Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Ally Financial (NYSE:ALLY) reported a GAAP net loss in the first quarter of 2025, while maintaining positive adjusted earnings as the company executes a strategic repositioning toward its core businesses. The financial services provider is divesting its credit card business and implementing significant balance sheet adjustments to improve long-term profitability.

The company’s shares closed at $32.18 on April 16, 2025, and were trading slightly lower in pre-market activity following the earnings release, down 0.75% to $31.94.

Quarterly Performance Highlights

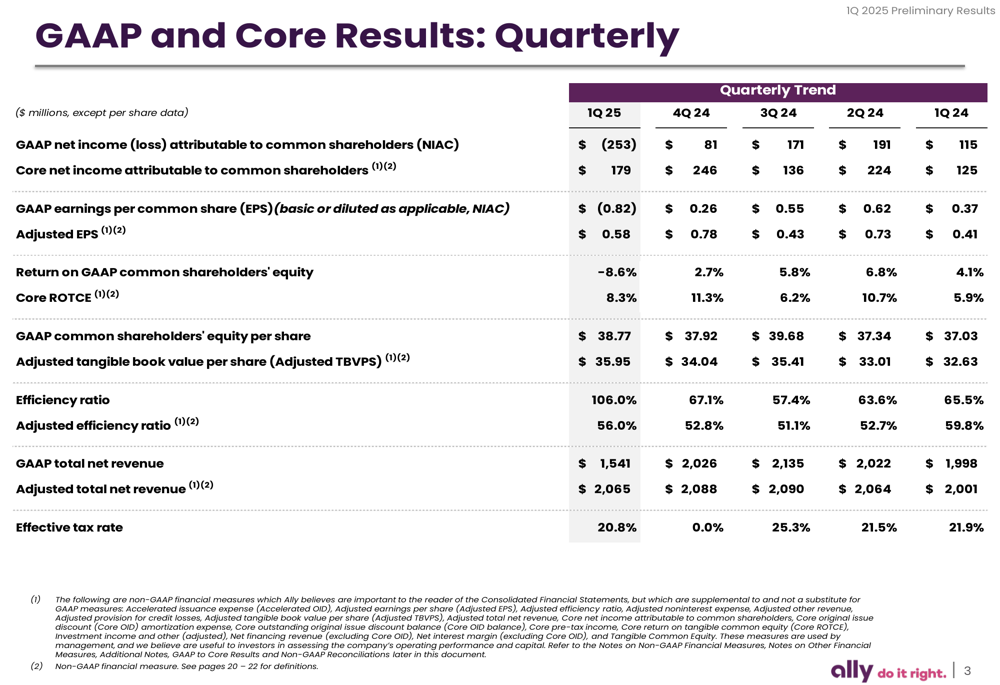

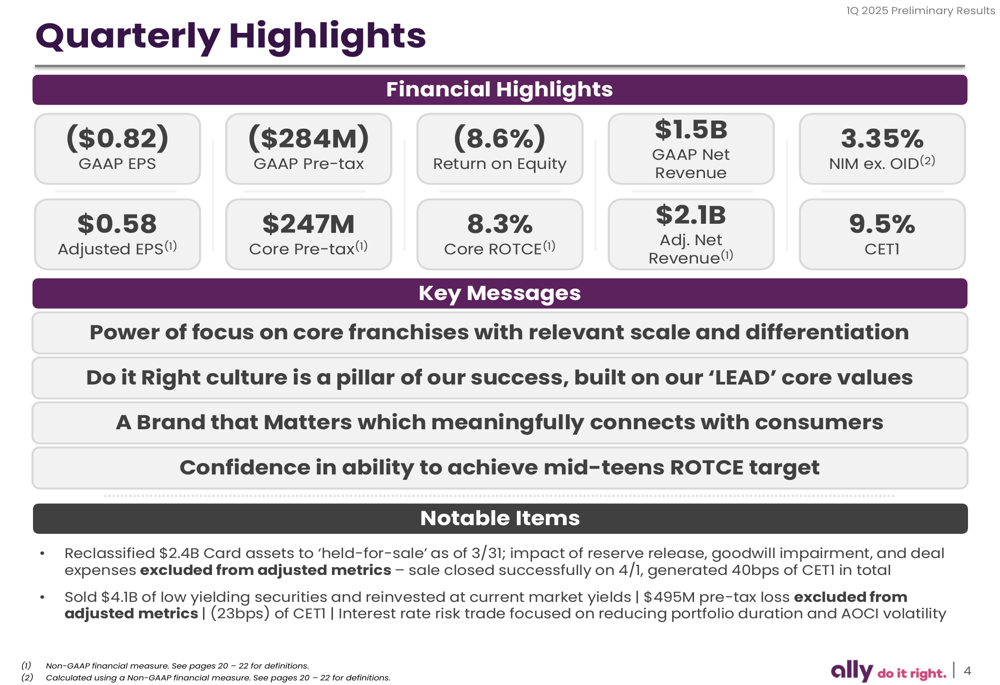

Ally reported a GAAP loss of $(0.82) per share for Q1 2025, a significant decline from the $0.26 EPS in Q4 2024 and $0.37 in Q1 2024. However, adjusted EPS came in at $0.58, reflecting the impact of one-time items. The company’s GAAP pre-tax loss was $(284) million, while core pre-tax income stood at $247 million.

As shown in the following quarterly results summary, the company’s performance metrics show significant divergence between GAAP and adjusted figures:

The quarterly highlights slide reveals the magnitude of repositioning activities, including reclassifying $2.4 billion in card assets to "held-for-sale" (which closed on April 1, generating 40 basis points of CET1 capital) and selling $4.1 billion of low-yielding securities, resulting in a $495 million pre-tax loss:

Net interest margin excluding OID was 3.35%, while the company maintained a CET1 ratio of 9.5%. GAAP net revenue came in at $1.5 billion, compared to adjusted net revenue of $2.1 billion.

Strategic Initiatives

Ally is executing a strategic shift to focus on its core franchises where it has demonstrated competitive advantages. The company highlighted its market-leading positions in auto finance, insurance, corporate finance, and digital banking.

The following slide illustrates Ally’s strength in these core business segments:

The company’s auto finance business generated $10.2 billion in consumer originations from 3.8 million applications, with a retail auto originated yield of 9.8%. Insurance written premiums grew 9% year-over-year, while corporate finance maintained strong performance with a 23% average ROE from 2014-2024.

Ally’s digital banking platform remains a key strength, with $146 billion in retail deposit balances, 92% of which are FDIC insured. The bank is 89% deposit-funded with a cumulative liquid beta of 60%.

Detailed Financial Analysis

The company’s balance sheet and net interest margin details reveal the composition of earning assets and funding sources:

Retail auto loans averaged $83.7 billion with a yield of 9.21% including hedges. Commercial auto loans totaled $21.7 billion with a 6.25% yield, while corporate finance loans reached $10.3 billion yielding 8.78%. On the funding side, deposits averaged $150.6 billion with a cost of 3.78%.

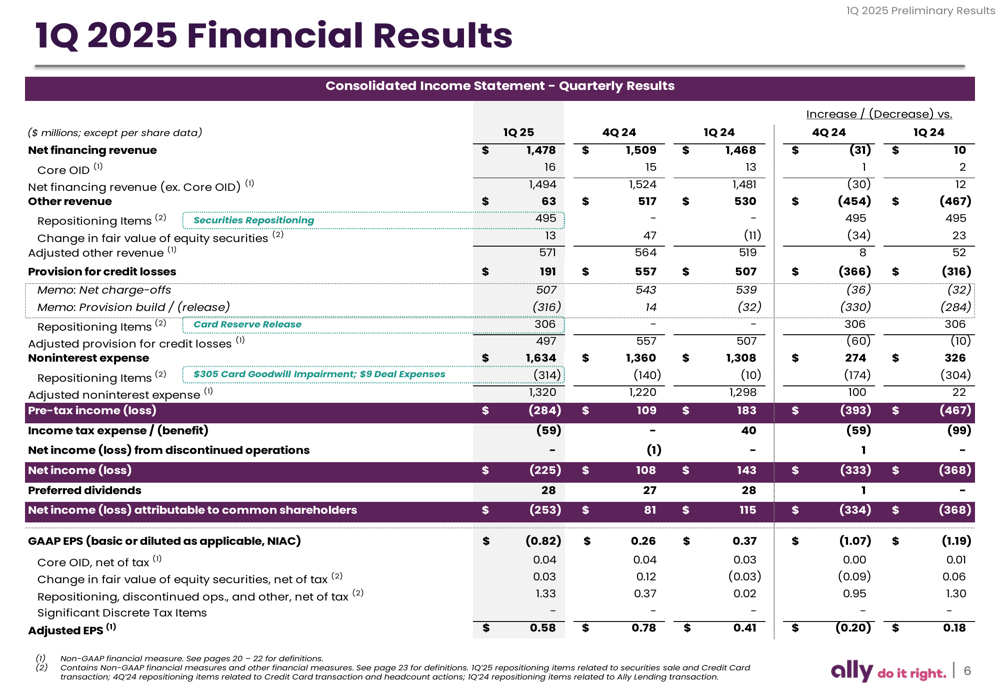

The consolidated income statement shows the significant impact of repositioning items:

Net financing revenue was $1,478 million in Q1 2025, relatively stable compared to $1,509 million in Q4 2024 and $1,468 million in Q1 2024. However, other revenue was significantly impacted by a $495 million repositioning item related to securities sales. Noninterest expense included $314 million in repositioning items, contributing to the pre-tax loss of $284 million.

Asset Quality & Credit Performance

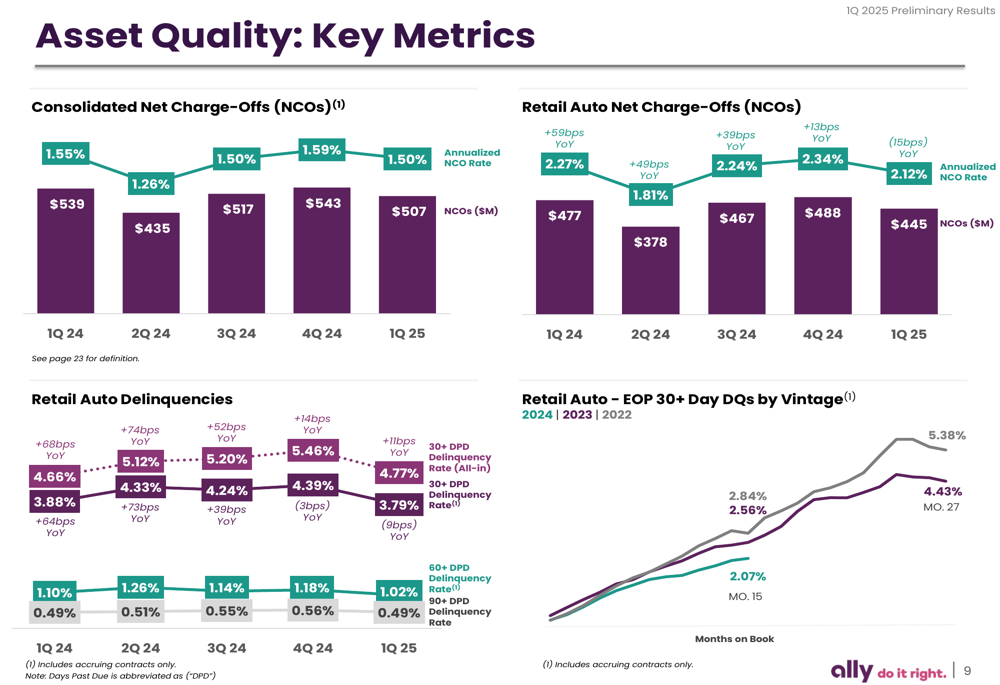

Credit metrics showed mixed performance in the quarter. The consolidated net charge-off rate was 1.50%, while the retail auto net charge-off rate was 2.12%:

Retail auto delinquencies showed some pressure, with the 30+ day delinquency rate at 4.77%. The 60+ and 90+ day delinquency rates were 1.02% and 0.49%, respectively.

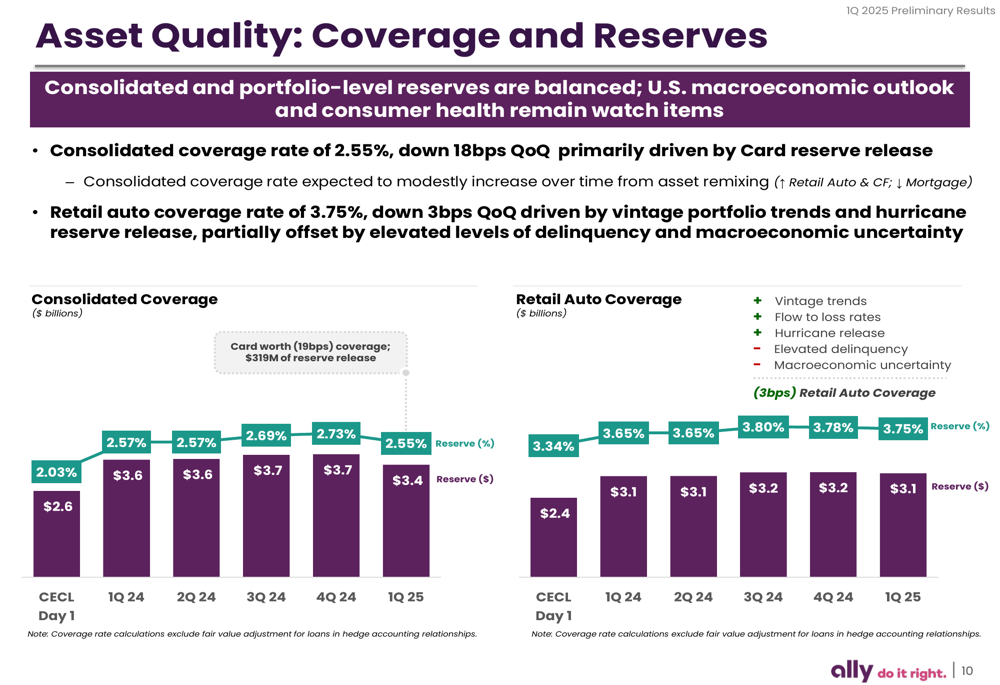

The company’s loan loss reserves remained substantial, with a consolidated coverage ratio of 2.55% and retail auto coverage of 3.75%:

Capital Position

Ally’s capital position is being strengthened through strategic actions, including the sale of its credit card business:

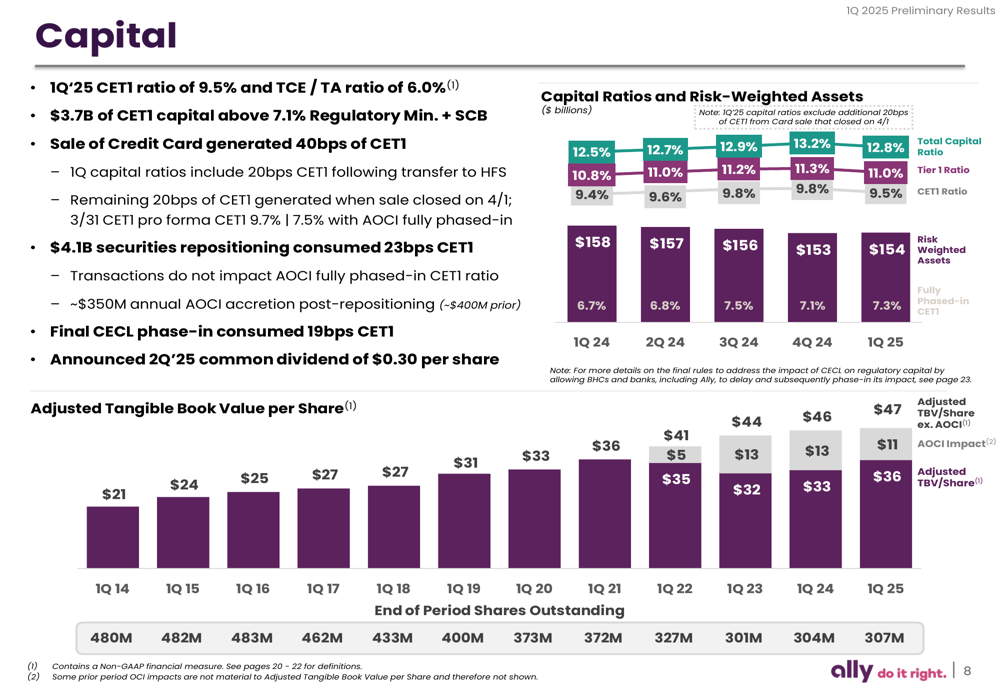

The company reported a CET1 ratio of 9.5% and a TCE/TA ratio of 6.0%. The sale of the credit card business is generating 40 basis points of CET1, with 20 basis points already reflected in Q1 following the transfer to held-for-sale status, and the remaining 20 basis points to be recognized when the sale closed on April 1.

The $4.1 billion securities repositioning consumed 23 basis points of CET1, while the final CECL phase-in consumed an additional 19 basis points. Adjusted tangible book value per share reached $36, up from $21 in Q1 2014.

Segment Performance

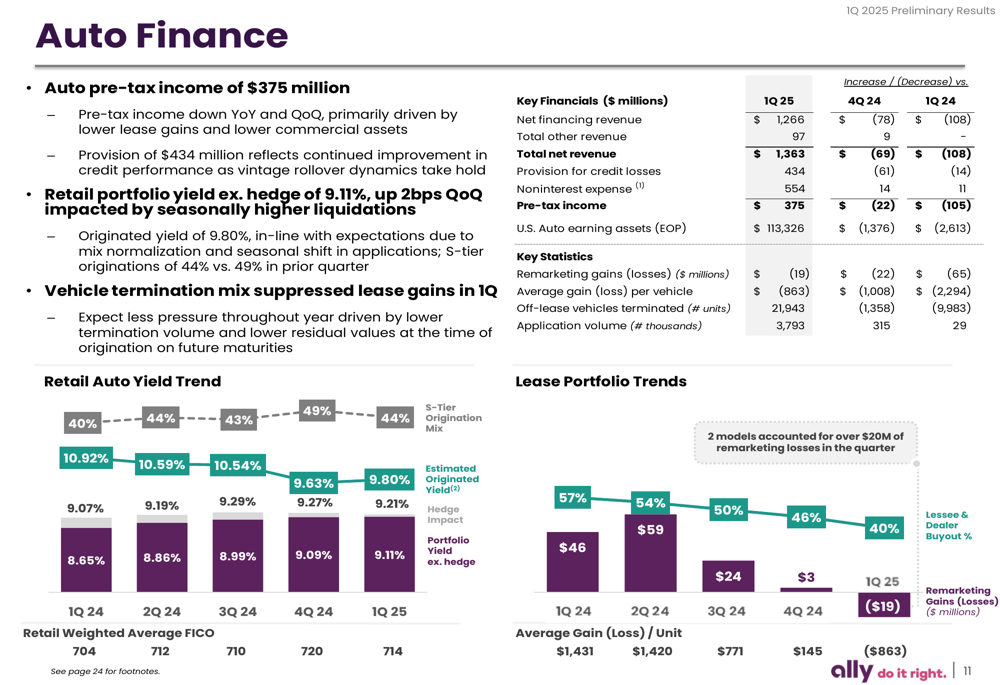

Auto Finance remained the largest contributor to earnings, with pre-tax income of $375 million:

Net financing revenue in the auto segment was $1,266 million, while provision for credit losses was $434 million. The average loss per vehicle was $863, an improvement from $1,008 in the previous quarter and $2,294 a year earlier.

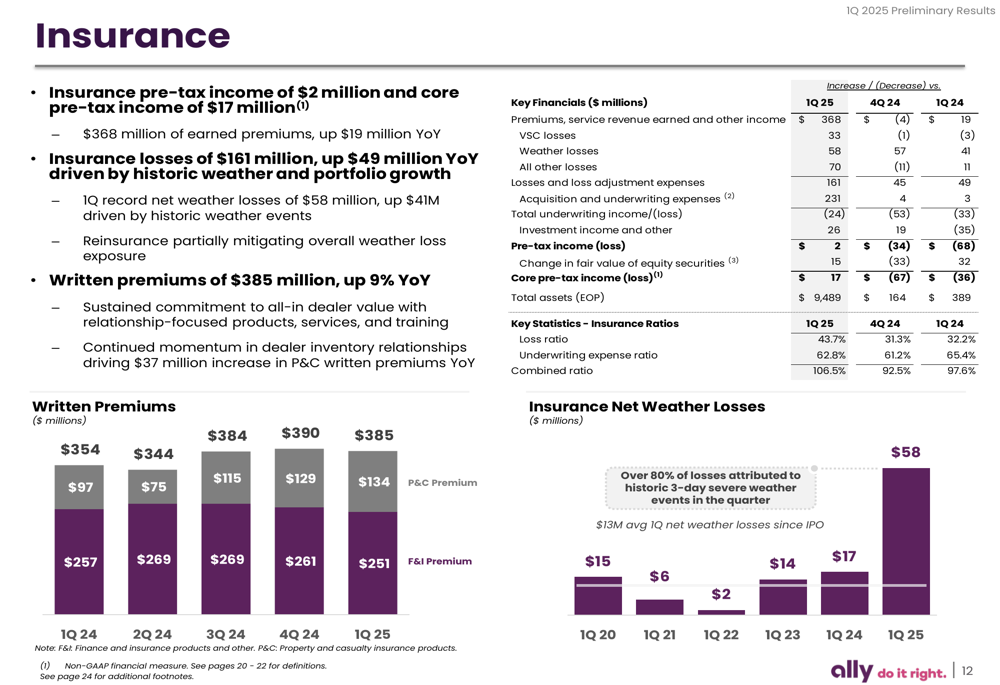

The Insurance segment reported pre-tax income of just $2 million, though core pre-tax income was $17 million:

Insurance losses of $161 million were up $49 million year-over-year, driven by historic weather events and portfolio growth. Written premiums reached $385 million, up 9% year-over-year.

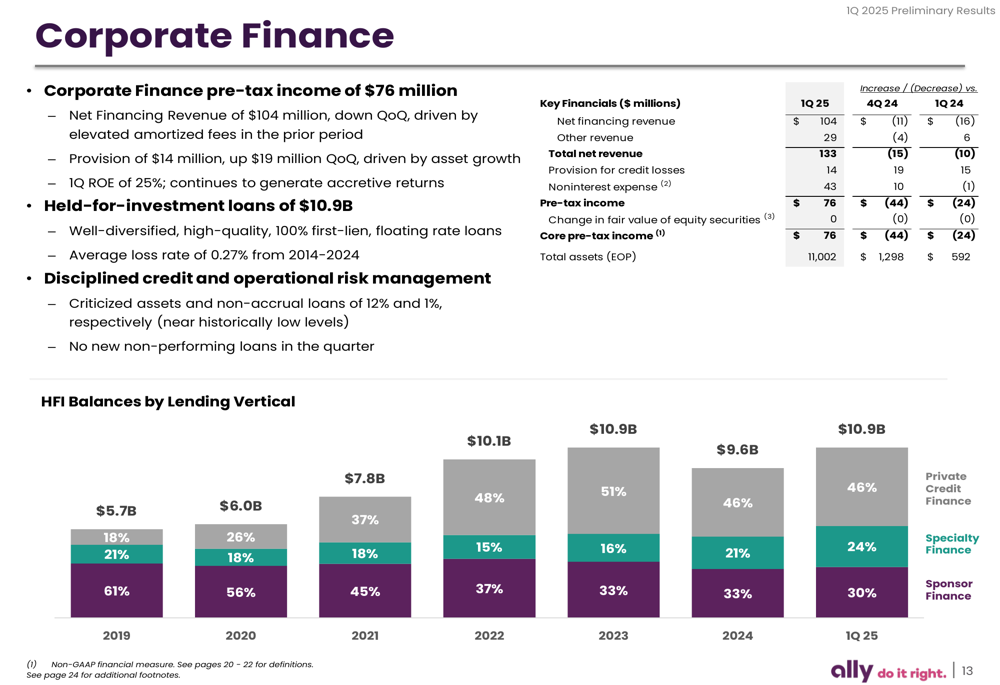

Corporate Finance delivered pre-tax income of $76 million with continued strong performance:

Forward-Looking Statements

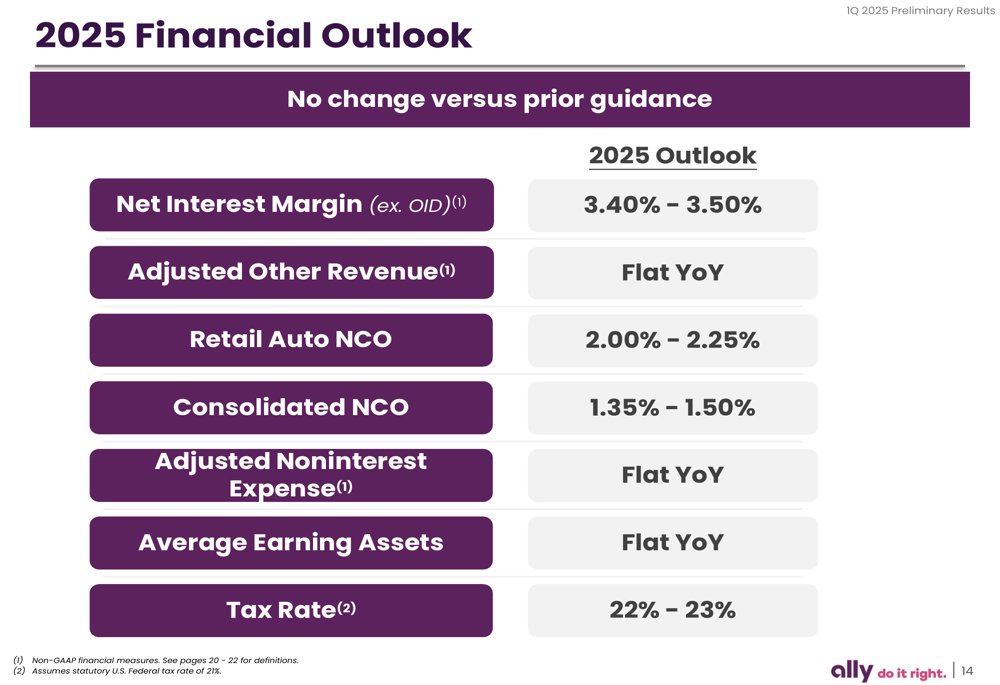

Ally maintained its previous financial outlook for 2025, projecting a net interest margin (excluding OID) of 3.40% to 3.50%:

The company expects retail auto net charge-offs of 2.00% to 2.25% and consolidated net charge-offs of 1.35% to 1.50%. Adjusted noninterest expense and average earning assets are projected to remain flat year-over-year, while the tax rate is expected to be 22% to 23%.

This guidance does not reflect any changes from prior projections, suggesting management’s confidence in the company’s trajectory despite the quarterly GAAP loss.

Analyst Perspectives

While the Q1 2025 presentation doesn’t include analyst perspectives, the company’s Q4 2024 earnings call provided some context for the strategic direction. CEO Michael Rhodes emphasized the company’s focus on core businesses, stating, "We are pursuing a more focused approach in our core businesses where we have demonstrated competitive advantages."

CFO Russ Hutchinson had previously noted, "The destination for us is clear in terms of where we’re going," highlighting management’s confidence in the strategic repositioning despite near-term volatility in results.

The strategic shifts and one-time charges in Q1 2025 appear to be consistent with the direction management outlined in previous communications, focusing on dealer financial services, corporate finance, and deposits while divesting non-core businesses like credit cards.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.