Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

Alimak Group (STO:ALIG), a global provider of vertical access solutions, presented its Q2 2025 results on July 18, showcasing continued margin improvement despite mixed divisional performance. The company’s shares have recently shown strength, trading at SEK 158, up 1.15% and near its 52-week high of SEK 158.8, suggesting investor confidence in the company’s strategic direction.

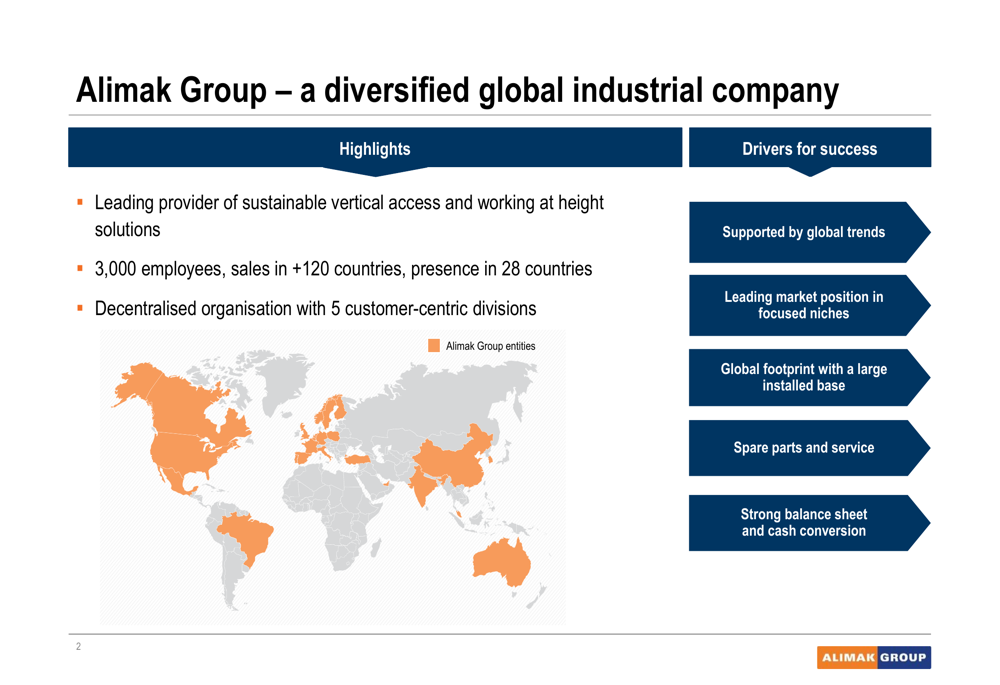

The presentation highlighted Alimak’s position as a diversified industrial company with 3,000 employees, sales in over 120 countries, and presence in 28 countries through a decentralized organization with five customer-centric divisions.

As shown in the following overview slide, Alimak Group’s global footprint and market positioning are key strengths:

Quarterly Performance Highlights

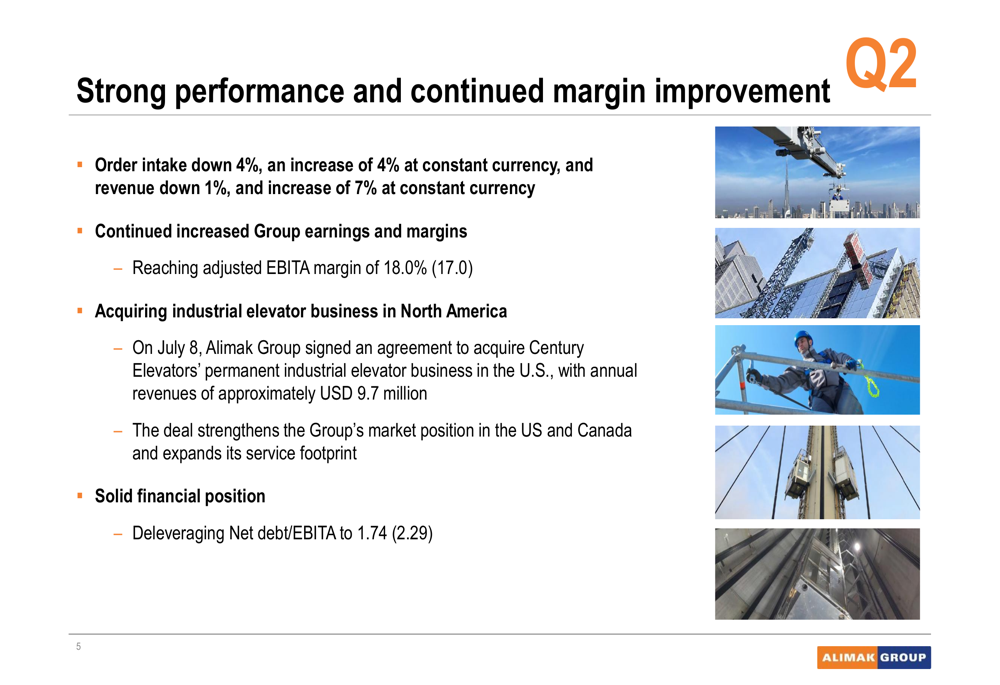

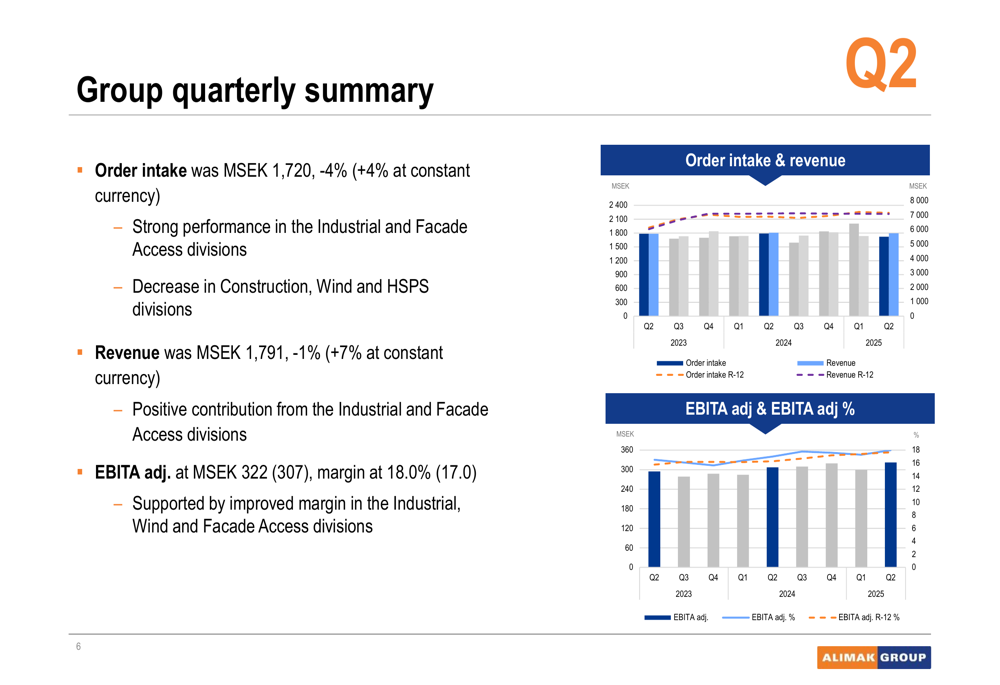

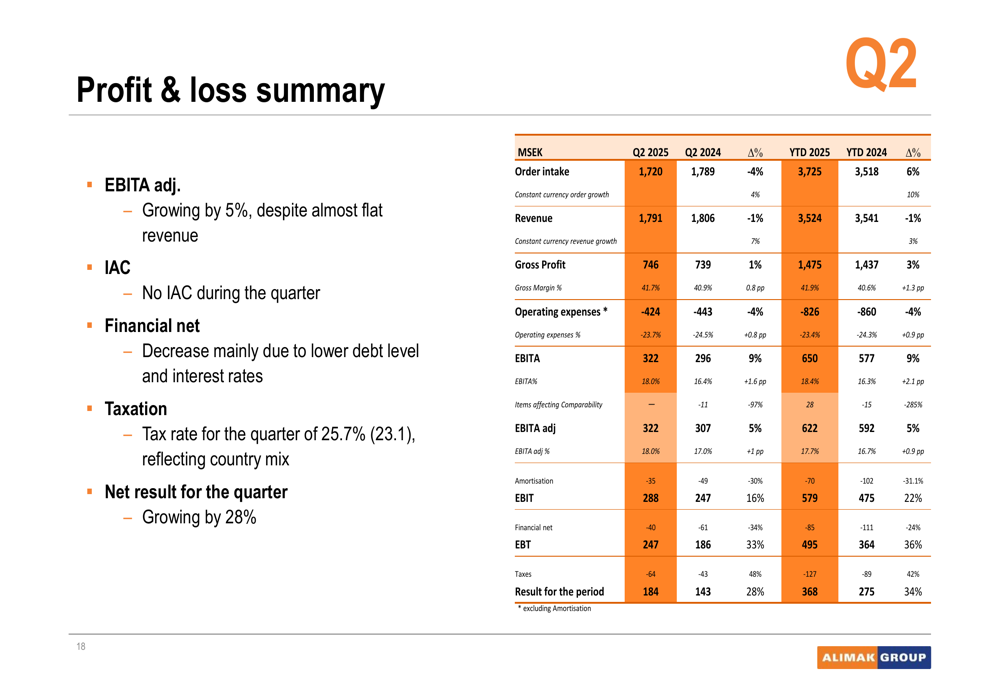

Alimak reported Q2 2025 results showing order intake down 4% (but up 4% at constant currency) and revenue down 1% (up 7% at constant currency) compared to Q2 2024. The company achieved an adjusted EBITA margin of 18.0%, an improvement from 17.0% in the same period last year, meeting its strategic target of >18%.

The following slide summarizes the key performance metrics for the quarter:

Financially, Alimak reported earnings per share of SEK 1.74, representing a 28% increase year-over-year, though this narrowly missed analyst forecasts of SEK 1.76 based on previous earnings reports. The company’s net debt/EBITA ratio improved to 1.74 from 2.29, well within its target of <2.5x.

The quarterly performance is clearly illustrated in the following chart showing order intake, revenue, and EBITA trends:

Service business, a key component across all divisions, showed resilience with revenue increasing by 5% (12% at constant currency) to MSEK 694, despite order intake decreasing by 10%. Services represented approximately 38% of both order intake and revenue, providing stability to the overall business.

Divisional Performance

Performance varied significantly across Alimak’s five divisions:

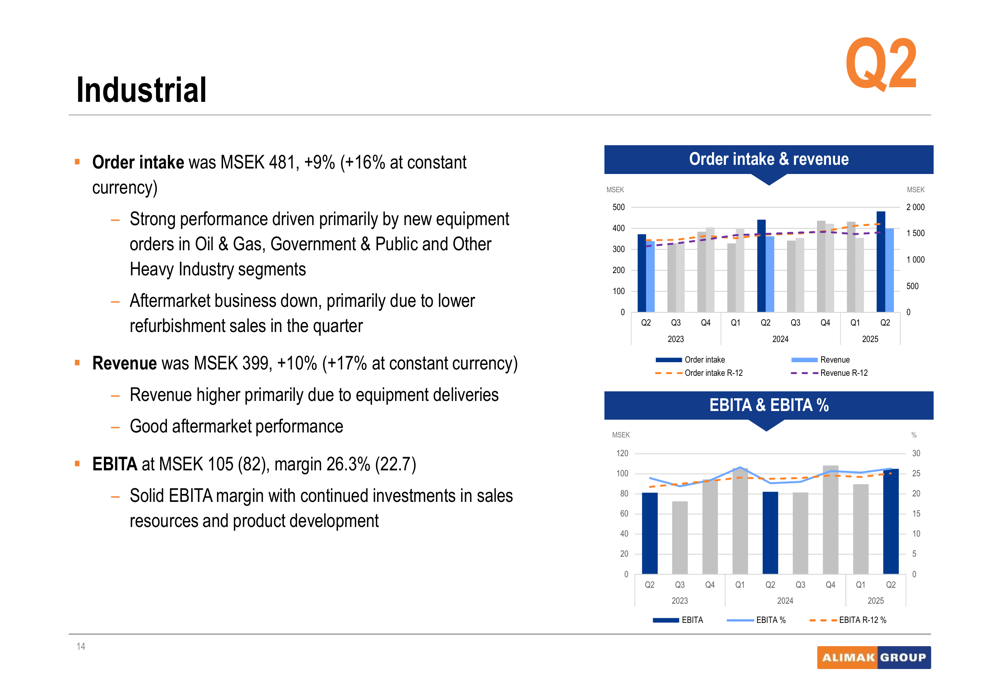

The Industrial division was a standout performer with order intake up 9% (16% at constant currency), revenue up 10% (17% at constant currency), and an impressive EBITA margin of 26.3% (up from 22.7%). Strong performance was driven by new equipment orders in Oil & Gas, Government & Public, and Other Heavy Industry segments.

The Facade Access division also performed well with order intake up 24% (35% at constant currency) and revenue up 1% (9% at constant currency). EBITA margin improved to 11.2% from 10.0%, though the division faces challenges with low factory load and margin losses on legacy projects.

In contrast, the Construction division experienced a 28% decline in order intake (-21% at constant currency) due to demand volatility, with revenue down 4% (but up 3% at constant currency). Despite these challenges, the division maintained its EBITA margin at 16.7% (up slightly from 16.6%).

The Height Safety & Productivity Solutions (HSPS) division saw order intake decrease by 10% (-4% at constant currency) and revenue decline by 9% (-3% at constant currency), attributed to a slow construction sector in Central and Southern Europe. EBITA margin decreased to 17.2% from 19.5%.

Similarly, the Wind division reported a 22% decrease in order intake (-15% at constant currency), affected by tariff uncertainties in the US and high year-over-year comparables in China. Revenue decreased by 8% (-2% at constant currency), though EBITA margin improved to 21.4% from 19.8%.

Strategic Initiatives

Alimak announced two significant strategic initiatives during the presentation:

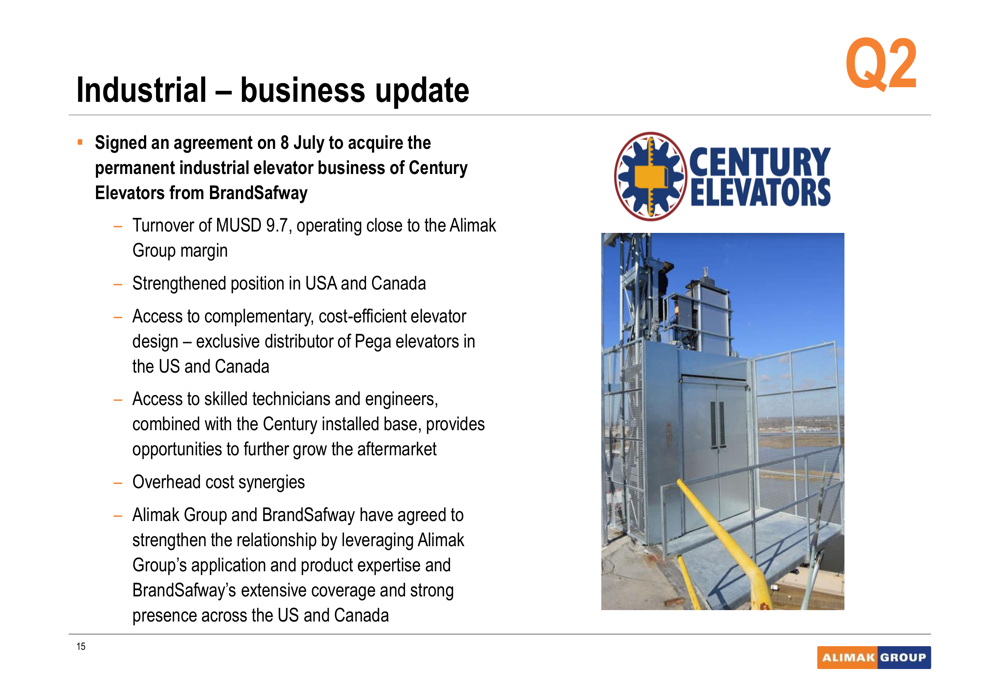

First, the company signed an agreement on July 8 to acquire Century Elevators’ permanent industrial elevator business in the U.S., with annual revenues of approximately USD 9.7 million. This acquisition strengthens Alimak’s position in North America and provides access to complementary elevator design and skilled technicians.

The following slide details the strategic rationale behind the Century Elevators acquisition:

Second, Alimak announced a restructuring plan for its Facade Access division, including organizational changes and capacity reduction in Spain. The estimated total restructuring cost is MSEK 60, with expected annual savings of MSEK 30 starting in 2026.

The company also continues to execute its "New Heights 2.0" program, focused on accelerating profitable growth through market analysis and updated division strategies. A Capital Markets Day is scheduled for November 25, 2025, where the company will share more about its strategic priorities.

Financial Position and Outlook

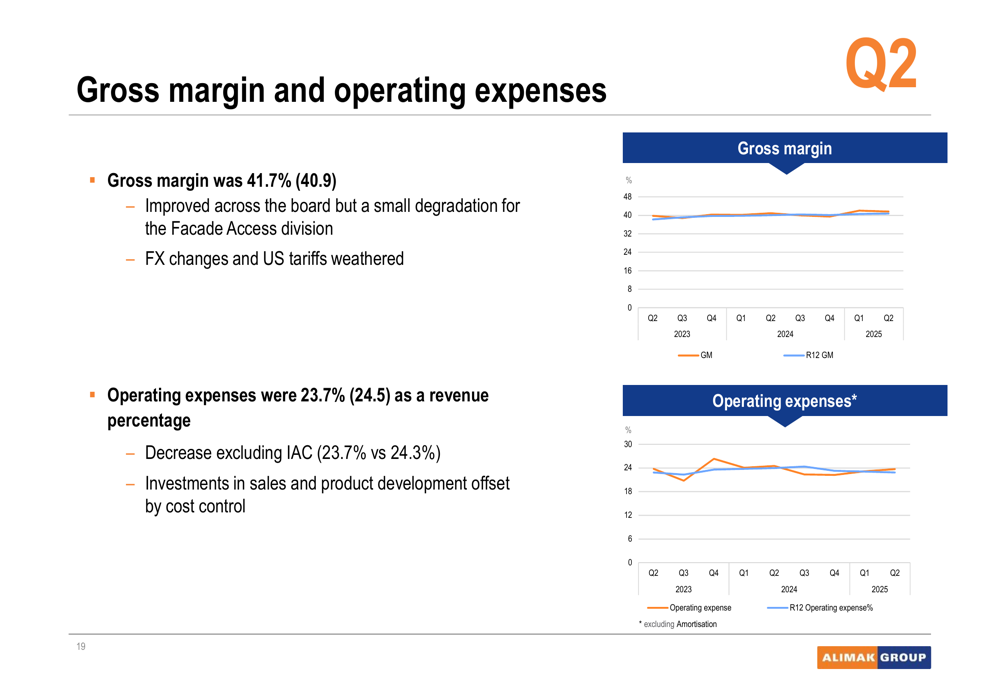

Alimak’s financial position remains solid, with improving profitability metrics across most divisions. Gross margin improved to 41.7% from 40.9%, while operating expenses decreased to 23.7% of revenue from 24.5%.

The comprehensive profit and loss summary shows strong year-over-year improvement in most key metrics:

The company’s gross margin and operating expense trends demonstrate consistent improvement over recent quarters:

Cash flow from operations increased to MSEK 182 from MSEK 164, reflecting continued focus on cash management despite working capital increases due to contract phasing in the Facade Access division.

Alimak reaffirmed its financial targets of 6-10% revenue growth and an EBITA margin above 18%, along with sustainability targets including 30% CO2 reduction by 2025:

Looking ahead, Alimak appears well-positioned to navigate market uncertainties with its diversified business model and strong balance sheet. The company’s focus on margin improvement and strategic acquisitions suggests a continued emphasis on profitable growth rather than pure volume expansion.

While some divisions face challenges, particularly Construction and HSPS due to construction market softness, the strong performance in Industrial and improving margins in Facade Access and Wind provide balance. The service business continues to offer resilience and growth opportunities across all divisions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.