Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

Anheuser Busch InBev SA (EBR:ABI) reported modest growth in its third quarter of 2025, with financial results showing resilience despite volume challenges across most markets. The company's shares closed at €52.98 on October 30, down 1.66% following the earnings announcement, as investors processed the mixed signals from the brewing giant's performance.

The world's largest brewer managed to deliver revenue growth of 0.9% and EBITDA growth of 3.3% for the quarter, demonstrating its ability to execute pricing strategies and cost management effectively in a challenging global beer market. The company's focus on premiumization and expansion beyond traditional beer categories continues to yield positive results, even as overall volumes declined.

Quarterly Performance Highlights

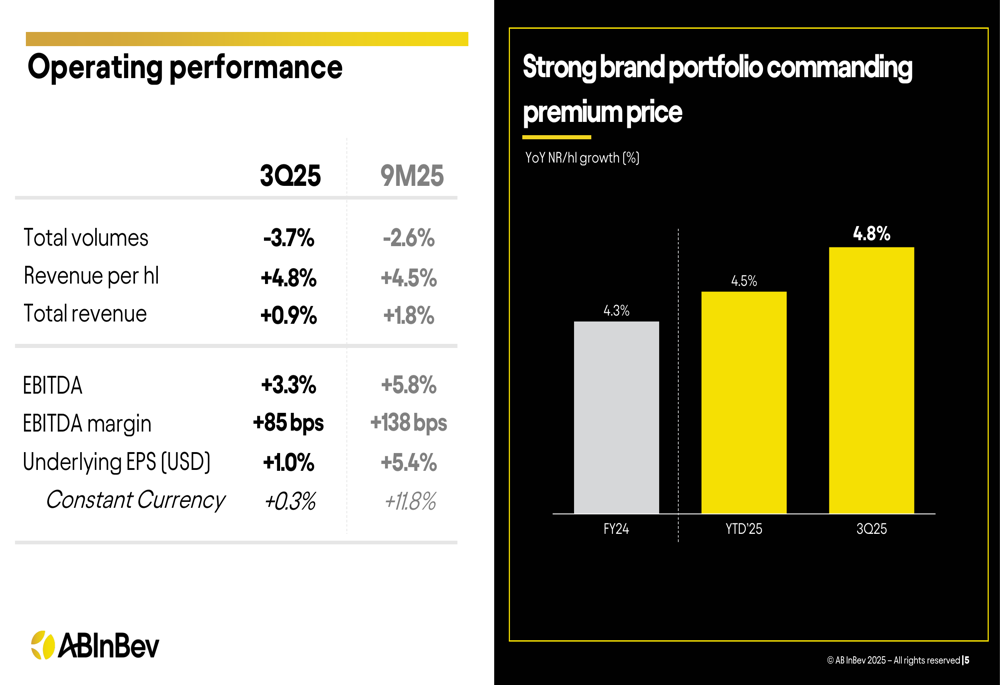

AB InBev's Q3 2025 results revealed a consistent pattern of volume challenges offset by pricing power and premium brand performance. Total volumes declined by 3.7% in Q3 and 2.6% for the first nine months of 2025, but revenue per hectoliter grew by 4.8% in the quarter, allowing for total revenue growth of 0.9%.

As shown in the following comprehensive performance overview:

The company's EBITDA grew by 3.3% in Q3 and 5.8% for the first nine months of 2025, with EBITDA margins expanding by 85 basis points in the quarter. Underlying earnings per share increased by 1.0% to $0.99, slightly below the 5.4% growth seen in the first nine months of the year.

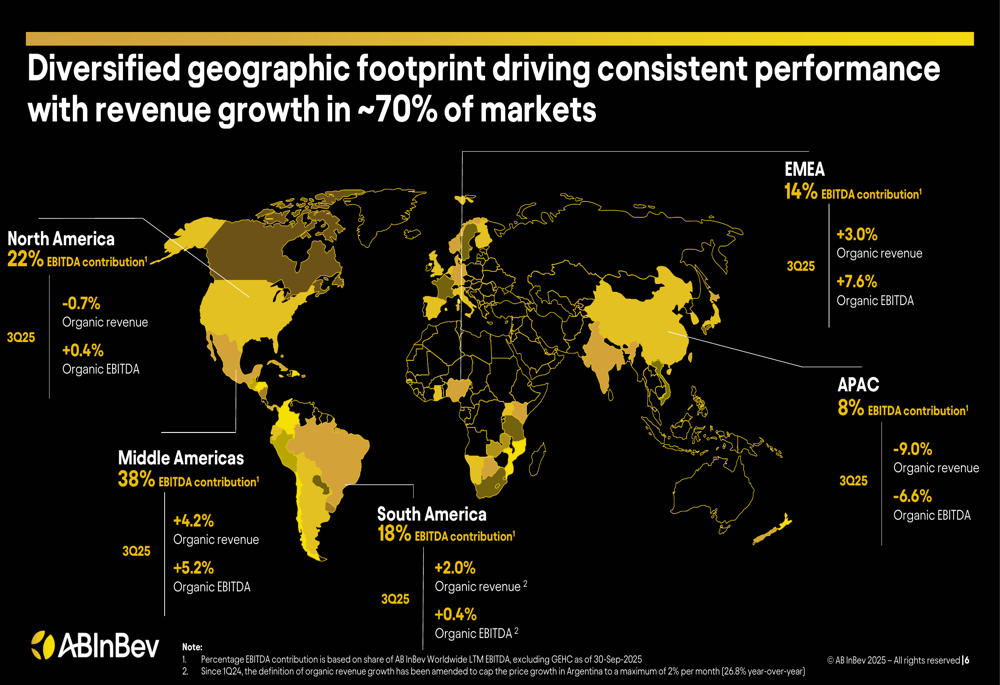

The company's geographic diversification has proven valuable in navigating regional challenges, with Middle Americas contributing 38% of total EBITDA, followed by North America at 22% and South America at 18%. This regional breakdown is illustrated in the following map:

Regional Performance Analysis

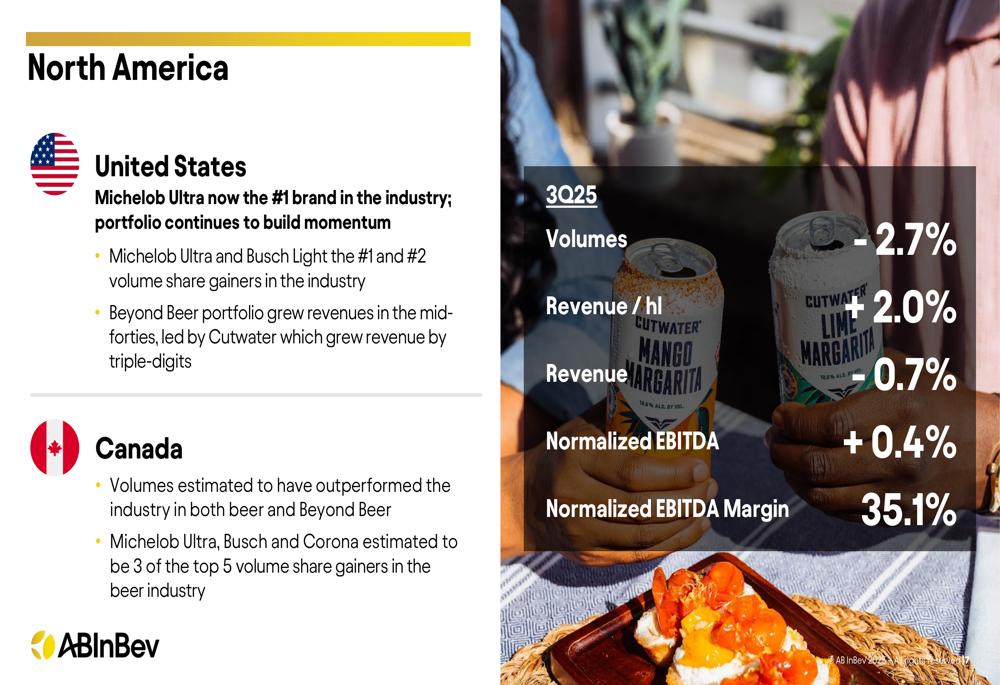

In North America, AB InBev reported a 0.7% revenue decline but managed to grow EBITDA by 0.4%, achieving an EBITDA margin of 35.1%. The region's performance was highlighted by Michelob Ultra becoming the number one beer brand by volume in the United States year-to-date, a significant milestone for the company.

The North American market showed mixed results but strong brand performance:

Middle Americas emerged as the strongest performing region, with revenue growing by 4.2% and EBITDA by 5.2%. Mexico delivered low-single-digit revenue growth driven by disciplined revenue management, while Colombia achieved double-digit top-line growth and mid-single-digit bottom-line improvement.

South America faced more significant challenges, particularly in Brazil where unseasonable weather impacted the industry. Despite this, the company gained market share in Brazil and delivered flat EBITDA with margin expansion through disciplined revenue and cost management. Argentina continued to face pressure from inflation, with volumes declining by low-single digits.

The Asia-Pacific region was the most challenging, with revenue declining by 9.0% and EBITDA by 6.6%, primarily due to ongoing market difficulties in China.

Strategic Initiatives & Brand Performance

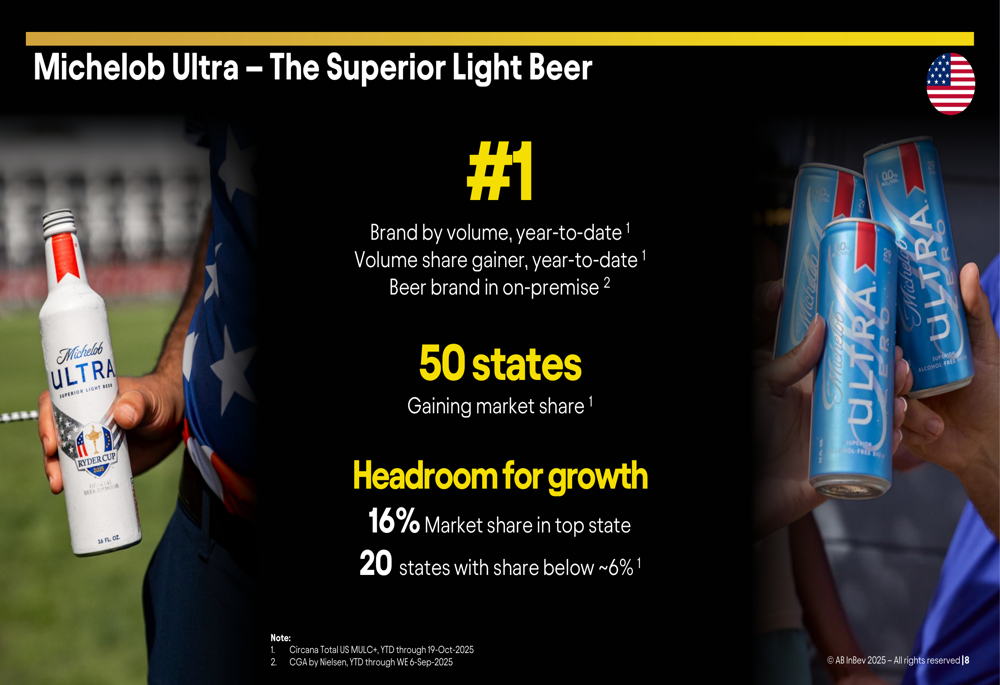

Michelob Ultra's rise to become the top beer brand by volume in the United States represents a major achievement for AB InBev's premiumization strategy. The brand, along with Busch Light, ranked as the top two volume share gainers in the U.S. market.

The following slide highlights Michelob Ultra's market leadership and growth potential:

Beyond traditional beer categories, AB InBev continues to see strong growth in no-alcohol beer (+27%) and its Beyond Beer portfolio (+27%), with the latter driven by products like Cutwater canned cocktails, which grew revenues in the mid-forties in the U.S. market.

The company's digital marketplace platform, BEES, continues to gain traction with quarterly GMV growing by 66% and approaching $1 billion, representing a significant opportunity for future growth.

Capital Allocation & Forward-Looking Statements

AB InBev announced a substantial $6 billion share buyback program, signaling increased confidence in its financial position and commitment to returning value to shareholders. Additionally, the company executed a $2 billion debt redemption and declared an interim dividend of €0.15 per share.

During the earnings call, CEO Michel Doukeris emphasized the company's commitment to innovation and consumer value, stating, "We are investing to provide superior value to our consumers." He also highlighted opportunities beyond the beer market, noting that "The addressable market outside beer is bigger than the beer category itself."

Looking ahead, AB InBev remains confident in delivering 4-8% EBITDA growth for 2025, with the upcoming FIFA World Cup in North America expected to provide a boost to the beer category. The company faces ongoing challenges from inflation, particularly in Latin America, and weather-related impacts on consumption patterns, but its diversified geographic footprint and strong brand portfolio position it to navigate these headwinds.

While volume trends remain a concern, AB InBev's ability to drive revenue per hectoliter growth and expand margins demonstrates the effectiveness of its premiumization strategy and operational efficiency initiatives in a challenging global beer market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.