BofA sees higher gold prices, likely to hit $5,000/oz in 2026

Algonquin Power & Utilities Corp (NYSE:AQN) presented its first quarter 2025 earnings results on May 9, showing a dramatic turnaround in profitability as the company continues to refocus its business on regulated utility operations following the divestiture of its renewable energy business.

Quarterly Performance Highlights

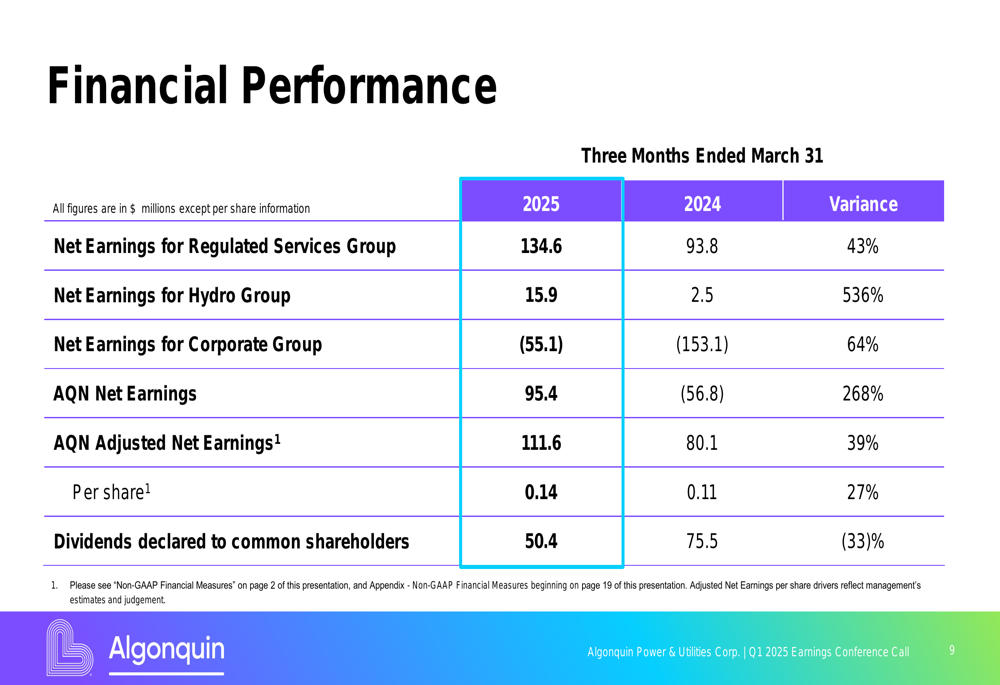

Algonquin reported net earnings of $95.4 million for Q1 2025, a 268% increase from the $56.8 million loss recorded in the same period last year. Adjusted net earnings rose 39% year-over-year to $111.6 million, while adjusted earnings per share remained flat at $0.14, matching the year-ago figure but significantly exceeding analyst expectations of $0.09.

The company’s stock responded positively to the earnings beat, rising 7.97% to $5.90 in trading following the announcement, though still trading below its 52-week high of $6.76.

"Our objective is to compare ourselves to best in class on both capital and O&M discipline," CEO Rod West emphasized during the earnings call, highlighting the company’s commitment to operational excellence and cost management as it positions itself as a "premium utility."

The following chart details the company’s financial performance by business segment:

Detailed Financial Analysis

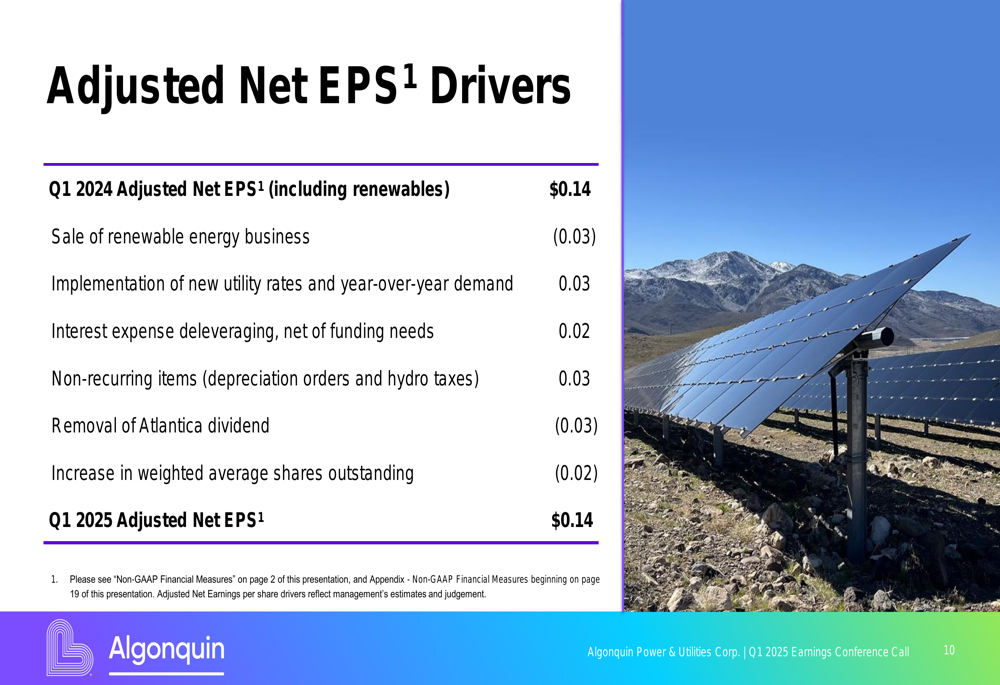

Despite the impressive headline earnings growth, Algonquin’s adjusted EPS remained flat year-over-year at $0.14 due to several offsetting factors. The company’s presentation provided a detailed breakdown of these EPS drivers:

As shown in the chart, positive contributions from new utility rates (+$0.03), interest expense savings from deleveraging (+$0.02), and non-recurring items (+$0.03) were offset by the impact of the renewable energy business sale (-$0.03), removal of Atlantica dividend (-$0.03), and dilution from increased shares outstanding (-$0.02).

The company also reported a 33% reduction in dividends declared to common shareholders, which fell to $50.4 million from $75.5 million in Q1 2024, reflecting the company’s strategic shift and capital allocation priorities.

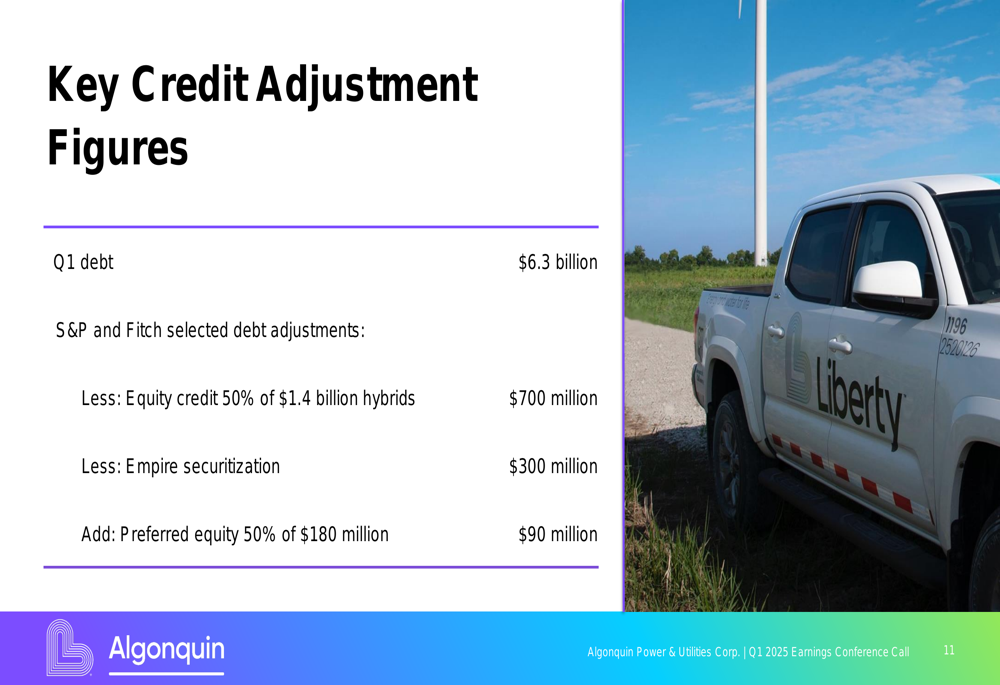

Algonquin’s debt position stood at $6.3 billion at the end of Q1, with the company highlighting several credit adjustments:

Strategic Initiatives & Rate Case Updates

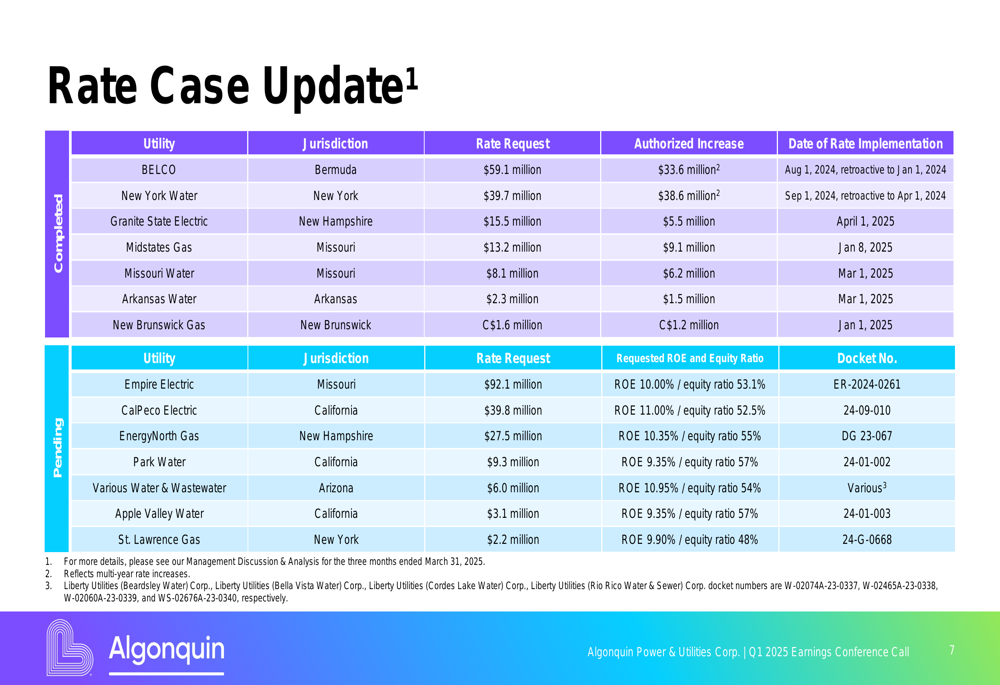

A key driver of Algonquin’s improved financial performance has been its success in securing rate increases across multiple jurisdictions. The company completed seven rate cases during the period, securing authorized increases totaling over $115 million across its electric, gas, and water utilities.

The following table provides a comprehensive overview of both completed and pending rate cases:

Notably, the company has several significant rate cases pending, including a $92.1 million request for Empire Electric in Missouri and a $39.8 million request for CalPeco Electric in California, which could provide additional revenue tailwinds if approved.

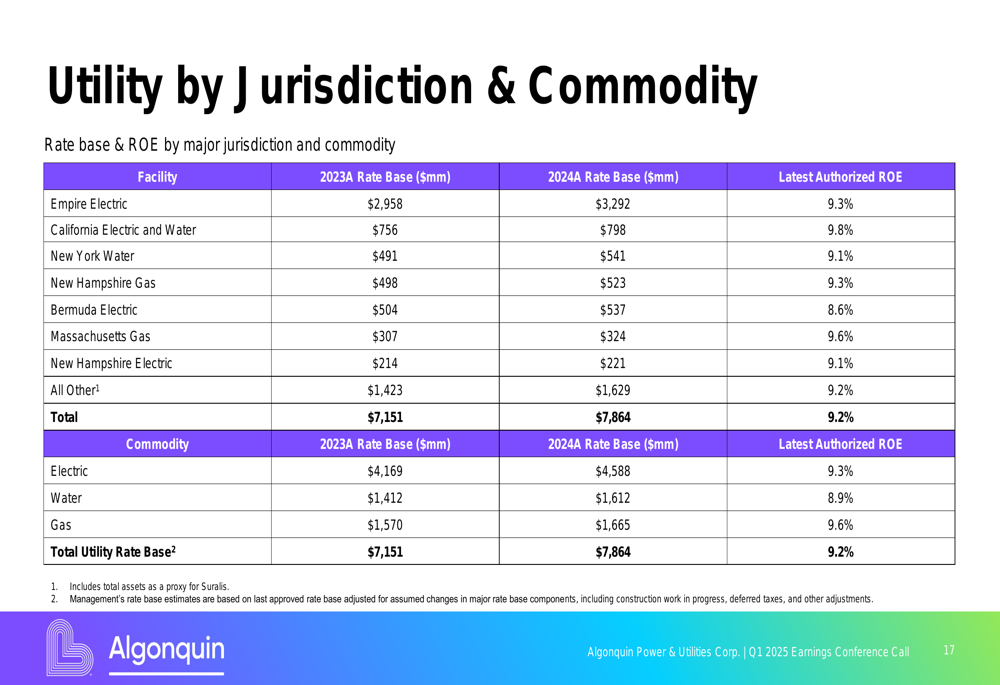

Algonquin’s regulated utility operations span across the United States, Canada, Chile, and Bermuda, serving over 1 million customer connections. The company’s rate base grew from $7,151 million in 2023 to $7,864 million in 2024, representing approximately 10% growth.

The following breakdown shows Algonquin’s utility rate base by jurisdiction and commodity:

Forward-Looking Statements

Algonquin announced plans to provide a more detailed investor update on June 3, 2025, where it is expected to outline adjusted net EPS ranges for 2025-2027. Analysts tracked by Investing.com forecast EPS of $0.31 for FY2025, with price targets ranging from $4.75 to $6.25.

The company is also evaluating a potential divestiture of its hydro portfolio, which could further refine its strategic focus on regulated utility operations. This follows the earlier sale of its renewable energy business, which has allowed the company to deleverage its balance sheet and improve its credit metrics.

While specific forward guidance wasn’t provided in the presentation, the company indicated it remains "on track to deliver 90-day outlook update," suggesting more concrete financial targets will be forthcoming in the June investor call.

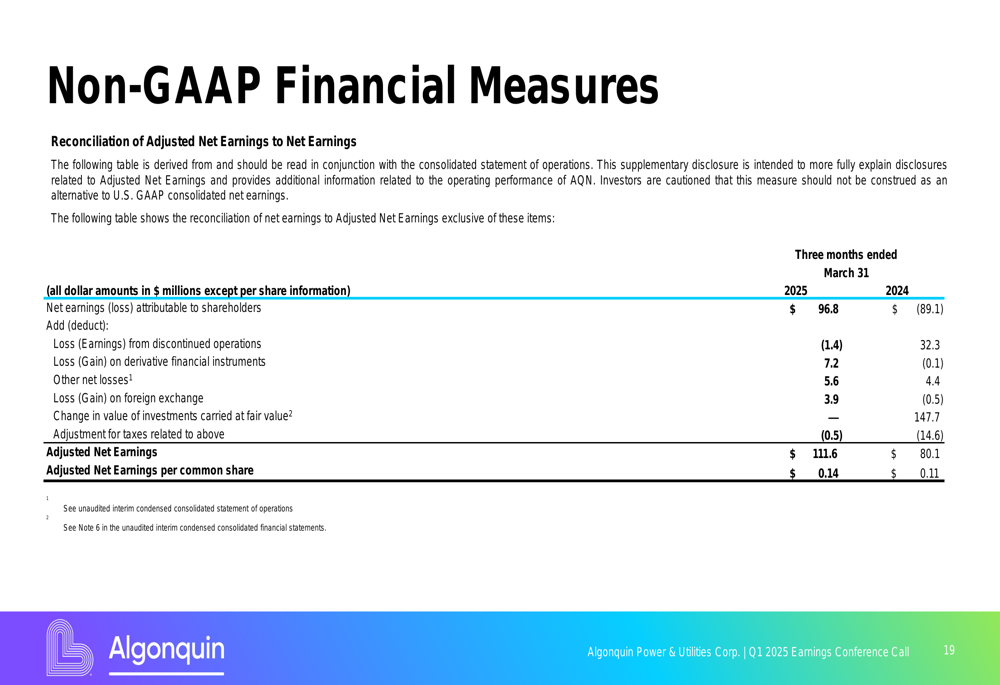

For reconciliation purposes, the company provided a detailed breakdown of its non-GAAP financial measures:

Investors will be watching closely to see if Algonquin can maintain its earnings momentum and successfully execute its strategy of becoming a premium regulated utility operator in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.