Intel stock spikes after report of possible US government stake

Alphabet (NASDAQ:GOOGL) Inc. (NASDAQ:GOOG) shares jumped 4.35% in aftermarket trading following the release of its Q1 2025 earnings presentation on April 24, 2025, which revealed strong financial performance across most segments. The tech giant reported 12% year-over-year revenue growth and a significant expansion in profitability metrics, with particularly impressive results from its Cloud division.

Quarterly Performance Highlights

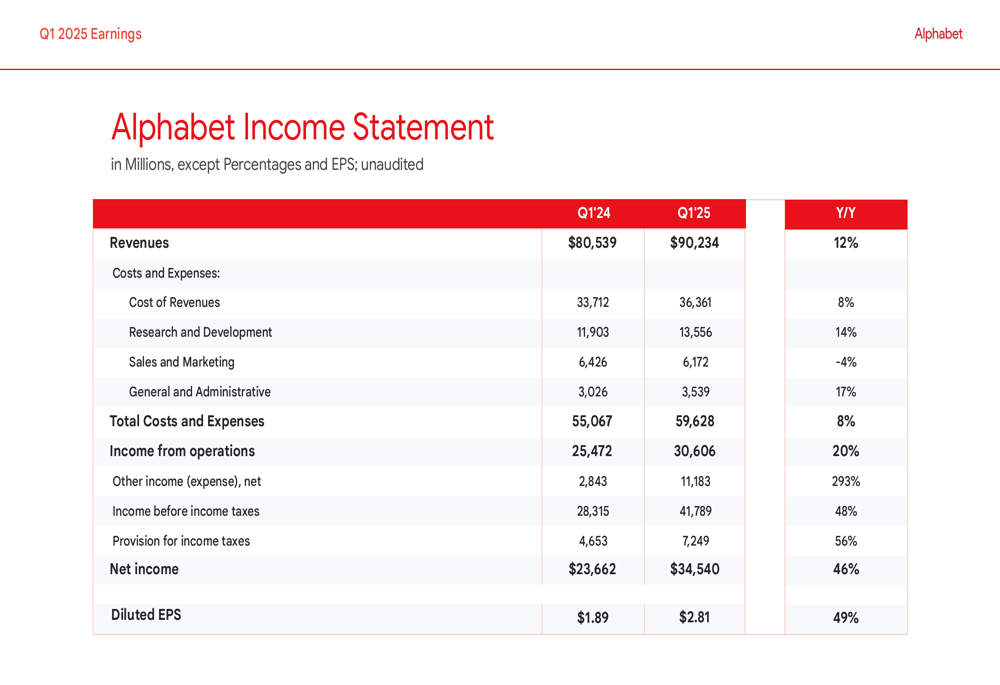

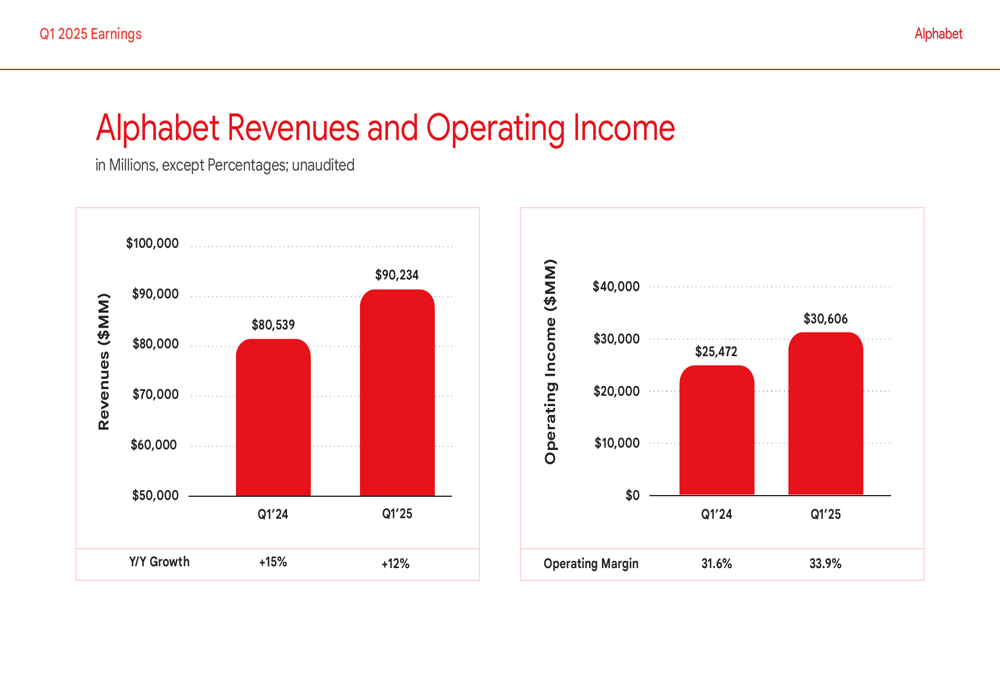

Alphabet delivered robust financial results for the first quarter of 2025, with total revenue reaching $90.23 billion, up 12% from $80.54 billion in the same period last year. The company’s operating income surged 20% year-over-year to $30.61 billion, while net income jumped an impressive 46% to $34.54 billion. Diluted earnings per share increased 49% to $2.81 from $1.89 in Q1 2024.

As shown in the following comprehensive income statement, Alphabet demonstrated strength across key financial metrics:

The company’s operating margin expanded to 33.9% in Q1 2025, up from 31.6% in the year-ago quarter, reflecting improved operational efficiency. This margin expansion occurred despite continued investments in research and development, which grew 14% year-over-year to $13.56 billion.

The following chart clearly illustrates Alphabet’s revenue and operating income growth:

Detailed Financial Analysis

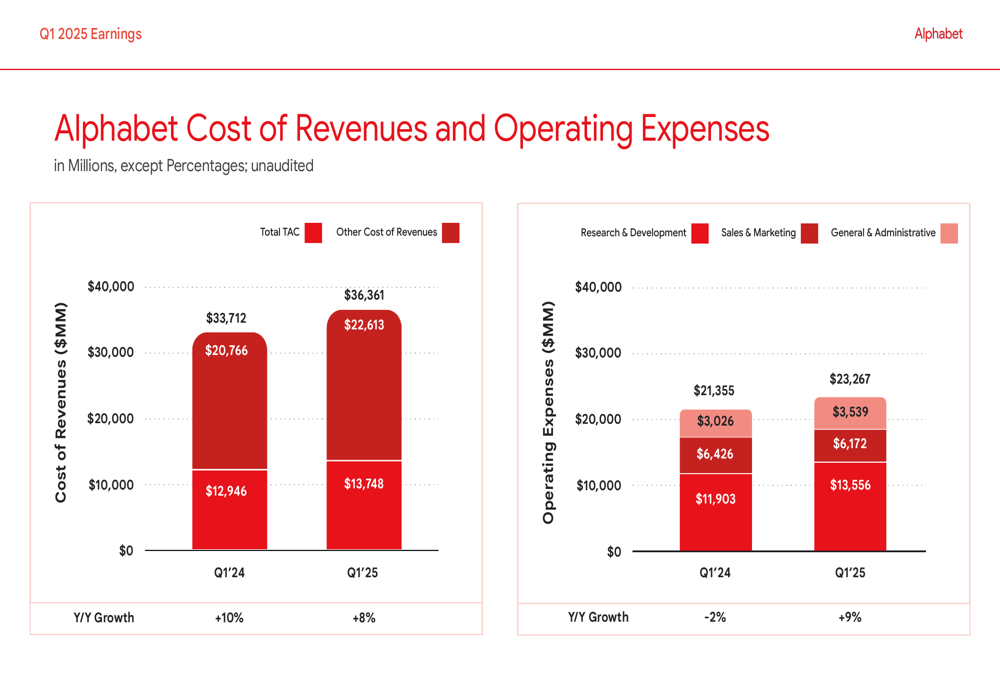

Alphabet’s cost structure showed disciplined management, with total costs and expenses growing at a slower rate (8%) than revenue (12%). The company achieved a 4% year-over-year reduction in sales and marketing expenses, which declined to $6.17 billion from $6.43 billion in Q1 2024.

Other income saw a dramatic increase of 293% to $11.18 billion, significantly contributing to the bottom line. This surge helped drive the 46% increase in net income, outpacing the growth in operating income.

The breakdown of costs and expenses reveals Alphabet’s spending priorities:

Google Services Performance

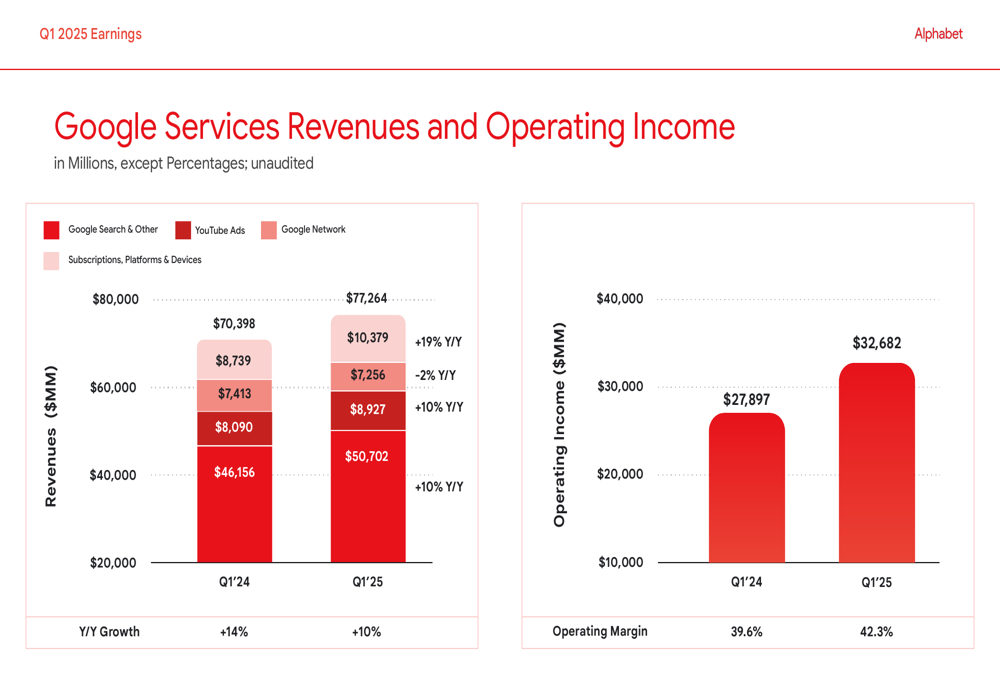

Google Services, which includes Search, YouTube, and other advertising products, generated $77.26 billion in revenue from Google Search & Other, representing a 10% year-over-year increase. However, YouTube Ads showed a concerning 2% decline to $7.26 billion from $8.74 billion in Q1 2024.

Despite this weakness in YouTube, Google Services overall delivered strong results with a 10% revenue growth and an operating margin of 42.3%, up from 39.6% in the prior year period.

The following chart details the performance of Google Services segments:

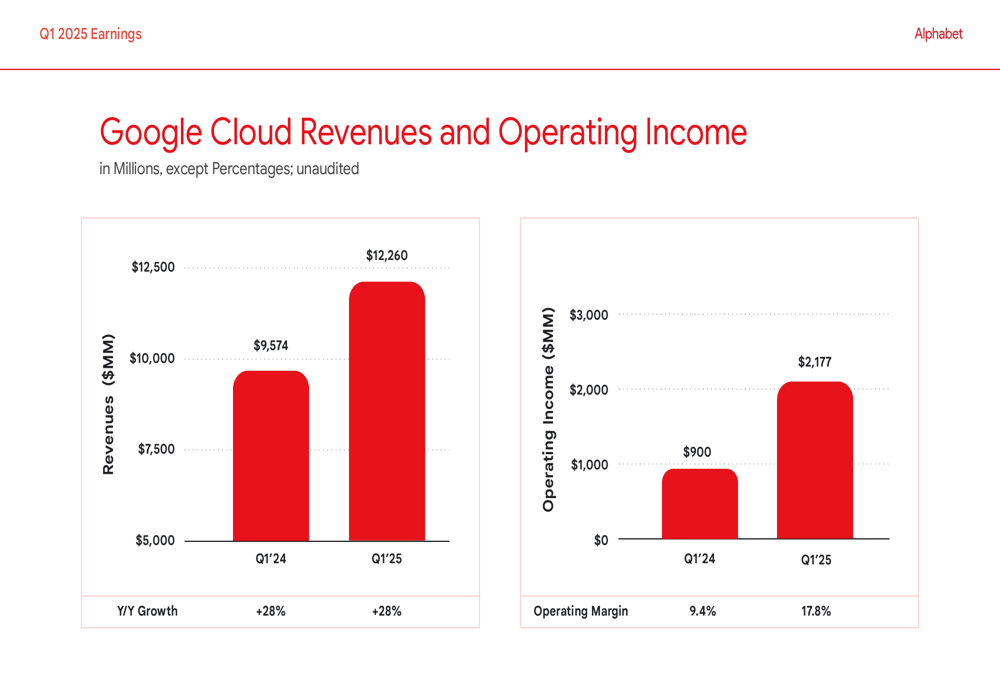

Google Cloud’s Continued Success

Google Cloud emerged as a standout performer in Alphabet’s portfolio, with revenue increasing 28% year-over-year to $12.26 billion. More impressively, Cloud’s operating margin nearly doubled to 17.8% from 9.4% in Q1 2024, demonstrating significant progress in profitability for this strategic growth segment.

The following chart highlights Google Cloud’s impressive trajectory:

This performance continues the momentum seen in previous quarters, as Google Cloud strengthens its position in the competitive cloud computing market against rivals Amazon (NASDAQ:AMZN) Web Services and Microsoft (NASDAQ:MSFT) Azure.

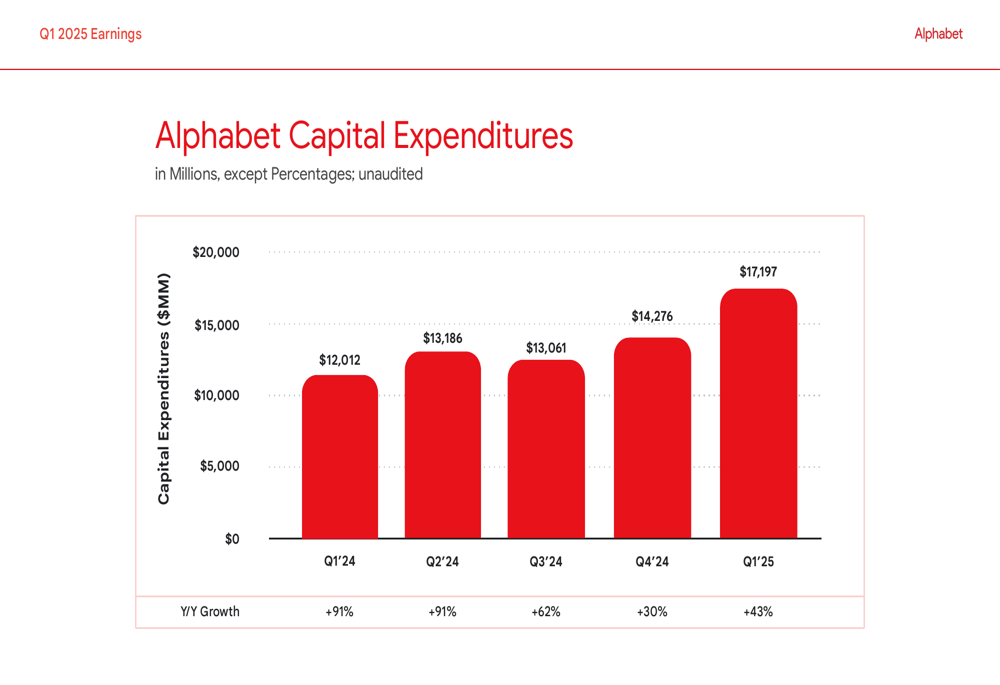

Capital Expenditures and Cash Flow

Alphabet significantly increased its capital investments in Q1 2025, with capital expenditures rising 43% year-over-year to $17.20 billion. This represents the fifth consecutive quarter of substantial capex growth, likely reflecting continued investments in data centers, technical infrastructure, and AI capabilities.

The following chart shows the consistent upward trend in capital expenditures:

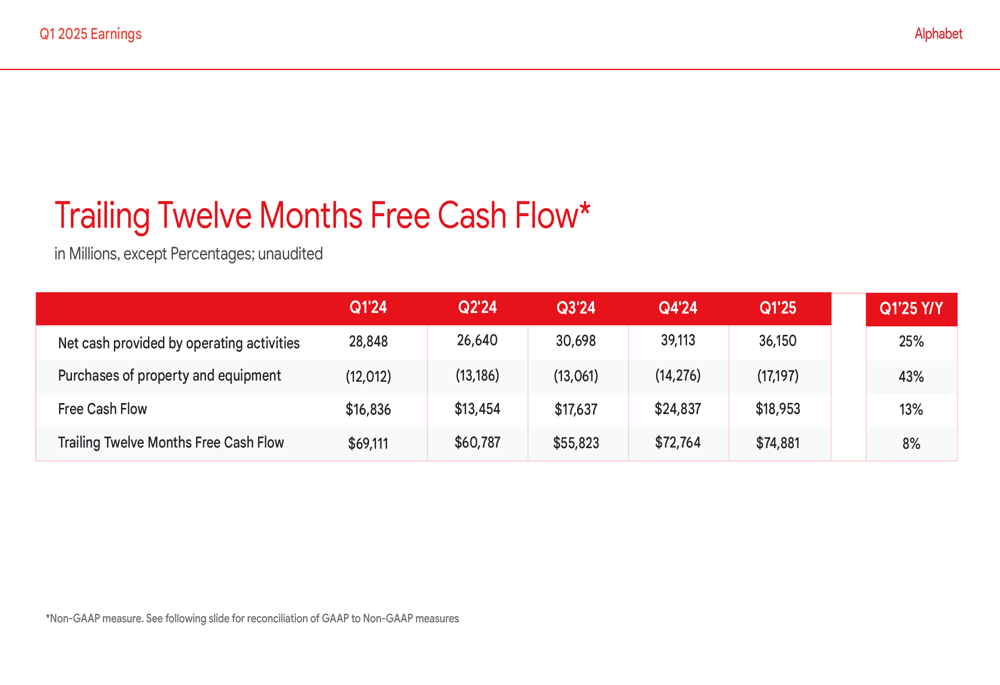

Despite these elevated investments, Alphabet maintained strong cash generation. Free cash flow for Q1 2025 reached $18.95 billion, a 13% increase from the prior year. On a trailing twelve-month basis, free cash flow grew 8% to $74.88 billion, demonstrating Alphabet’s ability to fund significant investments while still delivering improved cash returns.

The company’s cash flow metrics are detailed in the following table:

Forward-Looking Statements

While Alphabet’s presentation didn’t provide explicit guidance for future quarters, the significant investments in capital expenditures suggest continued focus on expanding infrastructure to support AI initiatives and cloud services growth. The consistent increase in R&D spending (up 14% year-over-year) also indicates ongoing commitment to innovation.

The company’s strong free cash flow position provides substantial flexibility for future investments, share repurchases, or potential dividend increases. However, the decline in YouTube advertising revenue bears watching, as it represents a rare weak spot in an otherwise strong performance.

Alphabet’s stock reaction in aftermarket trading suggests investors were pleased with the results, particularly the acceleration in profitability metrics and the continued strong performance of the Google Cloud segment. With shares trading at $168.50 in the aftermarket, up 4.35% from the closing price of $157.72, the market appears to be rewarding Alphabet’s ability to deliver both growth and margin expansion in a competitive technology landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.