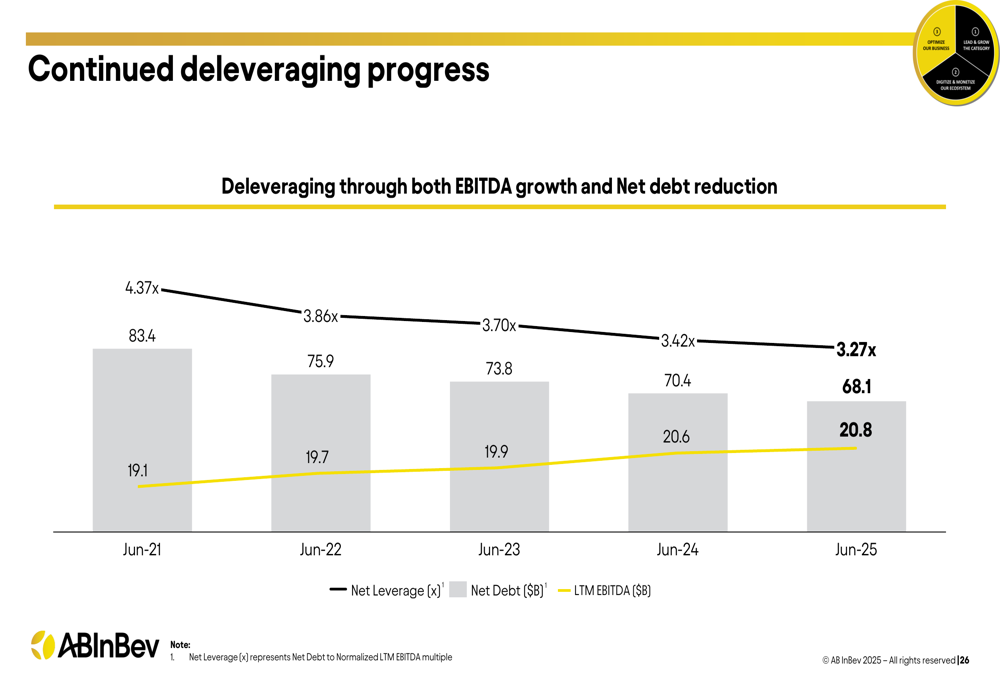

AB InBev continues to make progress on deleveraging, with net leverage decreasing from 4.37x in June 2021 to 3.27x in June 2025, while net debt reduced from $83.4 billion to $68.1 billion over the same period:

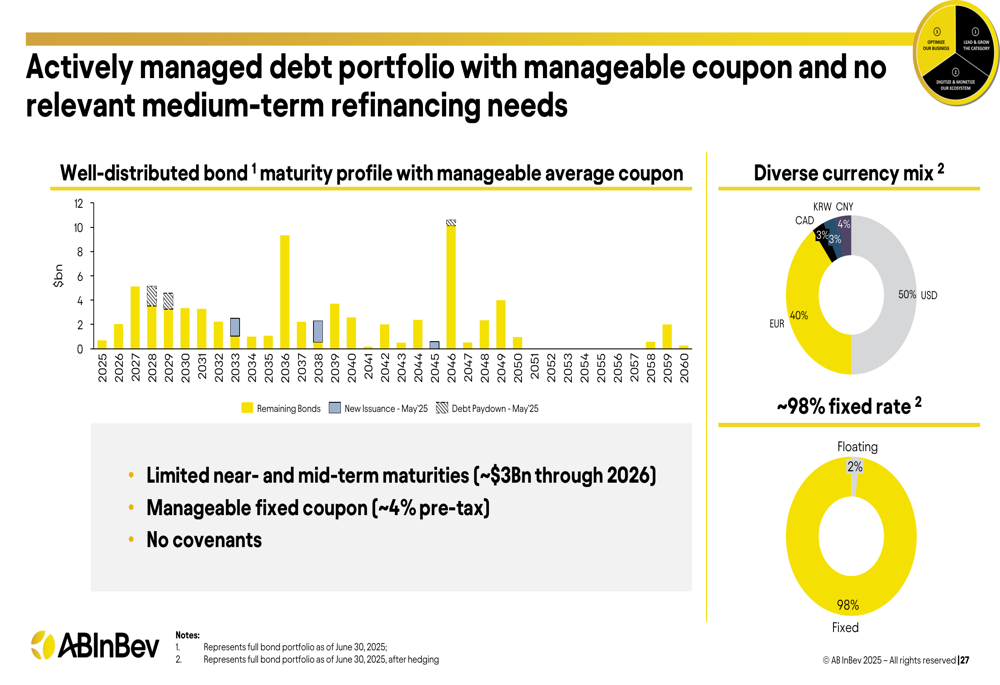

The company actively manages its debt portfolio with a well-distributed bond maturity profile, limited near-term maturities, and approximately 98% fixed-rate debt:

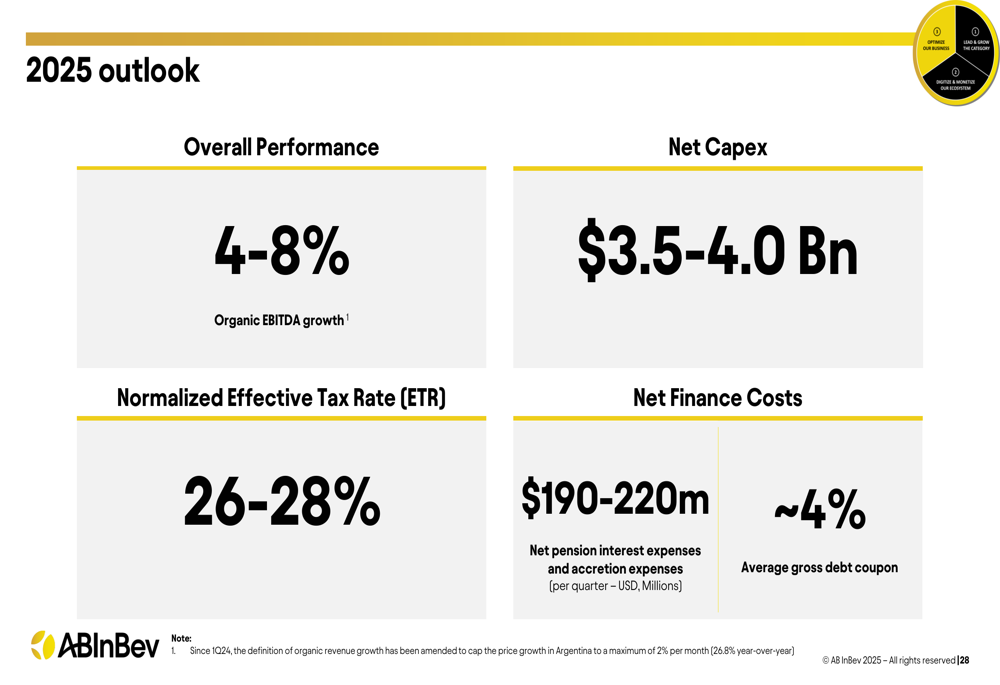

For the full year 2025, AB InBev maintained its outlook of 4-8% organic EBITDA growth, with net capital expenditure of $3.5-4.0 billion and a normalized effective tax rate of 26-28%:

Despite the solid financial performance and strategic progress, the market reaction suggests investors may be concerned about volume trends, particularly in Brazil and China, and the sustainability of growth through pricing alone. The company’s ability to revitalize volume growth while continuing its premiumization and digital transformation strategies will be key to watch in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.