Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

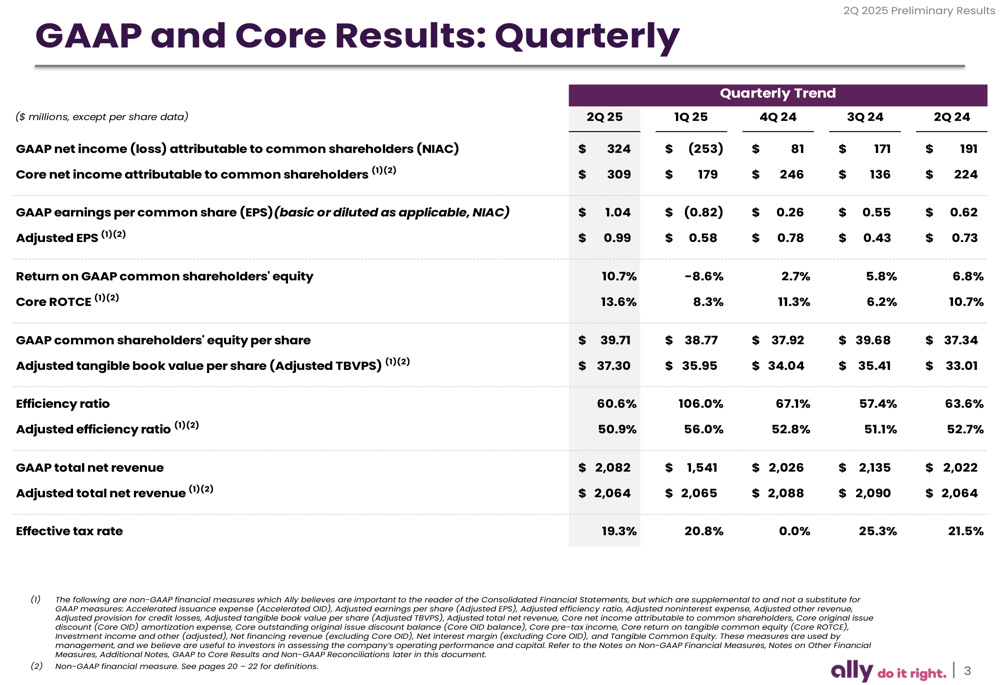

Ally Financial Inc (NYSE:ALLY) shares jumped over 5% in premarket trading after the company presented its Q2 2025 earnings results on July 18, showing a dramatic turnaround from the previous quarter’s loss. The financial services company reported GAAP EPS of $1.04, a significant improvement from the $(0.82) loss in Q1 2025 and up 67.7% from $0.62 in the same quarter last year.

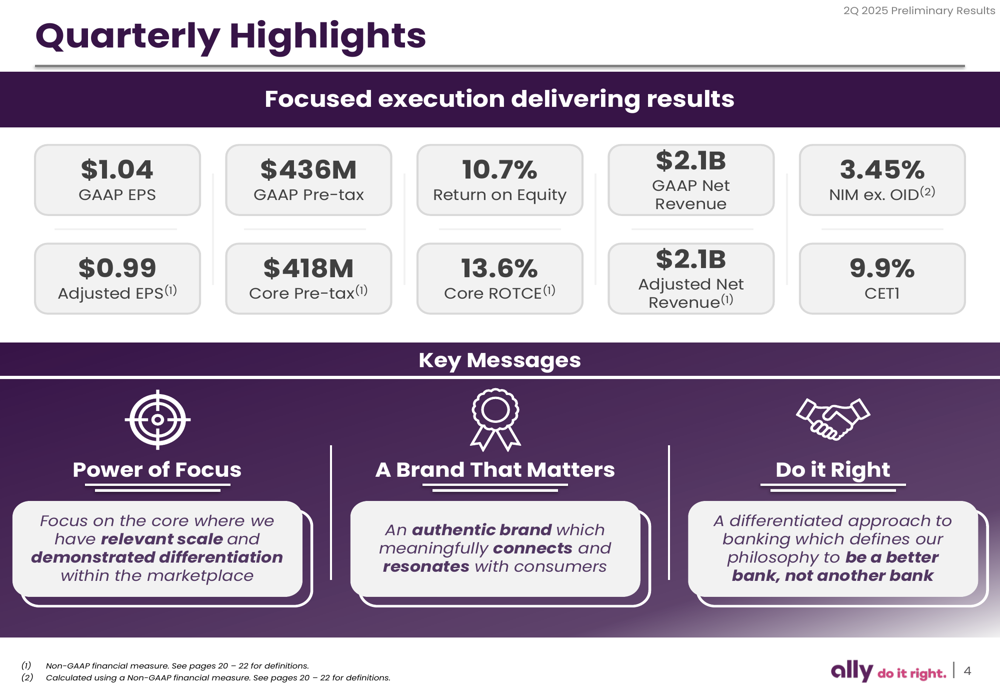

Quarterly Performance Highlights

Ally’s second quarter results demonstrated substantial improvement across key metrics, with GAAP net income attributable to common shareholders reaching $324 million, compared to a $253 million loss in Q1 2025 and $191 million in Q2 2024. The company’s core return on tangible common equity (ROTCE) climbed to 13.6%, up from 8.3% in the previous quarter.

As shown in the following comprehensive financial overview, Ally has demonstrated consistent improvement in several key metrics:

"We are leveraging the power of focus to originate accretive assets in our core business," said CEO Michael Rhodes during the earnings call, a strategy that appears to be paying dividends as evidenced by the company’s improved efficiency ratio of 60.6%, down from 106.0% in Q1 2025.

The quarterly highlights slide emphasizes Ally’s strategic priorities and key financial achievements:

Detailed Financial Analysis

Ally reported GAAP total net revenue of $2.082 billion for Q2 2025, a substantial increase from $1.541 billion in Q1 2025 and slightly higher than the $2.022 billion reported in Q2 2024. The company’s net interest margin (NIM) excluding OID improved to 3.45%, continuing the positive trend seen in the previous quarter.

The provision for credit losses decreased to $384 million in Q2 2025 from $457 million in Q2 2024, reflecting improved credit quality. Pre-tax income showed remarkable recovery at $436 million, compared to a loss of $284 million in Q1 2025 and $279 million in Q2 2024.

Ally’s balance sheet remains strong with earning assets of $178.1 billion and total loans and leases of $140.8 billion. The company maintains a solid deposit base of $148.4 billion, with 92% of retail deposits FDIC insured and 88% of the company being deposit funded.

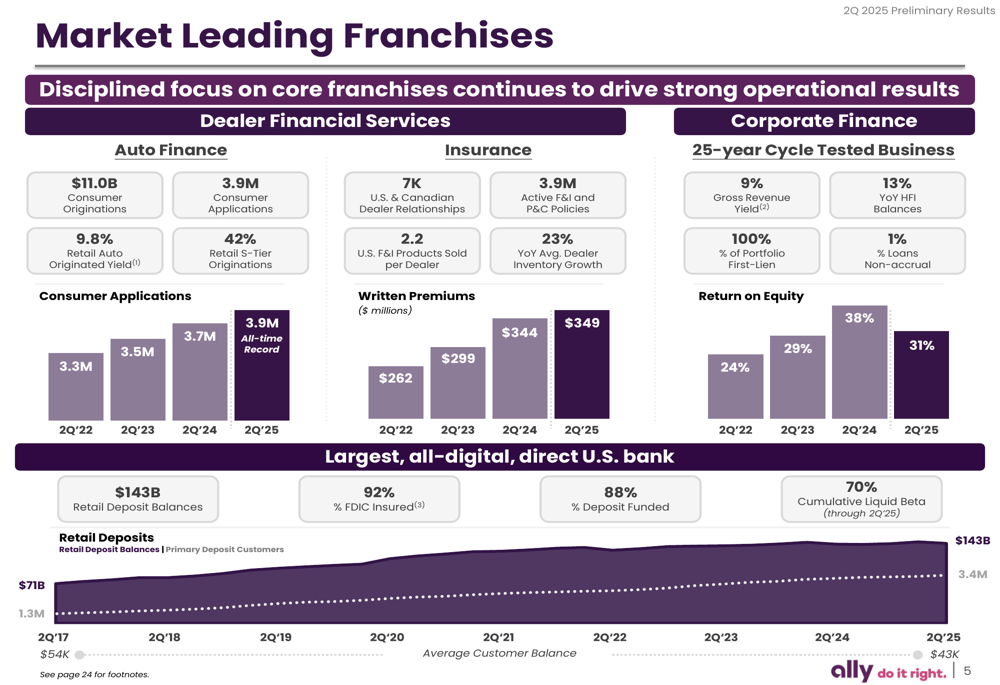

Strategic Initiatives and Business Segment Performance

Following the successful closure of the credit card business sale on April 1, Ally has sharpened its focus on its core businesses. The company highlighted its market-leading franchises across several segments:

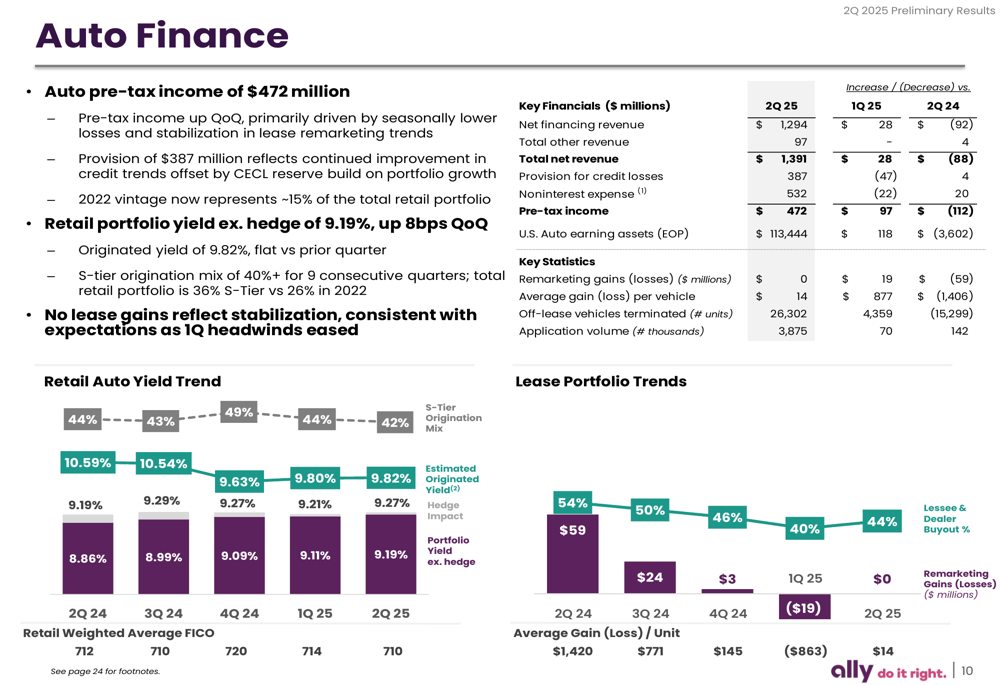

Auto Finance continues to be a key driver of Ally’s performance, with pre-tax income of $472 million in Q2 2025. Consumer originations reached $11.0 billion with 3.9 million applications, an all-time record. The retail auto originated yield remained strong at 9.8%, while the retail portfolio yield excluding hedge effects was 9.19%.

The following chart illustrates key metrics for Ally’s Auto Finance segment:

The Insurance segment generated pre-tax income of $28 million with written premiums of $349 million, while Corporate Finance delivered pre-tax income of $96 million with held-for-investment loans of $11.0 billion, showing the company’s continued focus on responsible growth across its core businesses.

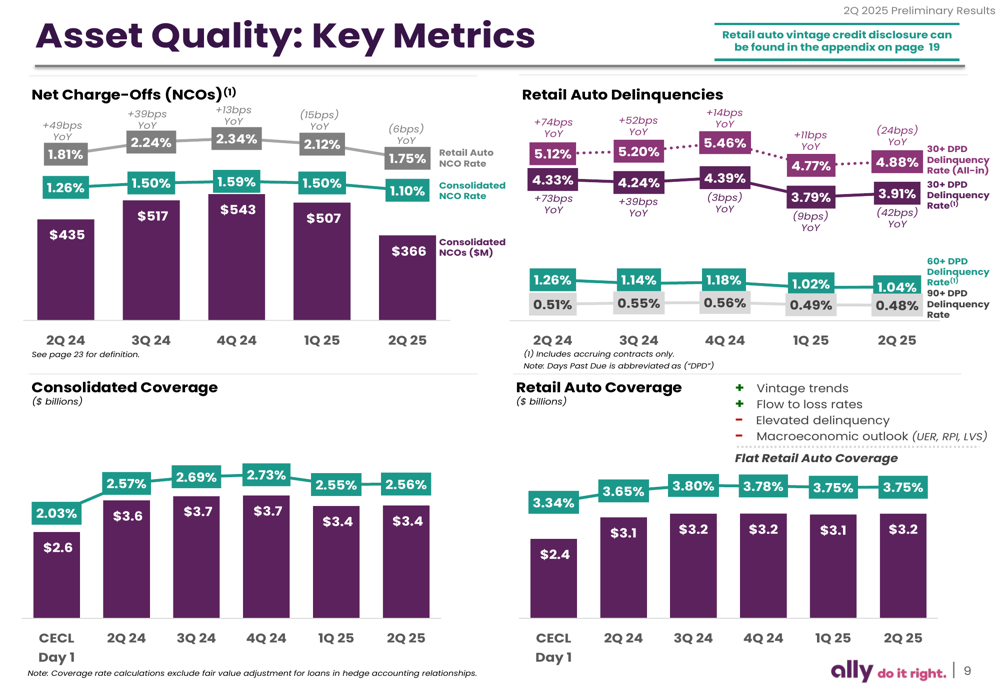

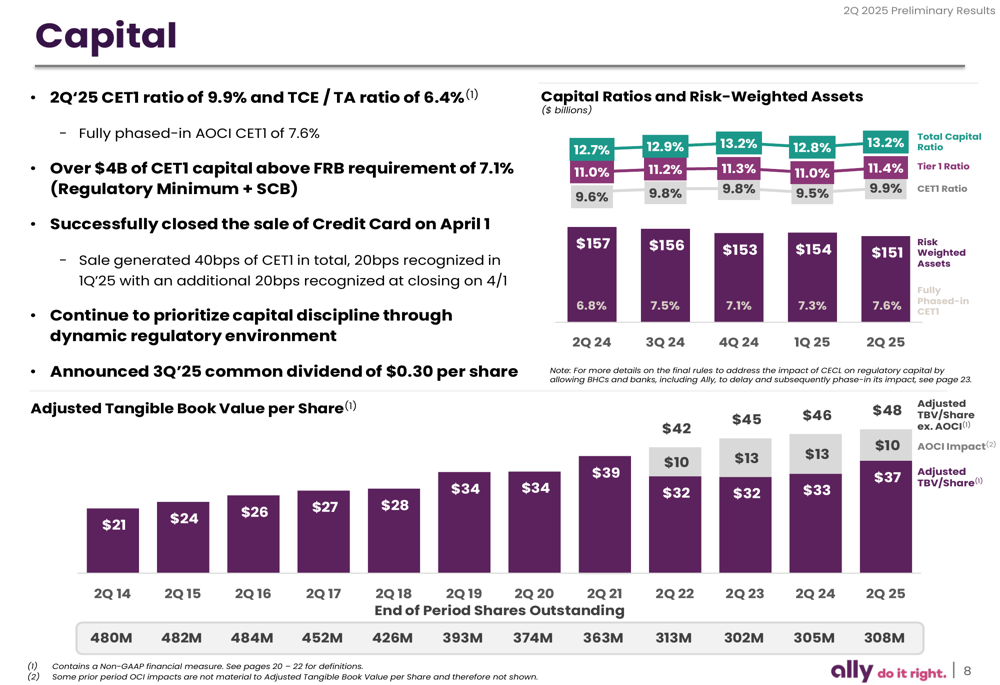

Asset Quality and Capital Position

Ally’s asset quality showed improvement in Q2 2025, with consolidated net charge-offs (NCOs) decreasing to 1.10% from 1.50% in Q1 2025. The retail auto NCO rate was 1.75%, while retail auto delinquencies were 4.88%, a slight increase from 4.77% in the previous quarter.

The following chart details Ally’s asset quality metrics:

The company maintains a strong capital position with a Common Equity Tier 1 (CET1) ratio of 9.9% and a TCE/TA ratio of 6.4%. Ally has over $4 billion of CET1 capital above the Federal Reserve Board requirement of 7.1%, demonstrating its financial stability and capacity for continued growth.

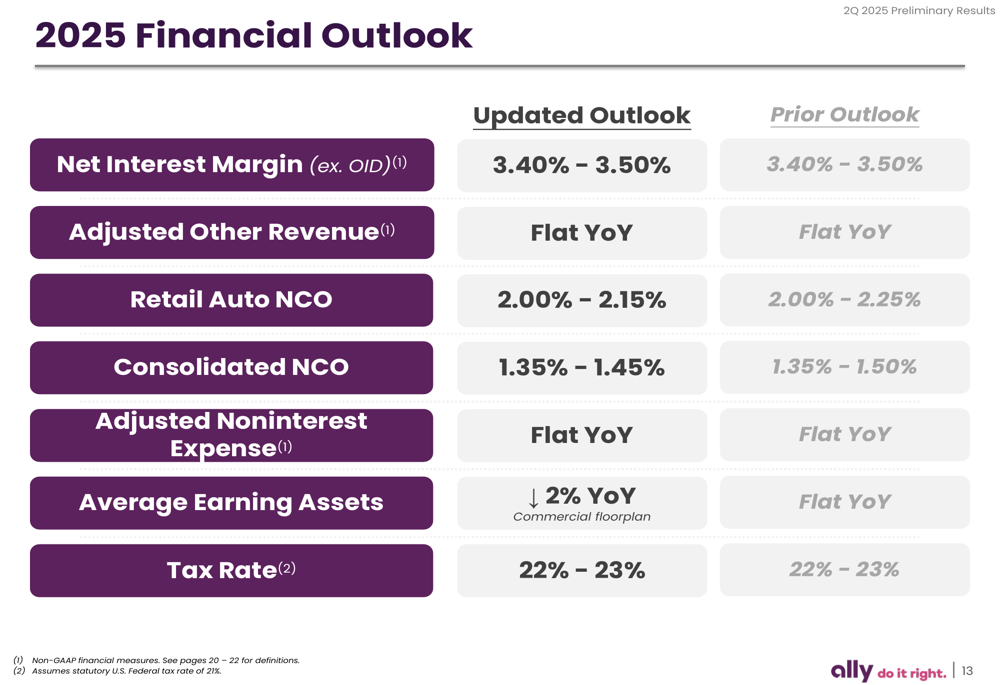

Forward-Looking Statements

Ally provided an updated financial outlook for 2025, maintaining its net interest margin (ex. OID) guidance of 3.40% - 3.50% and projecting flat year-over-year adjusted other revenue. The company expects retail auto net charge-offs to be between 2.00% - 2.15% and consolidated net charge-offs between 1.35% - 1.45%.

The following slide outlines Ally’s financial outlook for the remainder of 2025:

The company also announced a Q3 2025 common dividend of $0.30 per share, reflecting its commitment to returning capital to shareholders while maintaining financial discipline.

Ally’s strong Q2 2025 performance builds on the momentum seen in Q1, where the company beat analyst expectations with an adjusted EPS of $0.58 against a forecast of $0.47. With the divestiture of its credit card business now complete and improved performance across core segments, Ally appears well-positioned to deliver on its financial targets for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.