Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Allison Transmission (NYSE:ALSN) presented its Q2 2025 earnings results on August 4, 2025, revealing a quarter of mixed performance with flat revenue but improved profitability. The company’s stock rose 1.19% in aftermarket trading to $88.73, building on a modest 0.35% gain during regular trading hours.

The transmission manufacturer announced a significant $2.7 billion acquisition of Dana’s Off-Highway business while simultaneously revising its full-year guidance to reflect current market conditions and acquisition-related expenses. The quarter showed divergent performance across market segments, with defense sales surging while North American on-highway and global off-highway segments declined.

Quarterly Performance Highlights

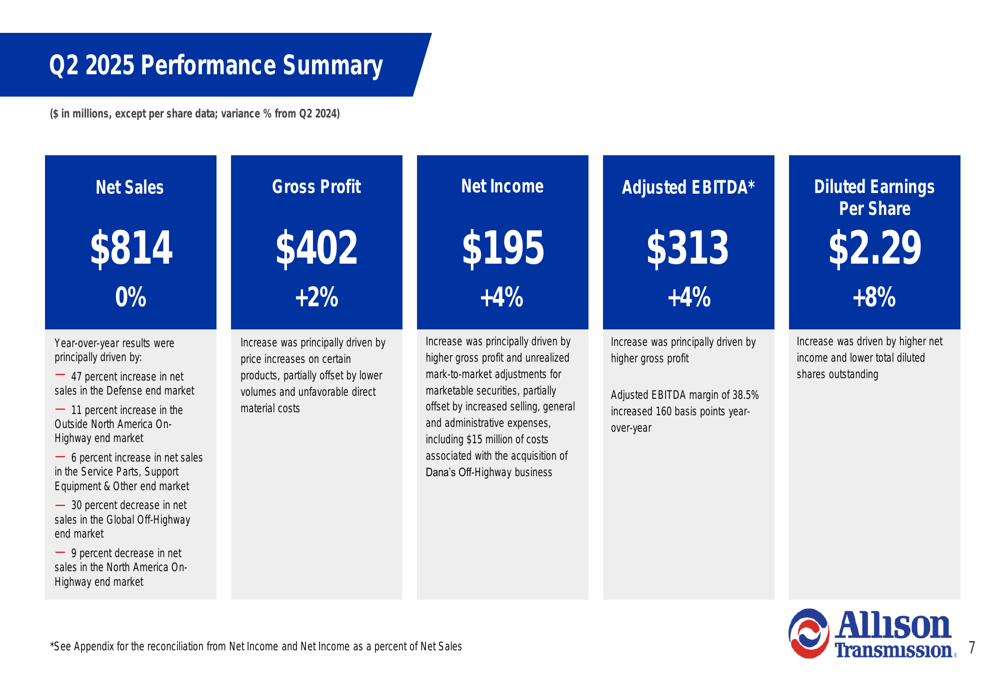

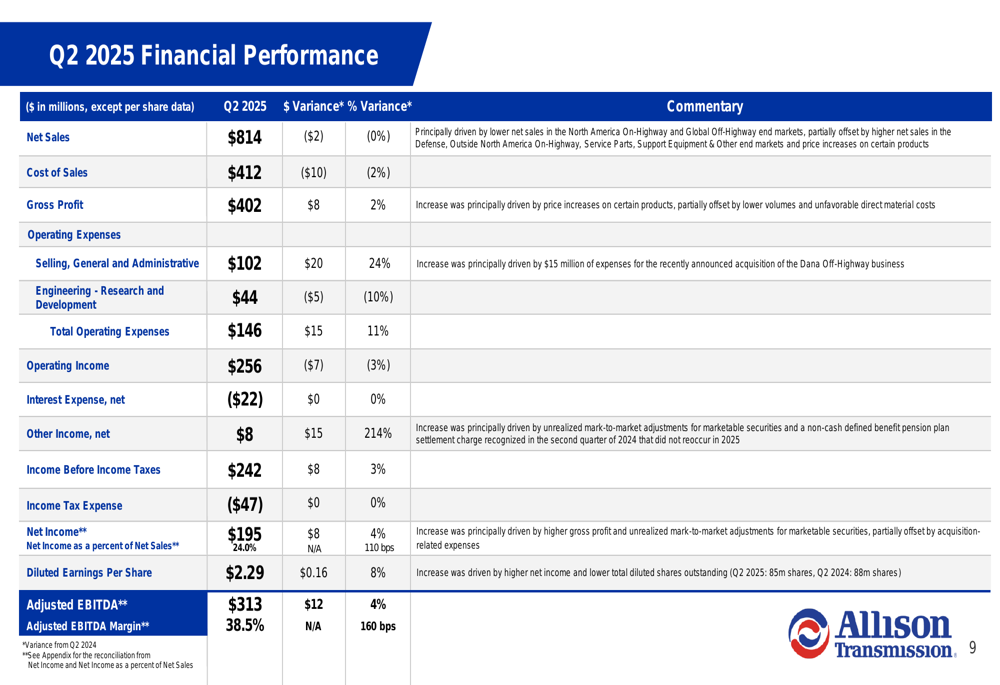

Allison Transmission reported Q2 2025 net sales of $814 million, essentially flat compared to the same period last year. Despite the stagnant revenue, the company achieved notable improvements in profitability metrics. Gross profit increased 2% to $402 million, while net income rose 4% to $195 million.

As shown in the following performance summary:

Diluted earnings per share reached $2.29, an 8% year-over-year improvement, continuing the positive trend from Q1 when the company reported EPS of $2.23. Adjusted EBITDA grew 4% to $313 million, with the adjusted EBITDA margin expanding by 160 basis points to 38.5%.

The company’s detailed financial performance shows effective cost management despite revenue challenges:

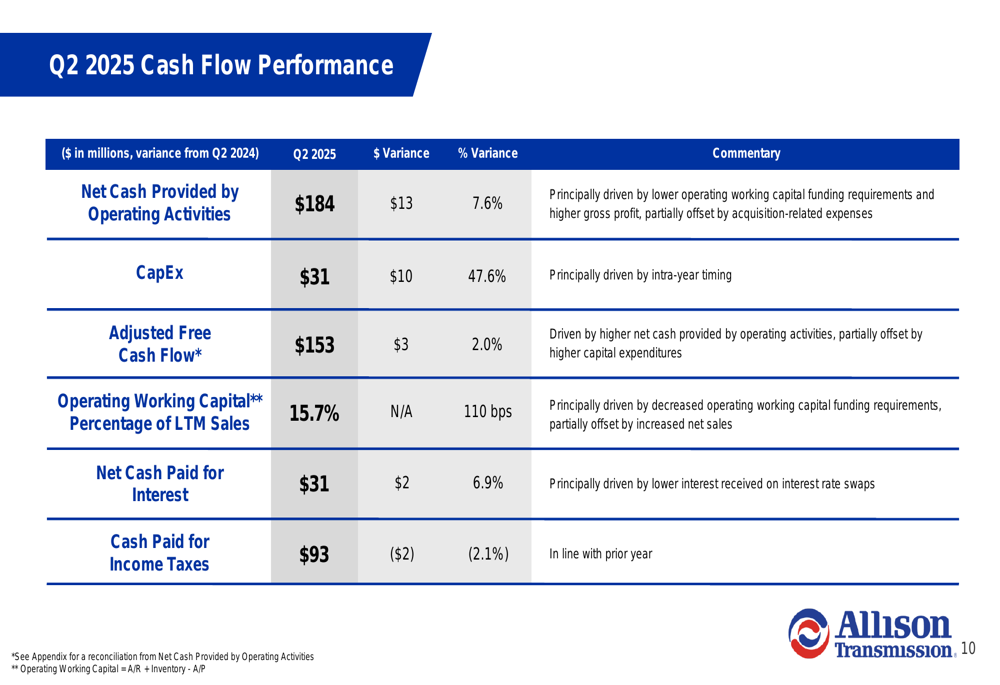

Allison’s cash flow performance remained solid, with net cash provided by operating activities increasing 7.6% to $184 million and adjusted free cash flow growing 2.0% to $153 million:

Dana Off-Highway Acquisition Details

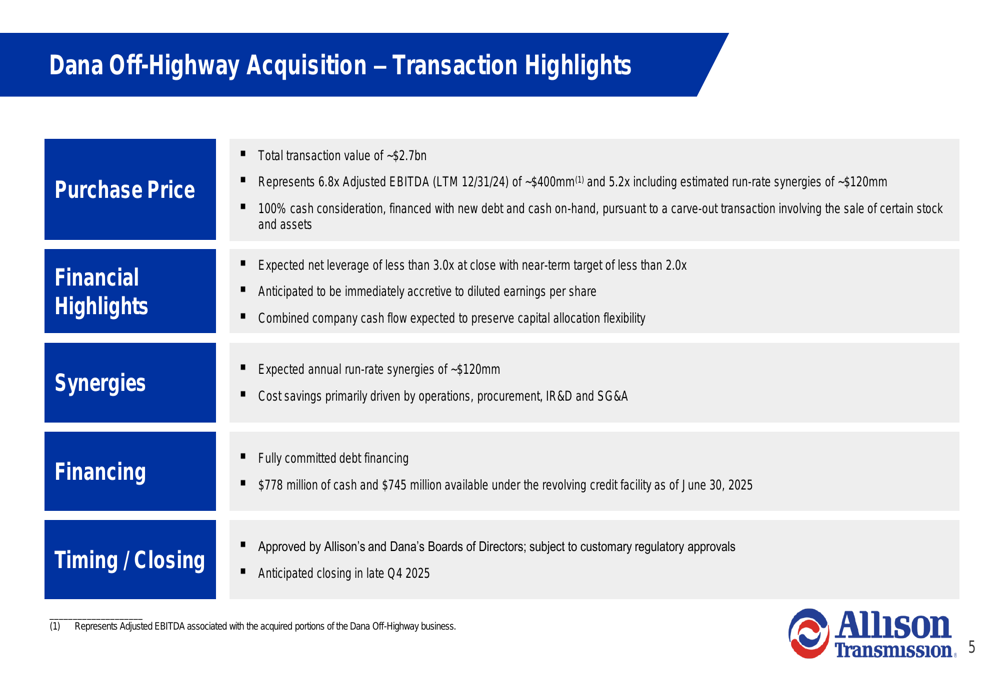

The most significant announcement was Allison’s planned acquisition of Dana’s Off-Highway business for approximately $2.7 billion in an all-cash transaction. The deal represents 6.8x the target’s adjusted EBITDA or 5.2x when including estimated run-rate synergies of approximately $120 million.

The transaction details reveal Allison’s strategic approach to financing and integration:

The acquisition has been approved by both companies’ boards of directors and is expected to close in late Q4 2025. Allison expects the deal to be immediately accretive to diluted earnings per share while maintaining financial flexibility with projected net leverage of less than 3.0x at closing.

Management highlighted the strategic benefits of the acquisition, positioning it as a catalyst for global growth:

Segment Performance Analysis

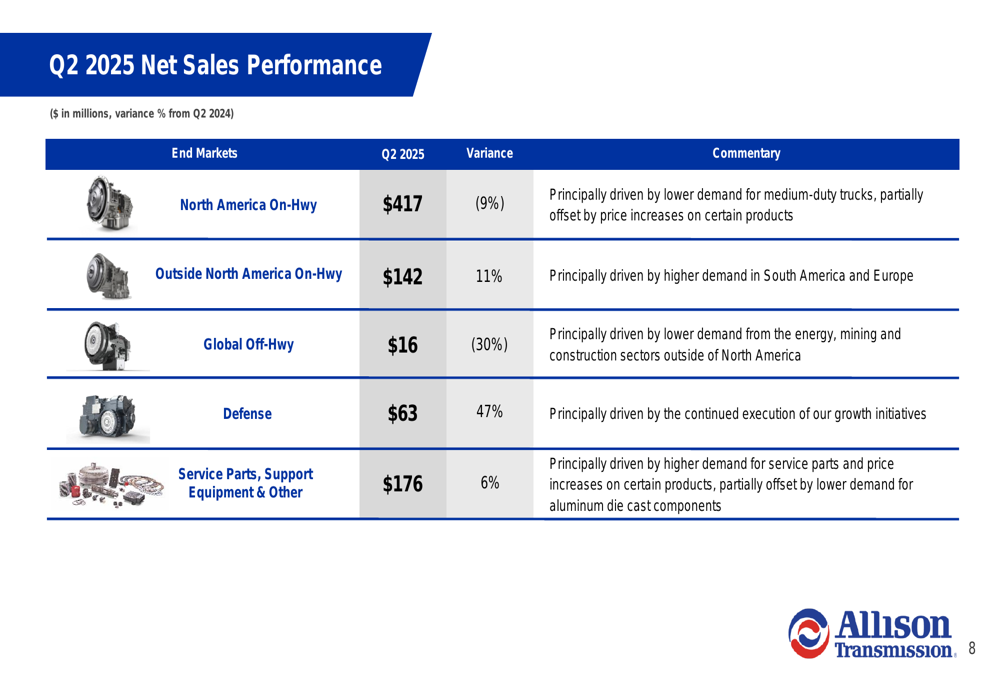

Allison’s end markets showed highly divergent performance in Q2 2025. The defense segment led growth with a 47% increase, while the Outside North America On-Highway segment grew 11%, and Service Parts increased 6%. However, these gains were offset by a 30% decrease in Global Off-Highway and a 9% decline in North America On-Highway.

The following breakdown illustrates the contrasting segment performance:

The North American On-Highway segment, despite its decline, remained the largest contributor to revenue at $417 million. The strong performance in defense sales ($63 million) represents a significant bright spot, likely driven by increased global defense spending amid ongoing geopolitical tensions.

Updated 2025 Guidance

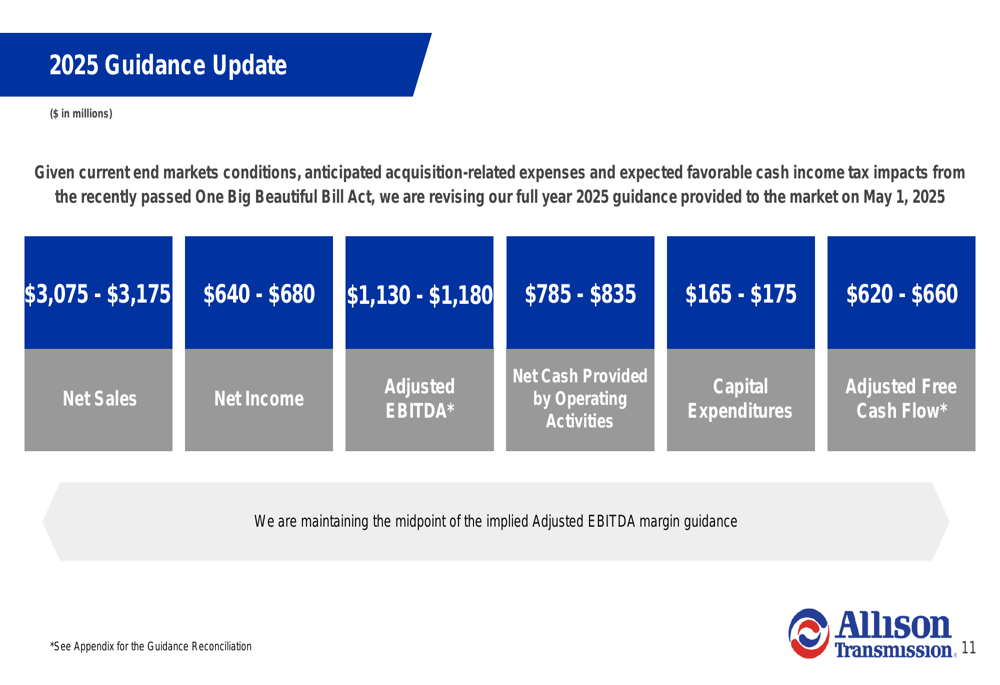

Allison revised its full-year 2025 guidance, citing current end market conditions, acquisition-related expenses, and the impact of the "One Big Beautiful Bill Act." The updated outlook represents a downward adjustment from the guidance provided in Q1, which had projected net sales between $3.2-3.3 billion and net income of $735-785 million.

The revised guidance provides the following ranges:

The company now expects net sales of $3,075-$3,175 million and net income of $640-$680 million. Adjusted EBITDA is projected at $1,130-$1,180 million, with adjusted free cash flow of $620-$660 million. Despite the revisions, management noted they are maintaining the midpoint of the implied Adjusted EBITDA margin guidance, indicating continued focus on operational efficiency.

Forward-Looking Statements

Looking ahead, Allison Transmission faces both opportunities and challenges. The Dana Off-Highway acquisition represents a significant strategic move that could enhance the company’s global market position and create new growth avenues. The expected annual run-rate synergies of approximately $120 million should support profitability once the integration is complete.

However, the revised guidance suggests caution regarding near-term market conditions. The significant decline in Global Off-Highway (-30%) and North America On-Highway (-9%) segments indicates potential headwinds in key markets. The acquisition-related expenses will also impact short-term financial performance before synergies are realized.

Investors will likely focus on the company’s ability to successfully integrate the Dana Off-Highway business while navigating challenging market conditions in some segments. The continued strength in defense and service parts businesses provides some diversification benefits that could help offset weakness in other areas.

With the stock trading at $88.73 in aftermarket trading, well below its 52-week high of $122.53, Allison shares may present an opportunity for investors who believe in the long-term strategic benefits of the Dana acquisition and the company’s ability to maintain its strong profit margins despite revenue challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.