TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Alfa Laval AB (STO:ALFA) released its Q1 2025 financial results on April 29, showcasing strong revenue growth despite facing headwinds in order intake. The company’s stock reacted negatively to the earnings announcement, with shares declining 0.23% to 393 SEK as of May 7, 2025, after initially dropping 1.1% following the results.

The Swedish industrial equipment manufacturer reported earnings per share (EPS) of 4.82 SEK, falling short of analyst expectations of 4.93 SEK, despite posting significant improvements in sales and profitability compared to the same period last year.

Quarterly Performance Highlights

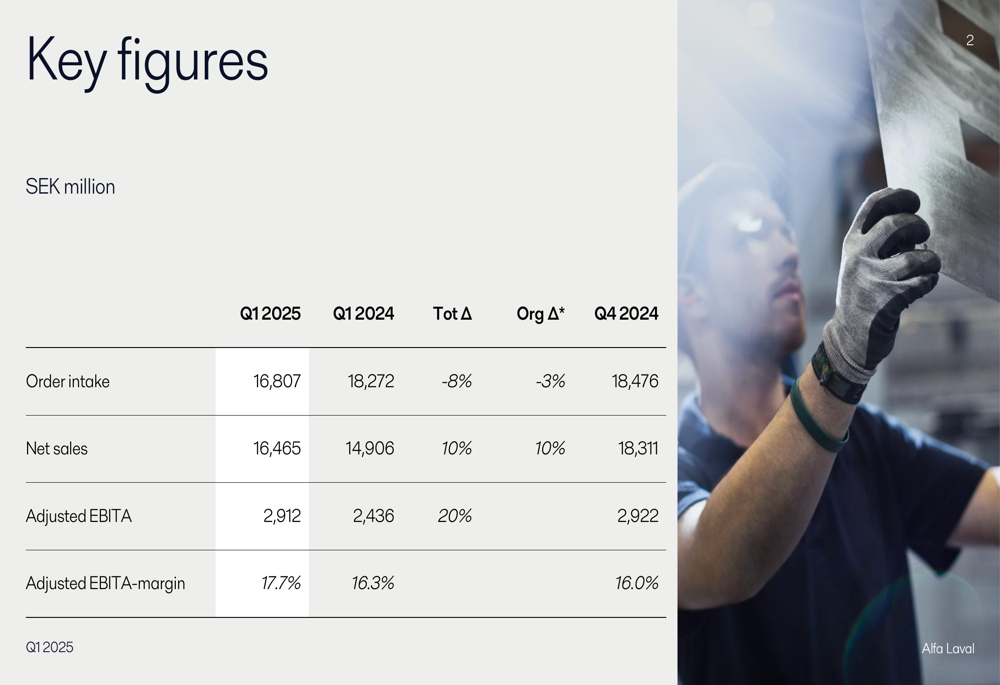

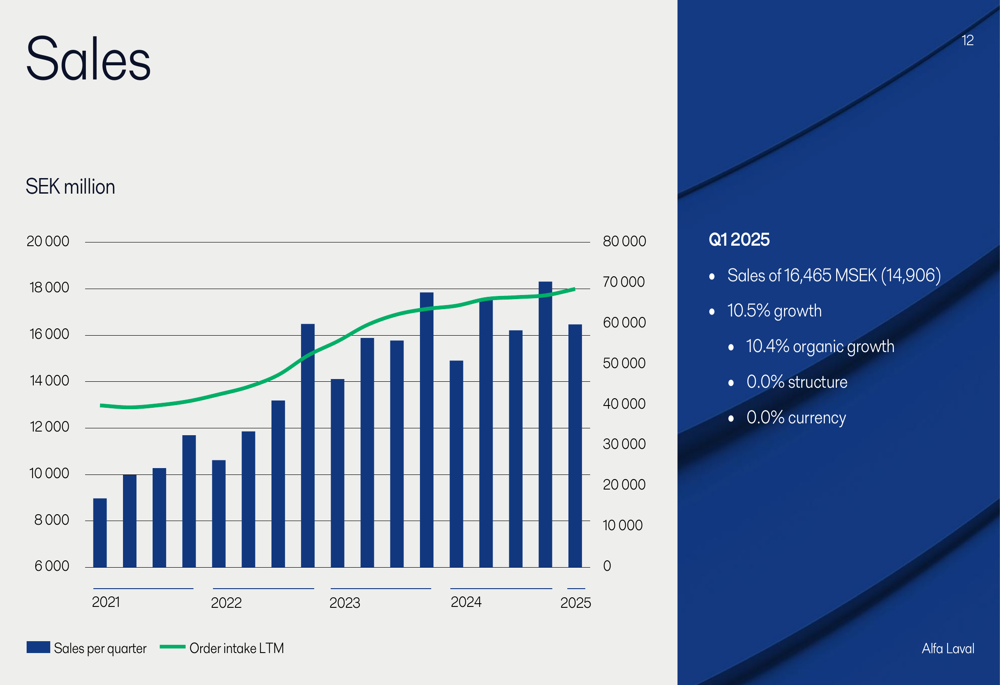

Alfa Laval delivered mixed results for the first quarter of 2025, with strong sales growth offset by declining order intake. Net sales reached 16,465 MSEK, representing a 10.5% increase compared to Q1 2024, with organic growth of 10.4%.

As shown in the following chart of key financial figures:

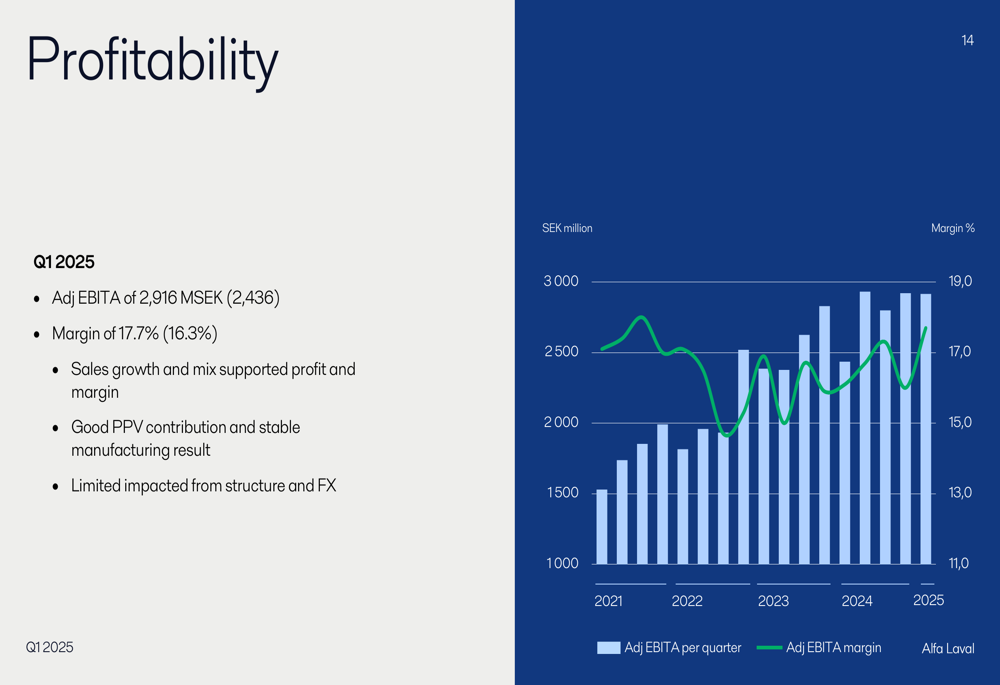

The company’s profitability metrics showed substantial improvement, with adjusted EBITA increasing by 20% to 2,912 MSEK and the adjusted EBITA margin expanding to 17.7% from 16.3% in the prior-year period. However, order intake declined by 8% to 16,807 MSEK, with organic decline of 3.2% and negative currency effects of 4.8%.

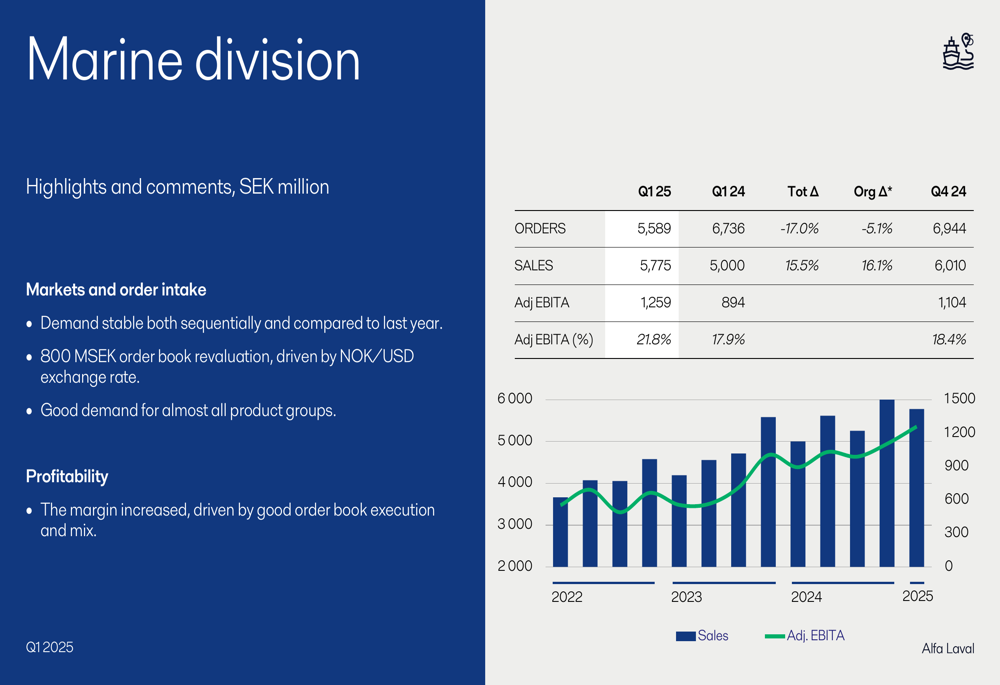

All three divisions contributed to the sales growth, though with varying performance in order intake. The Marine division showed the strongest profitability with an adjusted EBITA margin of 21.8%, as illustrated in the divisional breakdown:

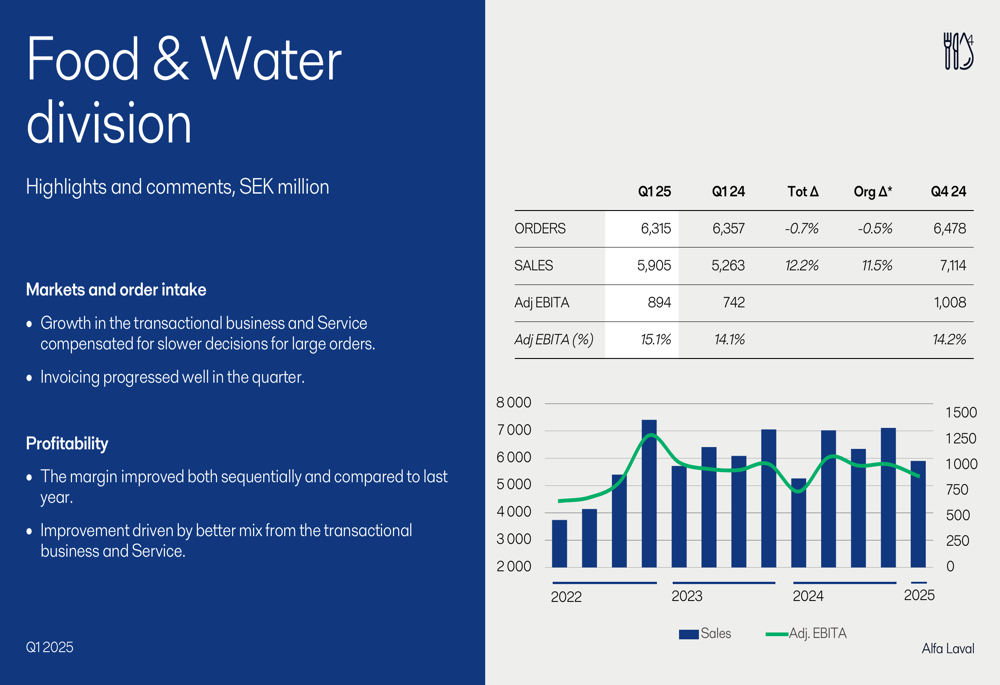

The Food & Water division demonstrated robust sales growth of 12.2% year-over-year, reaching 5,905 MSEK, with improved margins due to better mix from transactional business and service:

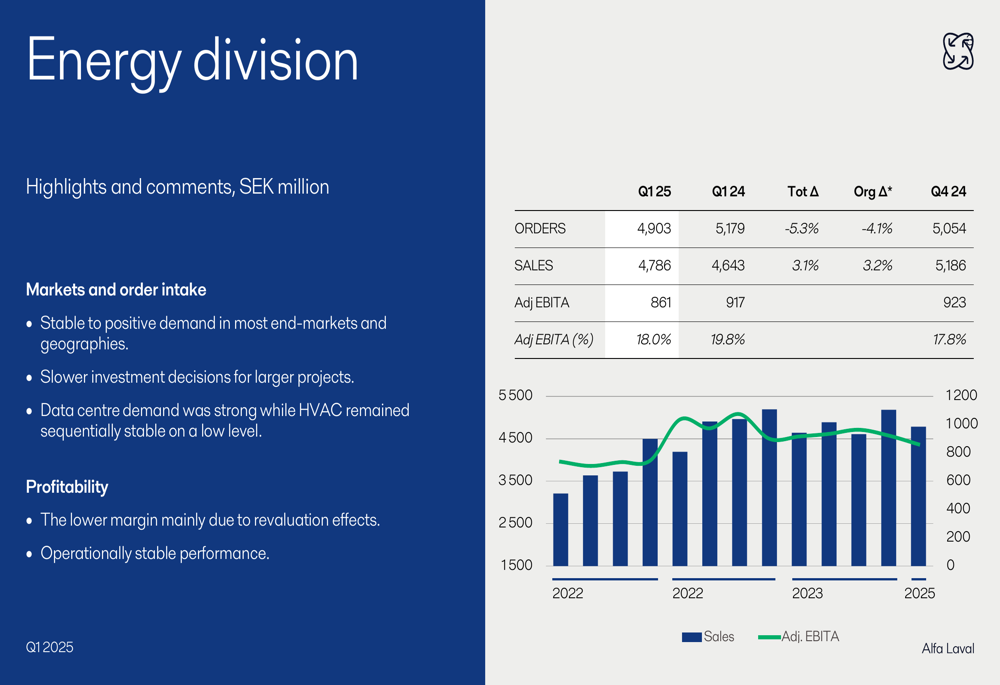

Meanwhile, the Energy division reported more modest sales growth of 3.1%, with stable to positive demand in most end-markets and particularly strong demand for data centers:

Strategic Initiatives

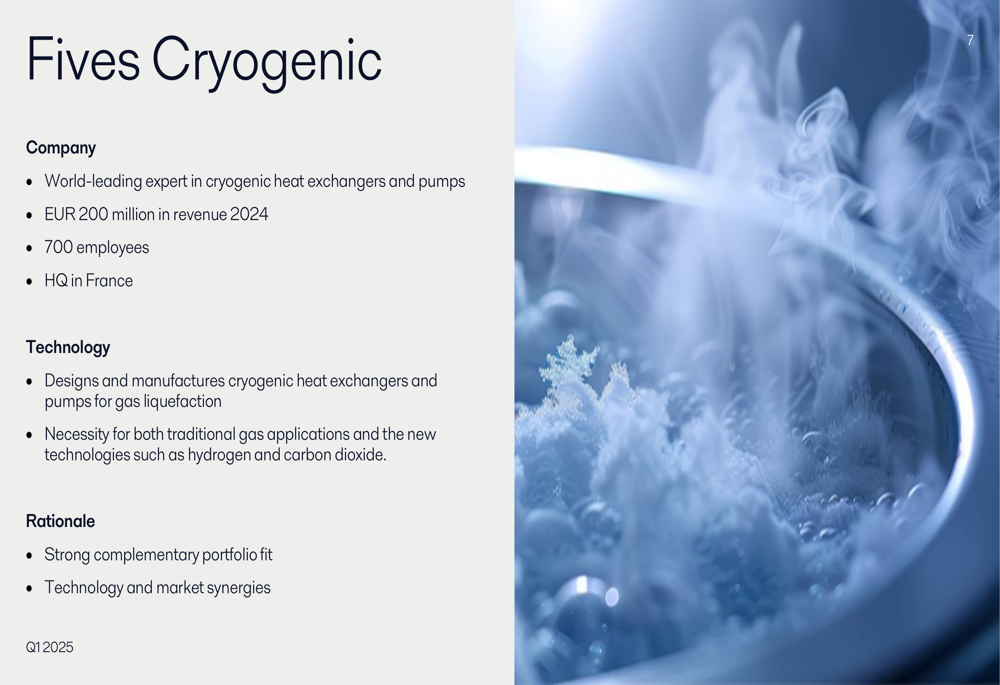

A key strategic development announced during the quarter was the acquisition of Fives Cryogenic, a world-leading expert in cryogenic heat exchangers and pumps. With EUR 200 million in revenue in 2024 and 700 employees, this acquisition strengthens Alfa Laval’s position in gas liquefaction technologies.

The acquisition provides complementary portfolio fit and technology synergies, particularly for both traditional gas applications and emerging technologies such as hydrogen and carbon dioxide processing:

Detailed Financial Analysis

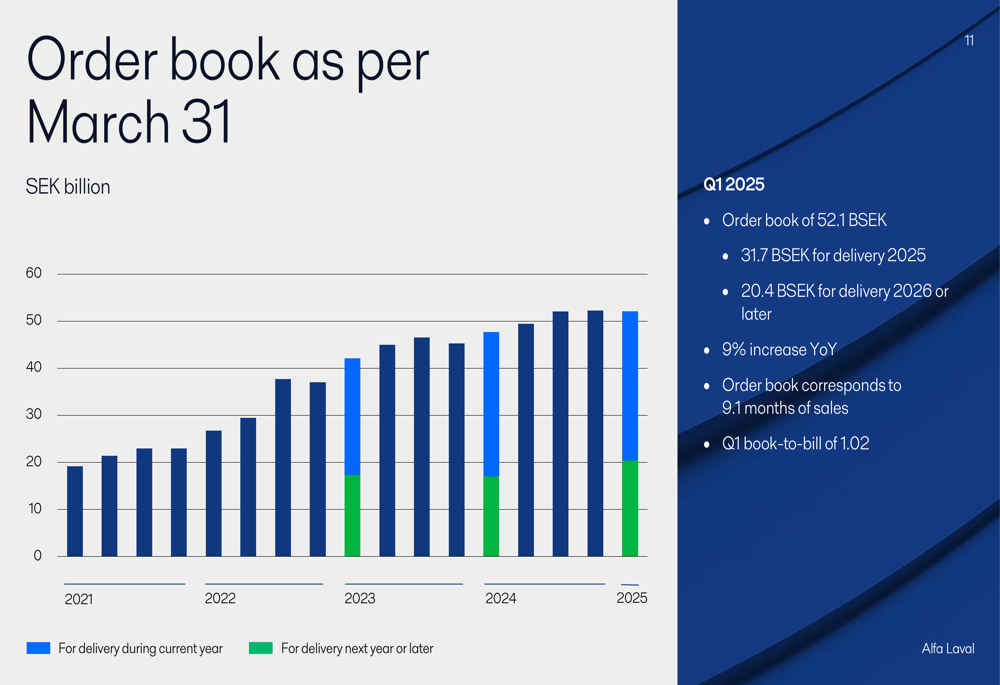

Alfa Laval’s order book remained strong at 52.1 billion SEK as of March 31, 2025, representing a 9% increase year-over-year. The order book corresponds to 9.1 months of sales, providing solid visibility for future revenue:

The company’s sales trend continued its upward trajectory, with quarterly sales reaching near-record levels:

Profitability performance showed consistent improvement, with adjusted EBITA margin reaching 17.7% in Q1 2025, supported by sales growth, favorable mix, and good price/cost contribution:

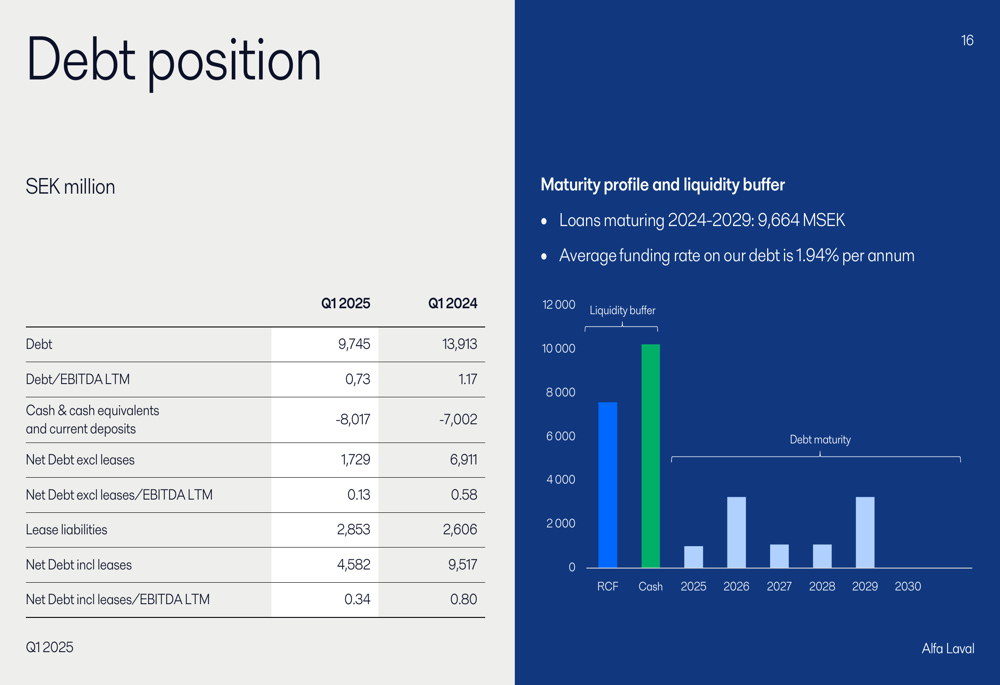

Alfa Laval significantly strengthened its financial position, reducing its net debt excluding leases to just 1,729 MSEK, resulting in a net debt to EBITDA ratio of only 0.13, down from 0.58 in Q1 2024:

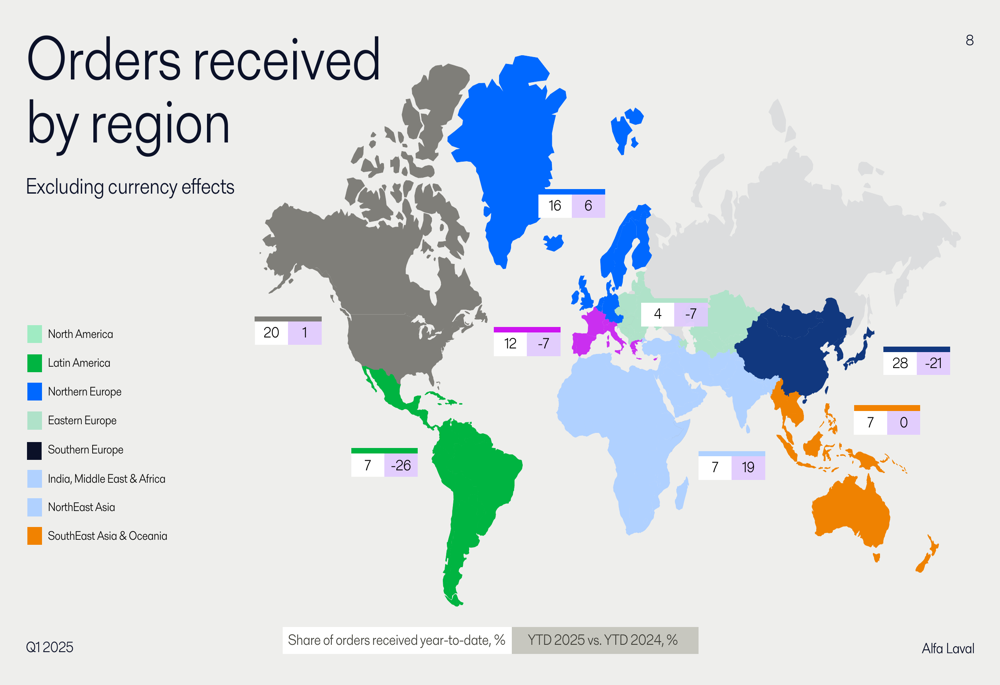

The company’s regional performance showed considerable variation, with strong growth in India, Middle East & Africa (+19%) and Northern Europe (+6%), while North East Asia (-21%) and Latin America (-26%) experienced significant declines:

Service orders continued to represent a substantial portion of the business, accounting for 42% of Marine division orders, 31% of Food & Water orders, and 30% of Energy division orders in Q1:

Forward-Looking Statements

Looking ahead, Alfa Laval provided a cautious outlook for the second quarter of 2025, stating: "We expect demand in the second quarter to be on about the same level compared to the first quarter." This suggests the company anticipates stable conditions without significant growth in order intake.

For the full year 2025, Alfa Laval estimates capital expenditures between 2.5 and 3.0 billion SEK, with projected currency impacts on EBITA of approximately 200 MSEK. The company expects a tax rate between 24-26% and has proposed an increased dividend of 8.50 SEK per share, up from 7.50 SEK previously.

CEO Tom Erixon highlighted the company’s strong financial position during the earnings call, noting that Alfa Laval is "essentially debt-free" with a healthy return on adjusted capital employed of 24%. He also emphasized the company’s competitive advantage, stating that challenging market conditions often work to Alfa Laval’s benefit in terms of market positioning.

While the presentation emphasized positive performance metrics, investors appeared to focus on the EPS miss and declining order intake, particularly in key Asian markets. The company faces potential challenges from currency revaluation impacts, slowing capital expenditure decisions in certain markets, and evolving tariff environments that could affect future performance.

Despite these challenges, Alfa Laval’s strong balance sheet, improved profitability, and strategic acquisitions position the company to navigate market uncertainties while continuing to invest in growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.