Oracle launches unified health data exchange console

Alcoa Corporation (NYSE:AA) presented its second quarter 2025 earnings results on July 16, revealing a significant sequential decline in financial performance primarily driven by lower alumina prices and tariff impacts. Despite these challenges, the company strengthened its cash position and made progress on strategic initiatives while maintaining a positive long-term outlook for aluminum demand.

Quarterly Performance Highlights

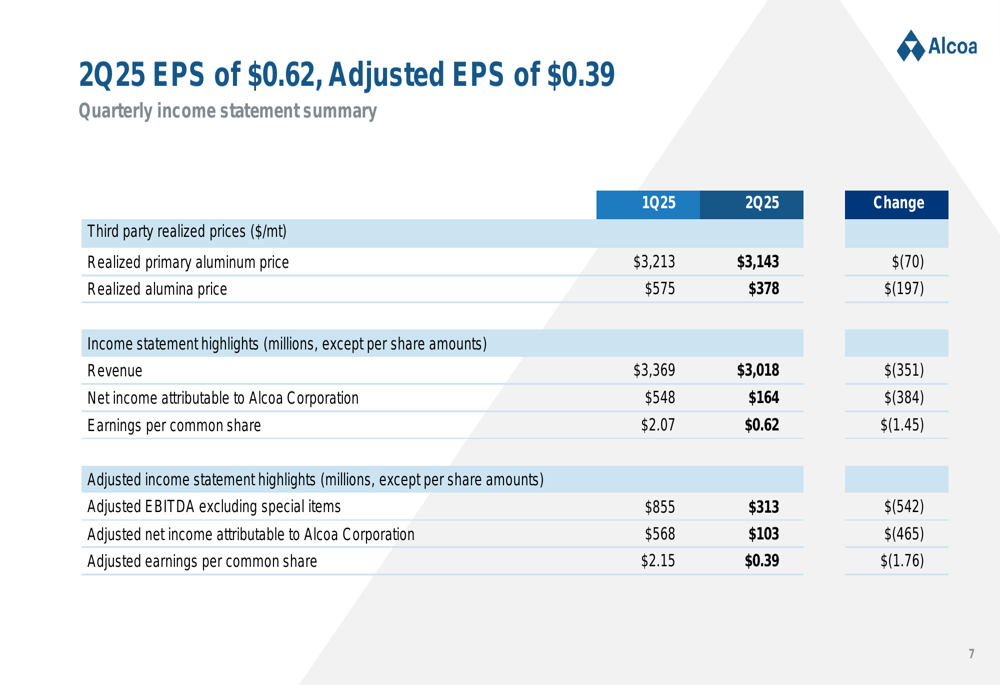

Alcoa reported a substantial drop in profitability for Q2 2025 compared to the previous quarter. Net income attributable to Alcoa Corporation decreased to $164 million from $548 million in Q1, while adjusted earnings per share fell to $0.39 from $2.15. Revenue declined to $3.02 billion from $3.37 billion in the previous quarter.

As shown in the following earnings summary chart, both realized aluminum and alumina prices decreased sequentially, contributing significantly to the earnings decline:

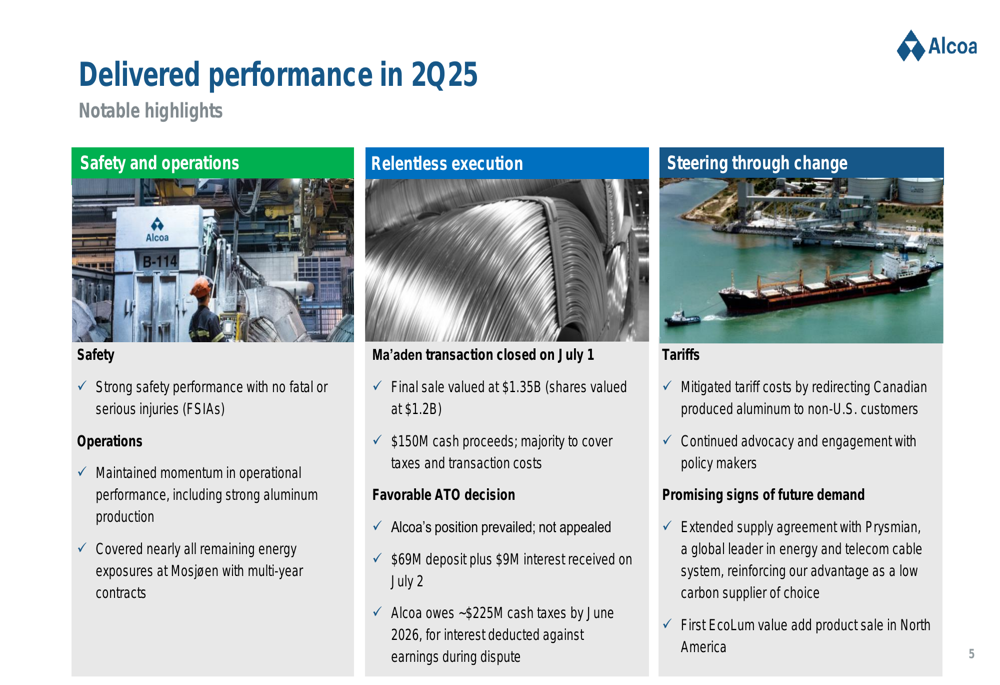

Despite the earnings pressure, Alcoa maintained strong operational performance with no fatal or serious injuries reported during the quarter. The company also covered nearly all remaining energy exposures at its Mosjøen facility with multi-year contracts and successfully closed the Ma’aden transaction on July 1 for $1.35 billion, generating $150 million in cash proceeds.

The following slide highlights these key achievements across safety, operations, and strategic execution:

Detailed Financial Analysis

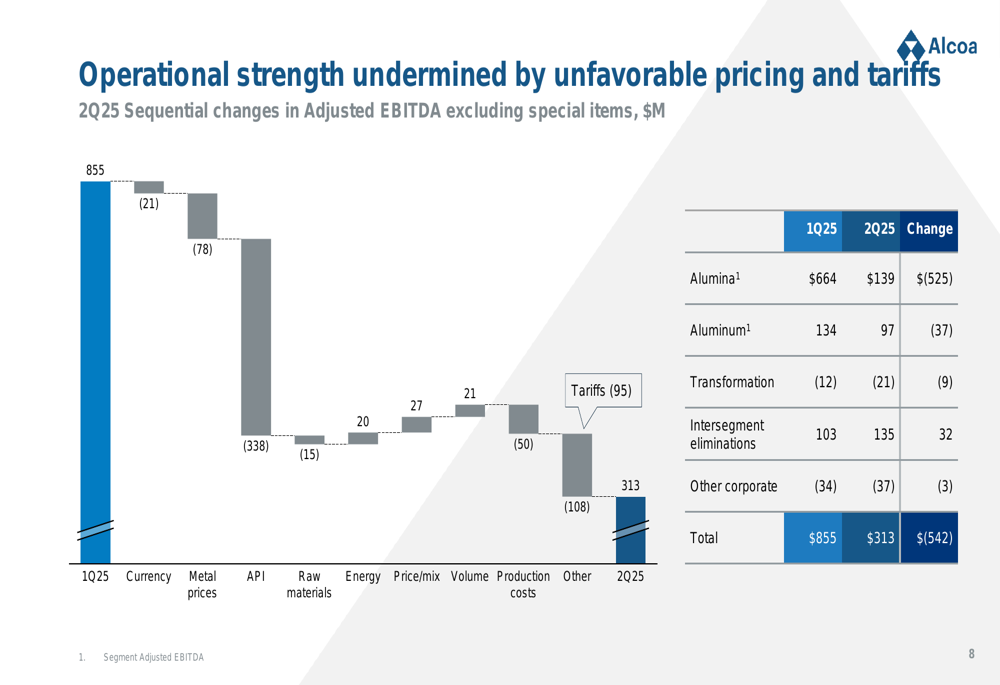

The sequential decline in Alcoa’s adjusted EBITDA was primarily driven by lower alumina prices, which had a negative impact of $338 million. Additional headwinds included tariffs ($95 million), production costs ($50 million), and currency effects ($21 million). These were partially offset by positive contributions from energy ($20 million), price/mix ($27 million), and volume ($21 million).

The following bridge chart illustrates these factors impacting the $542 million sequential decline in adjusted EBITDA:

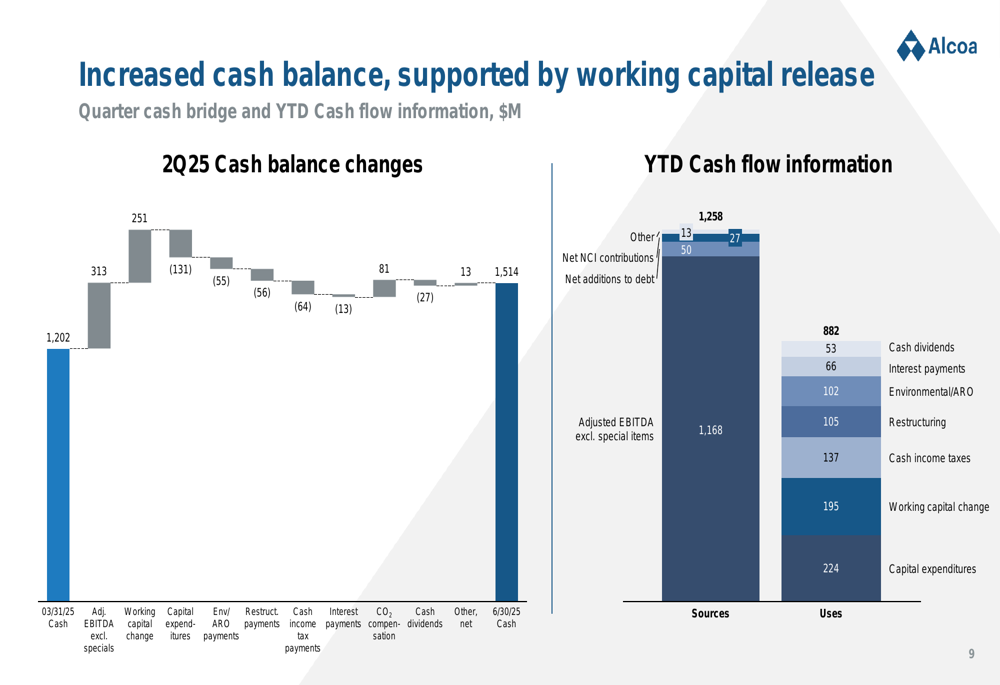

Despite the earnings decline, Alcoa’s cash position strengthened during the quarter, increasing from $1.2 billion on March 31 to $1.5 billion on June 30, 2025. This improvement was driven by positive working capital changes and adjusted EBITDA contribution, partially offset by capital expenditures, environmental payments, and other items.

The following cash flow bridge provides a detailed breakdown of these movements:

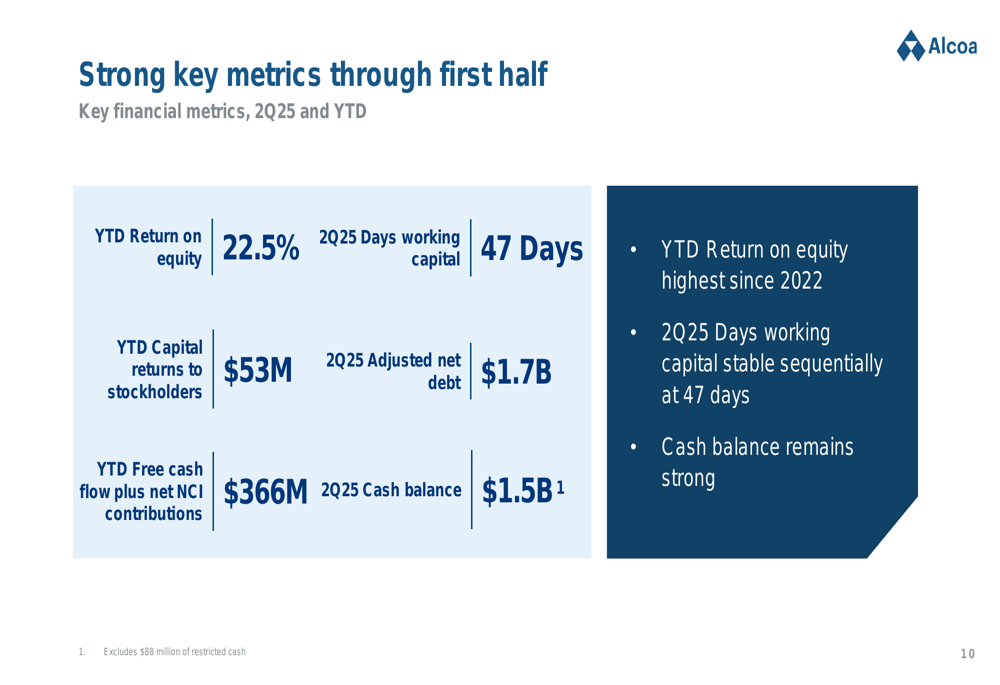

Alcoa maintained strong key financial metrics through the first half of 2025, including a 22.5% year-to-date return on equity, stable working capital at 47 days, and $366 million in year-to-date free cash flow plus net non-controlling interest contributions.

As illustrated in the following metrics summary:

Strategic Initiatives & Market Position

Alcoa completed the sale of its Ma’aden joint venture on July 1, generating $150 million in cash proceeds. The company also received a favorable Australian Taxation Office decision, resulting in a $69 million deposit plus $9 million in interest received on July 2, though Alcoa will owe approximately $225 million in cash taxes by June 2026.

In response to U.S. tariffs on aluminum, Alcoa has been redirecting Canadian aluminum and engaging in advocacy efforts with policymakers. The company also extended its supply agreement with Prysmian (BIT:PRY) and completed its first EcoLum value-add product sale in North America.

Market Dynamics & Industry Position

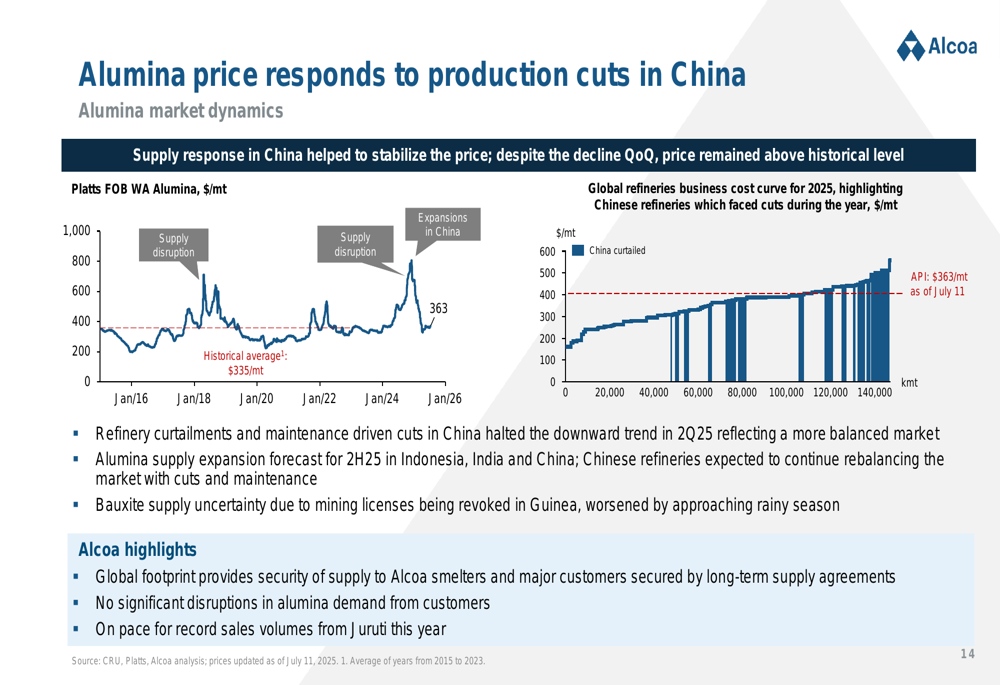

Alumina (OTC:AWCMY) prices faced downward pressure during the quarter, though refinery curtailments and maintenance-driven cuts in China helped stabilize the market. Bauxite supply uncertainty persists due to mining licenses being revoked in Guinea, compounded by the approaching rainy season.

The following chart illustrates these alumina market dynamics:

In the aluminum market, LME prices rebounded over Q2 from $2,285/mt to $2,600/mt, although average prices were down quarter-over-quarter. The U.S. tariff increase to 50% drove the Midwest premium higher, though it remains below the breakeven level considering the full tariff impact.

The aluminum market trends are illustrated in this chart:

Demand remained steady in Europe and North America during Q2, though tariff uncertainty prevented a sustained pickup. Alcoa reported stable value-added product order volumes in North America, with healthy demand for slab, billet, and rod products. In Europe, value-added product volumes improved slightly quarter-over-quarter, with billet demand improving and rod and slab demand remaining strong.

Forward-Looking Statements

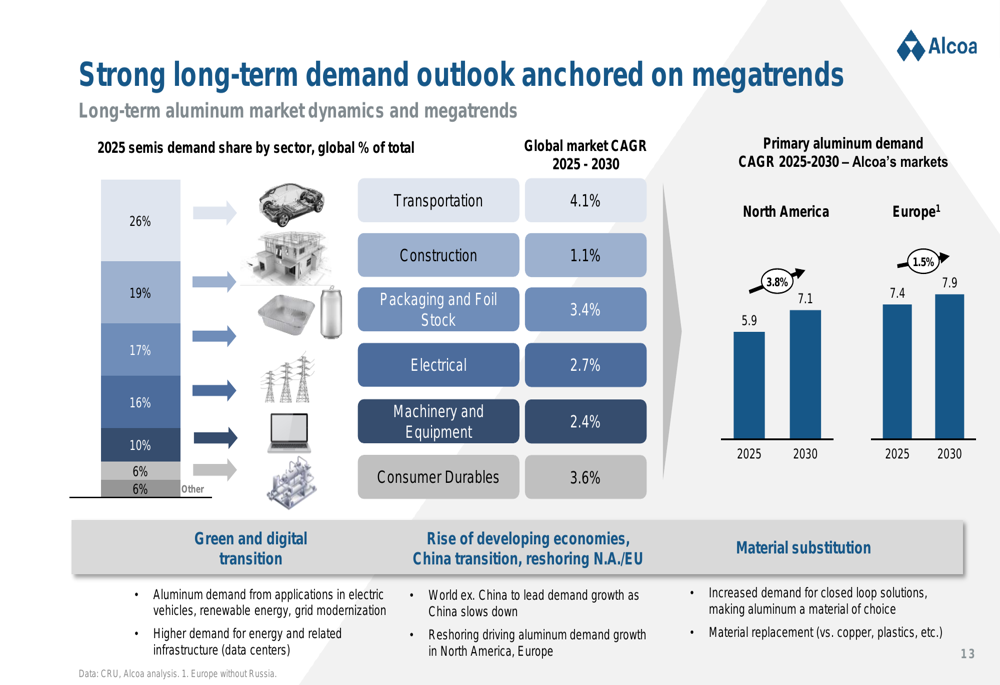

Alcoa maintains a positive long-term outlook for aluminum demand, driven by several megatrends including transportation electrification, renewable energy expansion, grid modernization, and data center growth. The company projects primary aluminum demand CAGR of 3.8% in North America and 1.5% in Europe for 2025-2030.

The following chart details these long-term demand drivers:

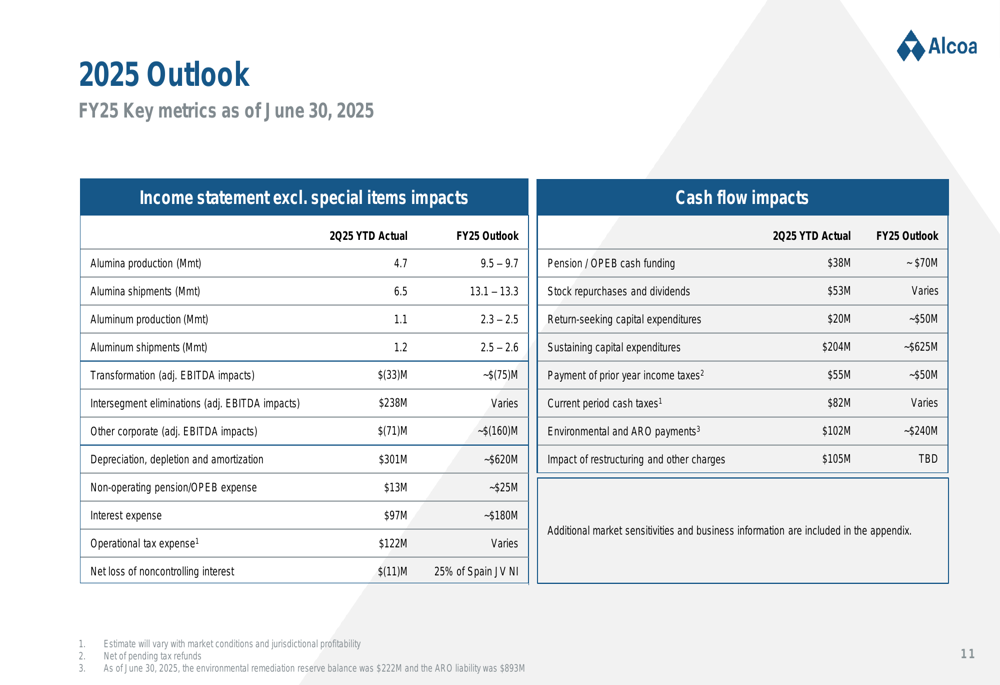

For the full year 2025, Alcoa expects alumina production of 9.5-9.7 million metric tons and aluminum production of 2.3-2.5 million metric tons. The company’s focus areas include safety, operational stability, continuous improvement, advancing tariff reform dialogue, and progressing Western Australia mining approvals.

As shown in the outlook slide:

Looking ahead, Alcoa’s CEO William Oplinger emphasized the company’s commitment to "focus on safety, stability, continuous improvement" while adapting operations to preserve profitability amid challenging market conditions.

Alcoa’s stock closed at $28.49 on July 16, 2025, up 0.25% for the day, and gained an additional 0.56% in after-hours trading following the earnings release. The stock has traded between $21.53 and $47.77 over the past 52 weeks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.