U.S. stocks open higher with government shutdown, Fed speakers in focus

Introduction & Market Context

Alfa | Sigma presented its second quarter 2025 earnings on July 24, 2025, marking its first full quarter as a pure-play packaged food business following the completion of its corporate transformation. The company announced that Alfa shares began trading as a focused food company on April 7, with its Global Industry Classification Standard (GICS) changing to "Consumer Staples" to align with this strategic shift.

The presentation highlighted the company’s finalized transformation, with preparations underway to change Alfa’s name and ticker to reflect its new identity. This strategic repositioning follows the spin-off of Controladora Alpek, which was classified as a "Discontinued Operation" under IFRS standards.

As shown in the following slide detailing the company’s transformation:

Quarterly Performance Highlights

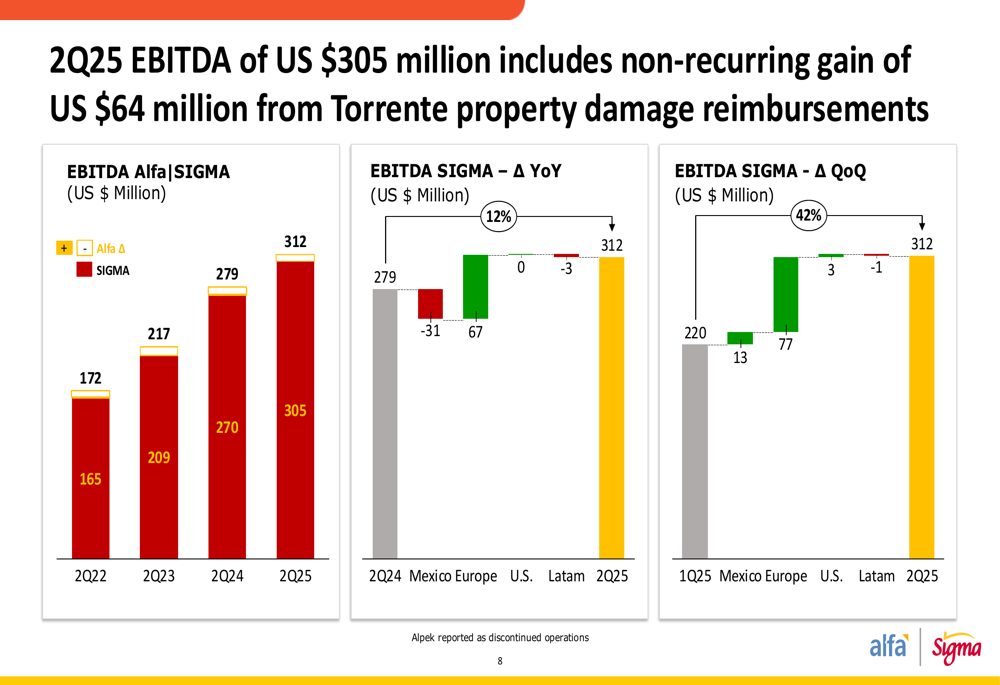

Alfa | Sigma reported Q2 2025 EBITDA of US $305 million, representing a 13% increase compared to the $270 million reported in Q2 2024. However, this figure includes a significant non-recurring gain of US $64 million from property damage reimbursements related to the Torrente facility in Spain. Year-to-date EBITDA reached US $576 million.

The company’s volume performance remained relatively stable at 460 kilotons, slightly down from 462 kilotons in Q2 2024, while revenue increased marginally to US $2,297 million from US $2,277 million in the same period last year. This performance reflects the company’s resilient volume and effective revenue management amid challenges from higher protein input costs and Mexican Peso depreciation.

The following chart illustrates the company’s EBITDA performance:

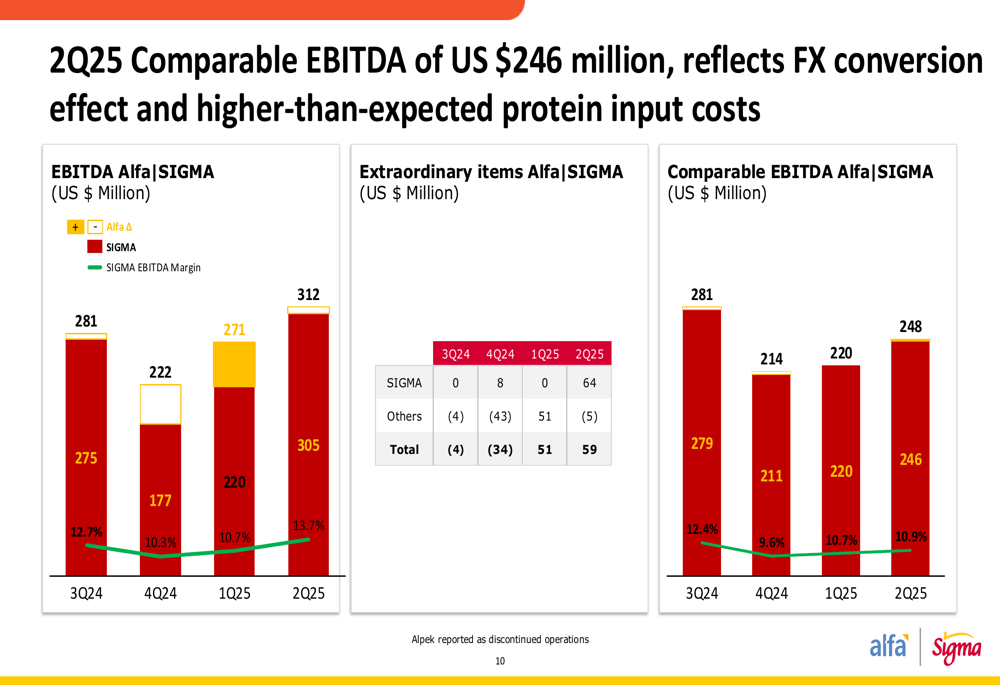

On a comparable basis, excluding extraordinary items, Q2 2025 EBITDA was US $246 million, reflecting foreign exchange conversion effects and higher-than-expected protein input costs. This provides a clearer picture of the company’s underlying operational performance.

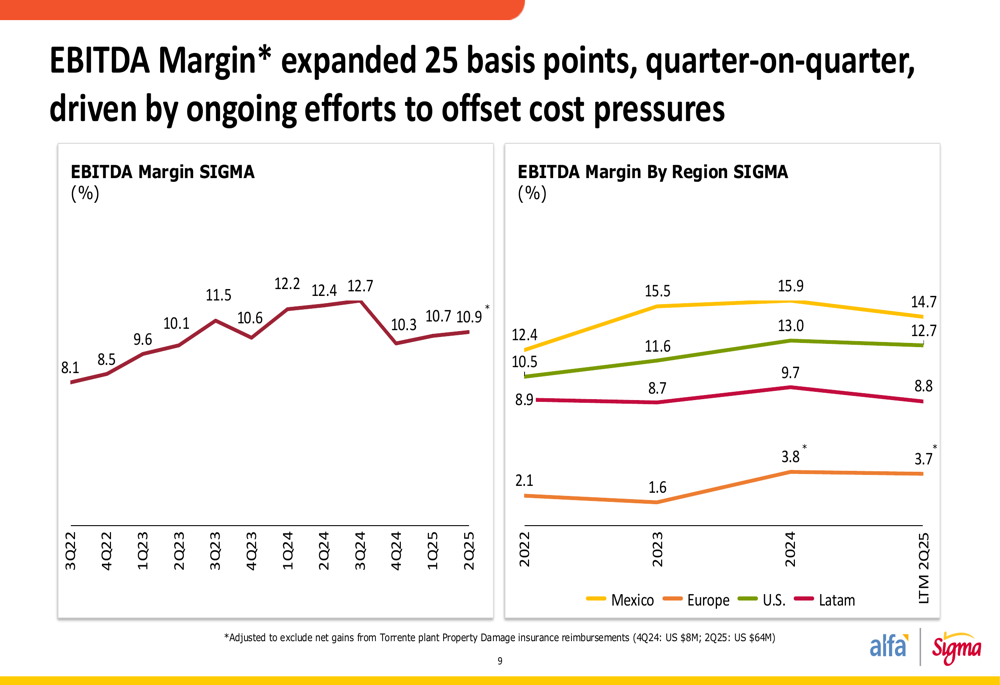

EBITDA margin expanded by 25 basis points quarter-on-quarter to 10.9%, driven by ongoing efforts to offset cost pressures. The margin trend shows the company’s ability to maintain profitability despite challenging market conditions.

Regional Performance Analysis

Alfa | Sigma’s performance varied significantly across regions, with each market facing unique opportunities and challenges:

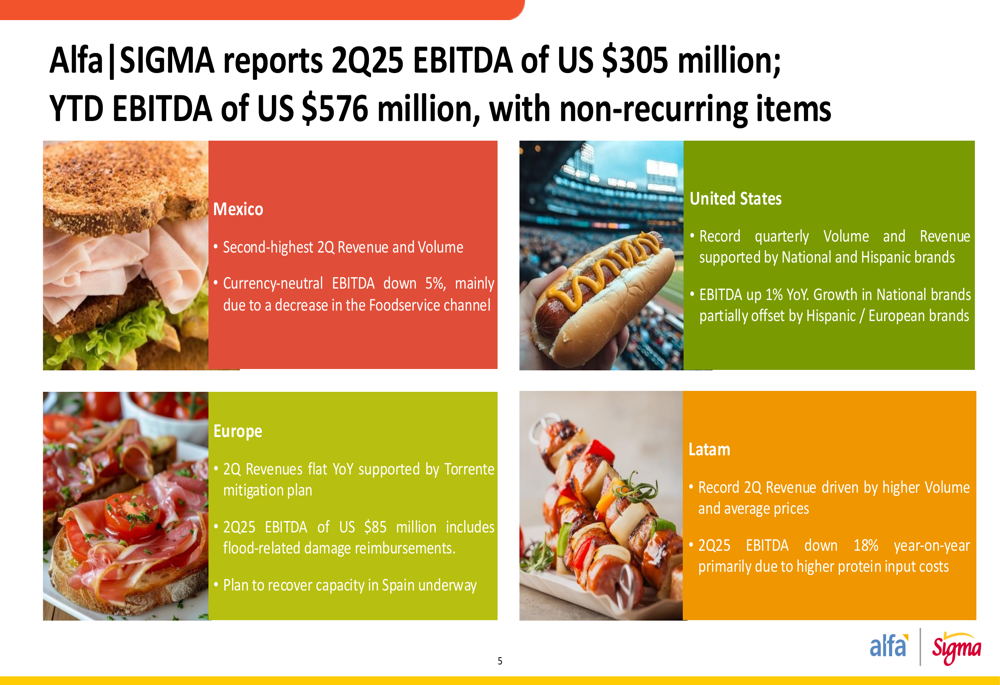

In Mexico, the company reported its second-highest Q2 revenue and volume, though currency-neutral EBITDA declined 5% year-over-year, primarily due to decreased performance in the Foodservice channel.

The United States achieved record quarterly volume and revenue, supported by strong performance in National and Hispanic brands. EBITDA increased 1% year-over-year, with growth in National brands partially offsetting challenges in Hispanic and European brands.

Europe delivered flat year-over-year revenues, supported by the Torrente mitigation plan. Q2 2025 EBITDA of US $85 million includes flood-related damage reimbursements, with plans to recover capacity in Spain underway.

Latin America achieved record Q2 revenue driven by higher volume and average prices, though Q2 2025 EBITDA declined 18% year-over-year, primarily due to higher protein input costs.

The following slide summarizes the regional performance highlights:

Financial Position and Debt

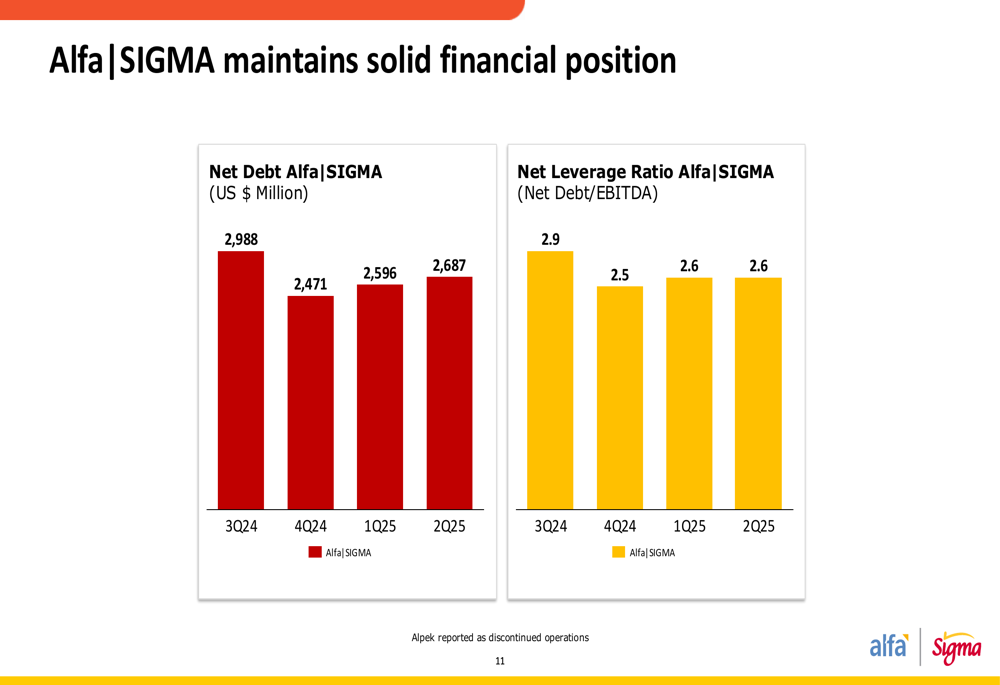

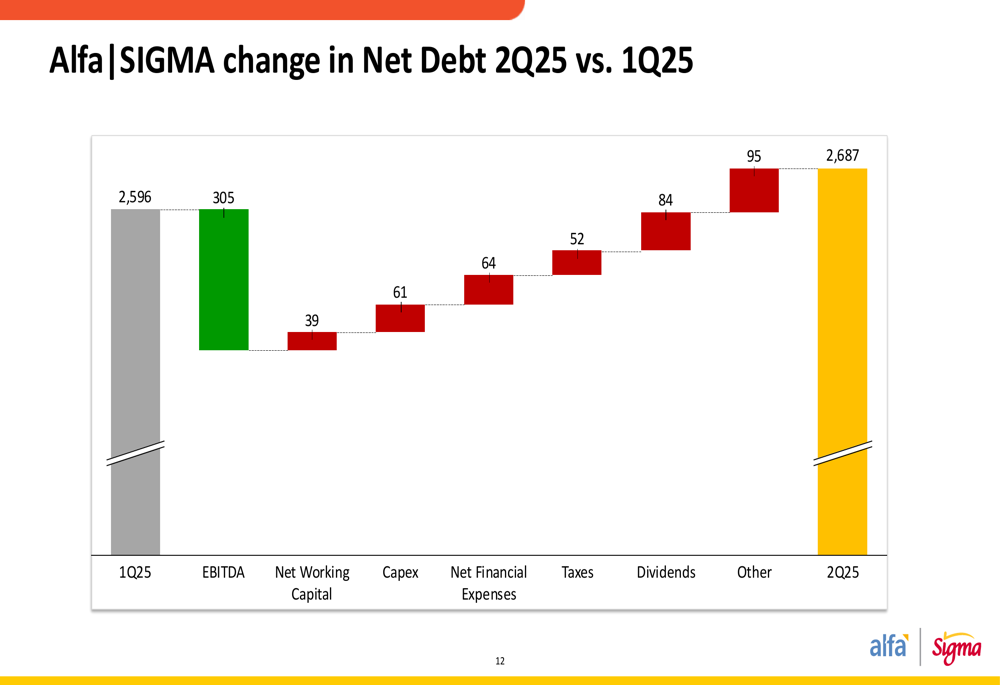

Alfa | Sigma maintained a solid financial position in Q2 2025, with net debt of US $2,687 million, up from US $2,596 million in Q1 2025. The net leverage ratio remained stable at 2.6x EBITDA.

The increase in net debt during the quarter was primarily driven by dividend payments of US $84 million, capital expenditures of US $61 million, net financial expenses of US $64 million, and tax payments of US $52 million. These outflows were partially offset by EBITDA generation of US $305 million.

The following waterfall chart details the changes in net debt from Q1 to Q2 2025:

Strategic Initiatives and Outlook

Alfa | Sigma outlined several strategic initiatives, with particular focus on the recovery plan for its Torrente facility in Spain. The company plans to invest €134 million in Valencia and €23 million in "La Bureba," with the new plant expected to be fully operational by 2027.

On the sustainability front, the company published SIGMA’s 2024 Sustainability and UN Global Compact reports, demonstrating its commitment to environmental and social responsibility. Additionally, Campofrío improved its position in Merco’s "Companies and Leaders" ranking in Spain, moving up two spots to 18th place year-over-year.

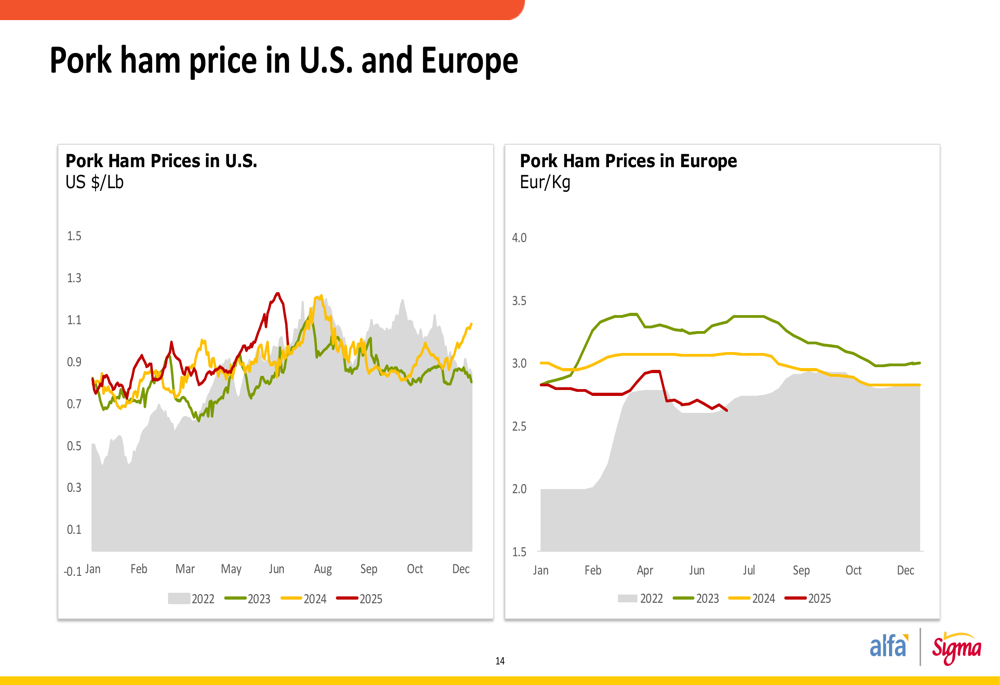

The company continues to monitor raw material price trends, which remain a key factor affecting profitability. Pork ham prices in the U.S. and Europe, poultry raw materials, and dairy commodities all impact the company’s cost structure and pricing strategies.

Looking ahead, Alfa | Sigma faces both opportunities and challenges. The completed transformation to a pure-play food business provides strategic clarity, while investments in recovery and capacity expansion position the company for future growth. However, ongoing pressures from raw material costs and currency fluctuations will require continued focus on operational efficiency and pricing strategies to maintain and improve margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.