ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Alfa Laval AB (STO:ALFA) presented its third quarter 2025 financial results on October 28, revealing solid sales growth and improved profitability despite declining order intake. The company's stock dipped 1.04% to 466.6 SEK following the presentation, suggesting investors remain cautious about future growth prospects despite the strong current performance.

The industrial equipment manufacturer, which specializes in heat transfer, separation, and fluid handling technologies, demonstrated resilience in a challenging market environment, with its Marine division delivering particularly strong results.

Quarterly Performance Highlights

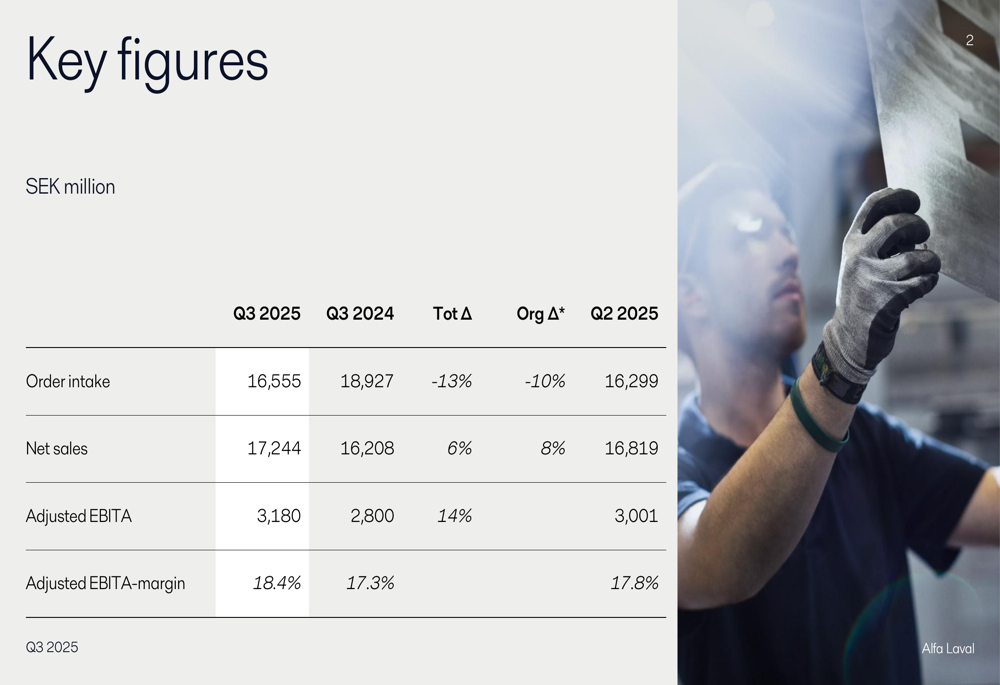

Alfa Laval reported Q3 2025 sales of 17,244 million SEK, representing a 6.4% increase compared to the same period last year, with organic growth reaching 8.2%. Meanwhile, order intake declined to 16,555 million SEK, down 13% year-over-year or 10.4% organically.

As shown in the following summary of key financial metrics:

Profitability improved significantly, with adjusted EBITA increasing 14% to 3,180 million SEK and the corresponding margin expanding to 18.4% from 17.3% in Q3 2024. This improvement was attributed to organic sales growth, favorable product mix, and good price/cost management.

Earnings per share rose to 5.53 SEK, up from 4.77 SEK in the comparable period, exceeding analyst expectations of 5.28 SEK according to market data. Despite these strong results, the book-to-bill ratio fell below 1.0 to 0.96, indicating potential challenges for future revenue growth.

The company's order book stood at 50.9 billion SEK as of September 30, representing a slight 2% year-over-year decrease but still corresponding to 8.9 months of sales. The order book is divided between 16.3 billion SEK for delivery in 2025 and 34.5 billion SEK for 2026 or later.

Divisional Performance Analysis

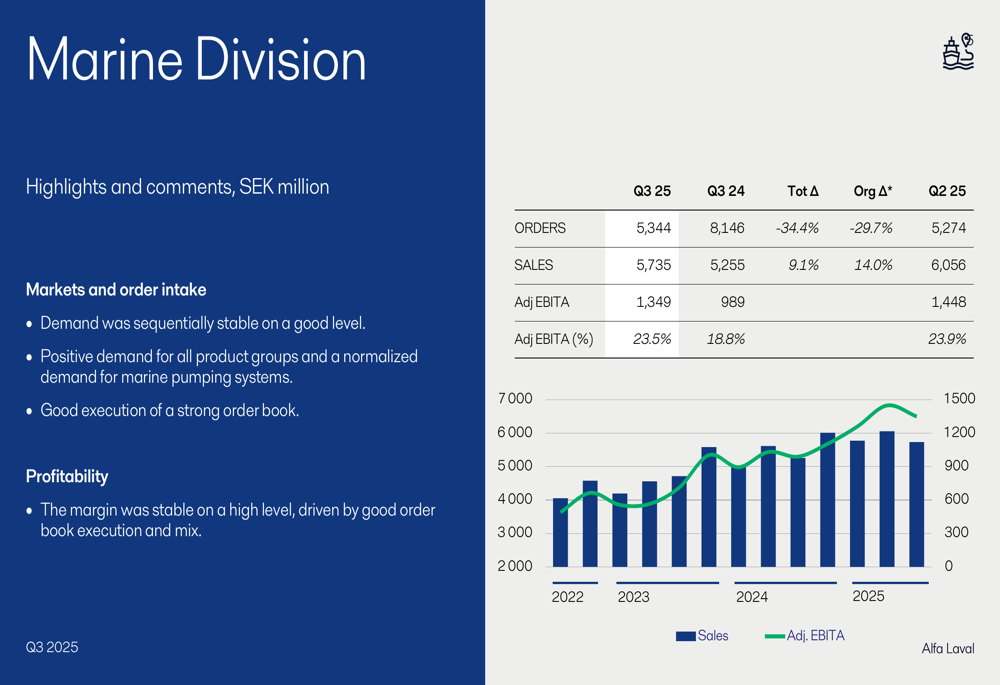

The Marine division emerged as the standout performer with an adjusted EBITA margin of 23.5%, up from 18.8% in Q3 2024. Despite a significant 34.4% year-over-year decline in orders, the division delivered 9.1% sales growth thanks to strong order book execution.

The Marine division's performance is illustrated in the following chart:

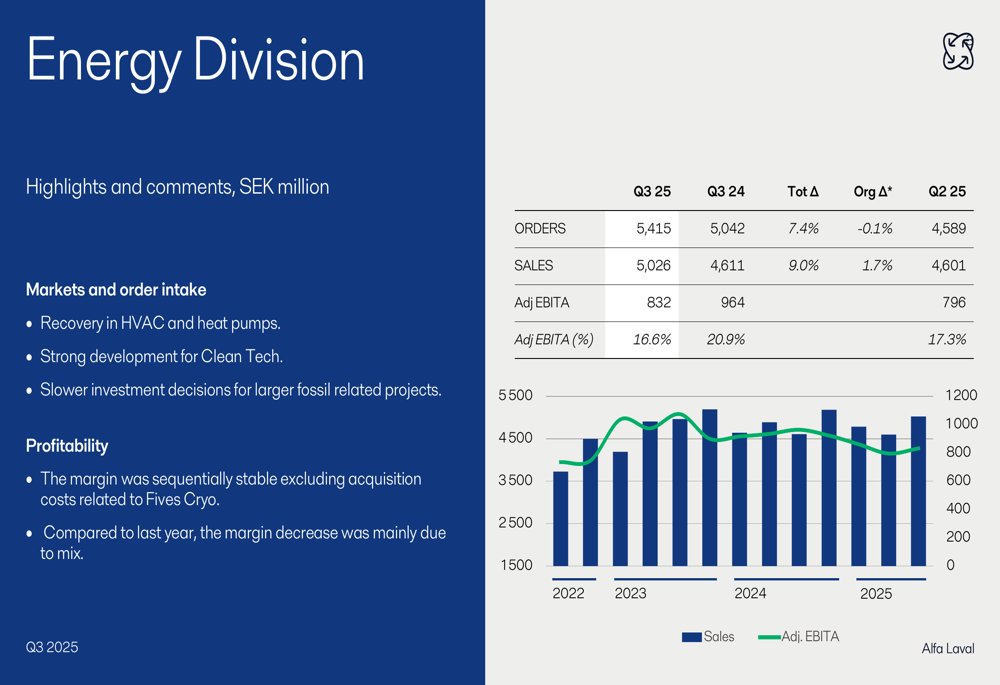

The Energy division reported a 7.4% increase in orders and 9.0% higher sales compared to Q3 2024. However, its adjusted EBITA margin contracted to 16.6% from 20.9%, which management attributed primarily to mix effects and acquisition costs related to Fives Cryo.

As shown in the Energy division's performance metrics:

The Food & Water division delivered modest growth with orders up 1.0% and sales increasing 2.2% year-over-year. Its profitability improved, with the adjusted EBITA margin rising to 16.1% from 15.7%, driven by a positive product mix.

Service orders remained a bright spot, representing significant portions of total orders across all divisions: Marine (40%), Food & Water (31%), and Energy (23%). The following chart illustrates the service order intake trend:

Financial Position and Cash Flow

Alfa Laval's financial position showed notable changes during the quarter, with significant acquisition activity impacting debt levels. The company's net debt excluding leases increased substantially to 11,977 million SEK, resulting in a net debt to EBITDA ratio of 0.86, up from 0.39 in Q3 2024.

Cash flow from operating activities reached 2,206 million SEK, down from 3,924 million SEK in the comparable period, primarily due to negative working capital developments of -1,107 million SEK compared to a positive 1,061 million SEK last year.

The profitability trend is clearly visible in the following chart showing adjusted EBITA and margin development:

Free cash flow amounted to 1,661 million SEK, but significant acquisition expenditures of 8,785 million SEK resulted in a negative cash flow after investing activities of -7,094 million SEK. This acquisition activity appears to be part of Alfa Laval's strategic growth initiatives, particularly in the cleantech sector.

Outlook and Market Reaction

Looking ahead, Alfa Laval provided a cautious outlook statement: "We expect demand in the fourth quarter to be on about the same level as in the third quarter."

This conservative guidance, combined with the declining order intake, likely contributed to the market's lukewarm reaction despite the strong financial results. The stock closed down 1.04% at 466.6 SEK following the presentation.

For Q4 2025, the company forecasts capital expenditures of approximately 0.7 billion SEK, with 2.5-3.0 billion SEK projected for FY 2026. The tax rate is expected to remain between 24-26%.

Alfa Laval continues to focus on growth opportunities in cleantech and marine technologies, with particular strength noted in China and the United States, which represent its top markets. The company appears well-positioned in energy transition technologies, though investors seem to be taking a wait-and-see approach regarding future growth prospects amid macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.