ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Aktia Bank (HEL:AKTIA) reported its second quarter 2025 results on August 5, showing a comparable operating profit of €26.2 million, down from €30.8 million in the same period last year. The Finnish bank's performance reflects the challenging interest rate environment, with declining net interest income partially offset by stable commission income and growth in wealth management assets.

The bank's stock closed at €10.04 on August 4, trading above its 52-week low of €8.69 but still well below its 52-week high of €11.20. Aktia's results come as many European banks face pressure from declining interest rates after a period of strong net interest income growth.

Quarterly Performance Highlights

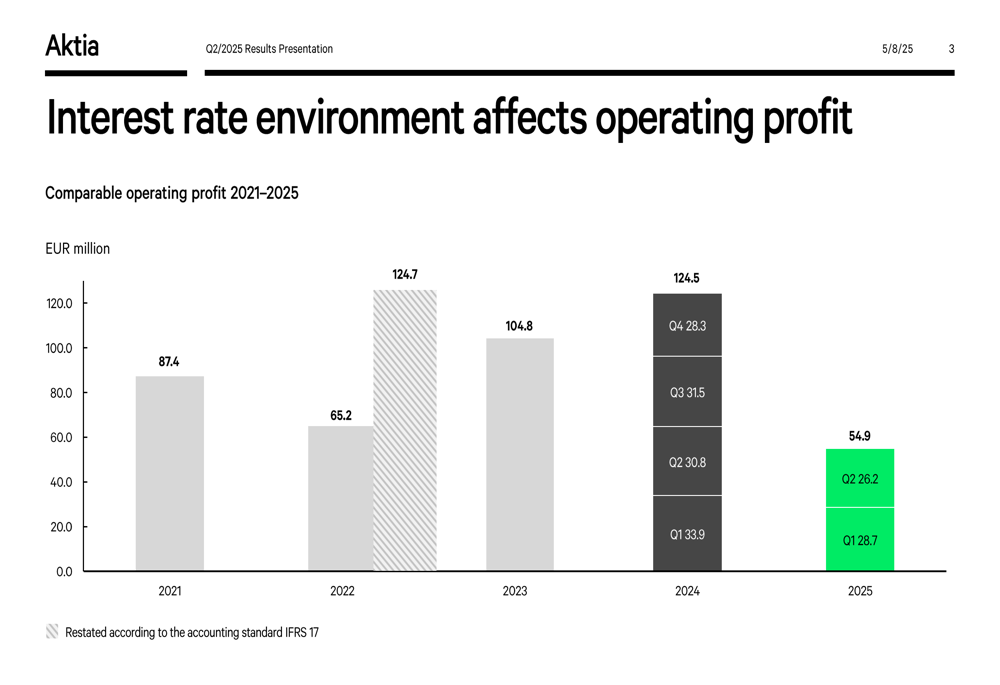

Aktia's financial performance for Q2 2025 was characterized by declining operating profit but relative stability in other key metrics. The comparable operating profit of €26.2 million represented a 15% decrease from Q2 2024, while the half-year figure of €54.9 million was down 15.1% from the first half of 2024.

As shown in the following chart of operating profit trends, Aktia's quarterly profits have been declining since their peak in 2024, primarily due to interest rate impacts:

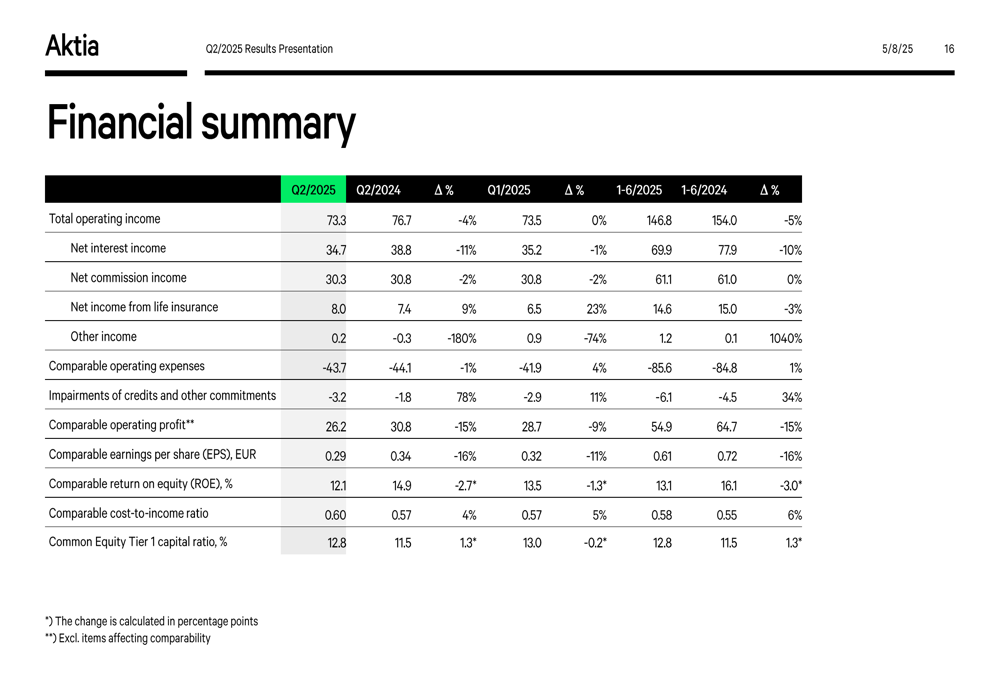

Total (EPA:TTEF) operating income decreased to €73.3 million from €76.7 million in Q2 2024. Net interest income fell to €34.7 million from €38.8 million, reflecting the impact of lower market rates. However, net commission income remained relatively stable at €30.3 million compared to €30.8 million in the same quarter last year.

The bank's comprehensive financial summary reveals mixed performance across key metrics:

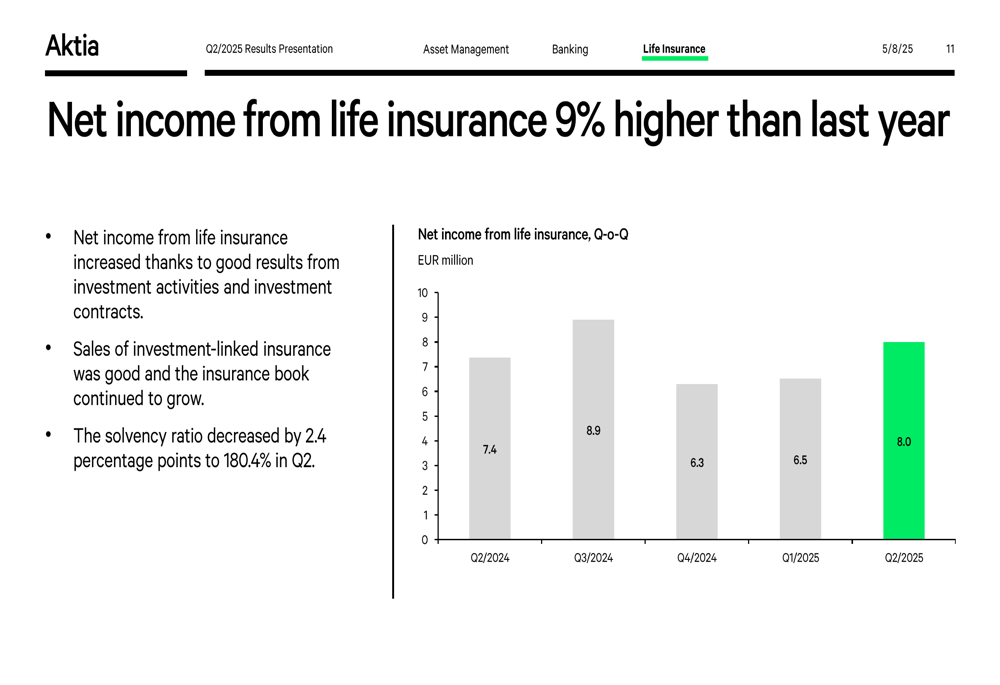

Net income from life insurance showed strong performance, increasing 9% year-over-year to €8.0 million. This growth was driven by good results, strong sales of investment-linked insurance, and a growing insurance book, although the solvency ratio decreased by 2.4 percentage points to 180.4%.

Strategic Initiatives

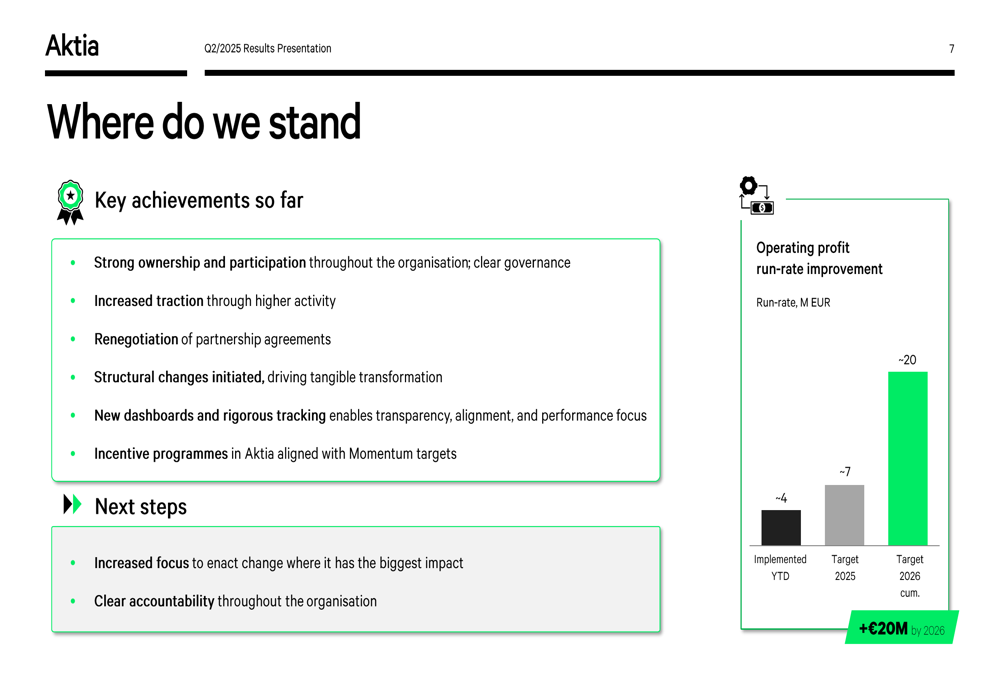

Aktia continues to make progress on its strategic acceleration program, which aims to increase operating profit run-rate by €20 million by 2026. The bank has implemented approximately €4 million in run-rate improvements year-to-date, with a target of €7 million for 2025.

The following chart illustrates the progress and targets of Aktia's strategic acceleration program:

The program consists of 10 focused streams, including boosting Premium Banking, growing Private Banking, strengthening Asset Management, enhancing insurance sales, and improving cost efficiency. Key achievements so far include strong ownership and participation, increased traction, renegotiation of partnerships, structural changes, new dashboards, and incentive programs.

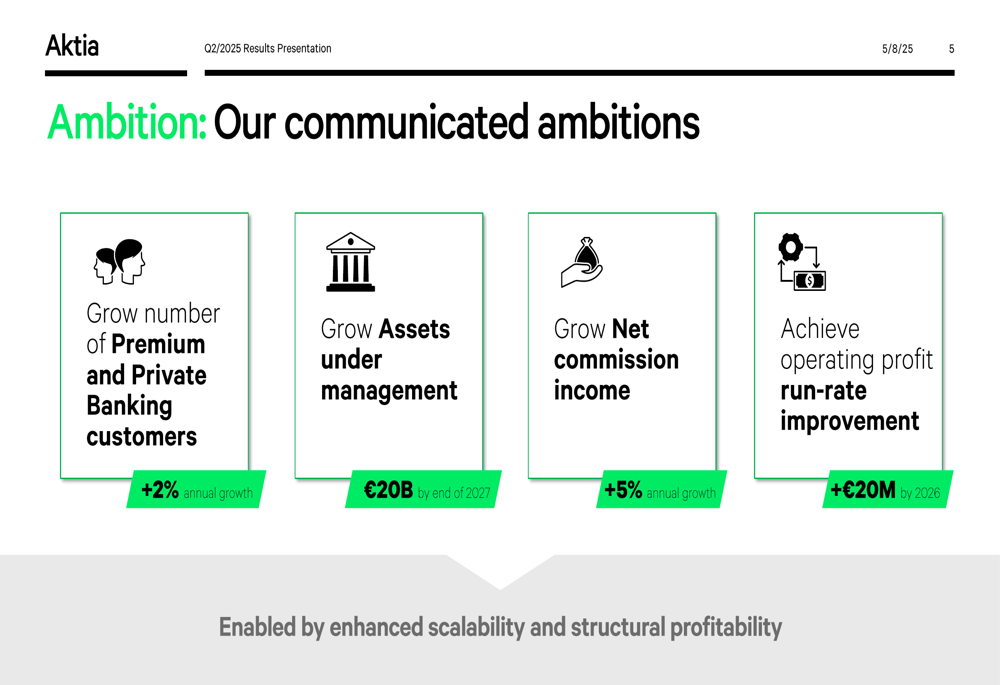

Aktia has also outlined clear long-term ambitions, including:

- Growing Premium and Private Banking customers by 2% annually

- Increasing assets under management to €20 billion by end of 2027

- Growing net commission income by 5% annually

- Achieving the €20 million operating profit run-rate improvement by 2026

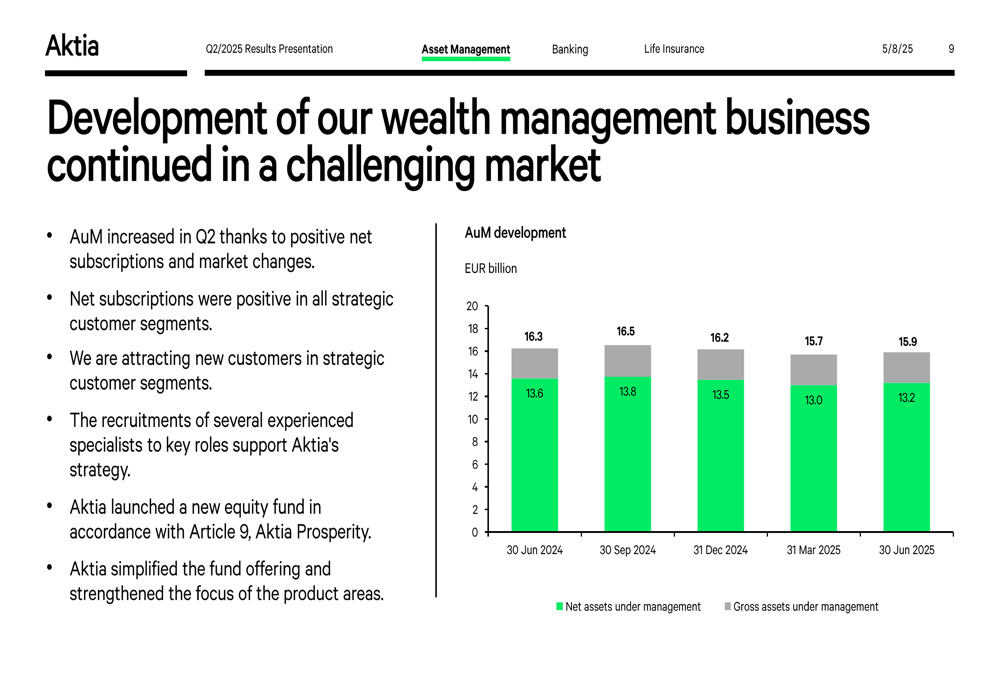

Wealth Management & Lending Growth

Despite challenging market conditions, Aktia's assets under management increased to €15.9 billion in Q2 2025, up from €15.7 billion in Q1 2025. This growth was driven by positive net subscriptions and new customer acquisition.

The following chart shows the development of Aktia's assets under management:

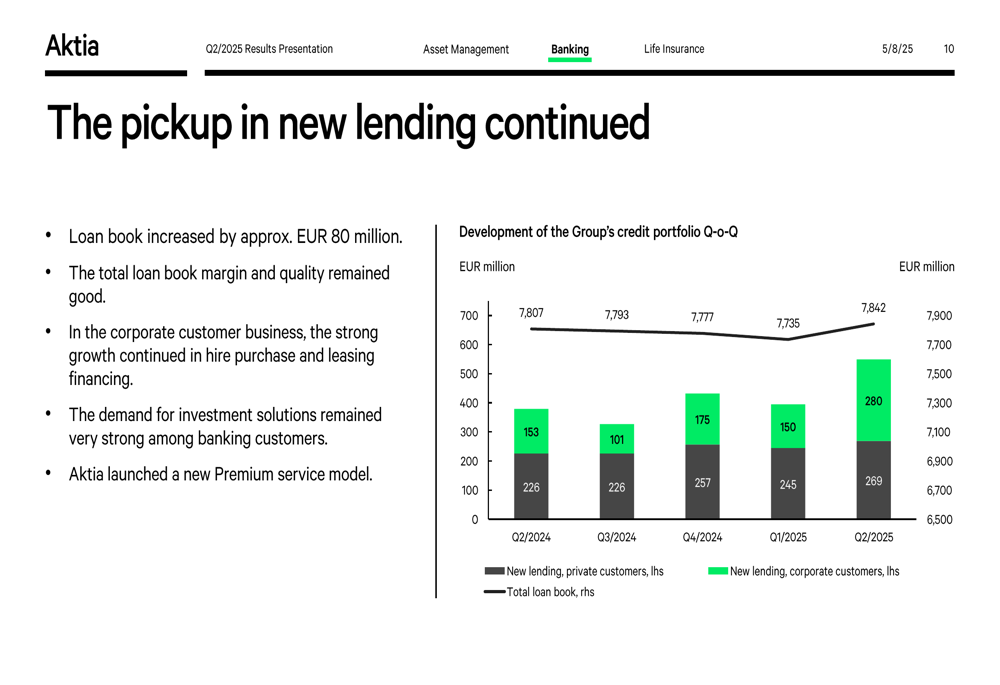

The bank also reported continued growth in lending, with the loan book increasing by approximately €80 million. New lending to private customers reached €269 million in Q2 2025, while new lending to corporate customers surged to €280 million, significantly higher than previous quarters.

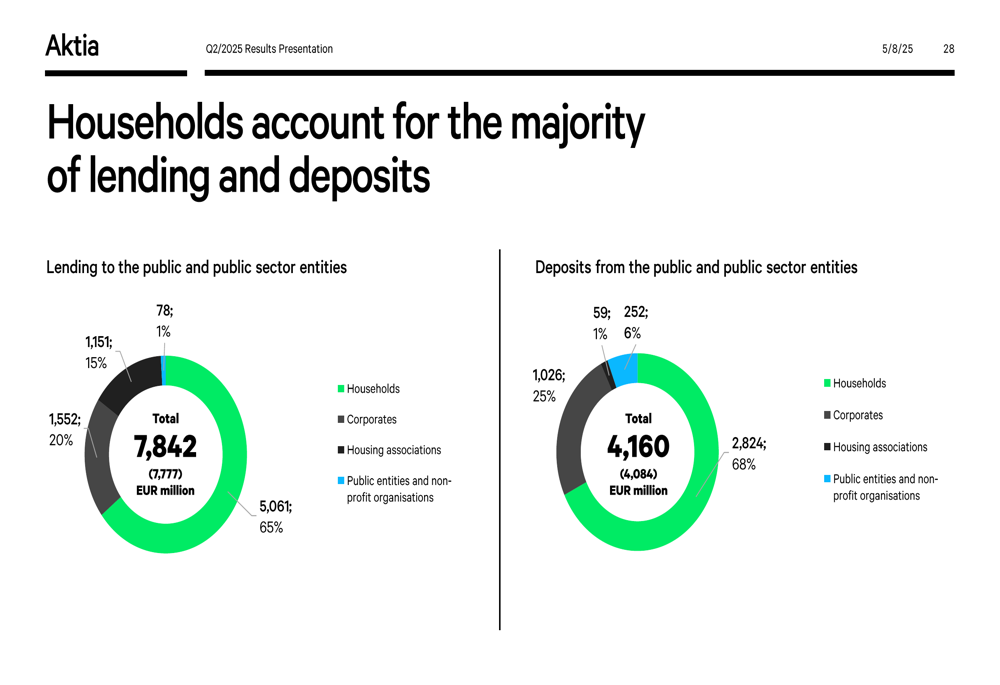

Aktia's lending and deposit portfolios remain primarily focused on the household segment, with 65% of lending and 68% of deposits coming from households. Corporate customers account for 20% of lending and 25% of deposits.

Capital Position & Cost Control

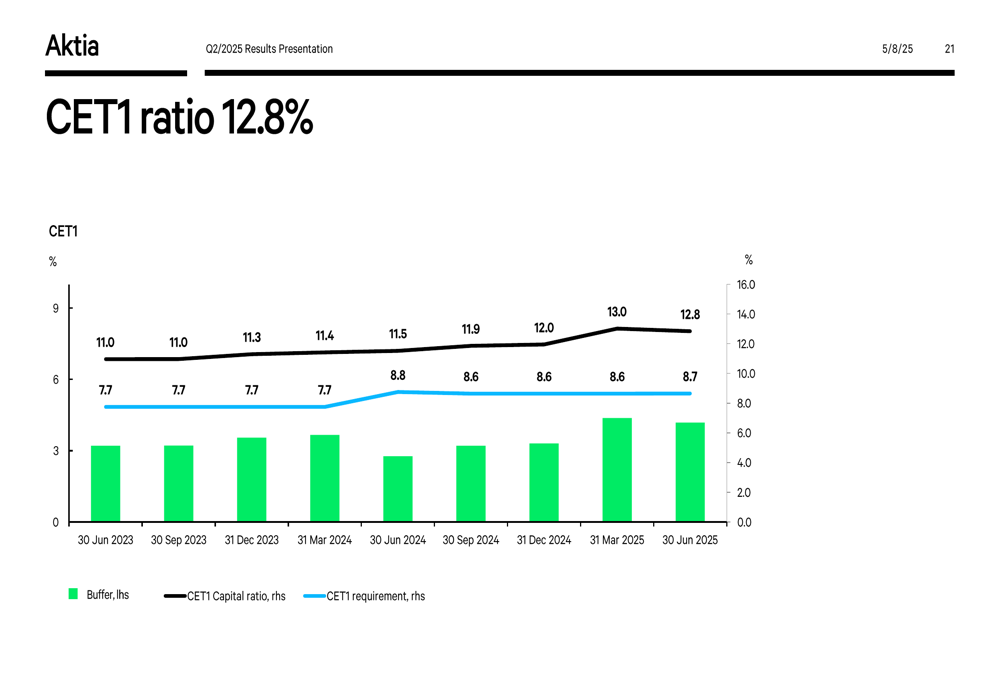

Aktia's Common Equity Tier 1 (CET1) capital ratio strengthened to 12.8% in Q2 2025, up from 11.5% in Q2 2024 and comfortably above regulatory requirements. This improvement provides the bank with additional financial flexibility.

Cost control remains a focus area for Aktia, with comparable operating expenses decreasing by 1% year-over-year to €43.7 million. However, the composition of expenses shifted, with IT expenses increasing by 6% and other operating expenses rising by 13%, while depreciation decreased by €2.0 million.

Credit loss provisions increased to €3.2 million in Q2 2025 from €1.8 million in Q2 2024, with annualized net credit losses at 15 basis points. The bank noted that its loan book primarily consists of loans to households with real estate collateral, and the increase in credit losses was due to individual impairments.

Forward-Looking Statements

Aktia's outlook for 2025 remains unchanged, with the bank expecting its comparable operating profit for the full year to be lower than the €124.5 million reported in 2024. This outlook is based on assumptions of lower net interest income, stable net commission income, steady life insurance business, increased operating expenses, and moderate credit losses.

The bank continues to focus on its strategic acceleration program to offset some of the pressure from the interest rate environment. With €4 million in run-rate improvements already implemented and a target of €7 million for 2025, Aktia appears to be making progress toward its longer-term goal of €20 million in improvements by 2026.

Sustainability remains a priority for Aktia, with 98.2% of its funds classified under SFDR Article 8 and 9. The bank also reported an employee Net Promoter Score (eNPS) of 29, above its target of 20, and a culture index of 4.3/5, indicating strong employee engagement despite the challenging business environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.