S&P, Nasdaq edge higher with gold spike, FOMC minutes in focus

Accel Entertainment Inc (NYSE:ACEL) reported record quarterly revenue of $336 million in its second quarter 2025 earnings presentation released on August 5, showing 8.6% year-over-year growth despite mixed performance across its geographic markets. The gaming terminal operator’s stock closed at $12.32, up 0.57% for the day, with a slight 0.24% gain in after-hours trading.

Quarterly Performance Highlights

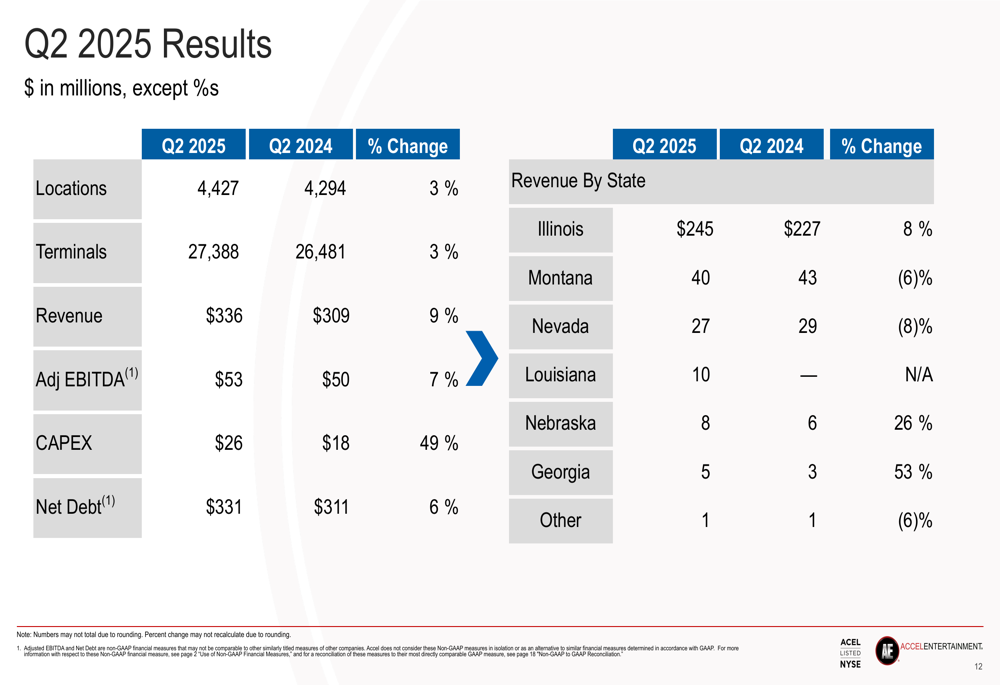

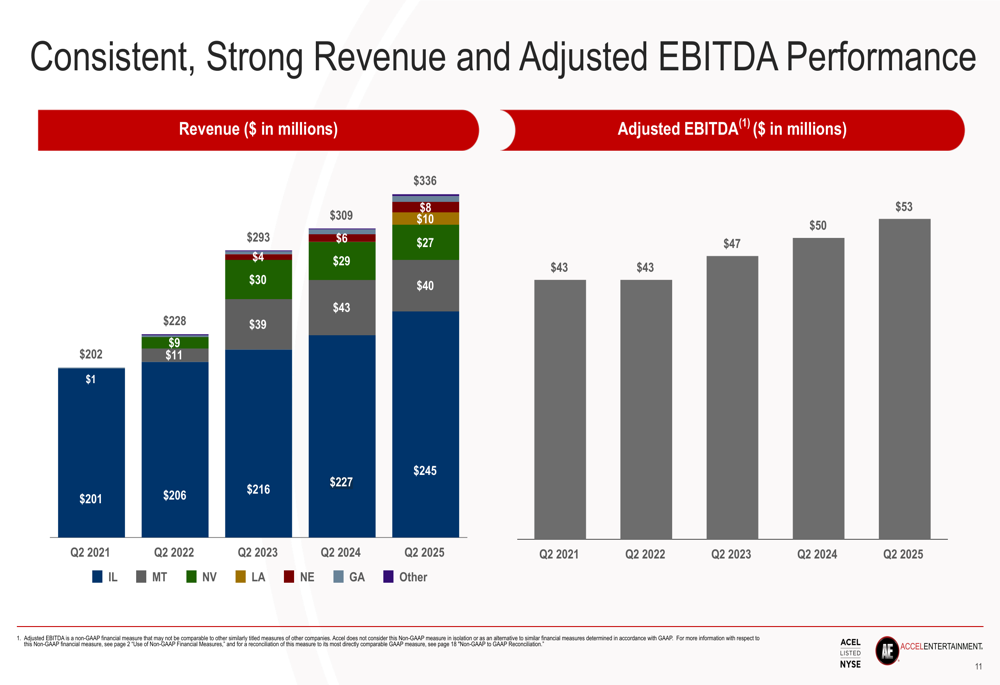

Accel delivered record revenue of $336 million, representing an 8.6% increase compared to Q2 2024. Excluding the impact of the Fairmount Park and Toucan Gaming acquisitions, revenue grew 2.4% to $317 million. The company also achieved record Adjusted EBITDA of $53 million, up 7.1% from the prior year period.

As shown in the following comprehensive results breakdown:

However, net income declined significantly, falling 50.2% year-over-year to $7 million. The company attributed this primarily to a $6 million loss from the change in fair value of contingent earnout shares, compared to a $5 million gain in the prior period.

This performance follows a mixed Q1 2025, when the company reported record revenue of $344 million but missed earnings per share expectations with $0.17 versus a forecasted $0.24. The sequential revenue decline from Q1 to Q2 ($344M to $336M) suggests some operational challenges despite the year-over-year growth.

Geographic Expansion and Market Performance

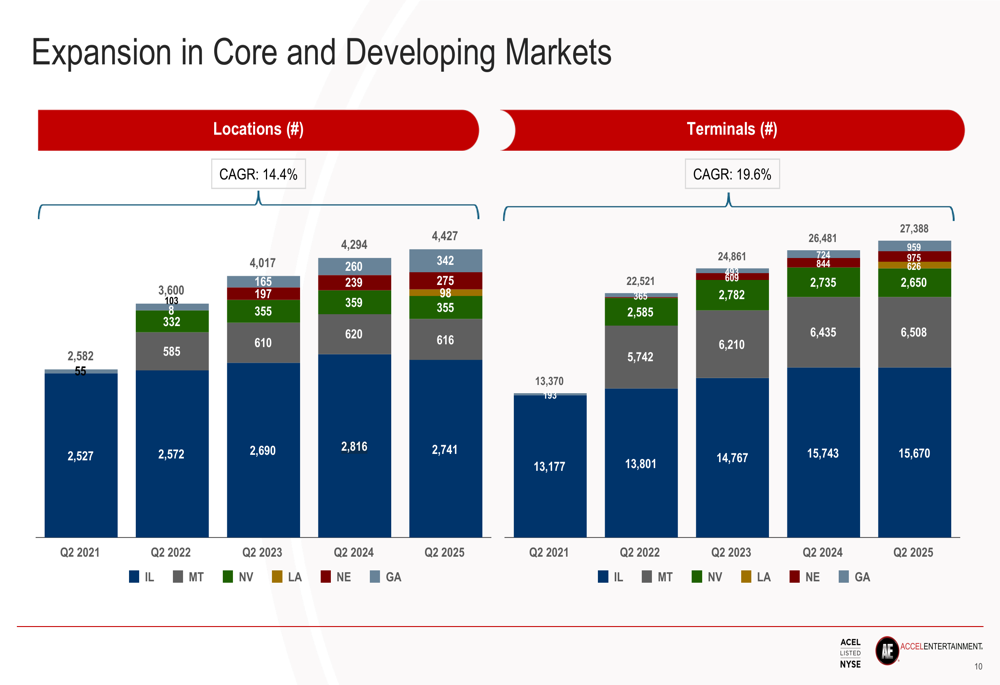

Accel’s expansion strategy has yielded mixed results across its six-state footprint. The company now operates 27,388 gaming terminals across 4,427 locations, representing year-over-year increases of 3% for both metrics.

The company’s expansion trajectory is clearly illustrated in the following chart:

Illinois remains Accel’s largest market, generating $245 million in Q2 revenue, an 8% increase year-over-year. Emerging markets showed strong growth, with Nebraska revenue up 26% to $8 million and Georgia revenue surging 53% to $5 million.

However, the company faced challenges in Montana and Nevada, where revenues declined 6% and 8% respectively. Louisiana operations, which commenced recently, contributed $10 million to quarterly revenue.

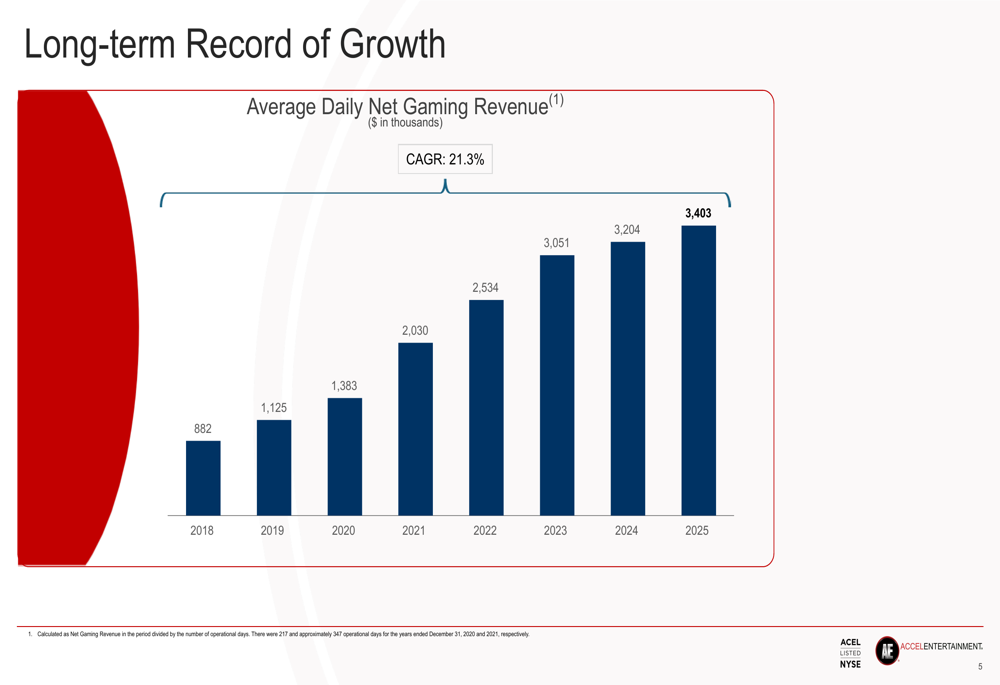

The company’s long-term growth trajectory in average daily net gaming revenue shows a consistent upward trend:

Capital Allocation Strategy

Accel continues to balance growth investments with shareholder returns. Capital expenditures totaled $26 million in Q2 2025, a 49% increase from Q2 2024, with the company affirming its full-year CapEx forecast of $75-80 million.

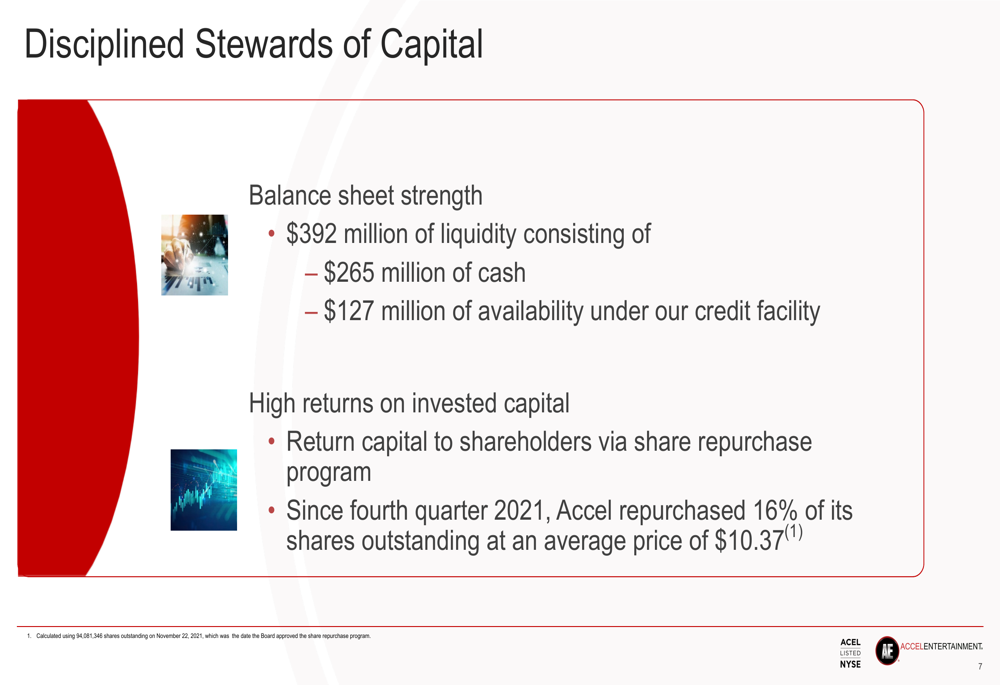

The company highlighted its disciplined approach to capital management, maintaining $392 million in liquidity, including $265 million in cash and $127 million in credit facility availability. Net debt increased 6% year-over-year to $331 million.

As illustrated in the company’s capital management overview:

Accel has continued its share repurchase program, buying back $7 million of Class A-1 Common Stock in Q2 2025. Since launching the program in November 2021, the company has repurchased 16% of its outstanding shares at an average price of $10.37, totaling $160 million.

A significant milestone in Q2 was the commencement of casino and racing operations at Fairmount Park Casino (EPA:CASP) & Racing in April 2025, representing a major capital investment for the company.

Revenue and EBITDA Trends

Accel’s presentation highlighted its consistent financial performance over time, with steady growth in both revenue and Adjusted EBITDA across multiple quarters:

The company’s financial model is built on contracted, recurring revenue streams, providing visibility into future performance. Accel emphasized its long-term agreements with location partners as a key strength of its business model.

Forward-Looking Statements

Looking ahead, Accel remains focused on expansion in both core and developing markets. The company’s presentation emphasized its position as a leader in the growing local gaming segment with significant untapped potential.

The company’s turn-key solution provider model continues to drive growth, with Accel now operating 27,388 gaming terminals across 4,427 locations in six states as of June 30, 2025:

Accel’s Q2 results reflect its ongoing geographic diversification strategy, reducing reliance on any single market while pursuing growth opportunities across multiple states. While the company faces challenges in some established markets like Montana and Nevada, strong performance in Illinois and rapid growth in emerging markets like Georgia suggest potential for continued expansion.

The significant capital expenditures forecast for 2025 ($75-80 million) indicate Accel’s commitment to growth investments, particularly in the Fairmount Park operation, while the company’s share repurchase program demonstrates confidence in its long-term value proposition.

Investors will be watching whether Accel can maintain its revenue growth trajectory while improving net income performance in coming quarters, particularly as newer markets like Louisiana mature and capital investments begin generating returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.