Introduction & Market Context

Abercrombie & Fitch Co. (NYSE:ANF) released its third-quarter 2025 results on November 25, showing continued momentum with 7% year-over-year revenue growth despite mixed brand performance. The company’s stock surged 24.71% following the announcement, reflecting investor confidence in its strategic direction and improved outlook.

The retailer, which operates Abercrombie & Fitch, abercrombie kids, Hollister, and Gilly Hicks Active brands, reported its 12th consecutive quarter of growth. This performance comes amid a challenging retail environment characterized by shifting consumer preferences and ongoing tariff pressures.

Quarterly Performance Highlights

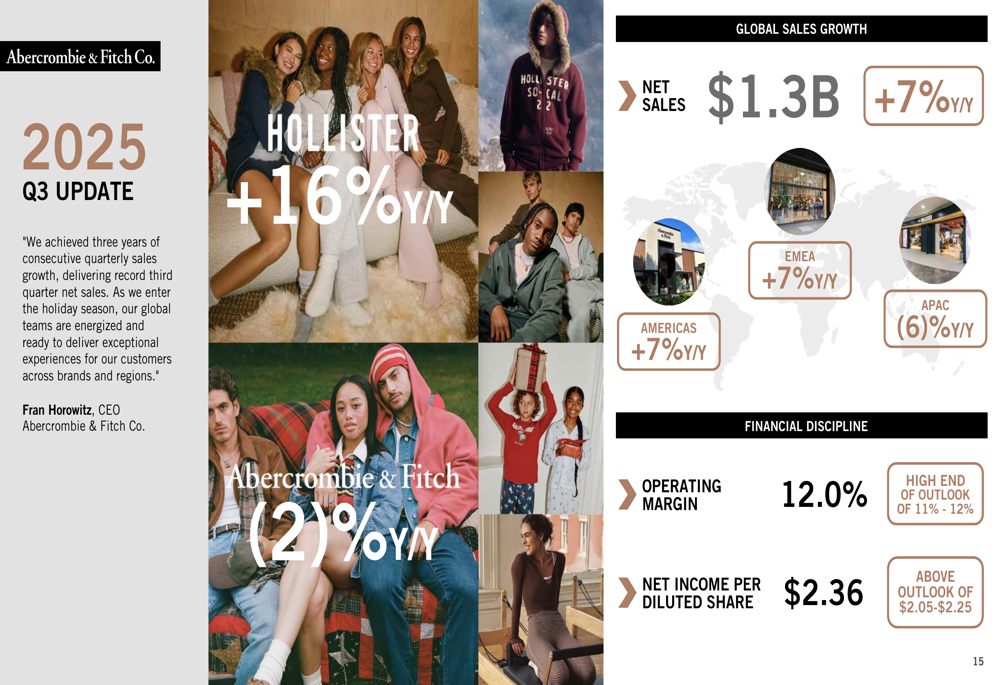

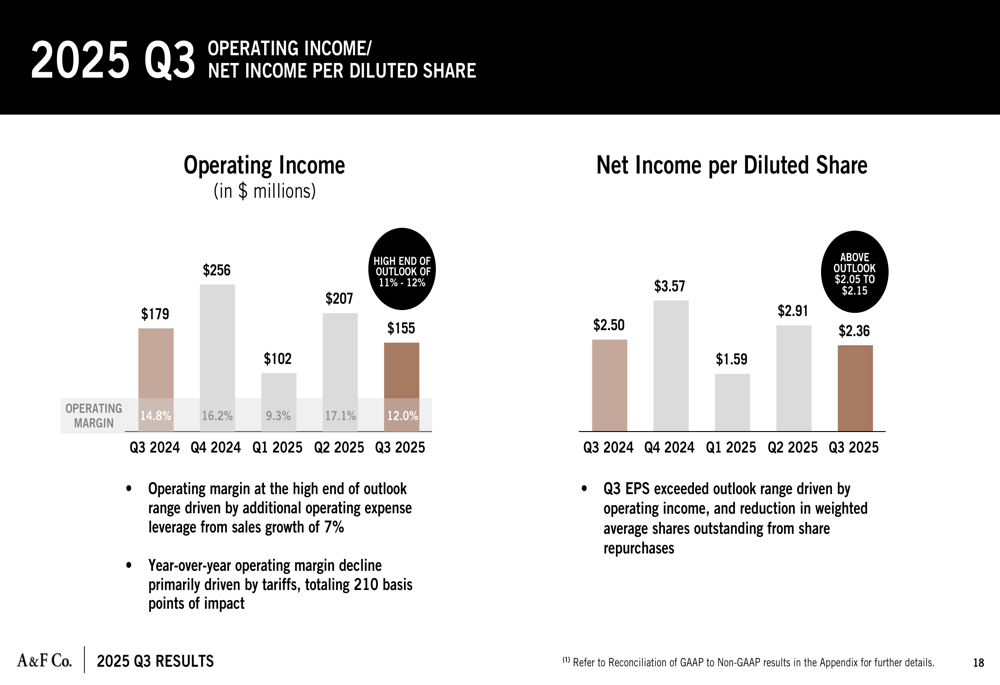

Abercrombie & Fitch reported net sales of $1.3 billion for Q3 2025, representing a 7% increase year-over-year. Operating income reached $155 million, resulting in an operating margin of 12.0%, which was at the high end of the company’s outlook range despite being lower than the 14.8% reported in Q3 2024.

As shown in the following quarterly update slide, earnings per diluted share came in at $2.36, exceeding the company’s outlook range of $2.05-$2.25:

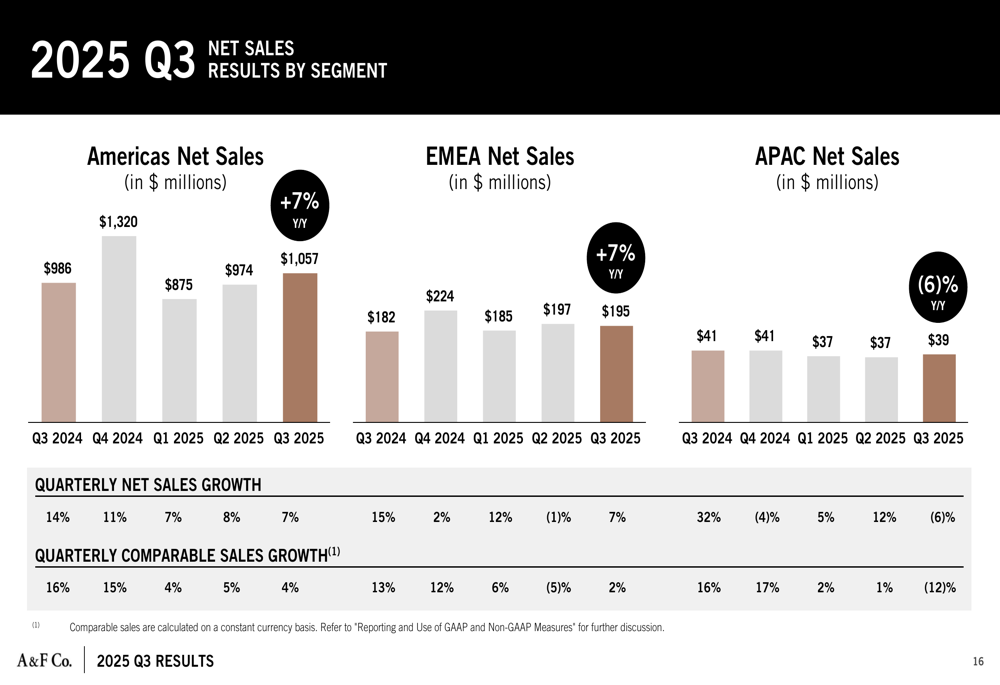

The company’s performance varied significantly by region and brand. Both the Americas and EMEA regions posted 7% year-over-year growth, while APAC experienced a 6% decline. The detailed regional breakdown reveals consistent growth in the Americas, with some volatility in international markets:

Brand Performance Analysis

The most striking aspect of Abercrombie & Fitch’s quarterly results was the divergence in brand performance. Hollister Brands demonstrated remarkable strength with 16% year-over-year growth, while Abercrombie Brands declined by 2%. This contrast is clearly illustrated in the following slide:

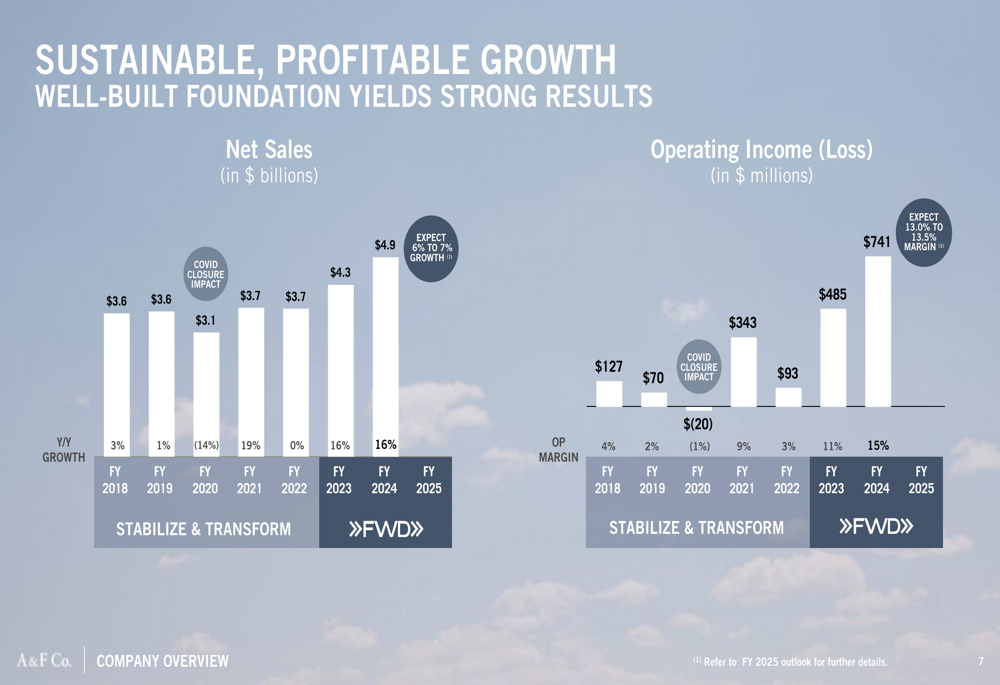

The company’s long-term growth trajectory shows significant improvement in both sales and profitability since 2018. Net sales have grown from $3.6 billion in FY 2018 to an expected $4.9 billion in FY 2025, while operating margins have expanded dramatically from 4% to a projected 13.0-13.5% for FY 2025:

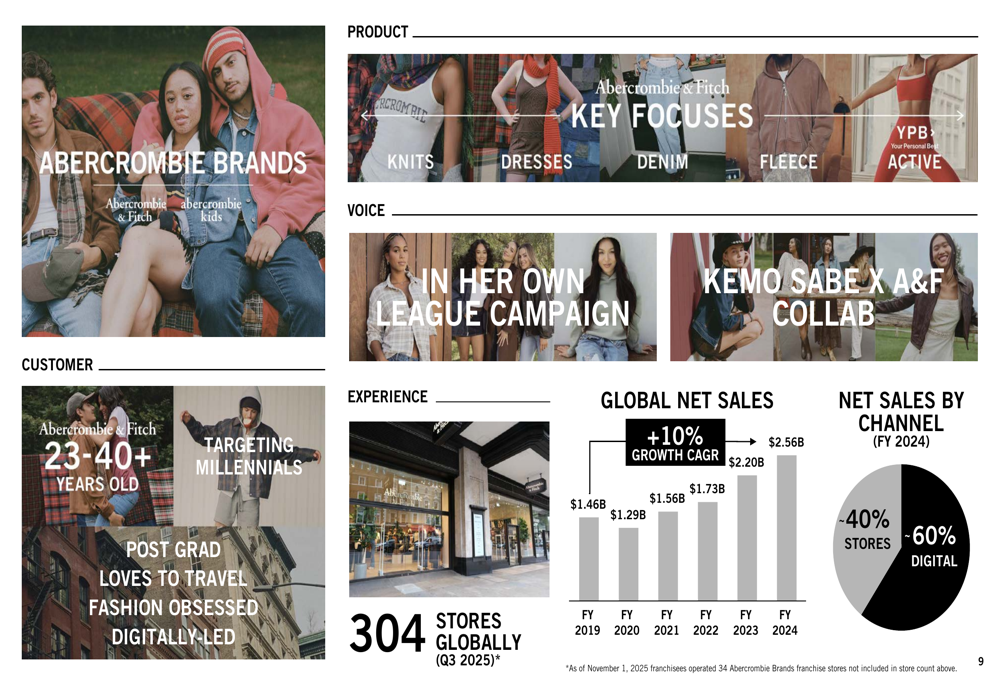

This performance divergence between brands reflects their distinct market positioning and customer bases. Abercrombie Brands target millennials aged 23-40+, with 60% of sales coming through digital channels:

Meanwhile, Hollister Brands focus on Gen Z teens aged 13-21, with a stronger store presence accounting for 70% of sales:

Strategic Initiatives

Abercrombie & Fitch’s ">>FWD>" strategy continues to guide its business transformation, focusing on three key pillars: executing global brand growth, accelerating enterprise-wide digital revolution, and operating with financial discipline.

The company’s digital transformation emphasizes both customer experience ("WOW THEM") and customer analytics ("KNOW THEM"), leveraging AI and personalization to drive engagement and sales. This approach has helped the company maintain strong digital sales, particularly for the Abercrombie brand.

Store expansion represents another key strategic initiative, with plans now calling for approximately 40 net new store openings in FY 2025, double the previously announced target of 20. This increased store opening plan signals management confidence in the company’s brick-and-mortar strategy, particularly for the Hollister brand where in-store shopping remains dominant.

Financial Position & Outlook

Despite ongoing investments in growth initiatives, Abercrombie & Fitch maintains a strong financial position with $606 million in cash and equivalents as of Q3 2025. Inventory levels stood at $730 million, up 5% from last year, with units up approximately 1% and tariffs contributing about 3% to cost.

The company’s operating margin declined year-over-year in Q3, primarily due to tariff impacts, which management quantified at 210 basis points:

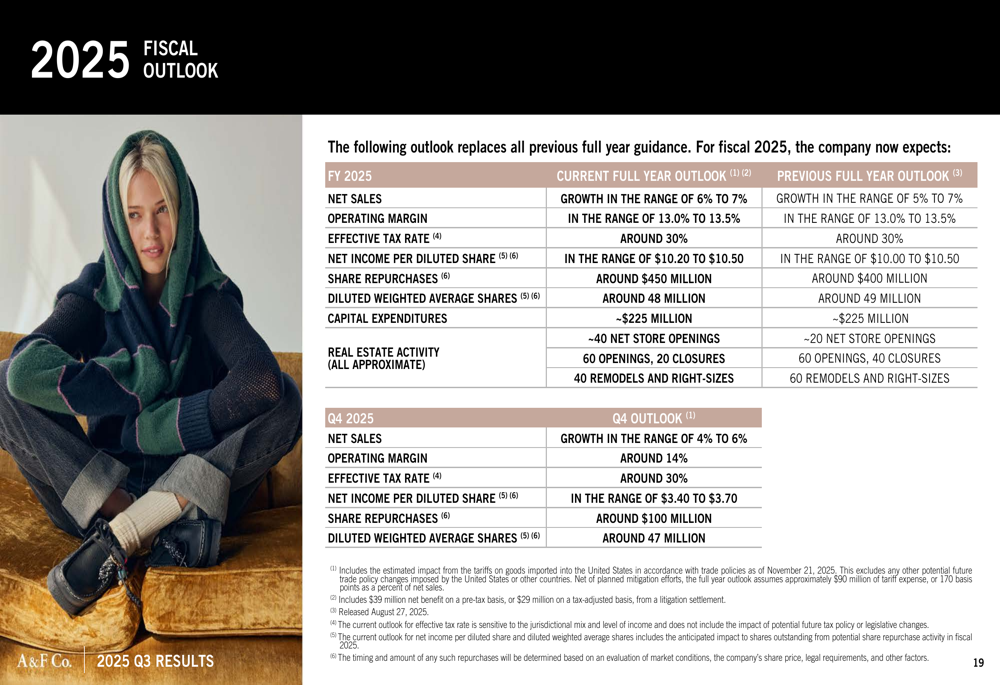

Looking ahead, Abercrombie & Fitch raised its full-year outlook, now expecting net sales growth of 6-7% (up from 5-7% previously) and earnings per diluted share of $10.20-$10.50 (improved from $10.00-$10.50). The company also increased its share repurchase target to approximately $450 million for FY 2025, up from $400 million previously:

For Q4 2025, the company expects net sales growth of 4-6% and an operating margin of approximately 14%, resulting in earnings per diluted share between $3.40-$3.70.

Forward-Looking Statements

During the earnings call, CEO Fran Horowitz expressed confidence in the company’s holiday season preparations, stating, "We are fully prepared for the holiday season, having used these past months and quarters to test and learn and build confidence in our assortment and brand positioning."

Management addressed the tariff challenges, with CFO Robert Ball noting, "We’re coming at this next chapter of tariffs from a position of strength." The company plans to implement targeted price increases for spring deliveries as part of its tariff mitigation strategy.

Abercrombie & Fitch’s share repurchase program continues to reduce the outstanding share count, with approximately 4.5 million shares repurchased year-to-date at an average cost of $77.79 per share. This ongoing buyback activity, combined with the increased store opening plans and raised guidance, suggests management remains confident in the company’s long-term prospects despite near-term challenges in the Abercrombie brand and APAC region.

The stock’s 24.71% surge following the earnings announcement reflects investor optimism about the company’s ability to navigate these challenges while continuing to deliver growth through its diversified brand portfolio and omnichannel strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.