S&P500 rises as Nvidia lifts tech, Fed minutes points to more rate cuts ahead

Introduction & Market Context

Alcoa Corporation (NYSE:AA) delivered strong first quarter 2025 results, with significant sequential improvement in profitability despite facing new tariff challenges. The aluminum producer reported adjusted earnings per share of $2.15, exceeding analyst forecasts of $1.58 by 36%, while revenue of $3.37 billion fell short of the expected $3.5 billion. Following the earnings announcement, Alcoa’s stock rose 1.58% during regular trading but declined 1.88% in after-hours trading, reflecting mixed investor sentiment.

The company’s performance comes amid a complex market environment characterized by volatile aluminum and alumina prices, new U.S. tariffs on Canadian aluminum, and ongoing challenges in the Chinese refining system. CEO William Oplinger emphasized the company’s focus on "safe operations" that "correlate to stability, productivity and profitability" as key to navigating these dynamic markets.

Quarterly Performance Highlights

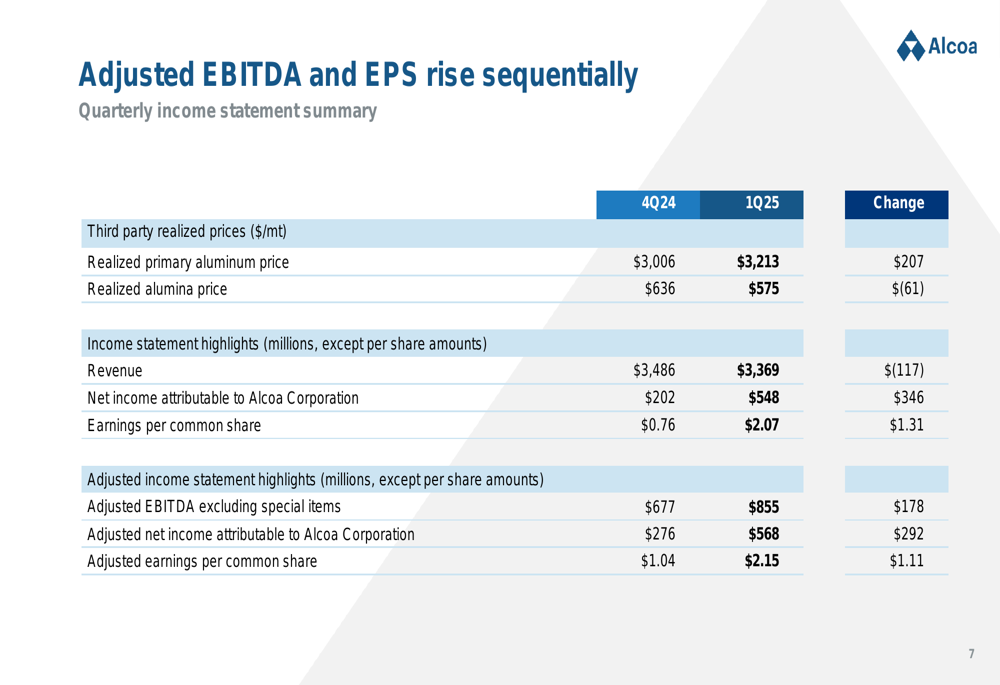

Alcoa reported substantial sequential improvement in its key financial metrics for Q1 2025. Adjusted EBITDA excluding special items increased by $178 million to $855 million, representing a 26% improvement from Q4 2024. Net income attributable to Alcoa Corporation more than doubled to $548 million from $202 million in the previous quarter.

As shown in the following quarterly income statement summary:

The company’s realized primary aluminum price increased by $207 to $3,213 per metric ton, while the realized alumina price decreased by $61 to $575 per metric ton. This pricing dynamic, along with lower intersegment profit elimination, drove the significant improvement in adjusted earnings per share, which rose from $1.04 in Q4 2024 to $2.15 in Q1 2025.

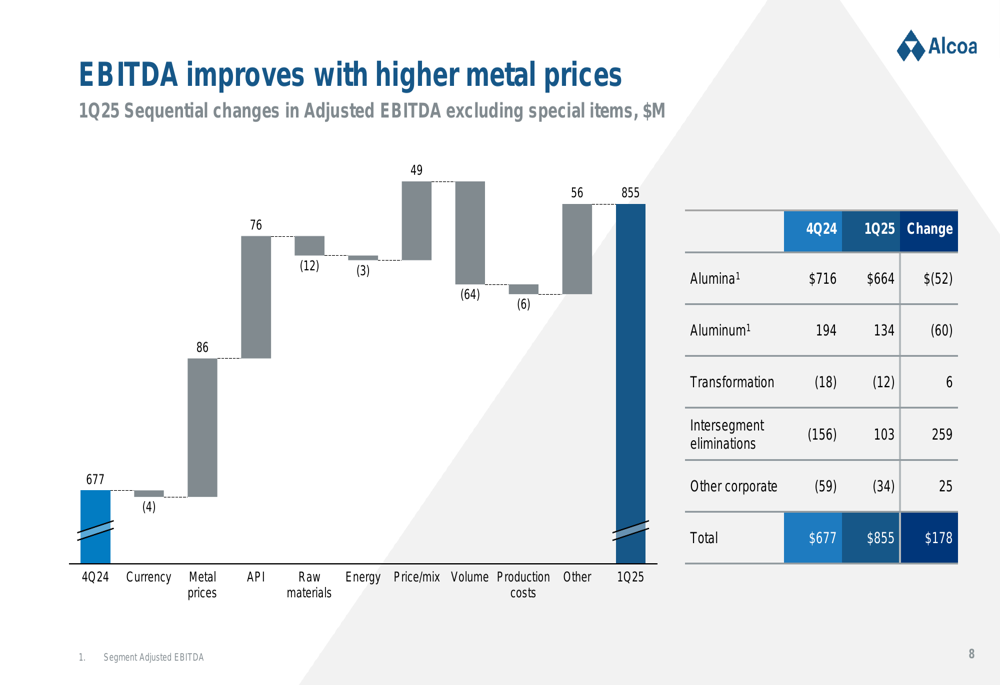

The sequential EBITDA improvement was primarily driven by favorable intersegment eliminations, which contributed $259 million in positive change, offsetting decreases in both the Alumina (OTC:AWCMY) and Aluminum segments:

Detailed Financial Analysis

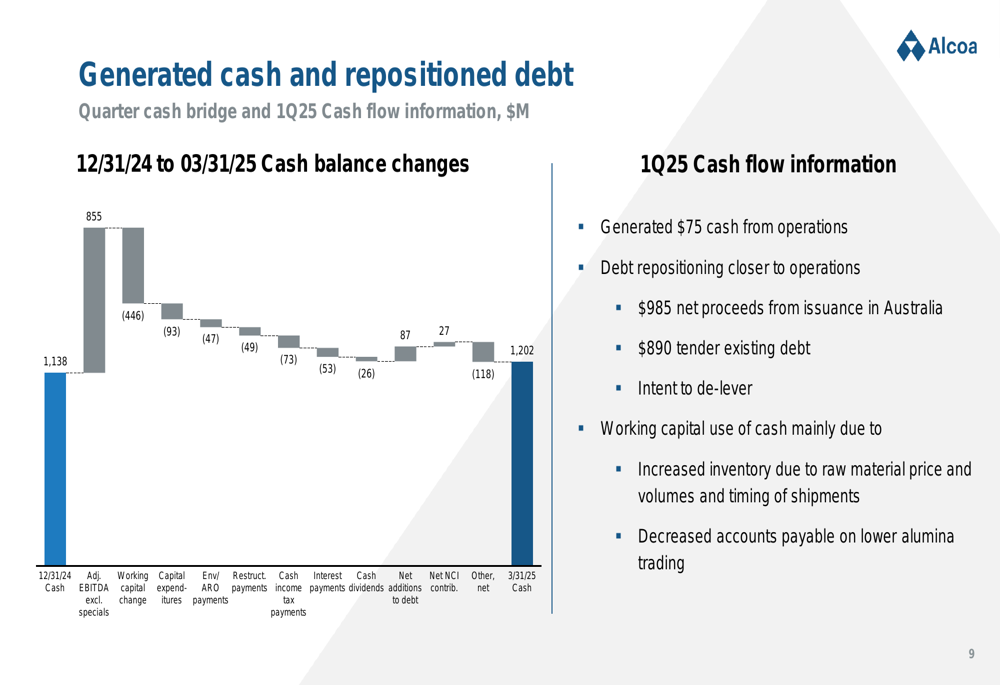

Alcoa maintained a strong cash position, ending the quarter with $1.2 billion in cash, up from $1.14 billion at the end of 2024. The company generated positive cash from operations of $75 million despite a significant working capital build, which is typical in first quarters. The cash flow was impacted by changes in working capital (-$446 million), primarily due to raw material price increases and decreased payables on lower alumina trading.

The following cash bridge illustrates the movement in cash balance during Q1 2025:

A significant financial development during the quarter was Alcoa’s debt repositioning, which included a $1 billion debt offering in Australia, with proceeds used to tender $890 million of existing debt. This strategic move extended debt maturities and lowered after-tax interest expense.

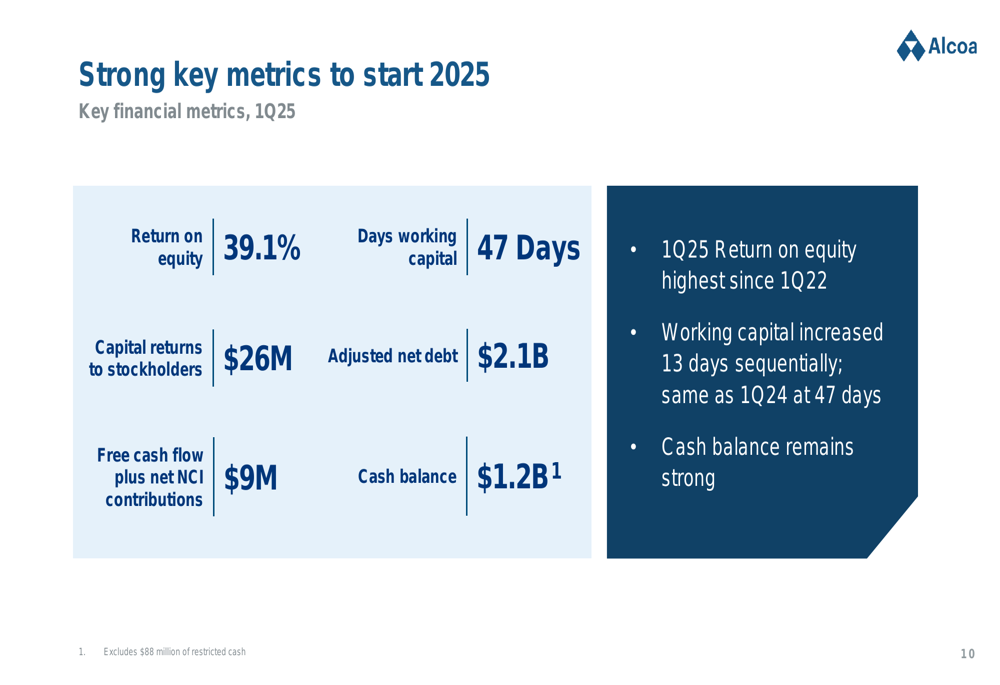

The company reported strong key financial metrics for Q1 2025, including a return on equity of 39.1% (the highest since Q1 2022), working capital of 47 days, and adjusted net debt of $2.1 billion:

Alcoa outlined its optimal capital structure targets, aiming for adjusted net debt between $1.0 billion and $1.5 billion, with a cash balance target of $1.0-$1.5 billion. The company’s current adjusted net debt of $2.1 billion indicates it is still working toward these targets.

Strategic Initiatives

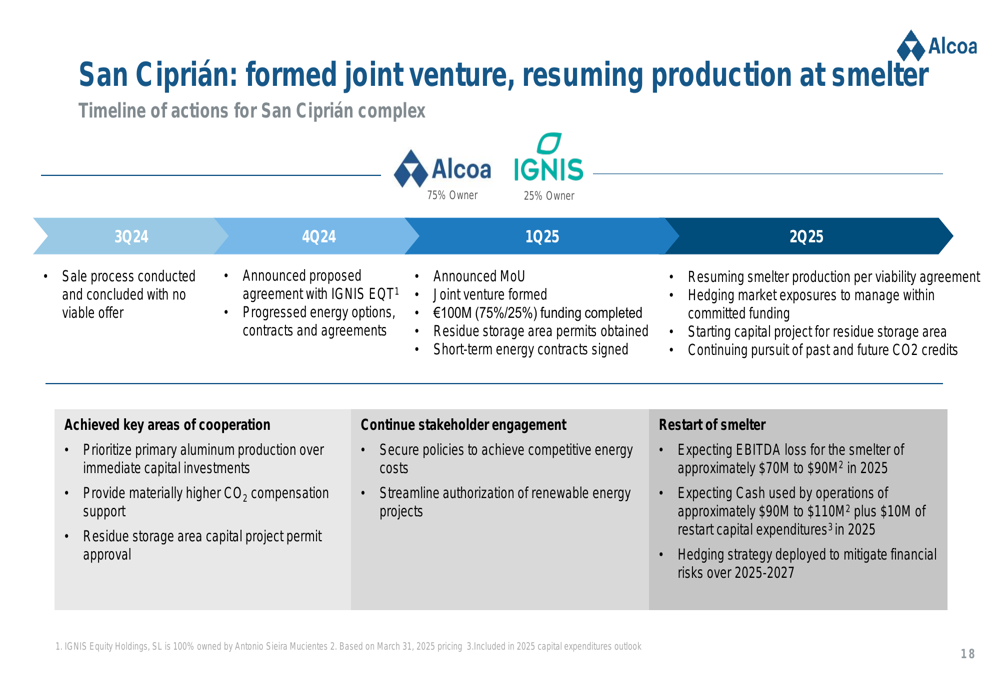

A key strategic development in Q1 2025 was the formation of a joint venture with Ignis EQT (ST:EQTAB) for Alcoa’s San Ciprián operations in Spain. This move follows an unsuccessful sale process that concluded with no viable offer in Q3 2024. The joint venture has completed €100 million in funding, and Alcoa expects to resume smelter production in Q2 2025.

The timeline for the San Ciprián joint venture is illustrated below:

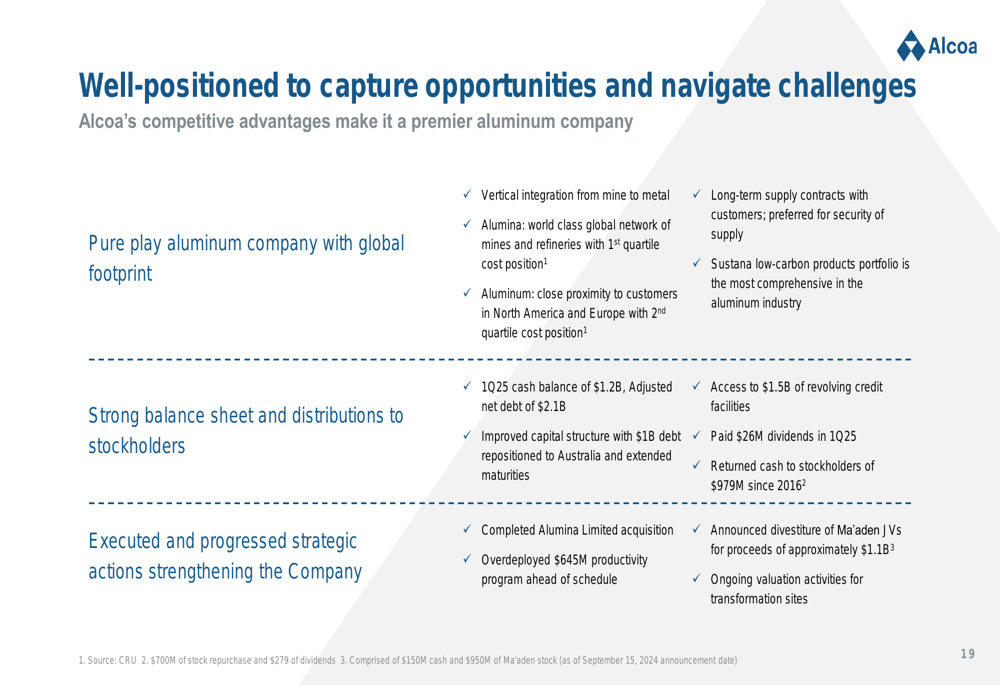

Alcoa is also progressing on other strategic initiatives, including the expected completion of the sale of its Ma’aden joint venture in Q2 2025. The company emphasized its vertical integration from mine to metal, maintenance of low carbon products, and long-term supply contracts as key competitive advantages.

Market Challenges & Opportunities

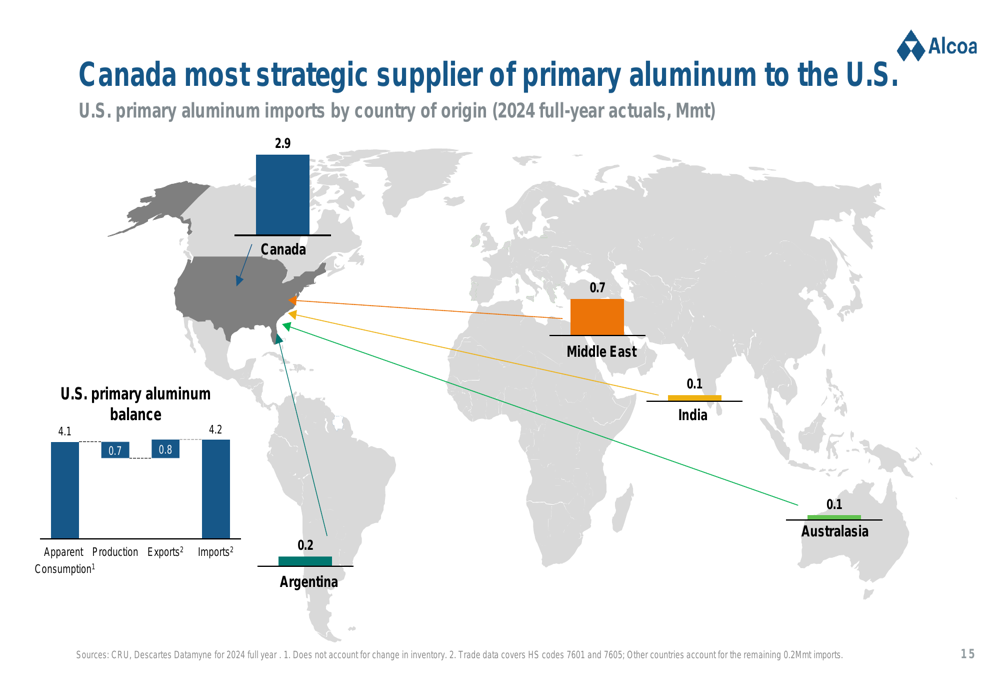

The implementation of a 25% tariff on Canadian aluminum imports to the U.S. in March 2025 represents a significant challenge for Alcoa. The company estimates this will have an approximately $100 million annual negative impact on its business, as approximately 70% of its aluminum produced in Canada is destined for U.S. customers.

As shown in the following chart, Canada is the most strategic supplier of primary aluminum to the U.S.:

CEO Oplinger highlighted that even if all idled smelting capacity in the U.S. were restarted (approximately 600,000 metric tons), the country would still face a shortfall of 3.6 million metric tons. Building sufficient new smelting capacity would require "at least five to six smelters" and "additional energy production equivalent to almost seven new nuclear reactors or more than 10 Hoover dams."

In the alumina market, prices have returned to historical averages after reaching record highs in Q4 2024:

Alcoa noted that with current alumina prices around $329/mt and high bauxite costs, over 80% of Chinese refineries are unprofitable, which could lead to production curtailments and provide price support.

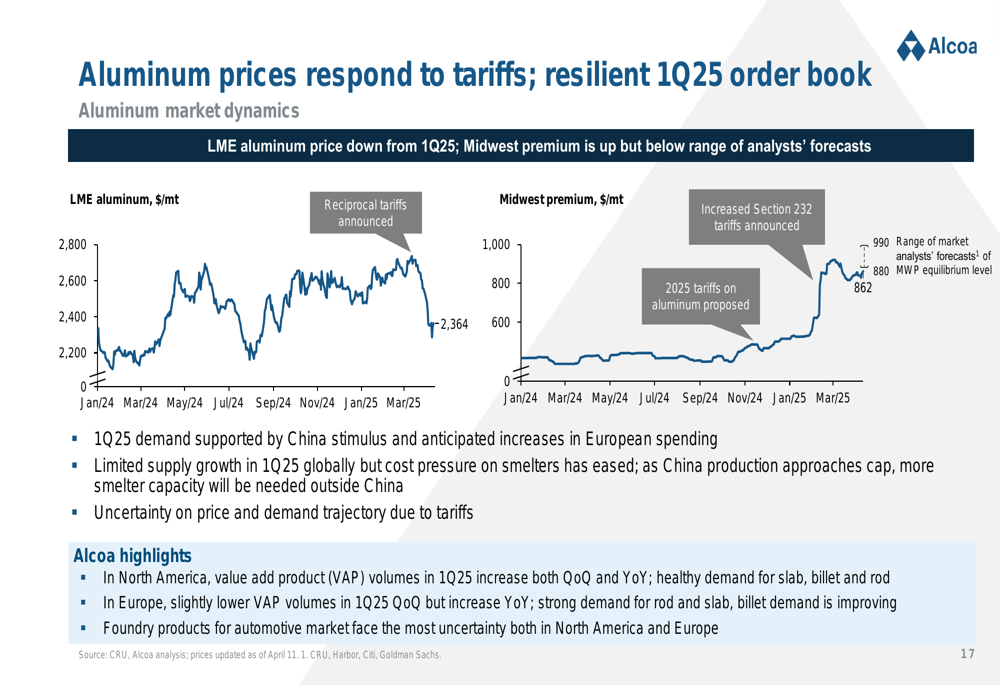

Aluminum prices have responded to the tariff announcements, with the LME price declining but the Midwest premium increasing, though not to the extent analysts had forecast:

Forward-Looking Statements

For Q2 2025, Alcoa expects its Alumina segment to maintain the strong performance delivered in Q1. However, the Aluminum segment performance is projected to be unfavorable by approximately $105 million due to U.S. Section 232 tariff costs on imports of Canadian aluminum (approximately $90 million sequentially) and operating costs associated with the restart of the San Ciprián smelter (approximately $15 million).

The company provided the following outlook for key metrics in 2025:

- Alumina production: 9.5-9.7 million metric tons

- Alumina shipments: 13.1-13.3 million metric tons

- Aluminum production: 2.3-2.5 million metric tons

- Aluminum shipments: 2.6-2.8 million metric tons

- Pension and OPEB: $70 million

- Return-seeking capital expenditures: ~$75 million

- Sustaining capital expenditures: ~$625 million

CFO Molly Beerman emphasized maintaining investment-grade leverage metrics as a key financial priority, with a target adjusted net debt range of $1.0-$1.5 billion.

Alcoa highlighted its strong positioning to navigate market challenges, emphasizing its vertical integration, low carbon products portfolio, and strong balance sheet:

During the earnings call, Oplinger stated, "We had a strong first quarter with improved safety and stable production," while also acknowledging the challenges ahead, particularly related to tariffs and market uncertainty. The company remains focused on operational excellence, strategic initiatives, and navigating the dynamic aluminum market to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.