Softbank Group Q2 profit blows past expectations; sells Nvidia stake for $5.8 bln

Introduction & Market Context

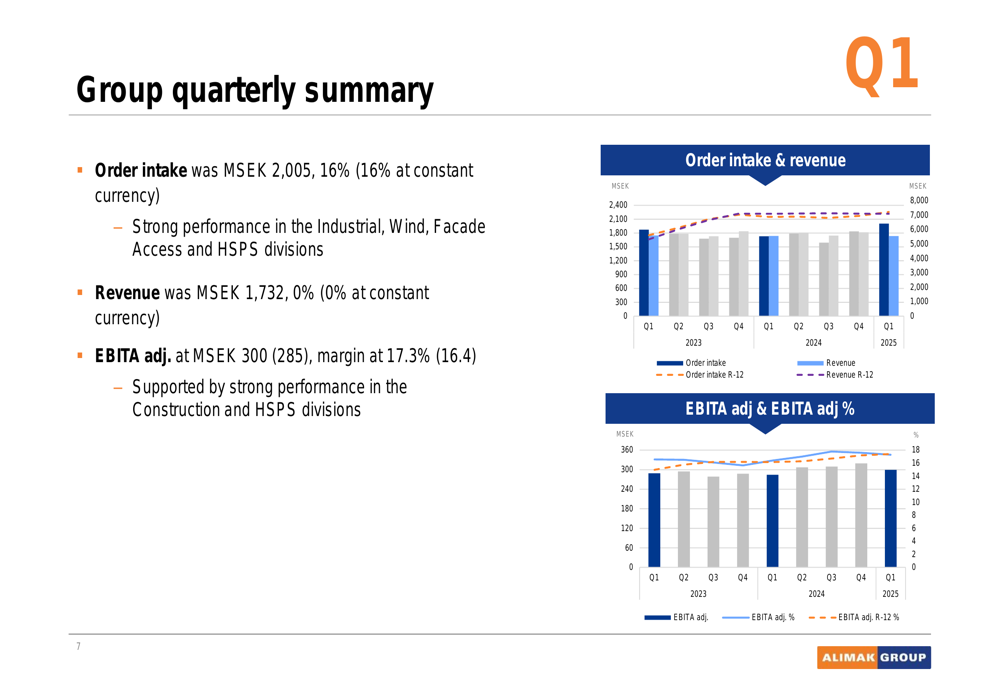

Alimak Group (STO:ALIG) presented its Q1 2025 financial results on April 24, showcasing strong order intake growth despite flat revenue performance. The global vertical access solutions provider reported a 16% increase in order intake to over BSEK 2, while adjusted EBITA margin improved to 17.3% from 16.4% in the same period last year.

The company’s stock declined 3.82% to SEK 115.8 following the presentation, possibly reflecting investor concerns about flat revenue growth despite the strong order intake. The stock remains well above its 52-week low of SEK 91.2 but has retreated from its recent high of SEK 147.

Quarterly Performance Highlights

Alimak Group’s Q1 2025 results demonstrated continued progress toward its financial targets, with particular strength in order intake and profitability metrics. While revenue remained flat at MSEK 1,732 year-over-year, the company’s adjusted EBITA increased to MSEK 300 from MSEK 285, representing a margin improvement to 17.3% from 16.4%.

As shown in the following chart of the group’s quarterly performance:

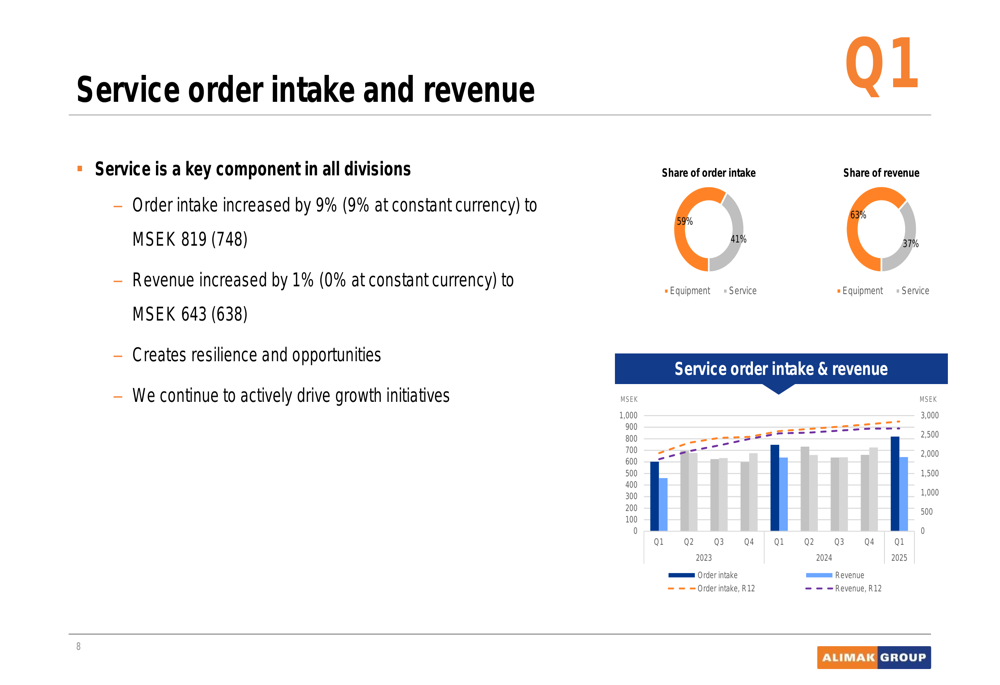

The company’s service business, a key component across all divisions, showed solid growth with order intake increasing 9% to MSEK 819. Service revenue grew marginally by 1% to MSEK 643, representing 41% of total revenue compared to 59% from equipment sales.

The following chart illustrates the service business performance:

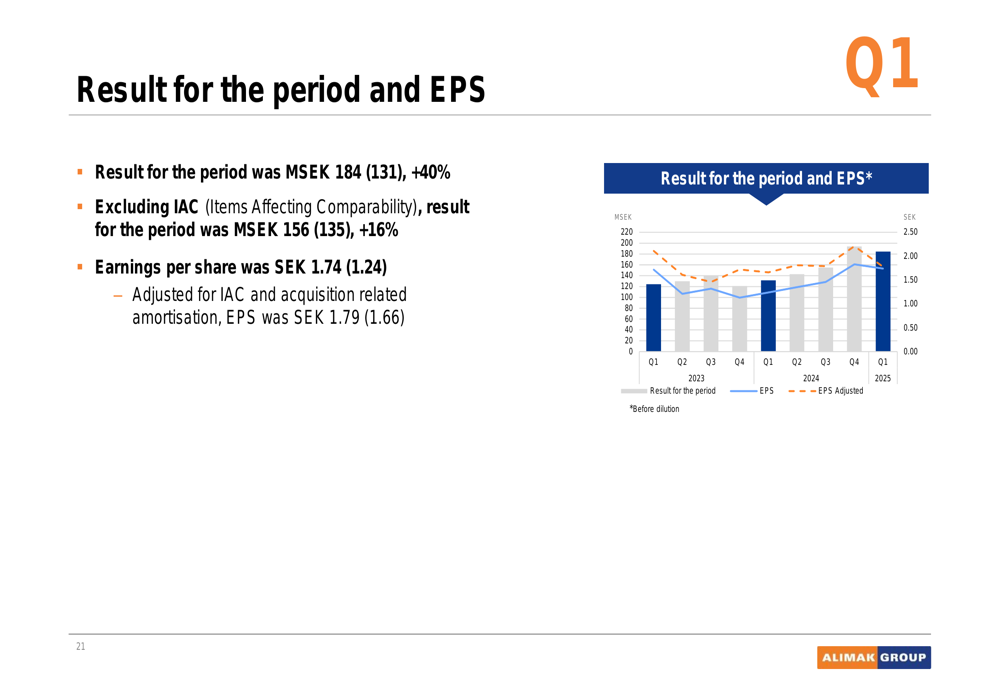

Net profit for the period increased significantly by 40% to MSEK 184, translating to earnings per share of SEK 1.74 compared to SEK 1.24 in Q1 2024. Excluding items affecting comparability, the result for the period increased by 16%.

This earnings growth is illustrated in the following chart:

Divisional Performance

All five of Alimak’s divisions reported order intake growth, though revenue and margin performance varied:

The Facade Access division posted a 17% increase in order intake to MSEK 496, driven by significant equipment orders in Hong Kong and Australia, along with refurbishment orders in Malaysia. Revenue declined slightly by 1% to MSEK 482, while EBITA margin remained stable at 9.5%.

The Construction division achieved modest order intake growth of 1% to MSEK 490, but delivered impressive revenue growth of 11% to MSEK 413. EBITA margin expanded significantly to 16.1% from 10.4%, driven by higher volumes and improved factory utilization.

Height Safety & Productivity Solutions (HSPS) reported 14% order intake growth to MSEK 382, despite a 1% revenue decline to MSEK 349. EBITA margin improved to 20.0% from 17.4%, supported by higher gross margins and effective cost control.

The Industrial division showed the strongest order intake growth at 32% to MSEK 432, with particularly strong performance in North America and the Middle East. However, revenue declined 11% to MSEK 354 due to timing of equipment deliveries. EBITA margin slightly decreased to 25.3% from 26.6%.

The Wind division delivered 24% order intake growth to MSEK 217, driven by strong equipment orders in APAC. Revenue remained flat at MSEK 153, while EBITA margin declined slightly to 18.2% from 19.8%.

Financial Position and Outlook

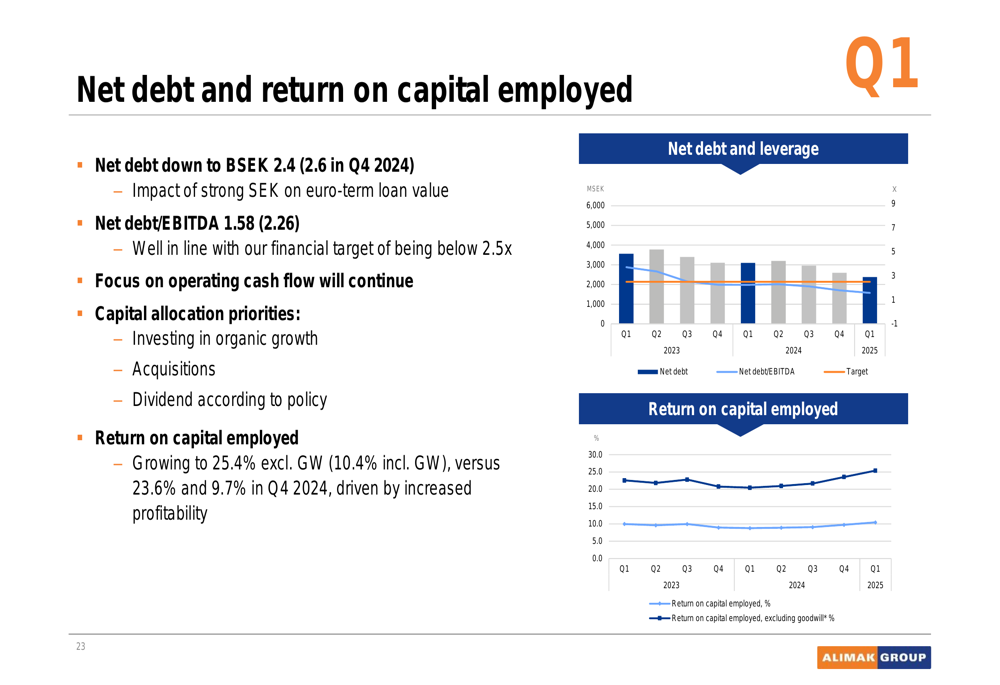

Alimak Group maintained a solid financial position in Q1 2025, with continued deleveraging and strong cash generation. Net debt decreased to BSEK 2.4 from BSEK 2.6 in Q4 2024, partly due to the strengthening of the Swedish krona against the euro. The net debt to EBITDA ratio improved to 1.58 from 2.26 a year earlier.

The following chart illustrates the company’s net debt and leverage trend:

Operating cash flow remained solid at MSEK 175, though lower than the MSEK 214 reported in Q1 2024. The company noted an increase in inventory to ensure future deliveries in response to the strong order intake.

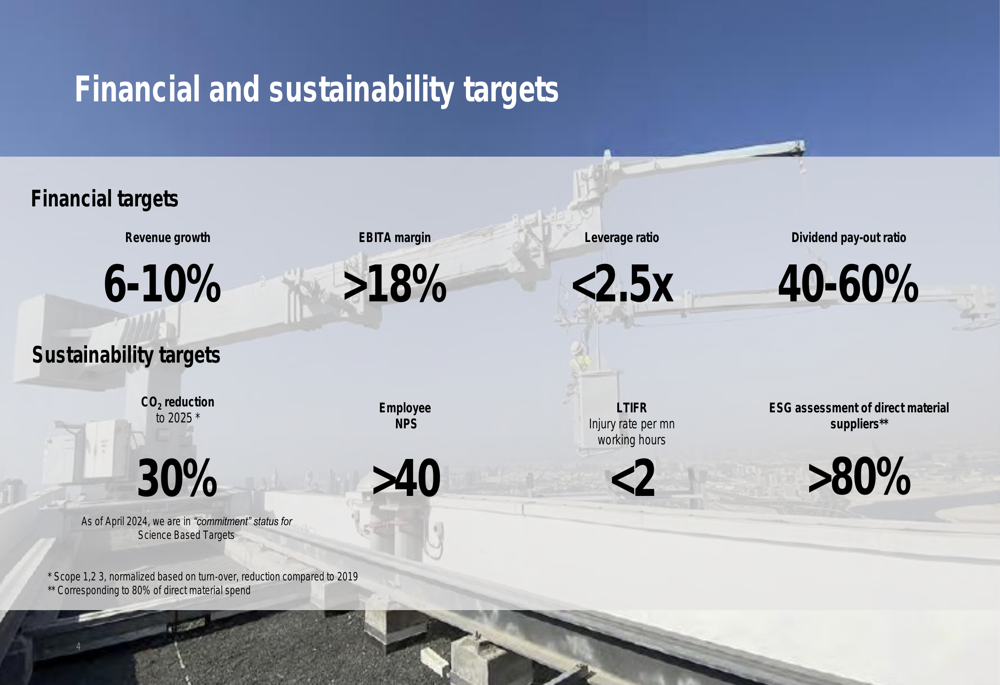

Alimak Group reaffirmed its financial and sustainability targets as part of its New Heights 2.0 program, which aims to deliver accelerated profitable growth. The company targets 6-10% revenue growth, an EBITA margin above 18%, and a leverage ratio below 2.5x.

These targets are illustrated in the following slide:

The company addressed concerns about US tariffs, noting that it has implemented short-term mitigation efforts including price management and supply chain optimization. Management expressed confidence that the tariffs would not significantly impact competitiveness in any of its divisions, though it acknowledged increased market uncertainty.

Strategic Initiatives

During the quarter, Alimak Group acquired key assets from Spanish company Camac Minor Hoists, including intangible assets that complement its light construction products portfolio. This acquisition aligns with the company’s strategy to expand its product offerings and strengthen its market position.

The company continues to execute its New Heights 2.0 program, which is currently in its third phase focused on profitable growth (2022-2025). Management indicated that market analysis will be conducted in 2024, with division strategies to be updated in 2025 to prepare for accelerated profitable growth in 2026-2030.

The Facade Access division launched Infrastructure Access Solutions to establish clear positioning for infrastructure projects, while the Construction division expanded its portfolio with the Vectio 350 transport platform range designed for building projects between 30 and 40 meters. The HSPS division reported success with temporary access solutions in North America and confirmed potential in the underground utility sector with its Tracrod product.

In summary, Alimak Group’s Q1 2025 presentation demonstrated continued progress toward its financial targets, with strong order intake growth and margin improvement across most divisions. While revenue remained flat, the growing order backlog suggests potential for revenue growth in coming quarters. The company maintains a solid financial position and continues to execute strategic initiatives to drive long-term profitable growth, despite some market uncertainties including US tariffs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.