September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Air Products and Chemicals Inc. (NYSE:APD) reported its fiscal third quarter 2025 results on July 31, 2025, highlighting sequential improvement in performance while unveiling a strategic shift toward its core industrial gases business. The company’s stock responded positively, rising 1.68% to $295 in premarket trading, according to available market data, after having closed at $290.13 the previous day.

The industrial gas giant’s presentation emphasized resilience in its core operations despite ongoing macroeconomic headwinds, a notable improvement from its challenging second quarter when the company missed earnings expectations and saw its stock drop nearly 5%.

Quarterly Performance Highlights

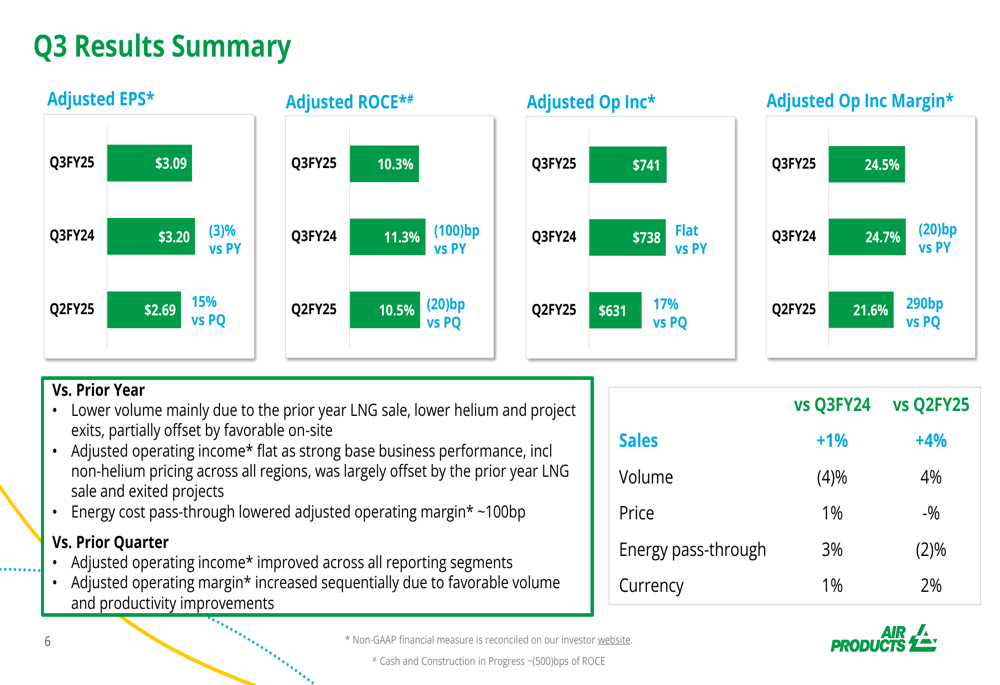

Air Products reported third-quarter adjusted earnings per share of $3.09, representing a 3% decline compared to the prior year but a significant 15% improvement from the second quarter. The company emphasized that these results exceeded its guidance for the quarter.

As shown in the following comprehensive results summary:

The company maintained relatively stable adjusted operating income at $741 million, flat year-over-year but up 17% sequentially. Adjusted operating margin stood at 24.5%, down slightly from 24.7% in the same quarter last year but showing substantial improvement from 21.6% in Q2 FY2025.

Sales volume declined 4% compared to the prior year but increased 4% sequentially. The company attributed the year-over-year volume decline primarily to lower helium sales, partially offset by favorable on-site performance.

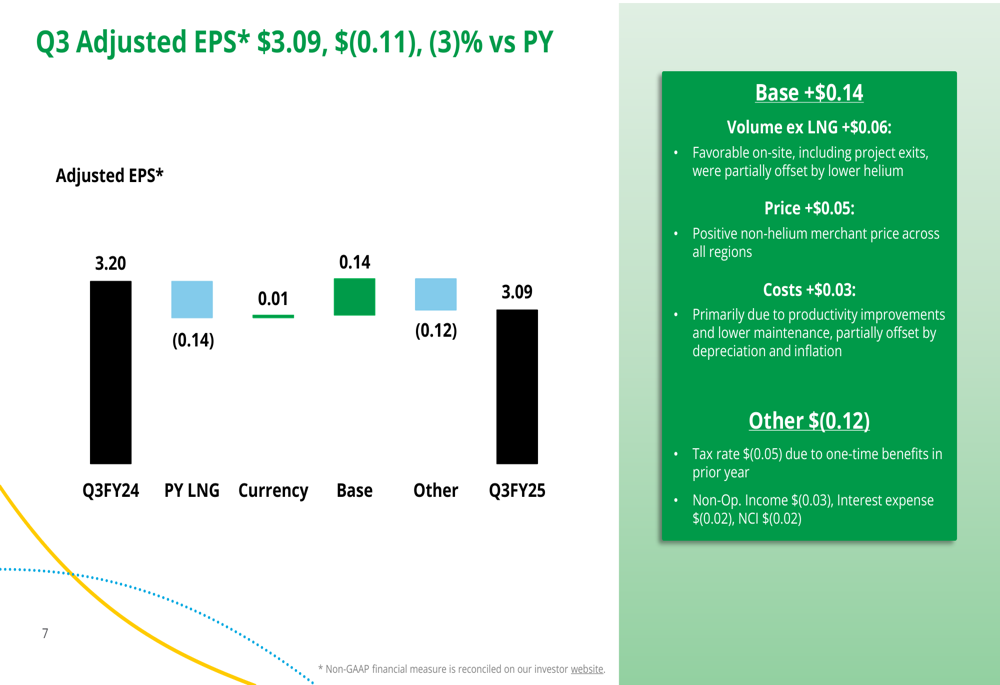

A detailed breakdown of the factors affecting the company’s adjusted EPS reveals both positive and negative influences:

The $0.11 year-over-year decline in adjusted EPS was primarily driven by the divestiture of the company’s LNG business (-$0.14) and other factors (-$0.12), partially offset by base business improvements (+$0.14) and modest currency benefits (+$0.01). Within the base business, Air Products achieved positive contributions from volume excluding LNG (+$0.06), pricing (+$0.05), and cost improvements (+$0.03).

Strategic Initiatives & 5-Year Roadmap

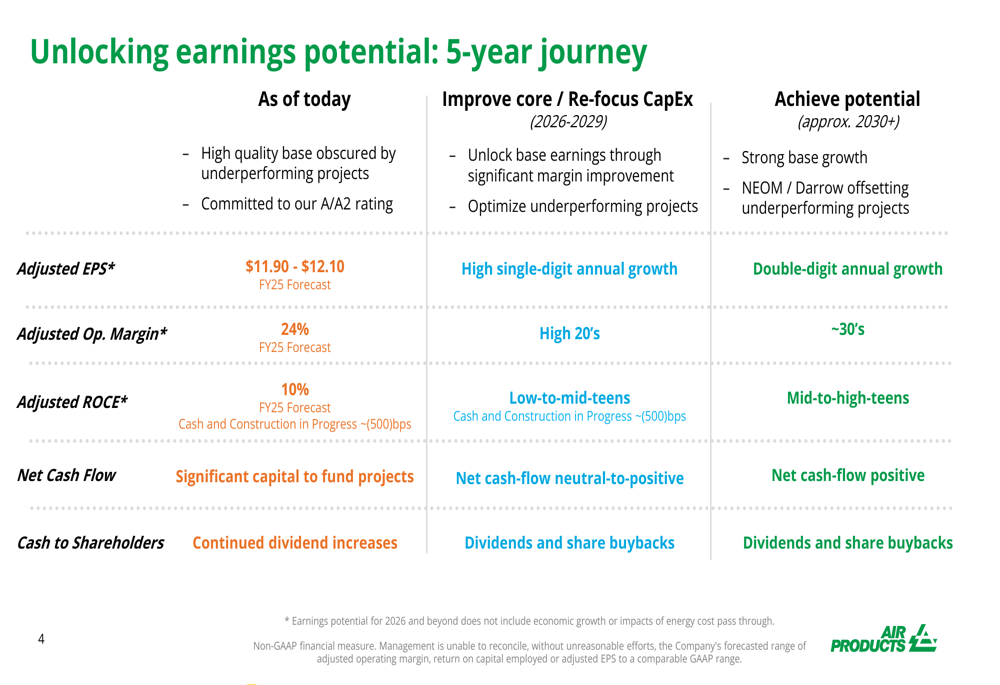

The centerpiece of Air Products’ presentation was its comprehensive 5-year strategic roadmap designed to unlock earnings potential through a renewed focus on its core industrial gases business and more disciplined capital allocation.

The company outlined its strategic approach as follows:

Air Products plans to focus on unlocking value through disciplined cost productivity, pricing optimization, operational excellence, and more rigorous capital allocation. The strategy includes finalizing current energy transition projects while redirecting investment toward core industrial gases projects, particularly in the electronics sector in Asia.

This strategic shift is mapped out in a detailed 5-year journey to improve financial performance:

The roadmap projects a progression from the current fiscal year 2025 forecast (adjusted EPS of $11.90-$12.10 and adjusted operating margin of 24%) to high single-digit annual growth during 2026-2029, followed by double-digit annual growth from approximately 2030 onward. Operating margins are expected to reach the high 20% range by 2026-2029 and approximately 30% by 2030+, while ROCE is projected to improve from the current 10% to mid-to-high teens by 2030+.

Notably, the company expects to transition from its current significant capital expenditure position to being net cash-flow neutral-to-positive by 2026-2029 and fully cash-flow positive by 2030+, enabling both continued dividend increases and share buybacks.

Regional Performance Analysis

Air Products’ performance varied significantly across regions, with Europe and Asia showing strength while the Americas faced some challenges.

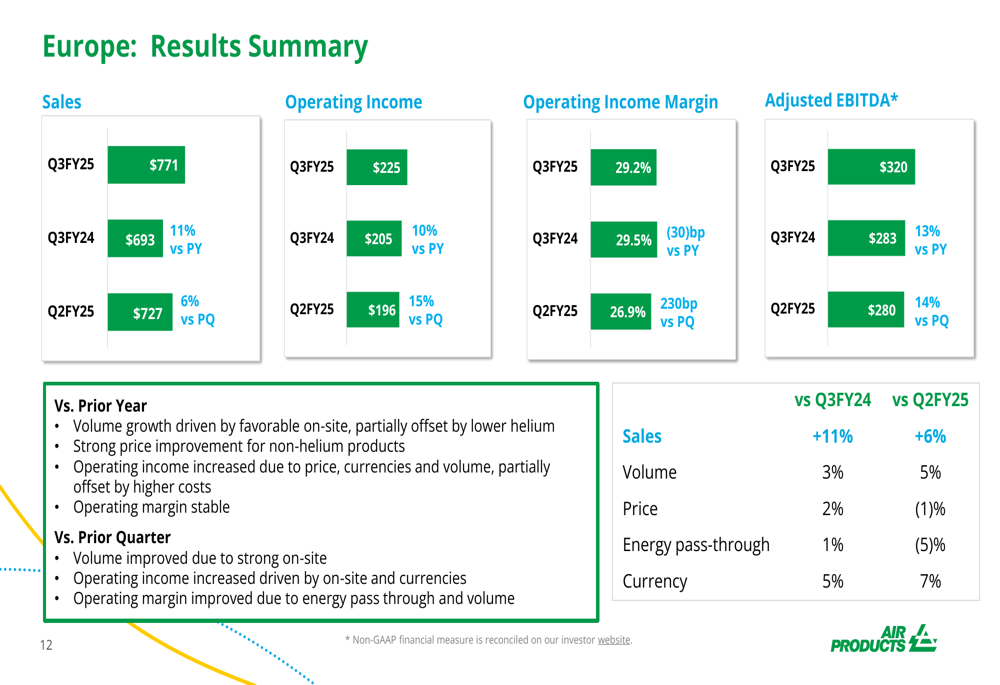

The European segment delivered particularly strong results:

European operations posted impressive 11% sales growth year-over-year, driven by 3% volume growth, 2% price improvement, and 5% favorable currency impact. Operating income increased 10% to $225 million, while adjusted EBITDA grew 13% to $320 million compared to the prior year.

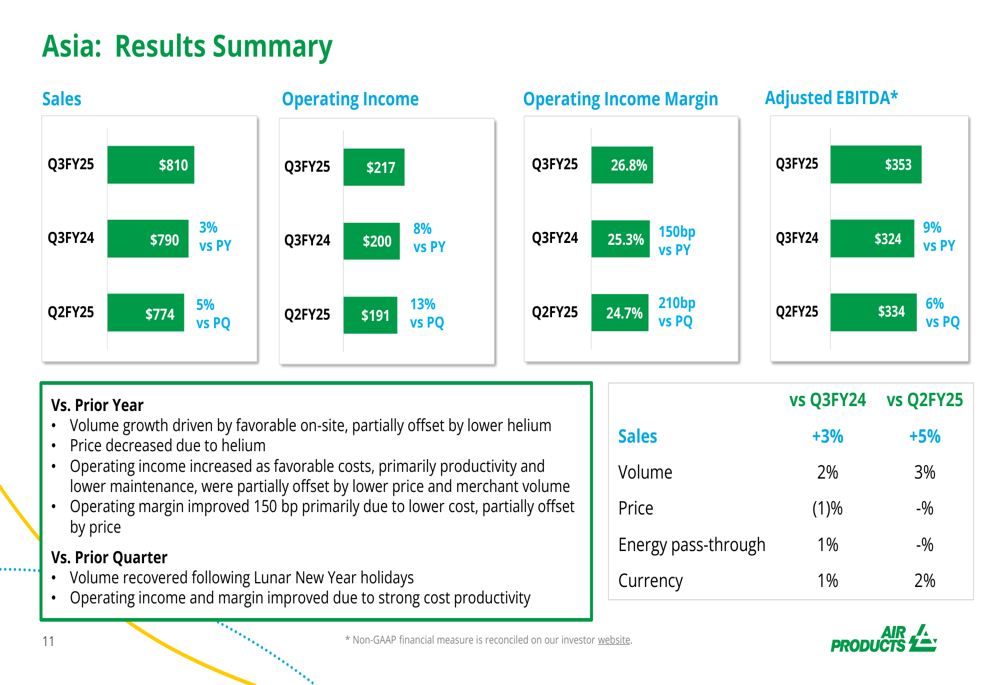

The Asian region also demonstrated solid performance:

Asia reported 3% sales growth year-over-year, with 2% volume growth and 1% favorable currency impact, partially offset by a 1% price decline. Operating income increased 8% to $217 million, while operating margin improved 150 basis points to 26.8%. Adjusted EBITDA grew 9% to $353 million compared to the prior year.

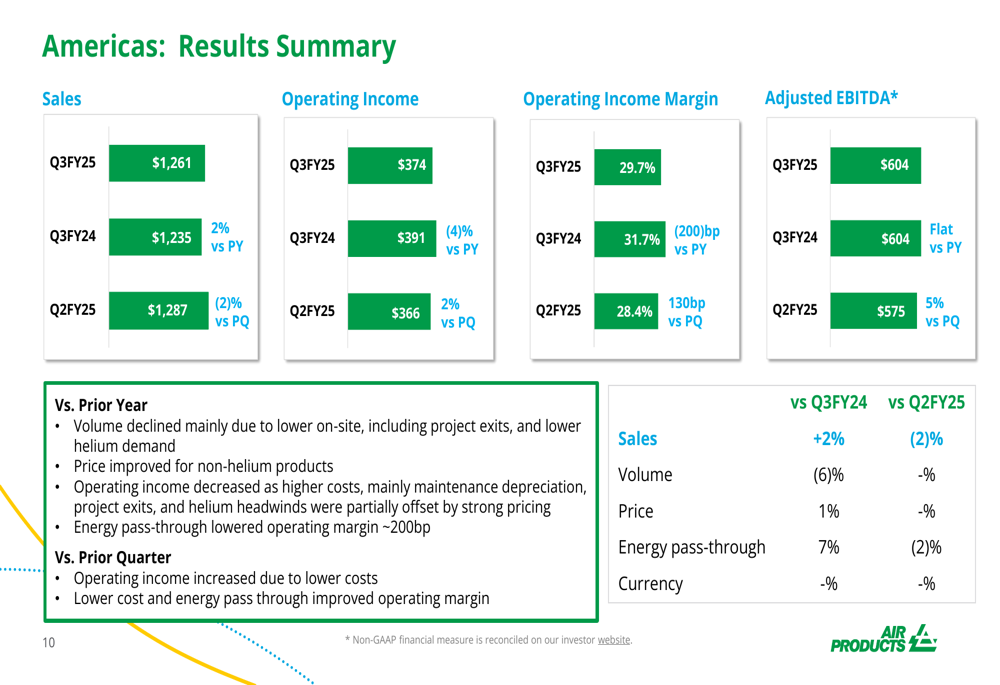

Meanwhile, the Americas region showed mixed results:

Americas sales increased 2% year-over-year, but this was entirely due to 7% higher energy pass-through, as volume declined 6%. Operating income decreased 4% to $374 million, while operating margin declined 200 basis points to 29.7%. Adjusted EBITDA remained flat at $604 million compared to the prior year.

Forward-Looking Statements & Guidance

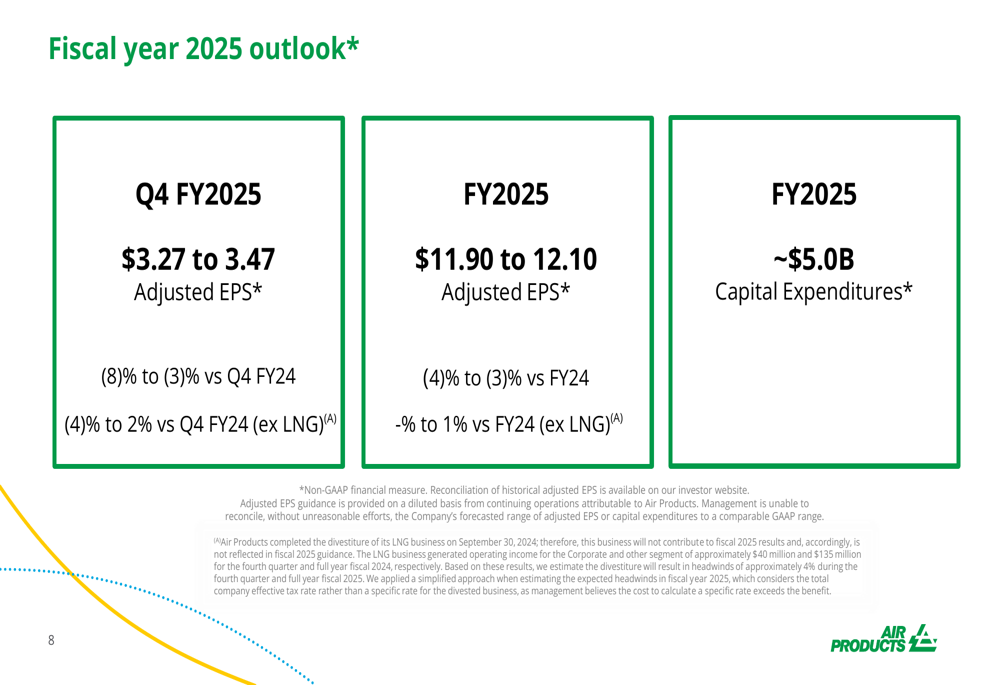

Air Products provided specific guidance for the fourth quarter and full fiscal year 2025:

For Q4 FY2025, the company expects adjusted EPS between $3.27 and $3.47, representing a decline of 3% to 8% compared to Q4 FY2024, or a range of -4% to +2% excluding the impact of the LNG business divestiture.

For the full fiscal year 2025, Air Products projects adjusted EPS between $11.90 and $12.10, representing a decline of 3% to 4% compared to FY2024, or a range of 0% to +1% excluding the LNG business impact. Capital expenditures are expected to be approximately $5.0 billion for the fiscal year.

This guidance reflects the company’s transition period as it implements its strategic shift toward core industrial gases operations and more disciplined capital allocation, setting the stage for the projected acceleration in growth rates from 2026 onward.

The market’s positive premarket reaction suggests investors are responding favorably to the company’s strategic direction and sequential improvement, despite the year-over-year pressure on key metrics. Air Products appears positioned to leverage its core strengths while addressing previous challenges that impacted its second-quarter performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.