US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Air Lease Corporation (NYSE:AL) presented its first quarter 2025 investor presentation highlighting the company’s strong performance and strategic positioning in a growing aircraft leasing market. The presentation comes after AL reported Q1 earnings that significantly beat analyst expectations, with EPS of $1.51 versus forecasts of $0.89 and revenue of $738 million compared to expected $713.85 million.

The company operates in a favorable industry environment where leasing’s market share of aircraft financing has grown dramatically from just 2.2% in 1970 to 50.6% in 2025, as airlines increasingly prefer leasing over direct ownership.

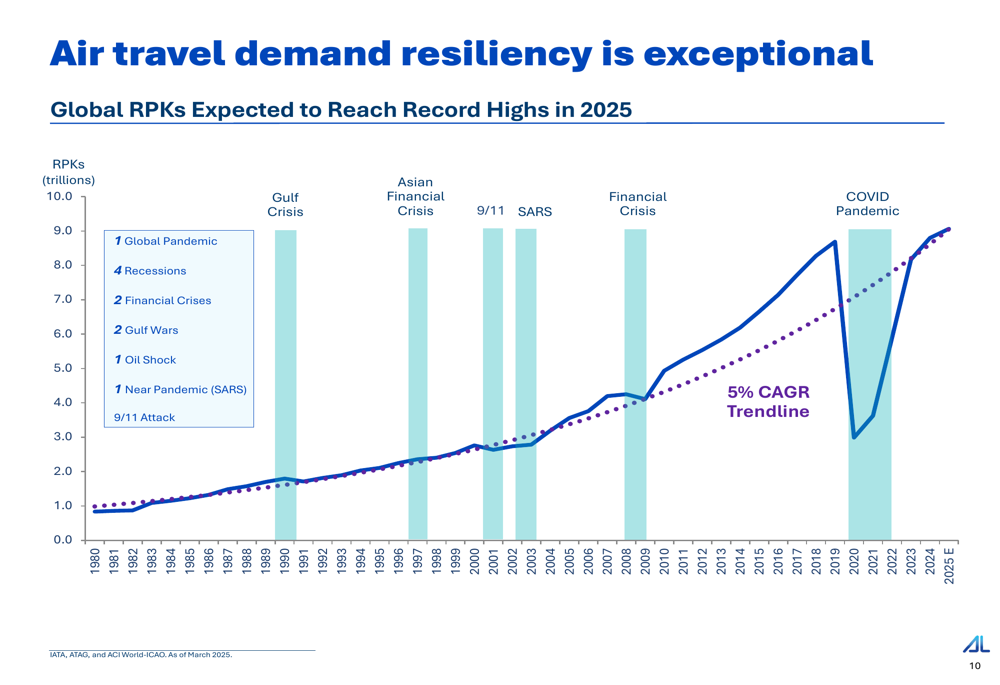

As shown in the following chart illustrating the historical resilience of air travel demand, global Revenue Passenger Kilometers (RPKs) are expected to reach record highs in 2025, continuing the long-term growth trend despite historical disruptions:

Executive Summary

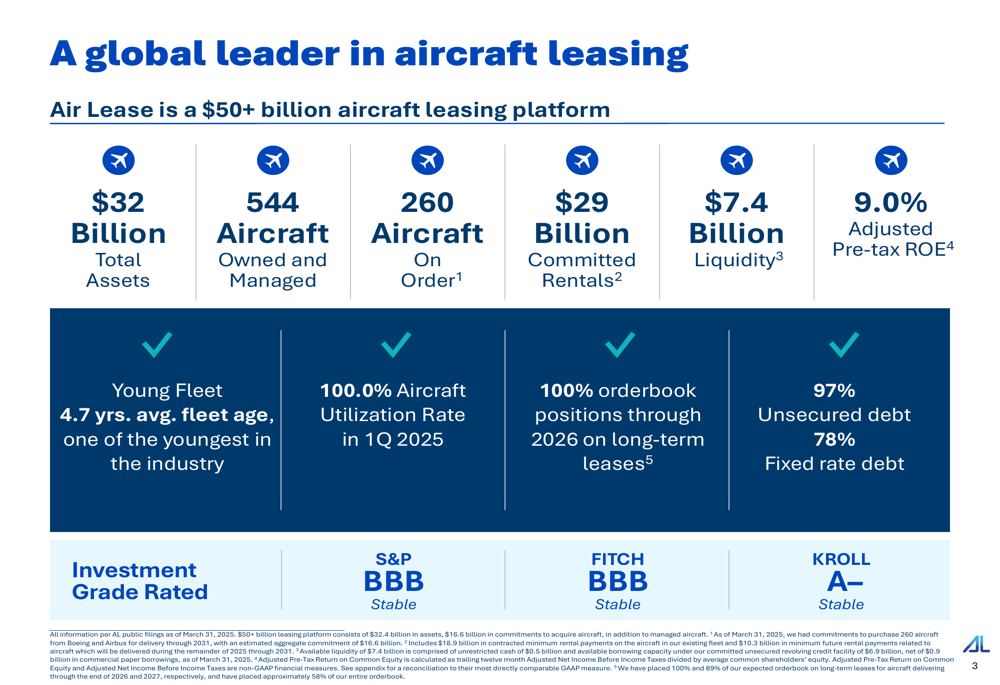

Air Lease reported strong fundamentals as of March 31, 2025, with $32 billion in assets, 544 aircraft owned and managed, and 260 aircraft on order. The company maintained perfect 100% fleet utilization in Q1 2025, continuing its impressive track record of operational efficiency.

The following overview highlights AL’s key financial metrics and operational strengths:

The company’s business model focuses on purchasing new aircraft directly from manufacturers at significant discounts, holding them for approximately the first third of their useful life, and then selling them to reinvest capital. Since going public in 2011, Air Lease has purchased over $48 billion in aircraft, generated more than $15 billion in operating cash flow, and sold over $9 billion in aircraft.

Fleet and Orderbook Strategy

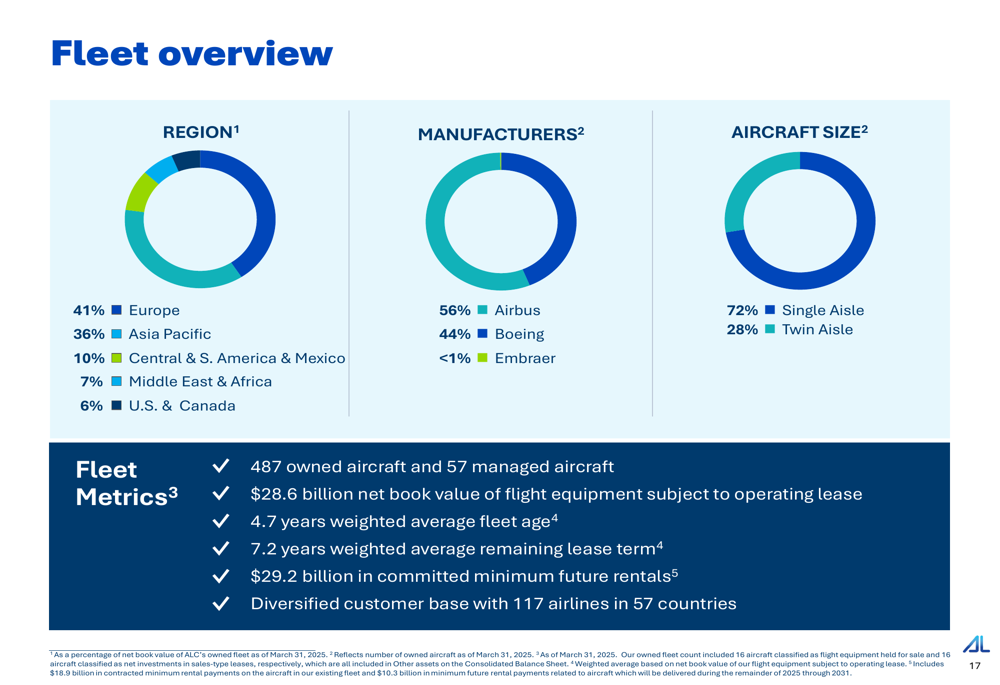

Air Lease maintains a geographically diverse fleet with 487 owned aircraft and 57 managed aircraft as of Q1 2025. The company’s portfolio is strategically balanced across regions, with 41% allocated to Europe, 36% to Asia Pacific, and the remainder distributed across other global markets.

The following chart illustrates the company’s fleet distribution by region, manufacturer, and aircraft type:

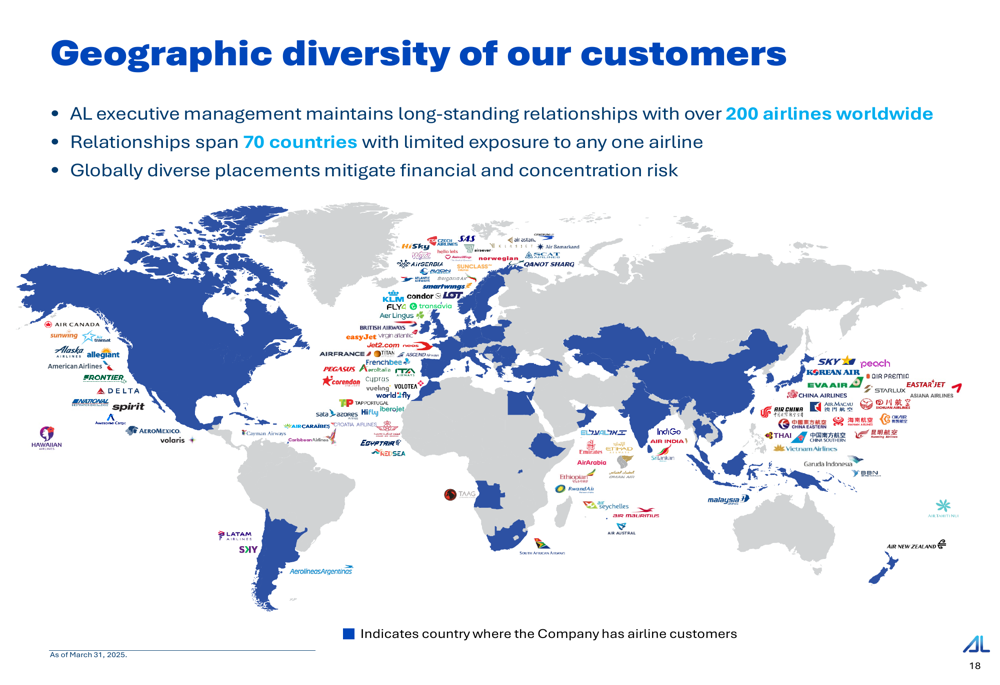

A key strength of Air Lease’s business model is its global customer reach, which helps mitigate concentration risk. The company maintains relationships with over 200 airlines across 70 countries, providing significant flexibility in aircraft placement.

As shown in the following world map highlighting AL’s customer base:

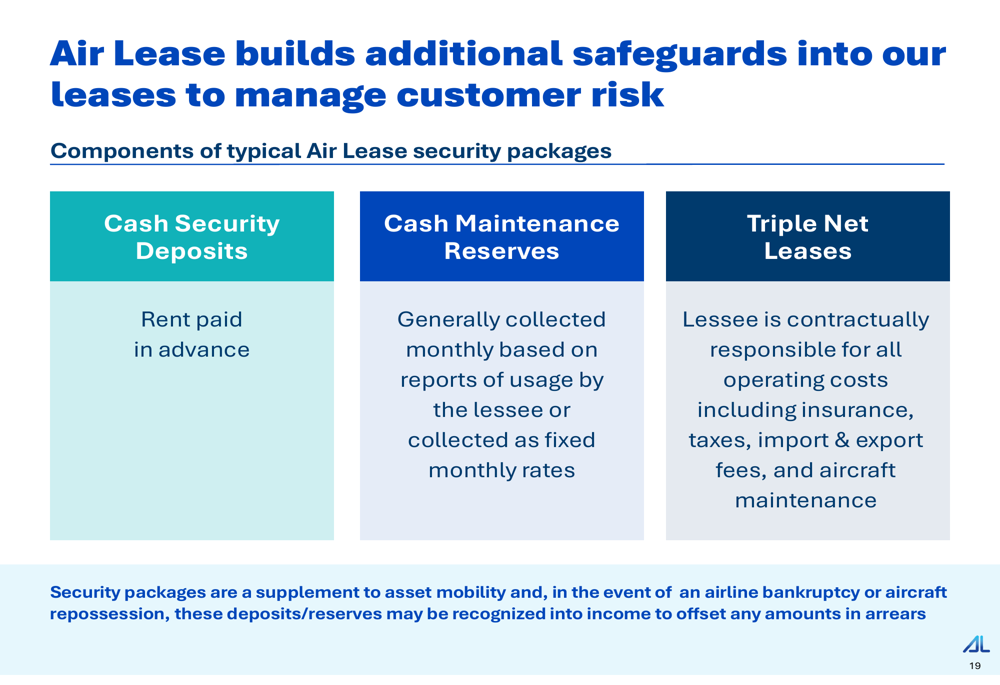

Air Lease has built significant safeguards into its leases to manage customer risk, including cash security deposits, maintenance reserves, and triple net lease structures. These protections supplement the inherent mobility of aircraft assets and provide financial buffers in case of airline bankruptcies or repossessions.

Financial Performance Highlights

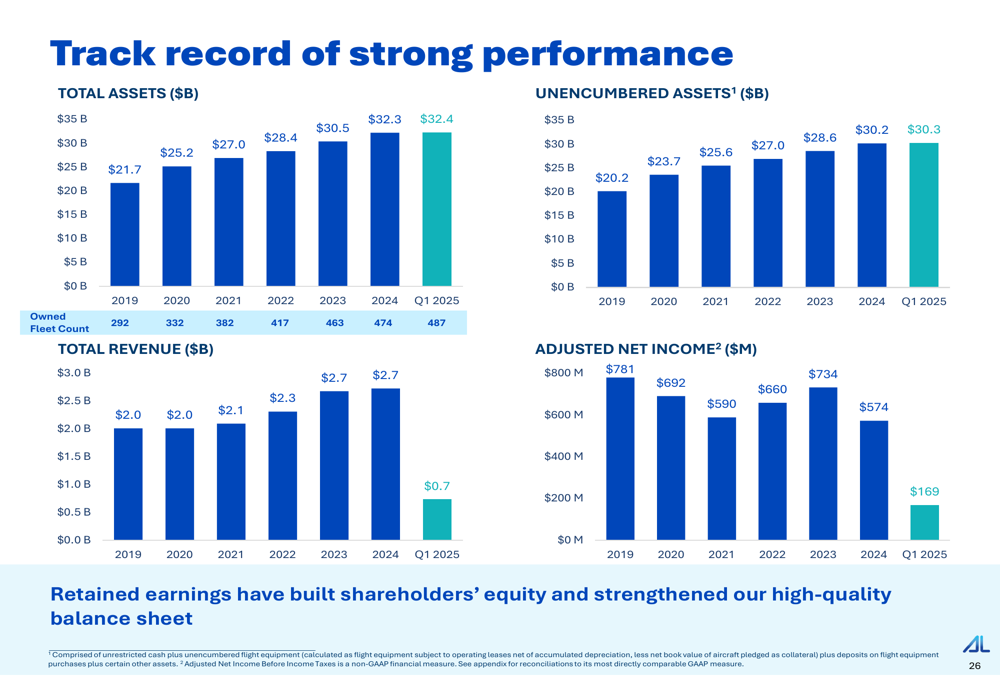

Air Lease has demonstrated consistent financial growth over the years. Total (EPA:TTEF) assets have increased from $21.7 billion in 2019 to $32.4 billion in Q1 2025, while the owned fleet has grown from 292 to 487 aircraft during the same period.

The following chart shows AL’s financial performance trajectory:

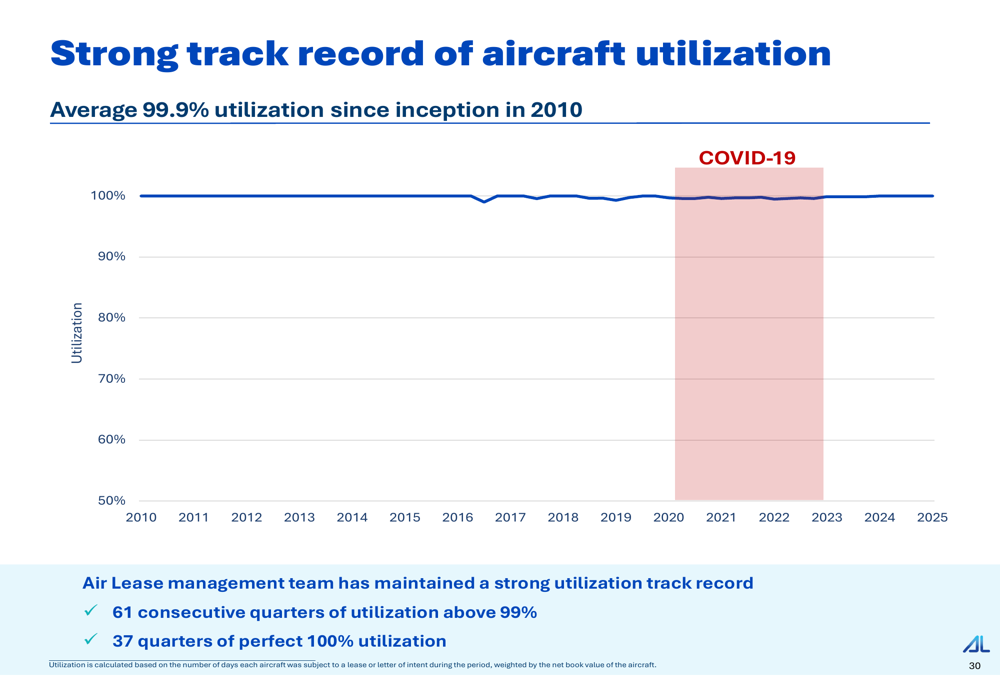

A particularly impressive aspect of Air Lease’s operational performance is its aircraft utilization track record. The company has maintained an average utilization rate of 99.9% since inception in 2010, with 61 consecutive quarters above 99% and 37 quarters at a perfect 100%.

Looking ahead, Air Lease expects significant improvement in its portfolio yield. The company anticipates a 150-200 basis point improvement from 2025 through the end of 2028, driven by increasing yields on new deliveries and extensions, the roll-off of COVID-era leases, and the natural seasoning of the portfolio.

Capital Structure and Liquidity

Air Lease maintains a strong capital structure with investment-grade ratings from major agencies (S&P:BBB, Fitch: BBB, Kroll: A-). The company has strategically shifted toward unsecured debt, which now comprises 97% of its debt portfolio, up from just 15% in 2010.

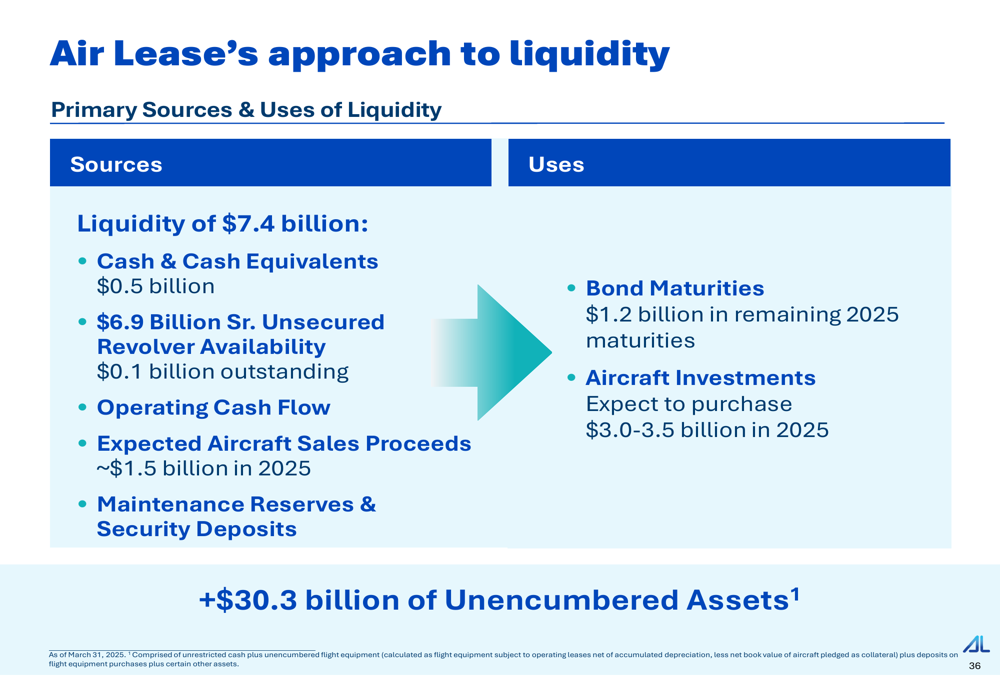

The company’s approach to liquidity is comprehensive, with multiple sources including $0.5 billion in cash and cash equivalents, $6.9 billion in revolving credit facility availability, operating cash flow, and expected aircraft sales proceeds of approximately $1.5 billion in 2025.

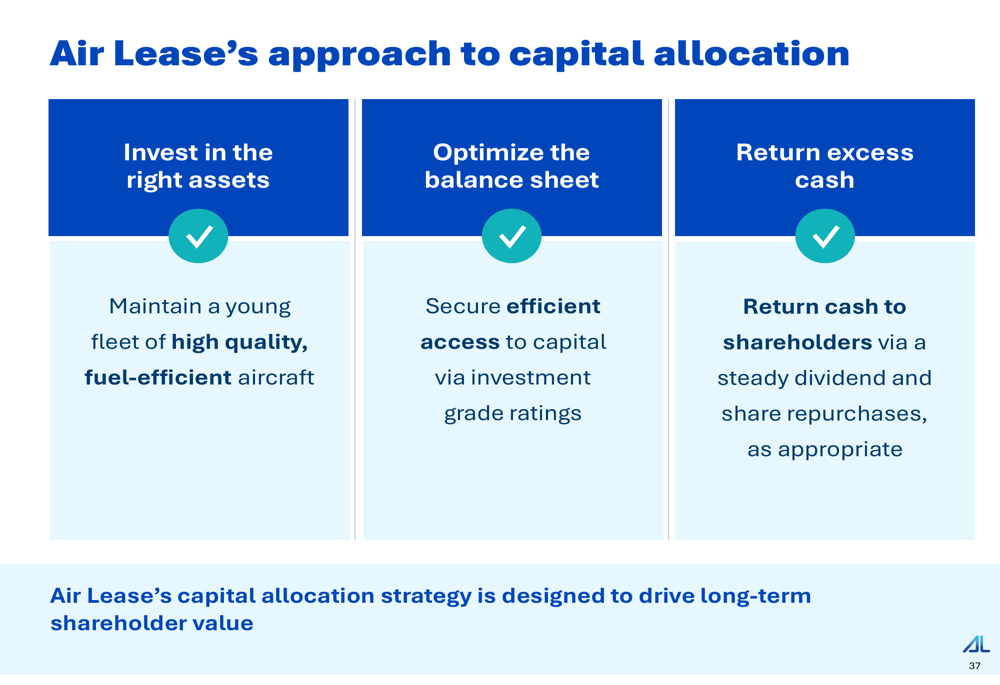

Air Lease’s capital allocation strategy focuses on three key areas: investing in the right assets to maintain a young, fuel-efficient fleet; optimizing the balance sheet to secure efficient access to capital; and returning excess cash to shareholders through dividends and share repurchases.

Forward-Looking Statements

Air Lease is well-positioned to benefit from several secular tailwinds in the aviation industry. The company expects continued growth in global air travel demand driven by the expanding middle class, particularly in Asia, and shifting consumer preferences toward experiences over goods.

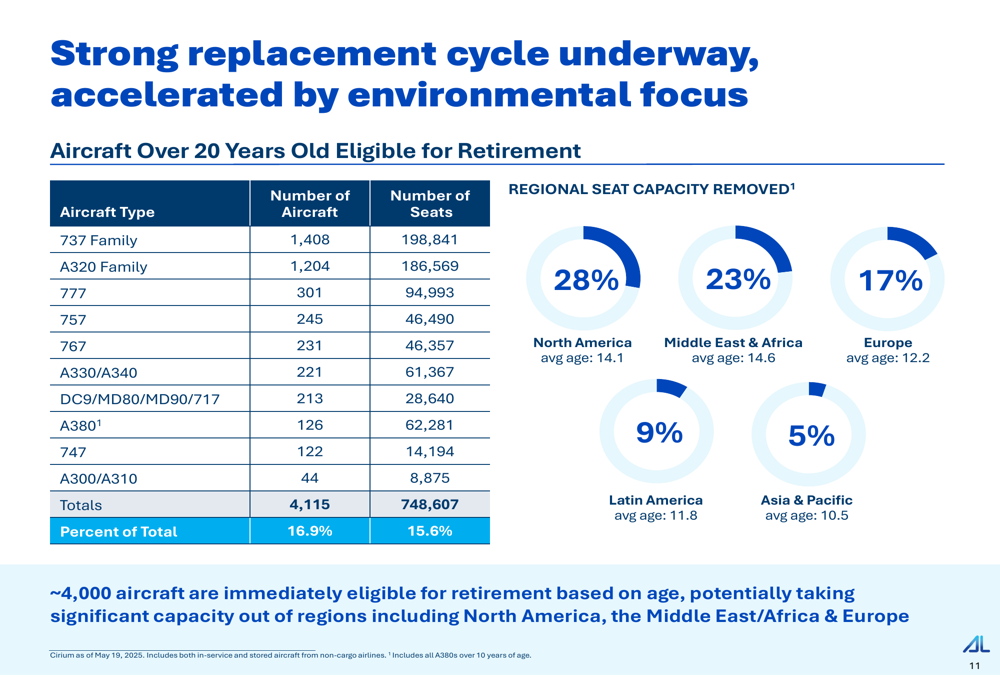

Additionally, the aircraft replacement cycle presents significant opportunities, with approximately 4,115 aircraft over 20 years old eligible for retirement, representing 16.9% of the global fleet.

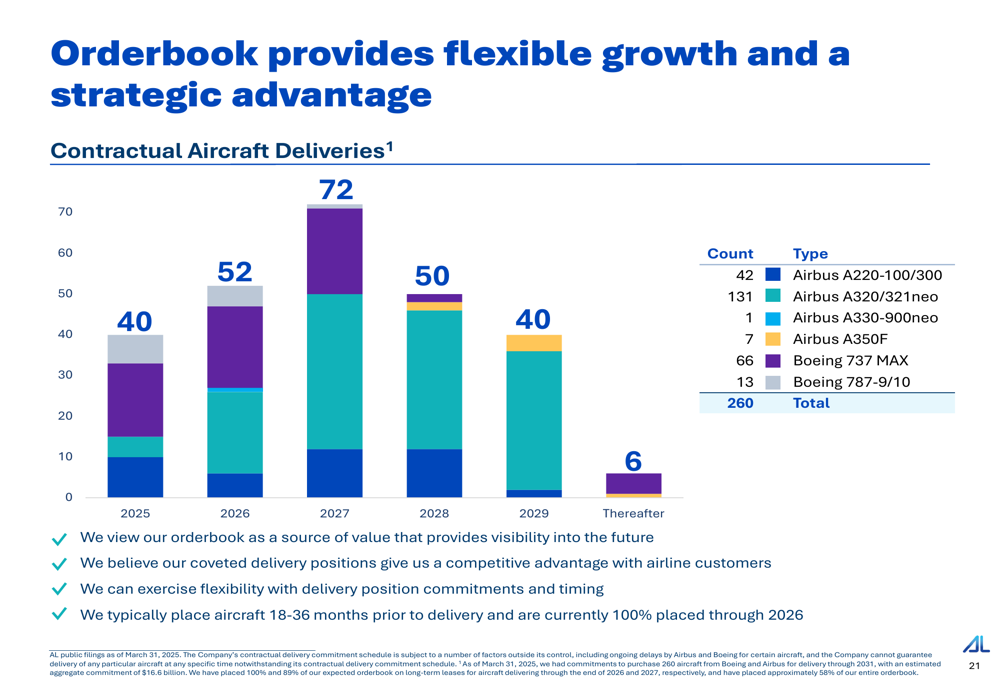

The company’s orderbook provides visibility into future growth, with 100% of expected aircraft deliveries through 2026 already placed on long-term leases. Air Lease plans to take delivery of 40 aircraft in 2025, 52 in 2026, and 72 in 2027.

In the Q1 2025 earnings call, CEO John Plueger expressed confidence in the company’s trajectory, stating, "We remain very positive about Air Lease’s prospects for 2025 and beyond." This optimism is supported by the company’s strong Q1 performance and strategic positioning in a growing market.

As of July 3, 2025, Air Lease’s stock was trading at $58.93, up 0.67% for the day and near its 52-week high of $59.95, reflecting investor confidence in the company’s strategy and execution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.