Gold prices dip as December rate cut bets wane; economic data in focus

Introduction & Market Context

Archer-Daniels-Midland Company (NYSE:ADM) presented its second-quarter 2025 earnings results on August 5, showing declining performance across key metrics amid challenging market conditions. The agricultural processing giant reported a 10% year-over-year decrease in both adjusted earnings per share and total segment operating profit, yet maintained its full-year outlook at the time.

The presentation came just three months before ADM would ultimately revise its guidance downward following its Q3 results, when the company lowered its full-year 2025 EPS guidance to $3.25-$3.50 from the approximately $4.00 projected in this Q2 presentation.

Quarterly Performance Highlights

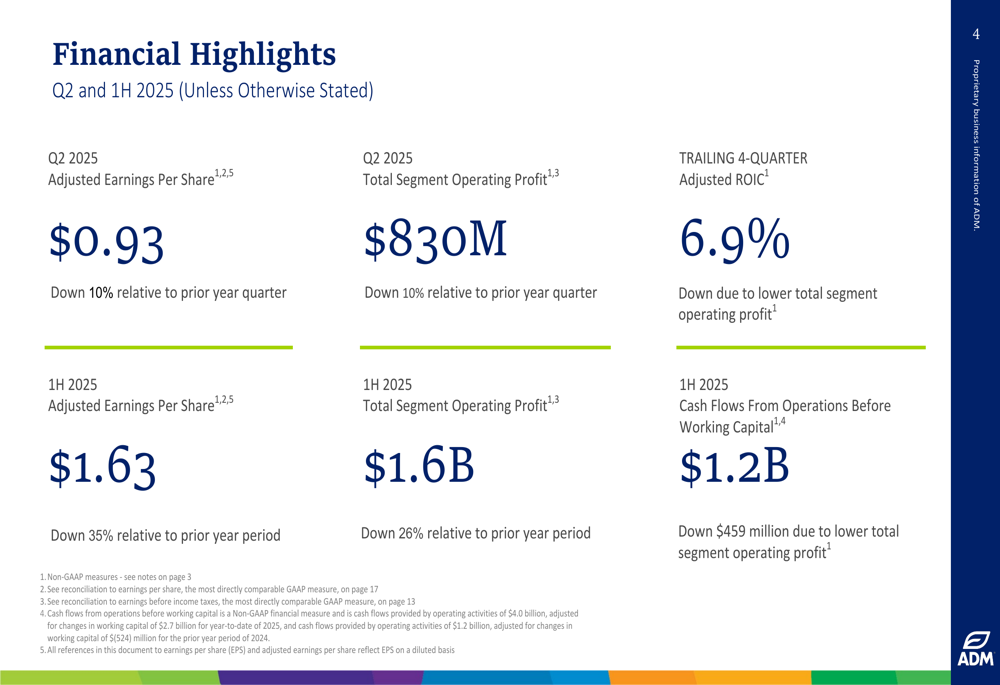

ADM’s second-quarter financial performance showed significant pressure across most business segments, with adjusted earnings per share of $0.93, down 10% from the prior year quarter. Total segment operating profit also declined 10% to $830 million.

As shown in the following financial highlights chart:

For the first half of 2025, the company reported adjusted EPS of $1.63, representing a steeper 35% decline compared to the same period in 2024. First-half total segment operating profit fell 26% to $1.6 billion. The company’s trailing four-quarter adjusted return on invested capital (ROIC) stood at 6.9%, below its long-term target of 10%.

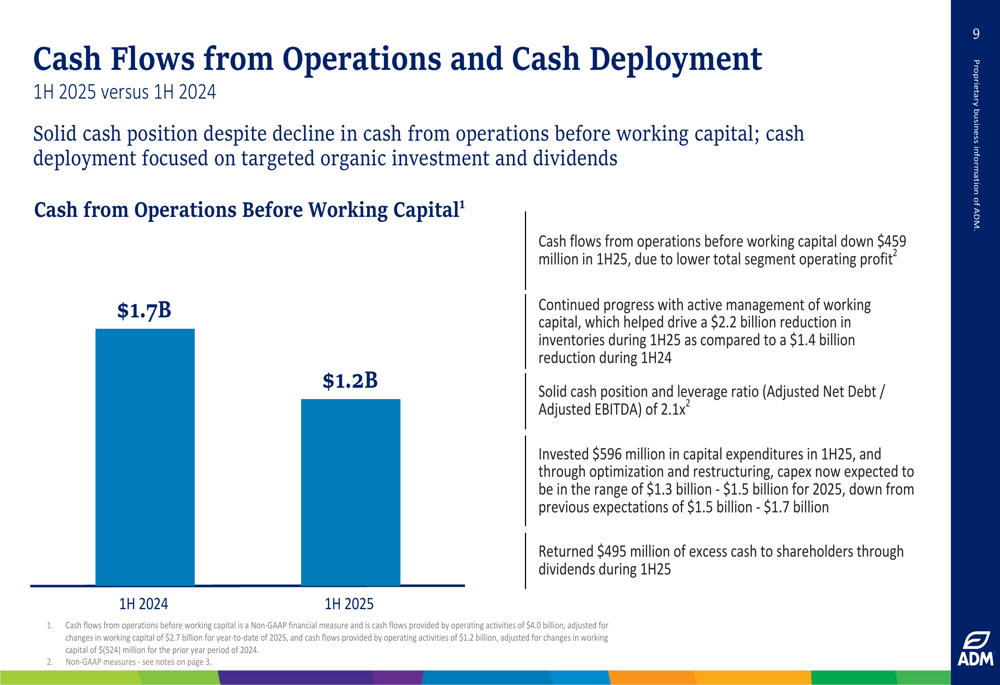

Cash flows from operations before working capital changes declined to $1.2 billion for the first half of 2025, down $459 million from the prior year, primarily due to lower operating profits.

Detailed Financial Analysis

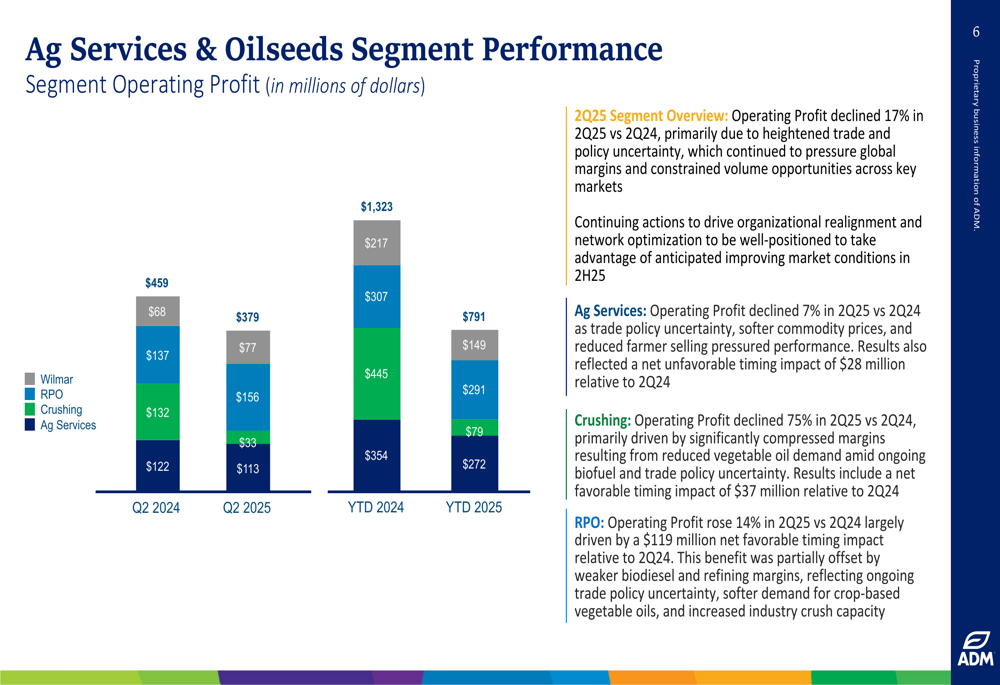

ADM’s Ag Services & Oilseeds segment, typically its largest profit contributor, faced significant headwinds with operating profit declining 17% in Q2 2025 compared to Q2 2024. The company attributed this to "heightened trade and policy uncertainty." Within this segment, crushing operations were particularly hard hit, with operating profit plummeting 75% year-over-year due to "significantly compressed margins."

The segment breakdown reveals the extent of these challenges:

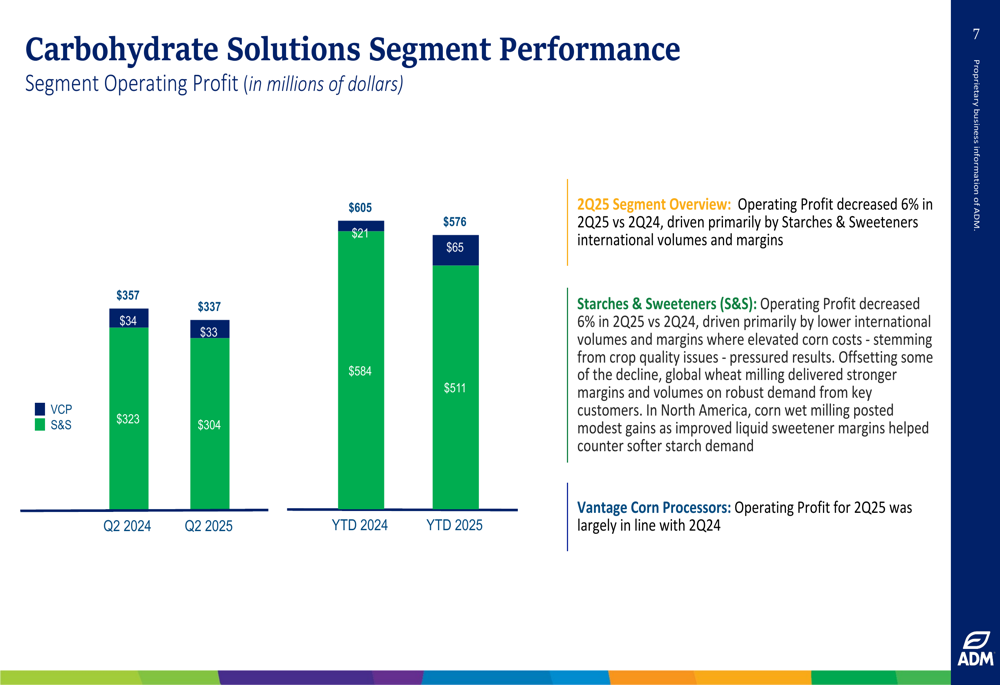

The Carbohydrate Solutions segment also experienced pressure, with operating profit decreasing 6% in Q2 2025 versus Q2 2024. This decline was primarily driven by lower international volumes and margins in the Starches & Sweeteners business.

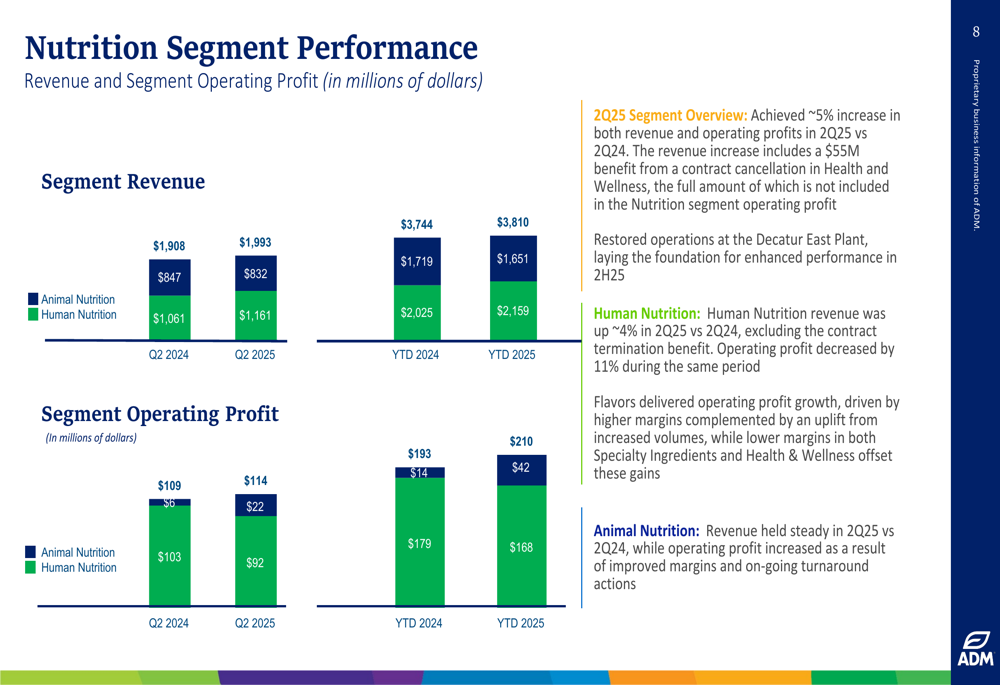

The bright spot in ADM’s portfolio was the Nutrition segment, which achieved approximately 5% increases in both revenue and operating profits compared to the prior year quarter. Human Nutrition revenue grew by about 4% (excluding a contract termination benefit), though operating profit decreased by 11%. Animal Nutrition revenue remained steady while operating profit improved due to better margins.

Strategic Initiatives

ADM emphasized its "self-help" strategy focused on four key areas: execution and cost focus, simplification, targeted organic growth investment, and capital discipline. The company highlighted several initiatives including network optimization in South and North America Nutrition Operations and the recommissioning of its Decatur East facility.

The company made significant progress in working capital management, driving a $2.2 billion reduction in inventories during the first half of 2025. This helped maintain a solid cash position with a leverage ratio (Adjusted Net Debt/Adjusted EBITDA) of 2.1x.

As shown in the cash flow and deployment slide:

ADM invested $596 million in capital expenditures during the first half of 2025 and projected full-year capex to be between $1.3 billion and $1.5 billion. The company continued its shareholder returns, paying $495 million in dividends during the first half of the year and announcing its 374th consecutive quarterly dividend.

Forward-Looking Statements

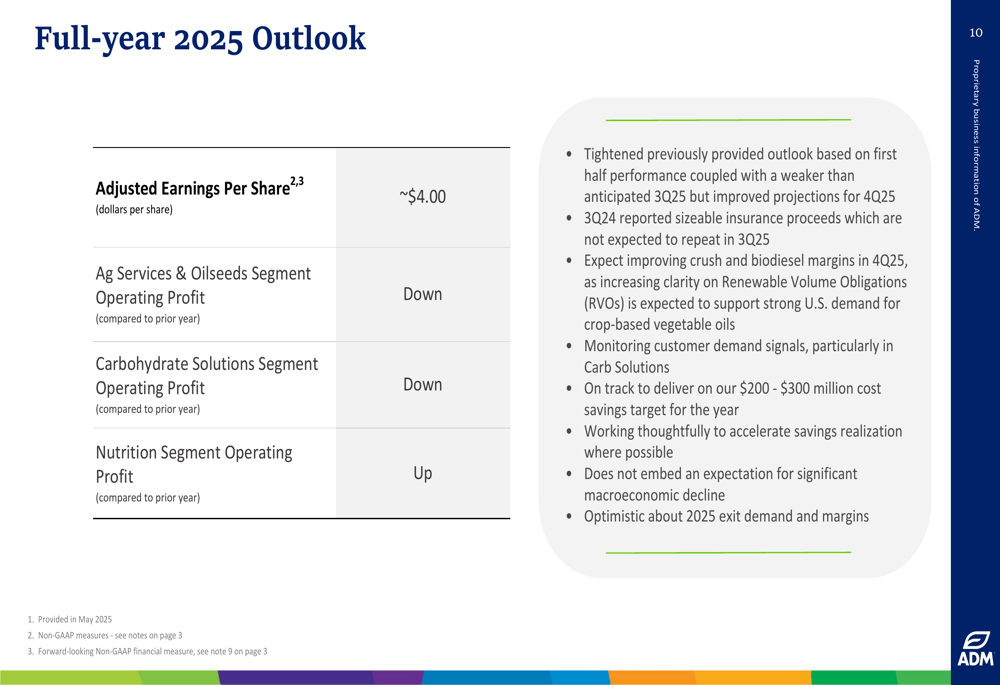

At the time of the Q2 presentation, ADM maintained its full-year 2025 adjusted earnings per share outlook of approximately $4.00, despite the challenging first half. The company expected improving crush and biodiesel margins in the fourth quarter and remained on track to deliver $200-300 million in cost savings for the year.

However, this outlook would prove optimistic. In its subsequent Q3 2025 earnings report on November 4, ADM significantly lowered its full-year EPS guidance to a range of $3.25-$3.50, citing continued industry challenges and market volatility. This downward revision triggered a 6.51% drop in the company’s stock price in premarket trading, with shares falling to $56.18.

Despite the near-term challenges, ADM’s management expressed optimism about future market conditions. During the Q3 earnings call, CEO Juan Luciano stated, "We look at 2026 and 2027 with a lot of optimism," suggesting confidence in the company’s long-term strategy despite current headwinds.

The company faces ongoing uncertainty in U.S. biofuel policy and China trade deals, softness in sweeteners and starches demand, and potential seasonal weakness in the Nutrition segment. Nevertheless, ADM continues to focus on innovation in areas such as next-generation flavor systems and postbiotics as part of its long-term growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.