Oracle stock falls after report reveals thin margins in AI cloud business

Insurer reports 28.6% return on equity with significant combined ratio improvements across segments

Introduction & Market Context

Allstate Corporation (NYSE:ALL) presented its second quarter 2025 earnings results on July 31, showing substantial improvement in underwriting performance and profitability metrics. The company’s shares were trading down 0.38% in premarket at $191.55, following a previous close of $192.28.

The Q2 results demonstrate a significant improvement from the first quarter of 2025, when Allstate reported an adjusted EPS of $3.53 that fell short of analyst expectations. The company’s strategic focus on expanding its insurance offerings while improving operational efficiency appears to be yielding positive results.

Quarterly Performance Highlights

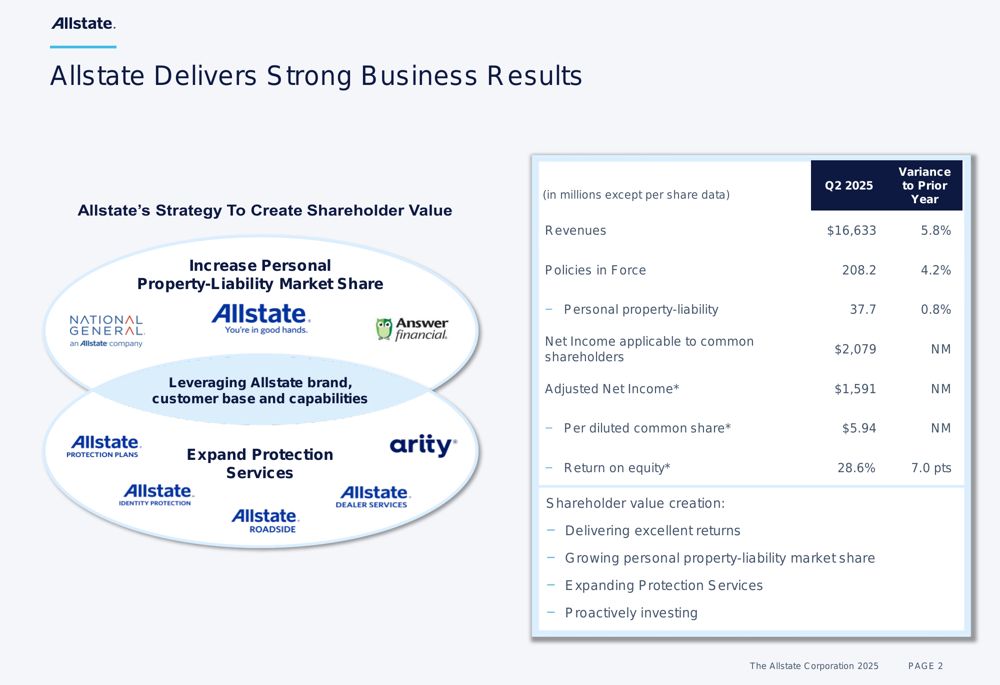

Allstate reported Q2 2025 revenues of $16,633 million, representing a 5.8% year-over-year increase. The company’s total policies in force reached 208.2 million, up 4.2% compared to the same period last year. Net income applicable to common shareholders was $2,079 million, while adjusted net income reached $1,591 million, translating to $5.94 per diluted common share.

As shown in the following comprehensive business results summary:

One of the most notable achievements was Allstate’s return on equity, which reached 28.6%, representing a 7.0 percentage point increase year-over-year. This metric significantly outperforms the 23.7% adjusted net income return on equity reported for the 12 months ending Q1 2025.

Property-Liability Segment Analysis

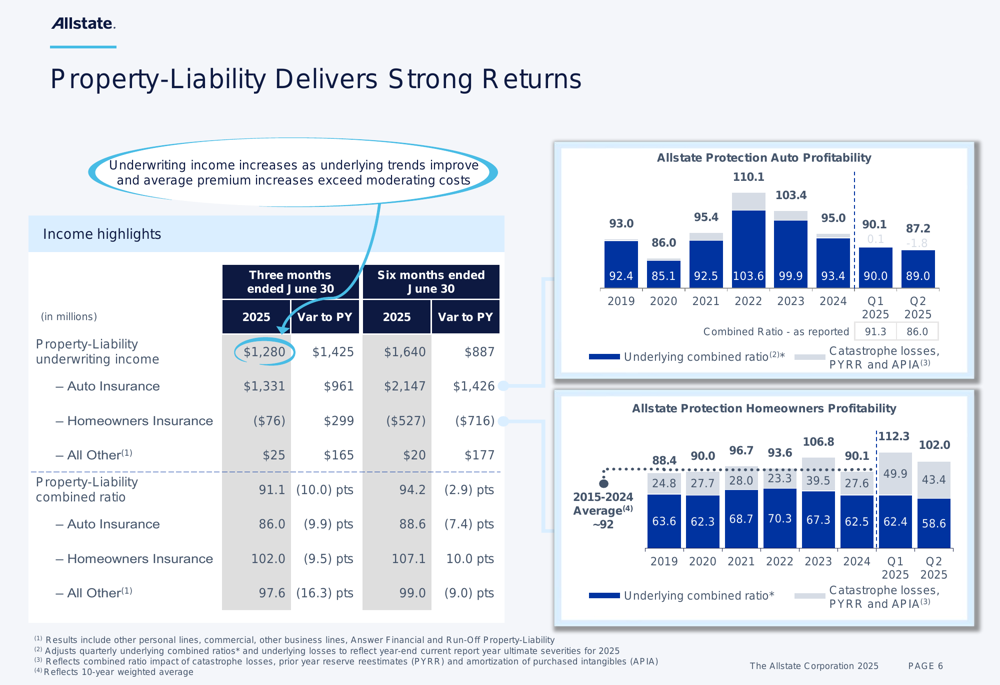

The Property-Liability segment delivered exceptional results, with a combined ratio of 91.1%, representing a 10.0 percentage point improvement. Auto insurance performance was particularly strong with an 86.0% combined ratio (9.9 percentage points better than prior year), while homeowners insurance showed improvement but remained slightly unprofitable with a 102.0% combined ratio.

The following chart illustrates the segment’s strong underwriting income and profitability trends:

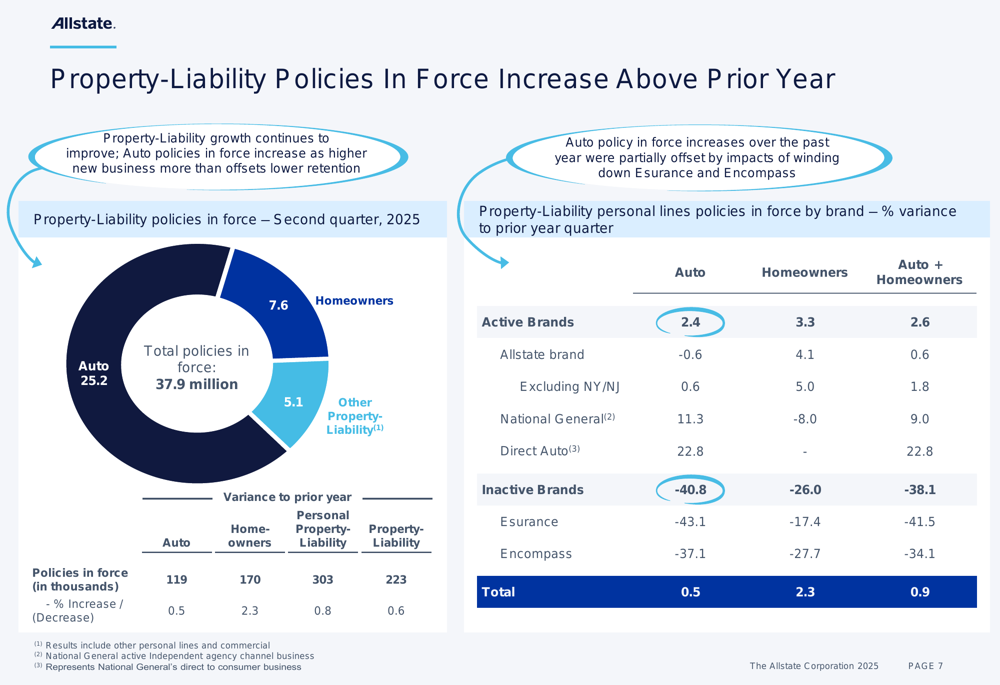

Allstate’s personal property-liability policies in force increased to 37.7 million, up 0.8% year-over-year. The company has successfully expanded its customer access through multiple distribution channels, resulting in significant growth in new issued applications.

The distribution of policies in force across different product lines shows the company’s balanced approach:

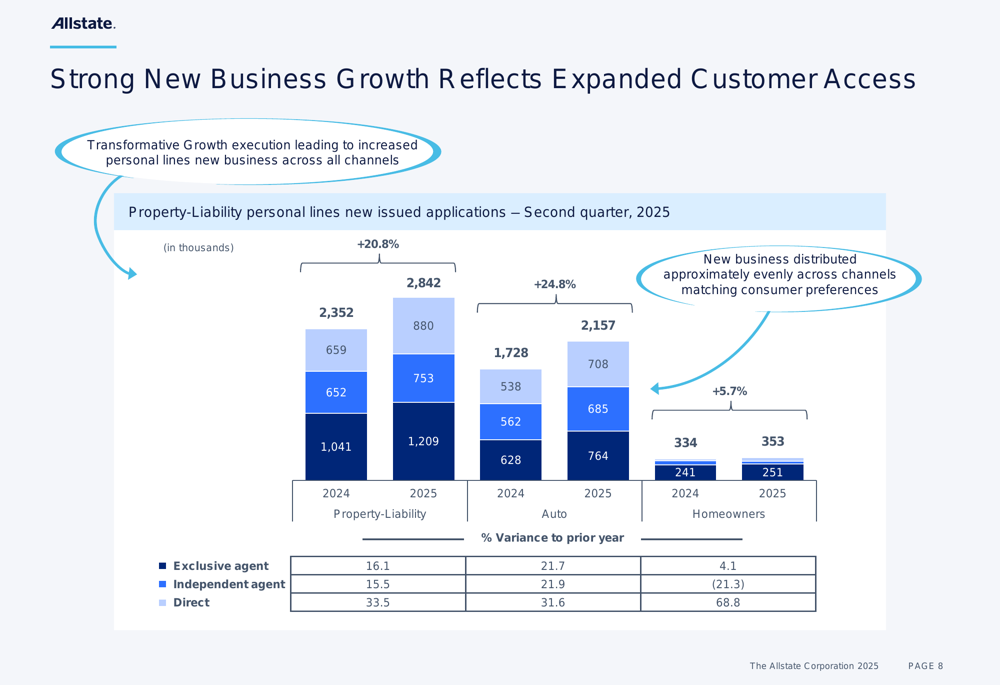

New business growth has been particularly strong, with personal lines new issued applications reaching 2,842 thousand in Q2 2025, compared to 2,352 thousand in Q2 2024. This growth spans across all distribution channels, including exclusive agents, independent agents, and direct channels.

The following chart demonstrates this expansion in customer access:

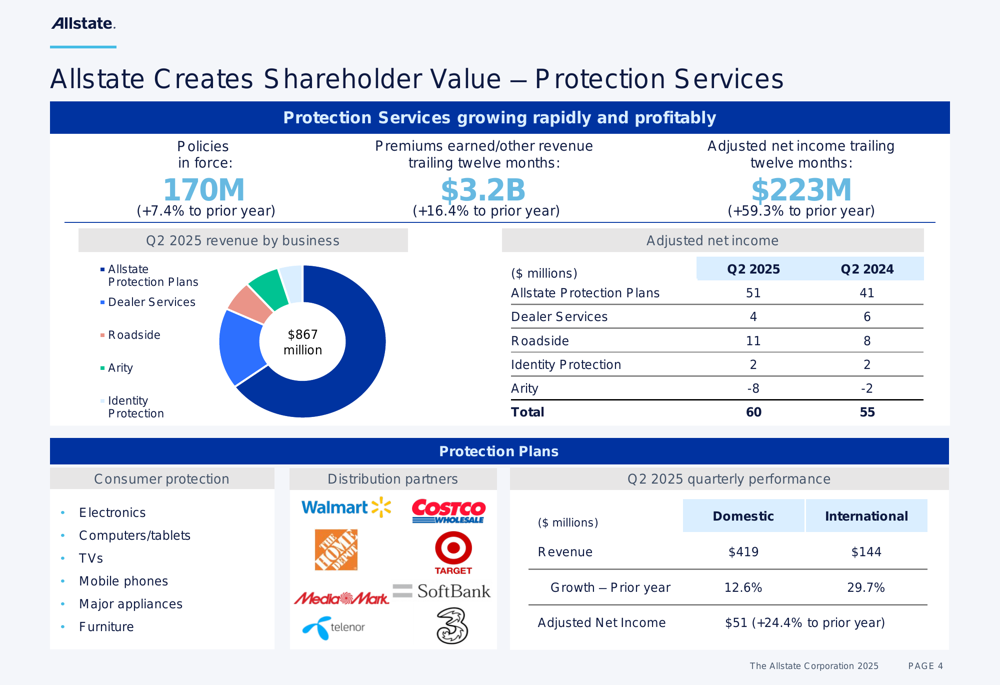

Protection Services Growth

Allstate’s Protection Services segment continues to be a significant growth driver for the company. Policies in force for this segment reached 170 million, representing a 7.4% increase year-over-year. Premiums earned and other revenue for the trailing twelve months totaled $3.2 billion, up 16.4%, while adjusted net income for the same period reached $223 million, a substantial 59.3% increase.

The segment’s performance breakdown by business unit and distribution partnerships is illustrated below:

Allstate Protection Plans, which includes partnerships with major retailers like Walmart (NYSE:WMT), Costco (NASDAQ:COST), and Home Depot (NYSE:HD), reported domestic revenue of $419 million and international revenue of $144 million, with growth rates of 12.6% and 29.7% respectively. This business unit delivered adjusted net income of $51 million, a 24.4% increase over the prior year.

Capital Management and Shareholder Returns

Allstate continues to demonstrate disciplined capital management. During the quarter, the company divested its Employer Voluntary Benefits and Group Health businesses for $3.25 billion, providing additional capital flexibility. The company returned significant value to shareholders through $1.1 billion in common and preferred dividends and $445 million in share repurchases.

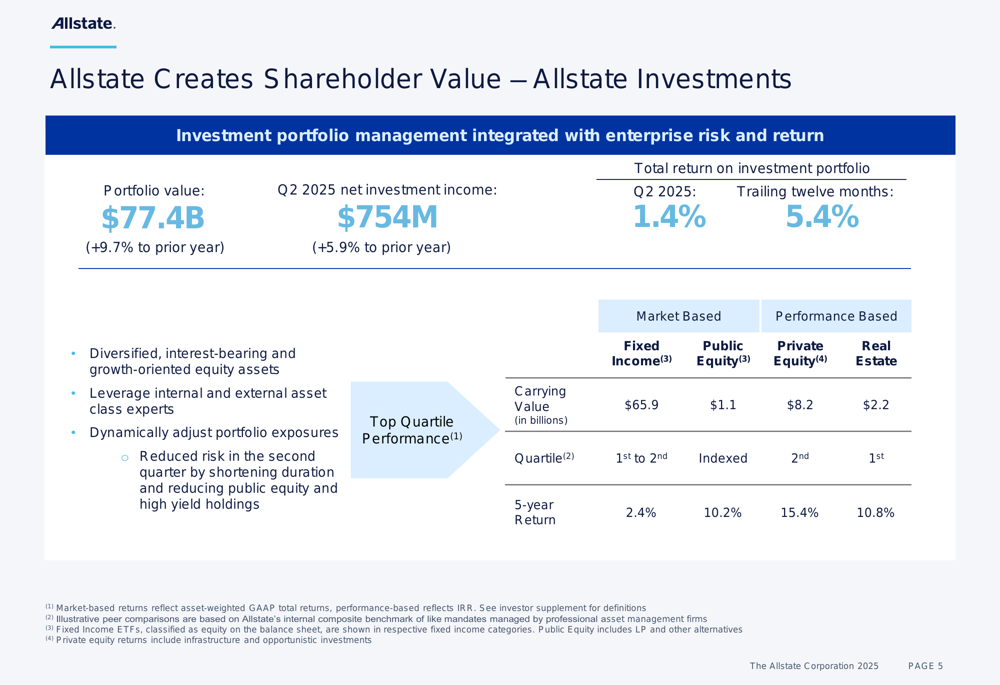

The company’s investment portfolio, valued at $77.4 billion (up 9.7% year-over-year), generated net investment income of $754 million in Q2 2025, a 5.9% increase from the prior year. The total return on the investment portfolio was 1.4% for the quarter and 5.4% for the trailing twelve months.

The investment portfolio’s composition and performance are detailed in the following slide:

Forward-Looking Statements

Looking ahead, Allstate’s strategy focuses on four key areas: delivering excellent returns, growing personal property-liability market share, expanding protection services, and proactive investments. The company aims to leverage its strong brand recognition and diverse distribution channels to continue expanding its customer base.

"Growth is the unlock to the valuation multiples," CEO Tom Wilson had stated during the Q1 2025 earnings call, emphasizing the company’s ability to maintain profitability while expanding. The Q2 results appear to validate this approach, with the company demonstrating both growth and improved profitability.

Allstate’s multi-faceted approach to shareholder value creation, combined with its strong financial results, positions the company well for continued success in the competitive insurance landscape. However, investors should monitor potential headwinds, including the impact of tariffs on auto insurance costs and ongoing retention challenges in certain market segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.