S&P 500 jumps as AMD rally leads tech higher

Introduction & Market Context

Alpha Metallurgical Resources (NYSE:AMR) released its August 2025 investor presentation amid significant market challenges for the metallurgical coal sector. The presentation comes following a disappointing Q1 2025 earnings report where the company posted an unexpected loss with earnings per share of -$2.50 against a forecasted $3.17. Despite these headwinds, Alpha’s stock has shown recent signs of recovery, trading up 8.15% in premarket to $140 as of August 8, 2025, after closing at $129.45 the previous day.

The investor presentation positions Alpha as a resilient industry leader with long-term growth potential, while acknowledging the cyclical nature of the metallurgical coal market. This comes as the company has implemented cost-cutting measures and reduced production guidance in response to current market conditions.

Strategic Industry Position

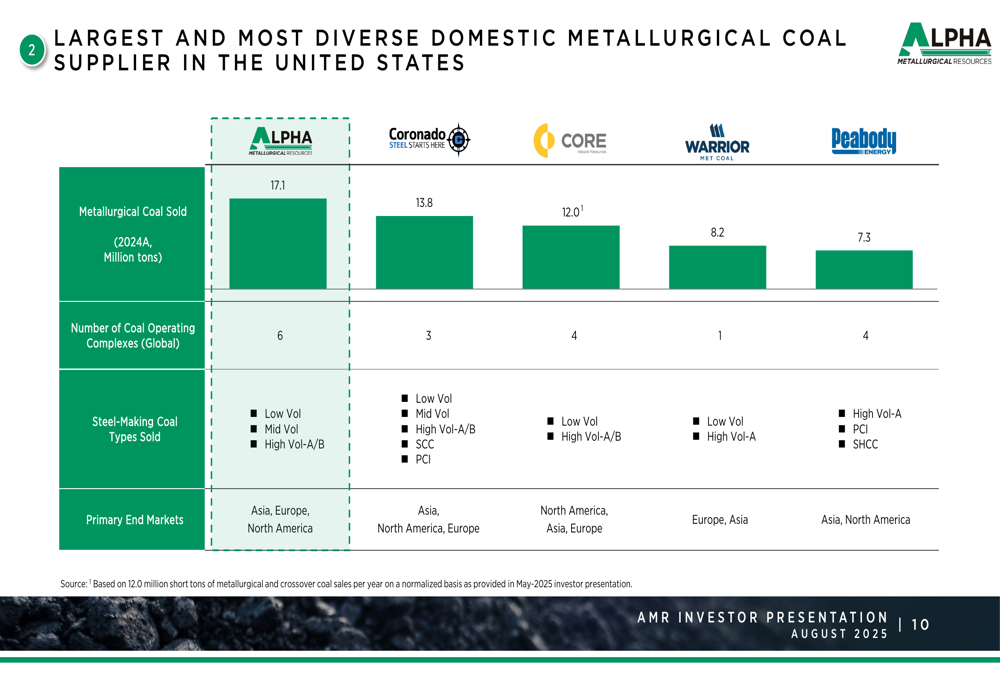

Alpha Metallurgical Resources highlights its position as the largest and most diverse domestic metallurgical coal supplier in the United States. The company’s presentation emphasizes its scale advantage compared to competitors, with 17.1 million tons of metallurgical coal sold in 2024, surpassing rivals Coronado (13.8 million tons), CORE (12.0 million tons), Warrior (8.2 million tons), and Peabody (7.3 million tons).

As shown in the following competitive positioning chart, Alpha operates more coal complexes and offers a more diverse product mix than its peers:

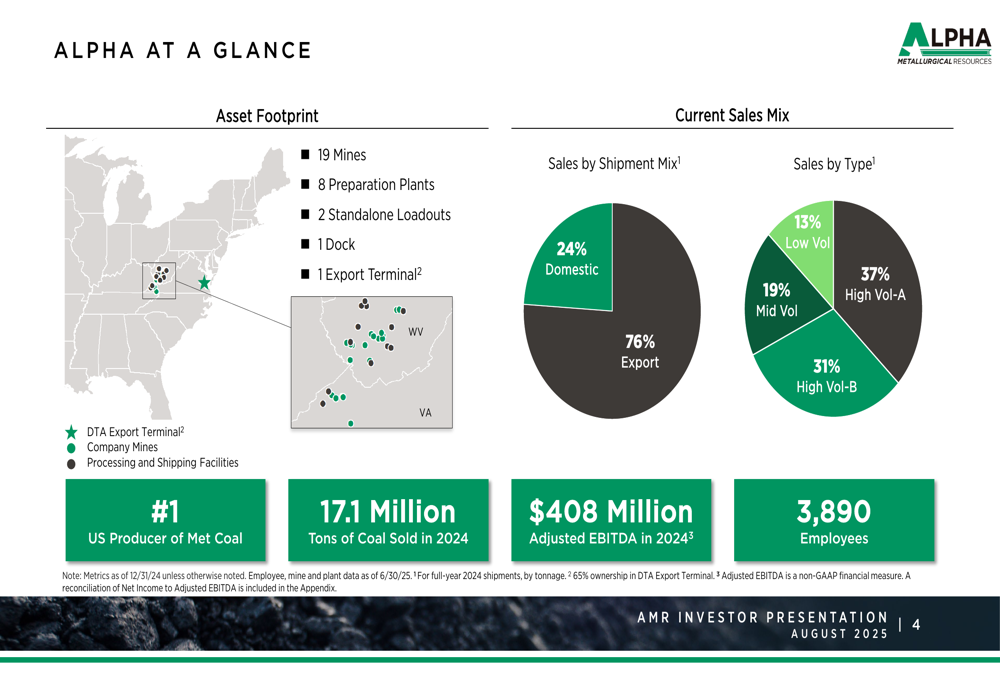

The company’s asset footprint includes 19 mines, 8 preparation plants, 2 standalone loadouts, 1 dock, and 1 export terminal (DTA) strategically located in the eastern United States. Alpha’s sales mix is predominantly export-oriented, with 76% of shipments going to international markets and 24% to domestic customers. The company produces a diverse range of coal types, including Low Vol (13%), Mid Vol (19%), High Vol-A (37%), and High Vol-B (31%).

The following slide provides a comprehensive overview of Alpha’s scale and market position:

Operational Strengths

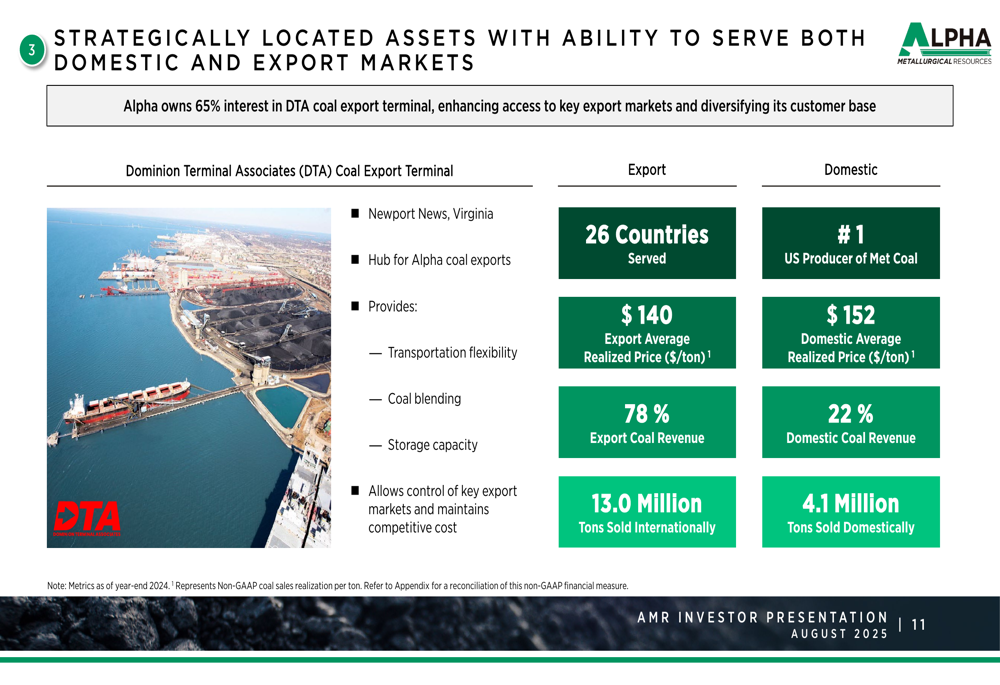

Alpha’s presentation emphasizes its strategically located assets and export capabilities as key competitive advantages. The company owns a 65% interest in the Dominion Terminal Associates (DTA) coal export terminal in Newport News, Virginia, which provides transportation flexibility, coal blending capabilities, and storage capacity.

This strategic position allows Alpha to serve 26 countries internationally while maintaining access to domestic markets. In 2024, the company achieved an average realized price of $140/ton for exported coal and $152/ton for domestic sales, with exports contributing 78% of coal revenue.

The following image illustrates Alpha’s strategic positioning for both domestic and export markets:

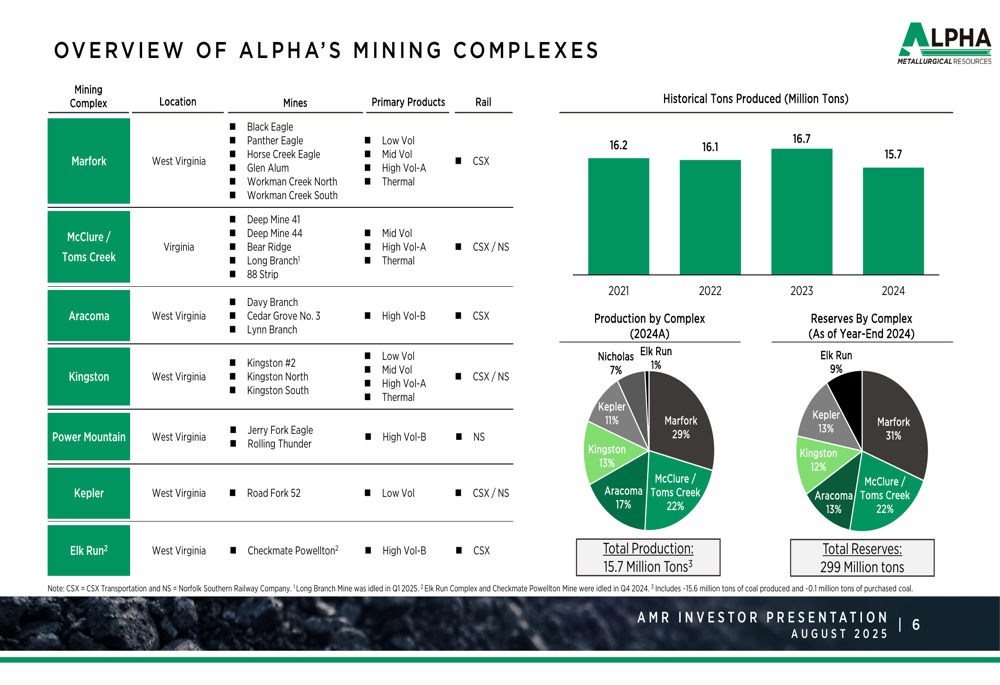

The company’s mining complexes are concentrated in West Virginia and Virginia, with varying production capacities and coal types. The presentation provides a detailed breakdown of these assets:

Alpha also emphasizes its commitment to safety and environmental stewardship, highlighting performance metrics that exceed industry averages. The company reports a Total (EPA:TTEF) Reportable Incident Rate approximately 35% lower than the industry average and a Non-Fatal Days Lost rate approximately 70% below industry norms. Environmental initiatives include planting 5.3 million trees since 2016 and maintaining a 99.9%+ water quality compliance rate.

Financial Performance & Outlook

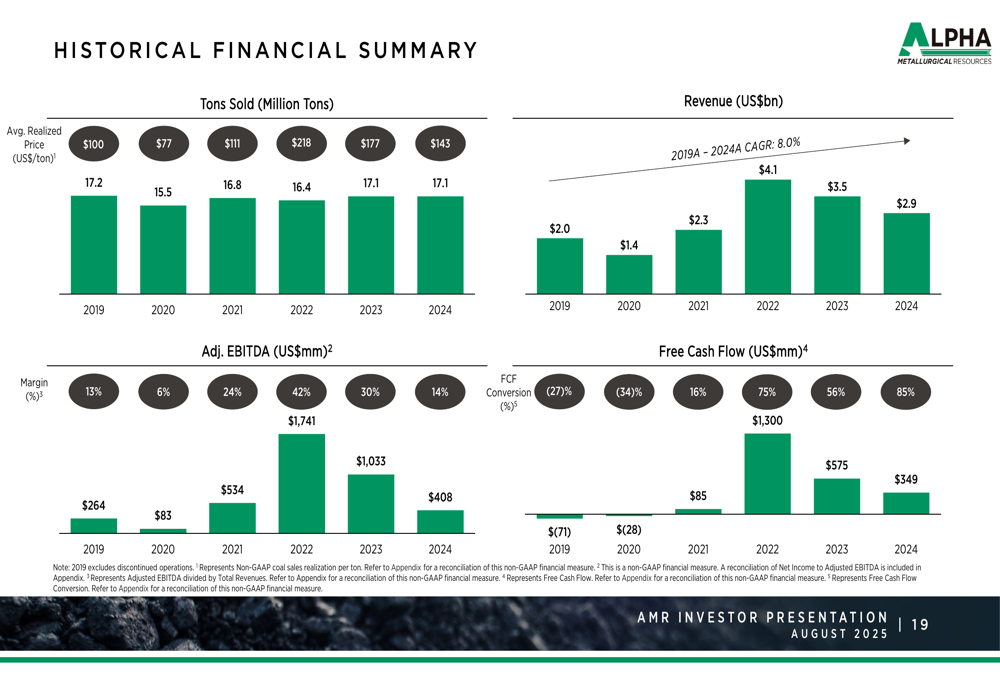

The investor presentation showcases Alpha’s historical financial performance from 2019 through 2024, revealing both the cyclical nature of the business and the company’s ability to generate significant cash flow during favorable market conditions. Revenue peaked at $4.1 billion in 2022 before declining to $2.9 billion in 2024, while Adjusted EBITDA followed a similar pattern, reaching $1.74 billion in 2022 before falling to $408 million in 2024.

The following historical financial summary illustrates these trends:

However, this historical performance contrasts sharply with Alpha’s recent Q1 2025 results, which showed significant weakness with adjusted EBITDA dropping to just $5.7 million from $53 million in Q4 2024. The earnings miss prompted a reduction in 2025 shipment guidance to 13.8-14.8 million tons, down from the 17.1 million tons shipped in 2024.

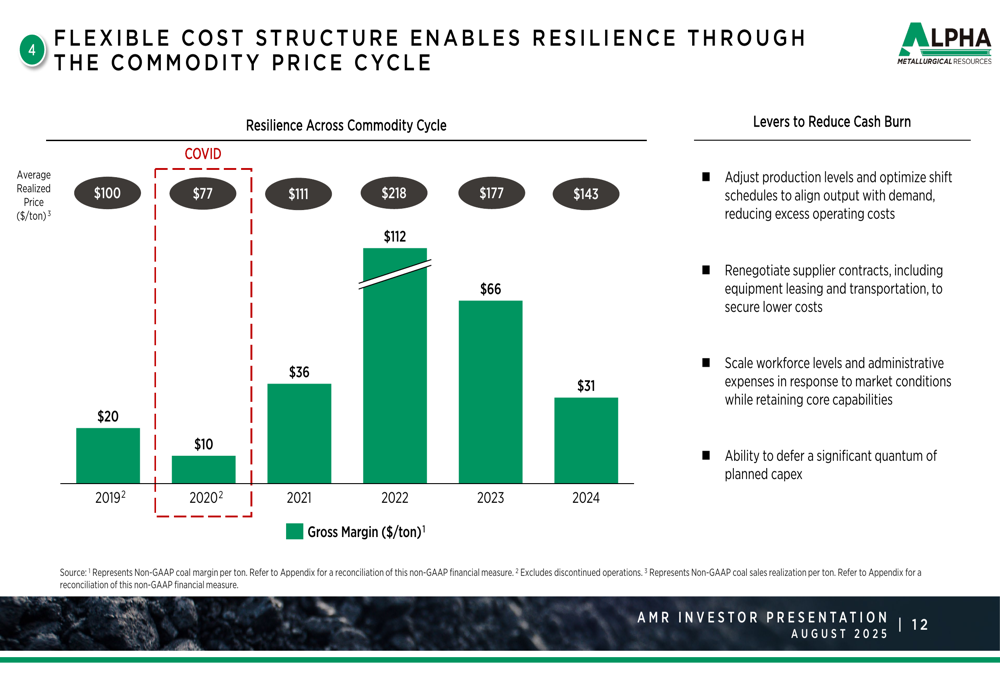

Alpha’s presentation emphasizes its flexible cost structure as a key element in navigating commodity price cycles. The company highlights its ability to adjust production levels, renegotiate contracts, scale workforce levels, and defer capital expenditures when necessary. This flexibility is illustrated in the following chart showing average realized prices and gross margins from 2019-2024:

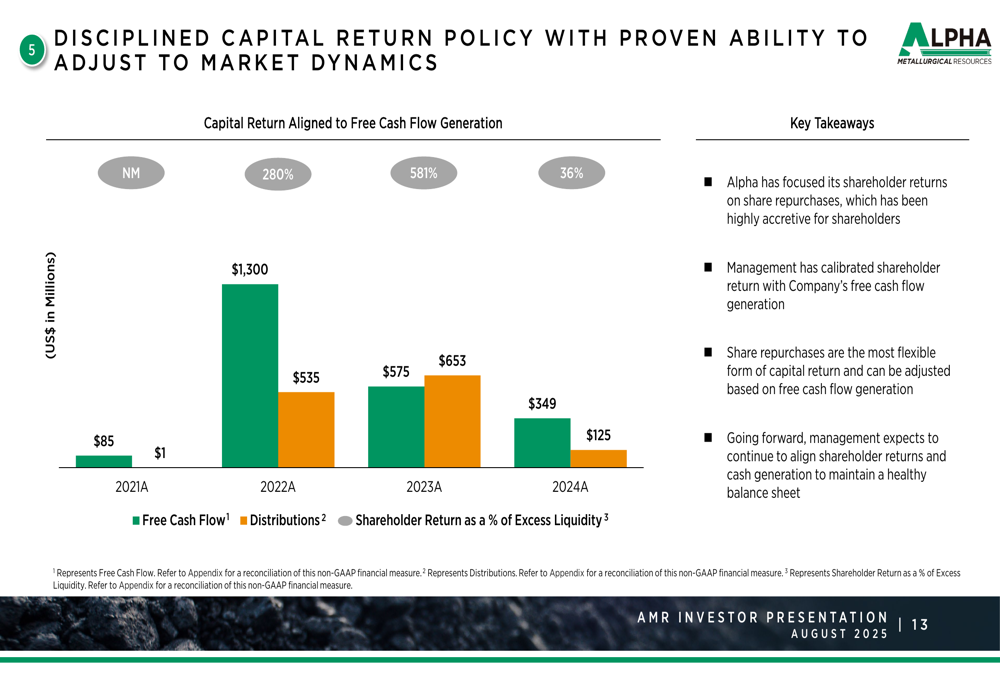

The company also outlines its disciplined capital allocation framework, prioritizing balance sheet strength with a target minimum liquidity of $250-300 million. Alpha has demonstrated a willingness to return capital to shareholders during strong market conditions, with capital returns reaching 581% of free cash flow in 2023 before moderating to 36% in 2024 as market conditions deteriorated.

Long-term Market Outlook

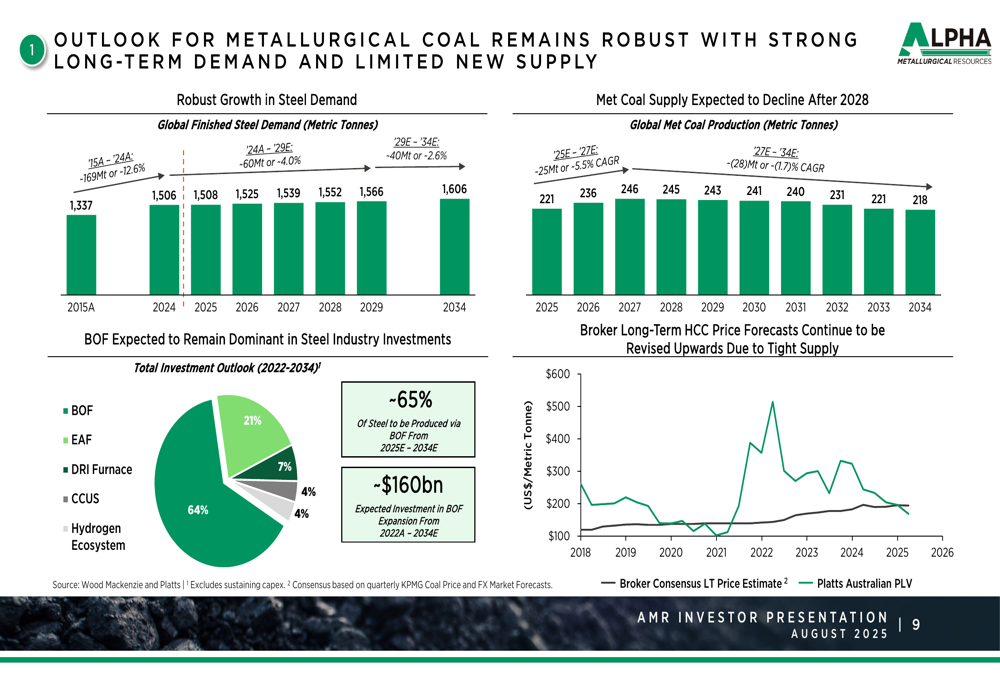

Despite current market challenges, Alpha’s presentation projects a robust long-term outlook for metallurgical coal demand. The company cites forecasts showing global finished steel demand increasing from 1,337 million tonnes in 2015 to 1,606 million tonnes by 2034. Simultaneously, global metallurgical coal production is expected to decline after 2028, potentially creating favorable supply-demand dynamics.

The presentation also notes that approximately 65% of steel is expected to be produced via the Basic Oxygen Furnace (BOF) method from 2025-2034, which requires metallurgical coal as a key input. This projection is supported by an estimated $160 billion of expected investment in BOF expansion.

The following chart illustrates these long-term market projections:

This optimistic long-term outlook stands in contrast to the current market weakness cited in Alpha’s Q1 2025 earnings report, where CEO Andy Edson emphasized the company’s focus on "internal opportunities" amid challenging conditions. The company’s Chief Commercial Officer Dan Horn acknowledged the weak market environment, noting that weak markets "tend to be more discounting against the indices."

Forward-Looking Statements

Alpha’s management team, led by CEO Andy Eidson, emphasizes their deep industry expertise and familiarity with the company’s asset base as key factors in navigating the current downturn. The presentation highlights the leadership team’s experience:

The company’s forward strategy focuses on maintaining financial flexibility while positioning for an eventual market recovery. Alpha has reduced its 2025 capital expenditure guidance to $130-150 million, reflecting a more cautious approach in the current environment.

Despite near-term challenges, Alpha continues to advance strategic projects, particularly the Kingston and Wildcat mine development mentioned by CEO Edson in the Q1 earnings call. The company’s presentation emphasizes its ability to adjust capital spending based on market conditions while maintaining operational readiness for market improvement.

Alpha’s August 2025 presentation reflects a company navigating the tension between current market headwinds and long-term industry optimism. While the recent stock price recovery suggests investors may be looking beyond the Q1 earnings disappointment, the company’s reduced guidance and cost-cutting measures underscore the significant challenges facing metallurgical coal producers in the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.