Gold prices edge up amid Fed rate cut hopes; US-Russia talks awaited

Introduction & Market Context

Alaska Air Group (NYSE:ALK) presented its Q1 2025 earnings results on April 23, 2025, reporting a quarterly loss that was narrower than the previous year but slightly below guidance. Despite the loss, the company highlighted industry-leading unit revenue performance and positive early results from its Hawaiian Airlines integration.

The airline’s stock fell 6.31% in premarket trading to $43.20, suggesting investors may have expected better results or were concerned about elements of the outlook. This reaction comes despite several positive metrics in the presentation, including year-over-year margin improvement and strong premium revenue growth.

Quarterly Performance Highlights

Alaska Air reported an adjusted net loss per share of ($0.77) for Q1 2025, which was $10 million below the company’s original guidance. However, the adjusted pretax margin of (4.5%) represented a significant 7-point improvement compared to the same quarter last year.

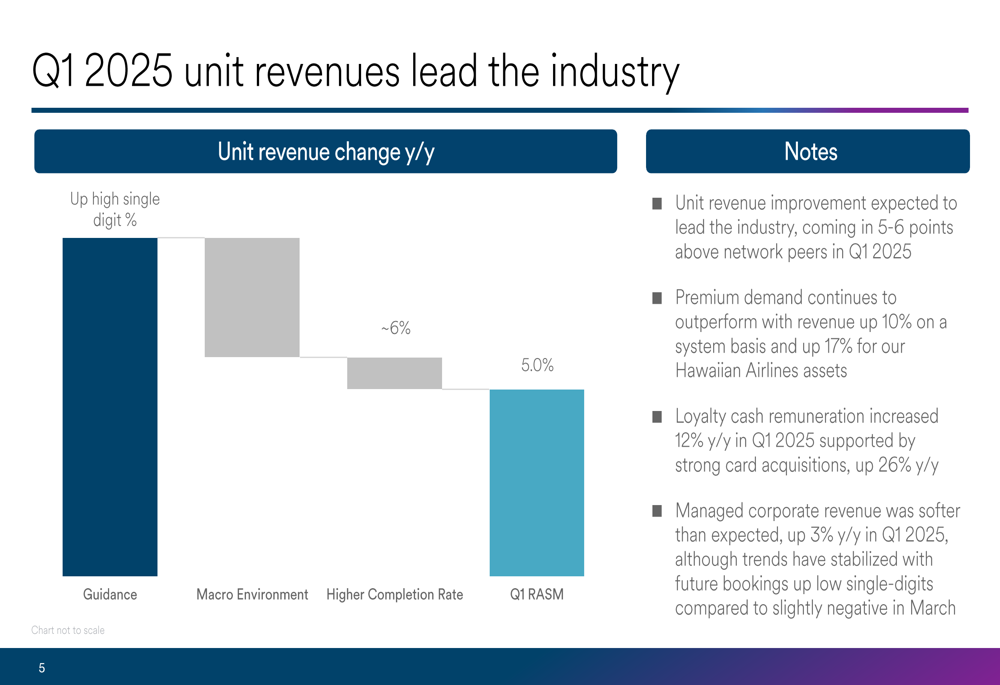

The company’s unit revenues increased by 5% year-over-year, which management noted was expected to lead the industry. This performance is particularly notable considering there was an approximately 3-point negative revenue impact from higher completion rates compared to the disrupted first quarter of 2024.

As shown in the following chart of unit revenue change year-over-year:

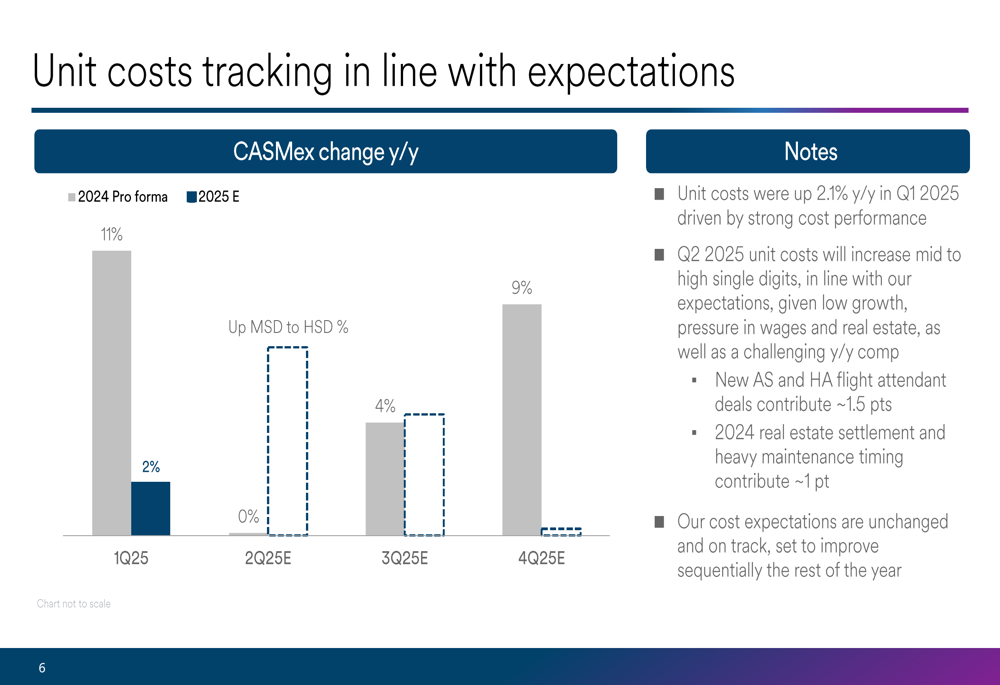

On the cost side, unit costs (CASMex) increased by 2.1% year-over-year in Q1 2025, which the company indicated was in line with expectations. The economic fuel cost per gallon averaged $2.61 for the quarter.

The following chart shows unit cost trends and projections:

Hawaiian Airlines Integration Progress

A significant focus of the presentation was the progress of the Hawaiian Airlines integration, which became part of Alaska Air Group’s consolidated financials from September 18, 2024. The company reported that Hawaiian operations are outperforming expectations, with a 14-point margin improvement year-over-year.

Hawaiian Airlines assets showed particularly strong performance in premium revenue, which increased 17% year-over-year. Additionally, the Huaka’i by Hawaiian loyalty program has grown to over 200,000 members, representing a 90% increase since December.

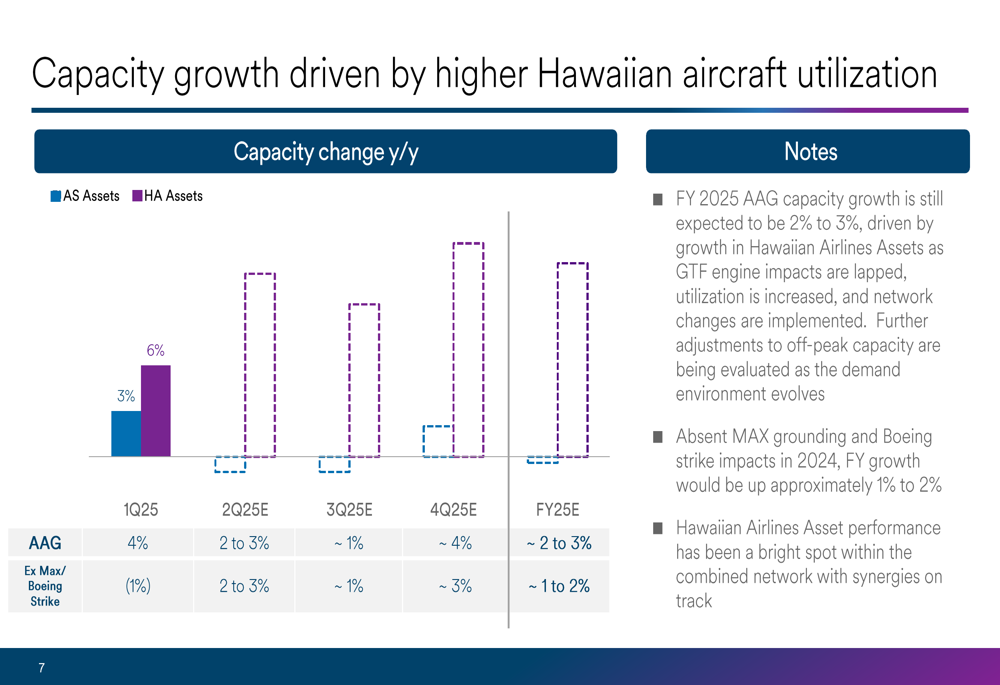

The company outlined capacity growth driven largely by higher Hawaiian aircraft utilization, as illustrated in this chart:

Alaska Air also provided an update on key integration milestones, with plans for a single loyalty program in the second half of 2025, a single operating certificate by Q4 2025, and a single passenger service system by Q2 2026. Joint collective bargaining agreements are expected to be implemented between 2025 and 2027.

Strategic Initiatives

The presentation highlighted progress on the company’s "Alaska Accelerate" strategic initiatives, which are targeting a total of $800 million in value across four key areas: Network ($400M), Product ($100M), Loyalty ($150M), and Cargo ($150M).

The company reported strong performance across all four pillars, with network initiatives delivering industry-leading RASM 5-6 points ahead of network carriers, product initiatives driving 10% premium revenue growth, loyalty initiatives increasing card acquisitions by 26% year-over-year, and cargo revenue growing 36% year-over-year.

As shown in the detailed breakdown of these initiatives:

Balance Sheet and Capital Allocation

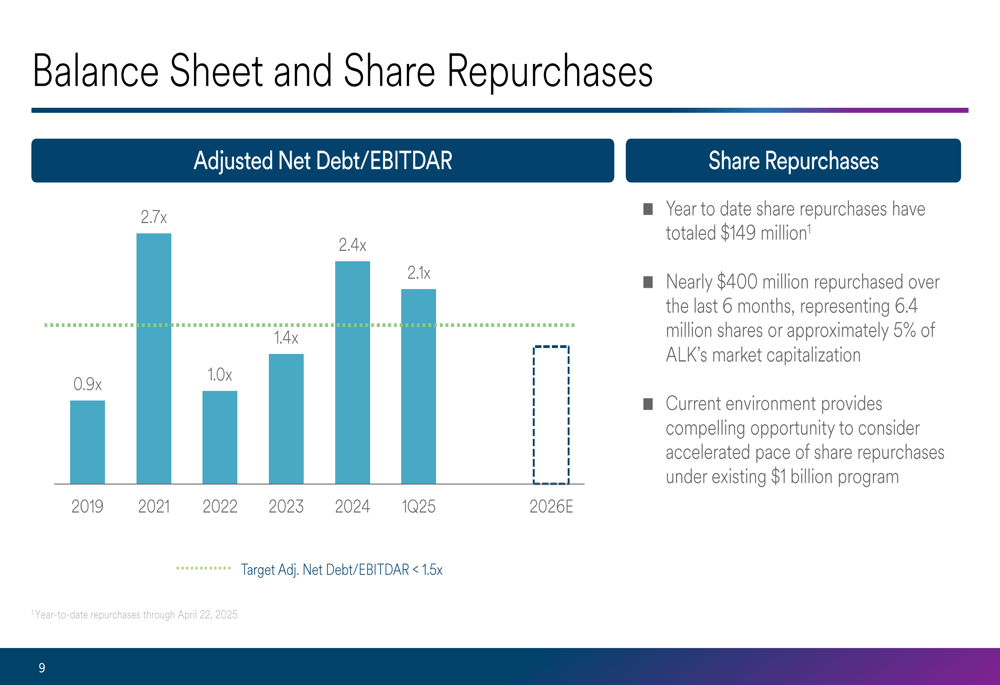

Alaska Air emphasized its strong balance sheet, with debt-to-cap at 58% and adjusted net debt to EBITDAR at 2.1x, an improvement from 2.4x at the end of 2024. The company has a target of maintaining this ratio below 1.5x.

The following chart illustrates the company’s debt metrics over time:

Despite the quarterly loss, Alaska Air has continued its share repurchase program, buying back $149 million in shares year-to-date, which represents nearly $400 million repurchased over the last six months. Management indicated that the "current environment provides compelling opportunity" for share repurchases.

Forward-Looking Statements

Looking ahead, Alaska Air maintained its full-year 2025 capacity growth forecast of 2% to 3%. The company noted that absent the MAX grounding and Boeing (NYSE:BA) strike impacts in 2024, full-year growth would be approximately 1% to 2%.

For Q2 2025, the company expects unit costs to increase by mid to high single digits. The company also indicated that while premium demand continues to outperform, managed corporate revenue was softer than expected, up only 3% year-over-year.

Alaska Air also highlighted ongoing challenges with West Coast refining supply, which has resulted in elevated LA refining margins affecting fuel costs. This situation bears monitoring as it could impact profitability in coming quarters if it persists.

Overall, while Alaska Air’s Q1 results showed year-over-year improvement and several positive trends, the quarterly loss and some cautionary notes about costs and corporate demand likely contributed to the negative premarket stock reaction. Investors will be watching closely to see if the Hawaiian integration and strategic initiatives can accelerate the company’s return to consistent profitability in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.