Gold prices jump to near 3-week high amid US shutdown progress

Introduction & Market Context

Advanced Drainage Systems Inc (NYSE:WMS) reported strong financial results for its second quarter of fiscal year 2026 during its earnings presentation on November 6, 2025. The water management solutions leader delivered robust growth despite mixed market conditions, with shares surging 8.91% in premarket trading to $146.74 following the announcement.

The company’s performance comes amid varying demand across its key markets, with non-residential construction showing strength while agricultural and infrastructure segments faced headwinds. ADS maintained a stable pricing environment while effectively managing costs, contributing to significant margin expansion.

Quarterly Performance Highlights

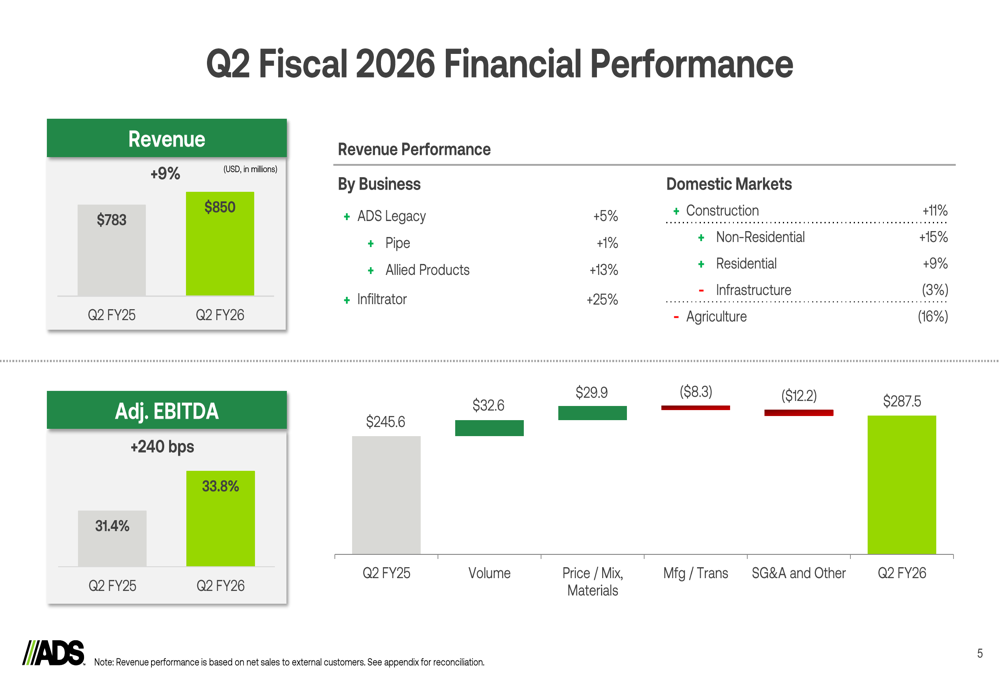

ADS reported Q2 FY2026 revenue of $850 million, representing a 9% increase from $783 million in the same period last year. This performance exceeded analyst expectations of $802.54 million. The company’s earnings per share reached $1.97, surpassing forecasts of $1.64 by 20.12%.

The revenue growth was driven by strong performance across multiple segments, with Allied Products up 13% and Infiltrator Water Technologies showing impressive 25% growth. The company’s core pipe business grew by a more modest 1%.

As shown in the following chart of quarterly revenue performance by segment:

Adjusted EBITDA margin expanded significantly to 33.8%, representing a 240 basis point improvement over the prior year’s 31.4%. This margin expansion was primarily driven by favorable volume, price/cost dynamics, and a beneficial mix of higher-margin Allied products and Infiltrator solutions.

The following waterfall chart illustrates the key factors contributing to EBITDA growth:

Detailed Financial Analysis

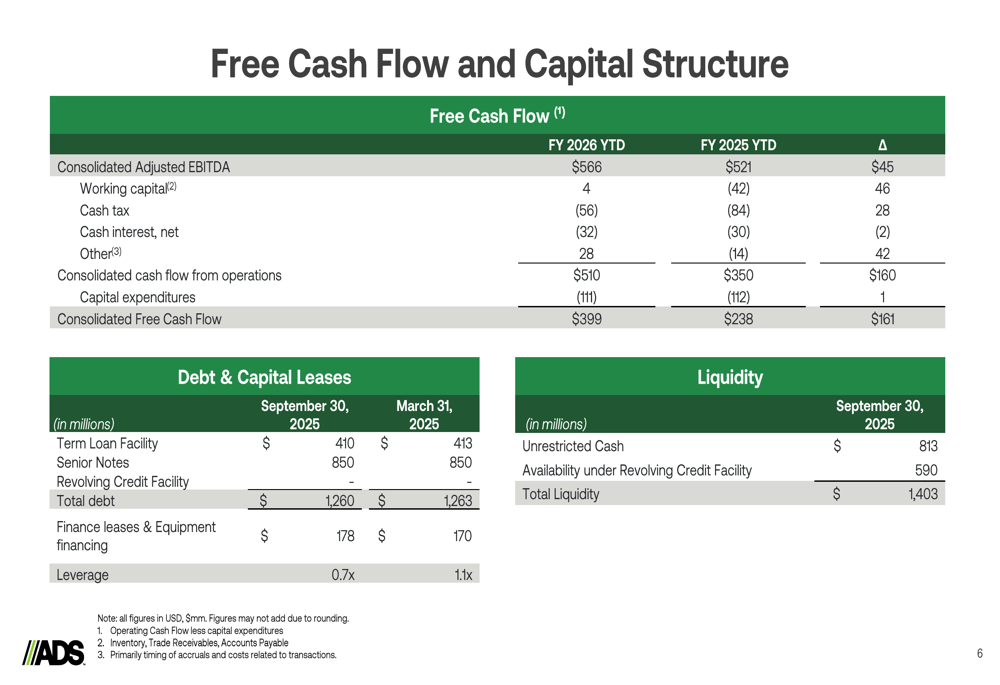

ADS demonstrated strong cash generation capabilities, with consolidated free cash flow reaching $399 million year-to-date, a substantial $161 million increase from the prior year. This improvement reflects both higher profitability and effective working capital management.

The company maintains a strong balance sheet with total debt of $1,260 million and a conservative leverage ratio of 0.7x. Unrestricted cash stands at $813 million, providing substantial liquidity of $1,403 million to support growth initiatives and the recently announced acquisition.

The financial position is detailed in the following capital structure overview:

Market performance varied significantly across segments. The domestic construction market showed resilience with 11% growth, driven by non-residential (+15%) and residential (+9%) strength. However, infrastructure declined by 3% and the agricultural segment faced more significant challenges with a 16% decline.

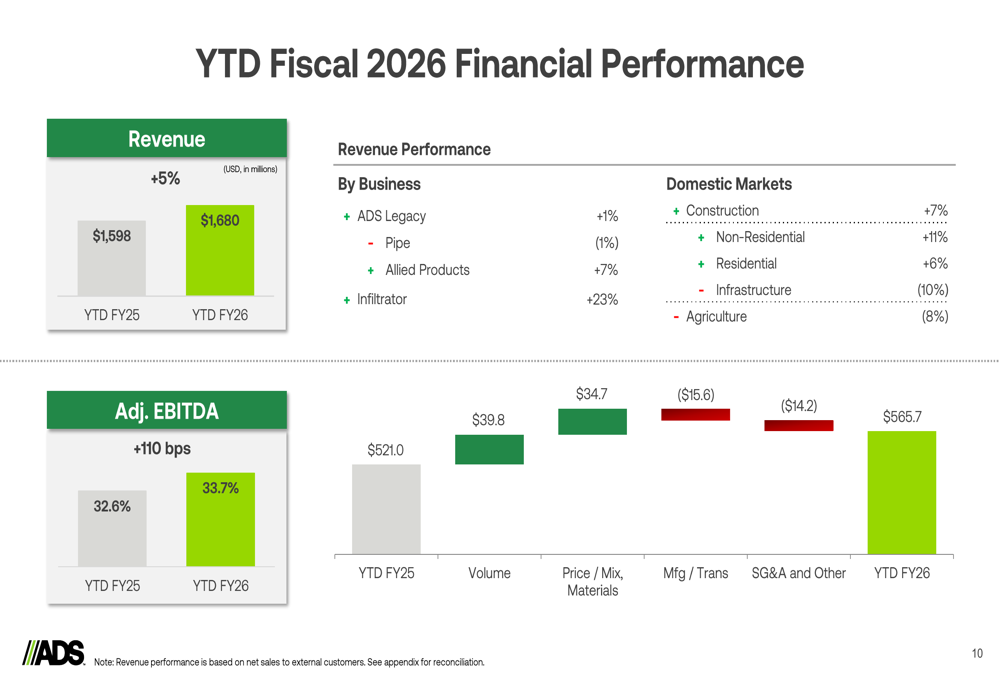

Year-to-date performance follows similar trends, with the company achieving 5% overall revenue growth to $1.68 billion and maintaining strong adjusted EBITDA margins of 33.7%.

Strategic Initiatives

The most significant strategic development announced during the presentation was the acquisition of NDS from Norma Group SE (DAX:NOEJ) for $1.0 billion. This acquisition, expected to close in the first quarter of calendar year 2026, represents a major expansion of ADS’s product portfolio and market reach.

CEO Scott Barbour highlighted the company’s continued execution in a challenging environment, stating, "We continue to execute effectively in a challenging environment," while CFO Scott Cottrill emphasized the company’s focus on margin improvement, noting, "We see a lot of different reasons why we can continue to accrete [margins] as we move forward."

The presentation also referenced the successful integration of the Orenco acquisition, which has contributed to the strong performance of the Infiltrator segment. The company’s strategic focus on high-margin Allied products such as StormTech chambers, Nyloplast basins, and Water Quality solutions has driven significant growth in this segment.

Forward-Looking Statements

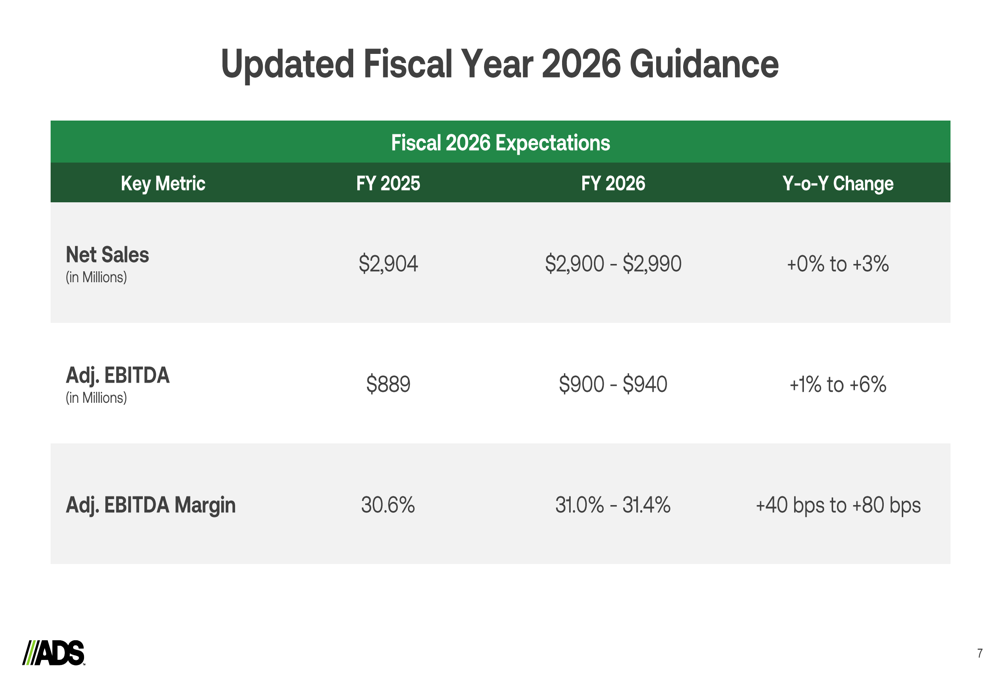

ADS maintained its full-year guidance with slight adjustments, projecting net sales of $2.900-$2.990 billion (0% to +3% growth) and adjusted EBITDA of $900-$940 million (+1% to +6% growth). The adjusted EBITDA margin is expected to improve by 40 to 80 basis points to 31.0%-31.4%.

The guidance details are presented in the following table:

The company provided a mixed outlook for market demand, expecting non-residential markets to be flat to down low-single digits, residential markets down low- to mid-single digits, infrastructure up low-single digits, and agriculture and international markets down double digits.

Despite these varying market conditions, management expressed confidence in their ability to navigate challenges through continued focus on high-margin products, operational efficiency, and strategic acquisitions. The NDS acquisition is expected to further strengthen the company’s market position and provide additional growth opportunities once completed in early 2026.

Potential risks identified include the impact of a possible government shutdown, seasonal challenges in winter months, mixed performance in the residential market due to interest rate impacts, challenges in the DIY channel, and ongoing logistics optimization efforts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.