S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

Alaska Air Group (NYSE:ALK) presented its second quarter 2025 earnings on July 23, showcasing results that exceeded guidance despite challenging industry conditions. The carrier reported an adjusted earnings per share of $1.78, surpassing the high end of its original guidance, with an overall adjusted pretax margin of 8.0%.

Despite this positive performance, Alaska Air’s stock declined 1.47% in premarket trading to $47.56, suggesting investors may have been looking for even stronger results or guidance. The company’s presentation highlighted its ongoing strategic initiatives and integration progress with Hawaiian Airlines.

Quarterly Performance Highlights

Alaska Air Group delivered solid financial results in Q2 2025, with adjusted earnings per share of $1.78 exceeding the high end of original guidance. According to the earnings transcript, the company achieved record revenue of $3.7 billion, representing a 2% year-over-year increase.

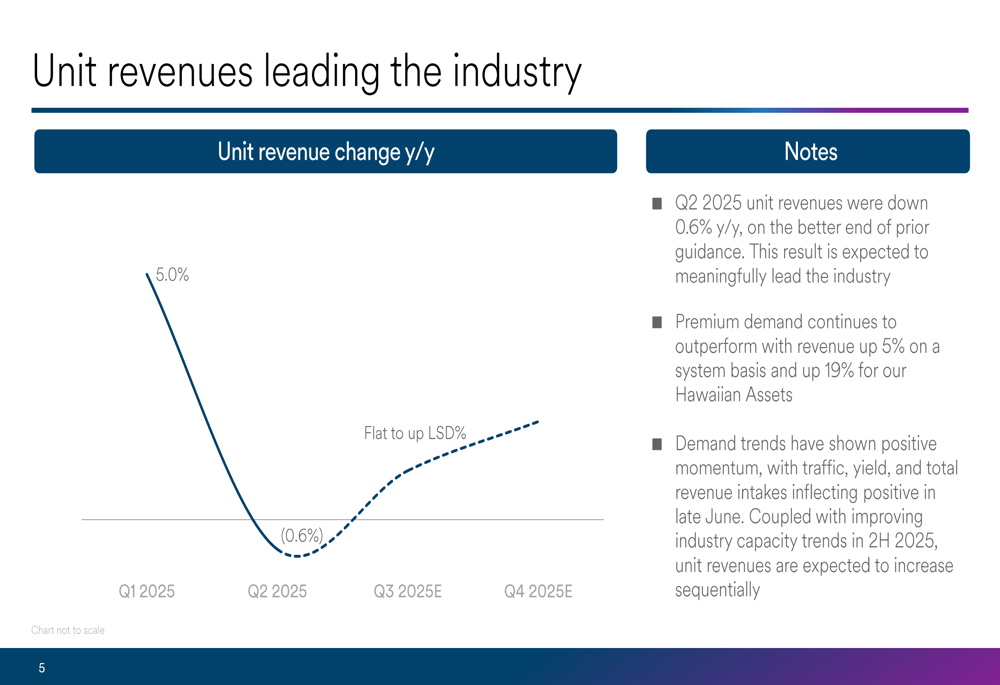

The company’s unit revenues decreased 0.6% year-over-year in Q2, though management emphasized this outperformed the broader industry. Premium demand continued to show strength with revenue up 5% on a system basis and an impressive 19% for Hawaiian Assets.

As shown in the following chart of unit revenue trends, the company expects sequential improvement in the second half of the year:

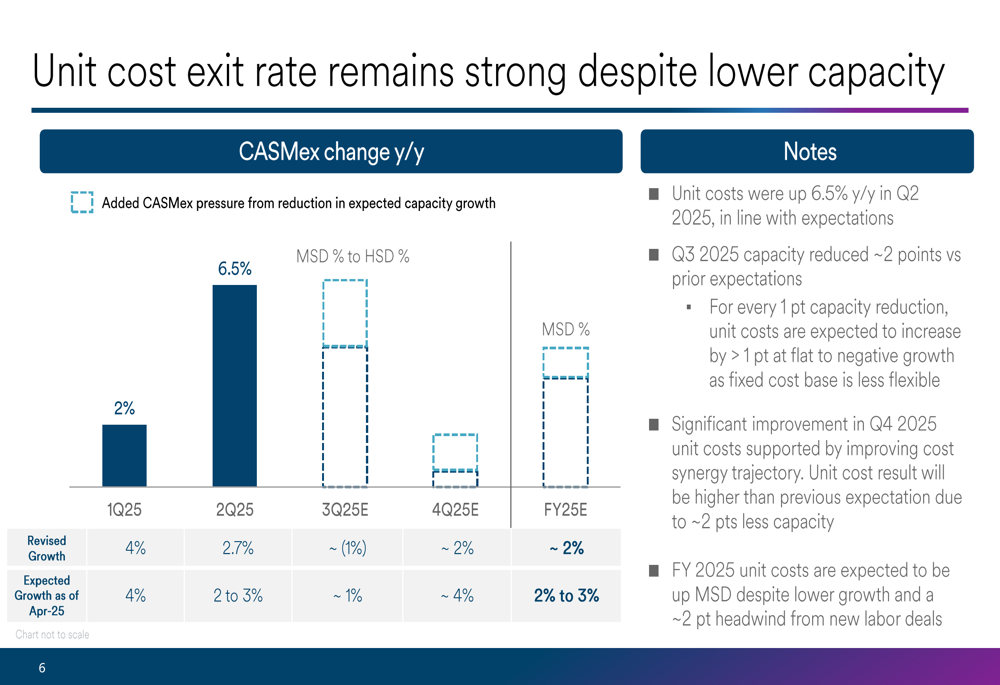

On the cost side, unit costs increased 6.5% year-over-year in Q2 2025, in line with management’s expectations. The company has revised its capacity growth downward for Q3 2025 by approximately 2 percentage points compared to prior expectations, while projecting significant unit cost improvement in Q4 2025.

The following chart illustrates the company’s unit cost trajectory and capacity adjustments:

Fuel costs averaged $2.39 per gallon in Q2 2025. The company noted that crude oil prices declined over 10% from April through early June before increasing again in late June, while West Coast refining margins decreased and remained relatively stable throughout much of the quarter before spiking in late June due to a large refinery outage and peak summer demand.

Strategic Initiatives Progress

Alaska Air’s presentation highlighted significant progress across its "Alaska Accelerate" strategic initiatives, which span Network, Product, Loyalty, and Cargo segments. The company reported that these initiatives are progressing well and remain on track to deliver the targeted financial benefits.

The comprehensive overview of these initiatives and their progress is illustrated in this slide:

A key milestone was the Hawaiian Assets reaching their first profitable quarter since the acquisition. The company has also expanded its international presence, launching Seattle-Tokyo Narita service in May 2025, with Seoul Incheon service planned for September 2025 and Rome service for Spring 2026. Additionally, Alaska announced the acquisition of five additional Boeing 787 aircraft to support its growth strategy.

In the Product segment, premium revenue remained resilient with 5% growth, while approximately 40% of 737 premium retrofits have been completed. The company also announced a multi-year refresh of Airbus A330 interiors and a new state-of-the-art lobby in Seattle set to open in January.

The Loyalty program continued to perform well, being named "Best Airline Rewards Program" by U.S. News for the 11th consecutive year. Active card accounts increased 10% year-over-year, while the Hawaiian resident program "Huakaʻi by Hawaiian" has grown to approximately 250,000 members. A single loyalty brand and new premium card are scheduled to launch in August.

Cargo operations showed particularly strong growth, with revenue up 34% year-over-year. The company completed delivery of the last two Amazon A330 freighters and commenced international widebody cargo operations on the Seattle-Tokyo route.

Financial Outlook

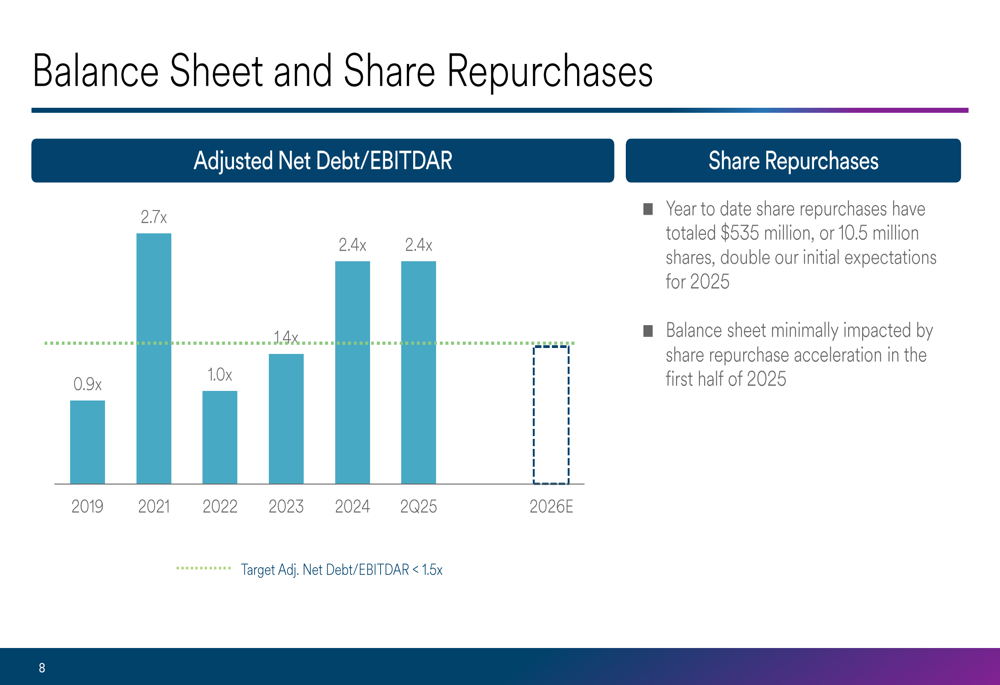

Alaska Air maintained a strong balance sheet despite accelerating its share repurchase program. Year-to-date share repurchases totaled $535 million, or 10.5 million shares, double the company’s initial expectations for 2025. The adjusted net debt to EBITDAR ratio remained at 2.4x, unchanged from the previous quarter.

The following chart illustrates the company’s debt position over time:

For the full year 2025, Alaska Air expects capacity growth of approximately 2%, down slightly from the previous guidance of 2-3%. Unit costs are projected to increase by mid-single digits despite lower growth and approximately 2 percentage points of headwind from new labor deals.

According to the earnings transcript, the company is maintaining its full-year adjusted EPS guidance of at least $3.25 and remains committed to its longer-term target of $10 EPS by 2027.

Integration Milestones

Alaska Air provided an update on key integration milestones following its acquisition of Hawaiian Airlines. The company is preparing to launch a single loyalty program platform and premium credit card in August 2025, while working toward obtaining a single operating certificate by Q4 2025.

Integration of the passenger service system is planned for Q2 2026, with vendor selection and preparatory work already underway. Joint collective bargaining negotiations with union groups have commenced and are expected to continue through 2027.

These integration efforts are critical to achieving the synergy targets outlined in the Alaska Accelerate program. According to CEO Ben’s comments in the earnings call, "Alaska Accelerate is working," suggesting management’s confidence in the integration progress and overall strategy.

The company’s strong Q2 performance, despite revenue headwinds, indicates that Alaska Air is effectively executing its strategic initiatives while navigating industry challenges. With Hawaiian Assets achieving profitability and international expansion underway, Alaska Air appears well-positioned to capitalize on its strengthened network and enhanced product offerings in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.