Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

AltaGas Ltd (TSX:ALA) released its Q1 2025 financial results on May 1, 2025, showcasing modest growth amid its ongoing strategic shift toward a lower-risk business model. The company reported normalized EBITDA of $689 million, up 4.4% from $660 million in Q1 2024, while normalized earnings per share increased slightly to $1.15 from $1.14 in the same period last year.

The results reflect AltaGas’s continued execution of its strategy to increase contracted cashflows and reduce commodity exposure, with the Utilities segment delivering strong performance while the Midstream segment faced headwinds. The company’s stock closed at $40.80 on the reporting day, down 0.86% amid broader market fluctuations.

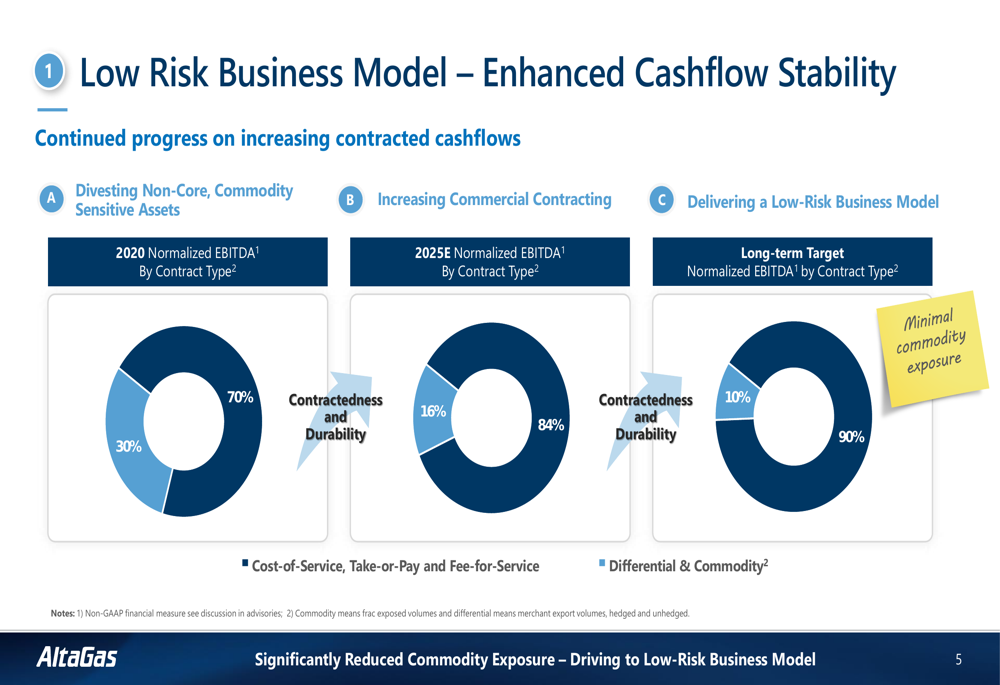

As shown in the following chart, AltaGas has been steadily transitioning toward a lower-risk business model with enhanced cashflow stability through increased contracted revenues:

Quarterly Performance Highlights

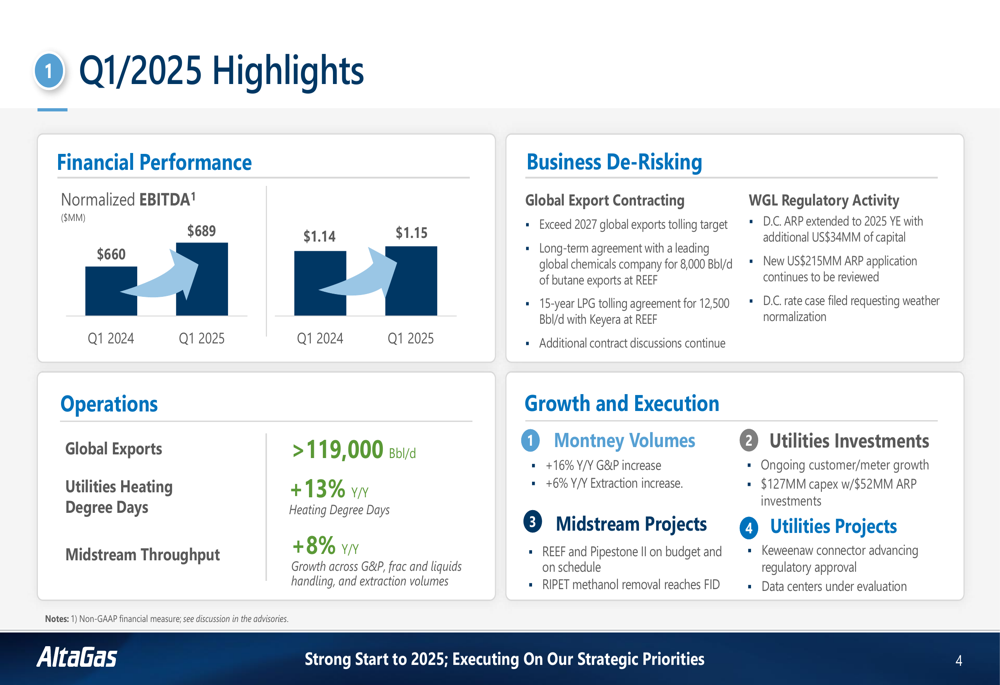

AltaGas reported several key achievements in Q1 2025, including exceeding its 2027 global exports tolling target and securing long-term agreements for LPG exports. The company’s global exports exceeded 119,000 barrels per day, while utilities heating degree days increased 13% year-over-year and midstream throughput grew 8%.

The following slide highlights the company’s Q1 2025 performance across financial, operational, and strategic dimensions:

The company’s financial results showed divergent performance across segments. The Utilities segment delivered a 15% year-over-year increase in normalized EBITDA to $501 million, driven by strong retail performance, favorable weather conditions in D.C. and Michigan, lower operating and maintenance costs at WGL, and asset optimization.

In contrast, the Midstream segment experienced a 20% decline in normalized EBITDA to $197 million, primarily due to lower margins in global exports despite higher volumes, increased operating expenses, and the absence of one-time gains that benefited Q1 2024 results.

Segment Analysis

Utilities Segment

The Utilities segment was the standout performer in Q1 2025, with normalized EBITDA increasing 15% year-over-year to $501 million. This growth was driven by several factors, including strong retail results, colder weather in D.C. and Michigan, ongoing cost management initiatives, and rate base growth through modernization investments.

The company highlighted a 9% year-over-year reduction in operations and maintenance costs across all utilities, driven by process efficiencies and a focus on core operations. Capital investments in the quarter totaled $127 million, with $52 million directed to accelerated replacement programs (ARP) and modernization initiatives.

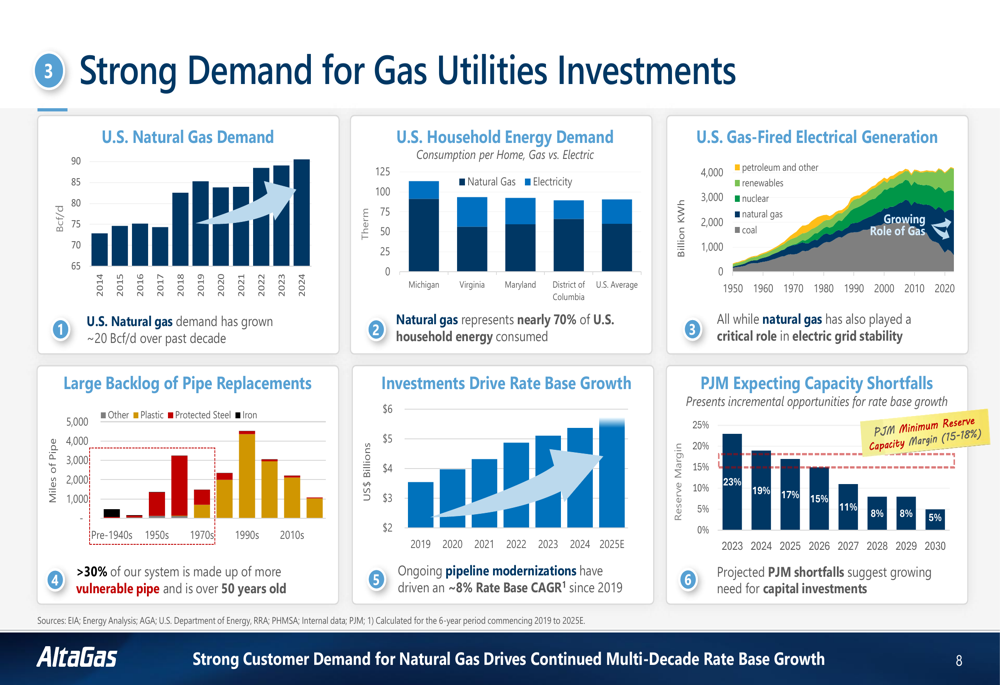

As illustrated in the following chart, strong demand fundamentals continue to support AltaGas’s utilities investments:

Midstream Segment

The Midstream segment faced challenges in Q1 2025, with normalized EBITDA declining 20% year-over-year to $197 million. This decrease was primarily attributed to lower margins in global exports despite higher volumes, increased operating expenses, and the absence of one-time gains that benefited Q1 2024 results, including a gain on ARO settlement at Alton and a hedging gain.

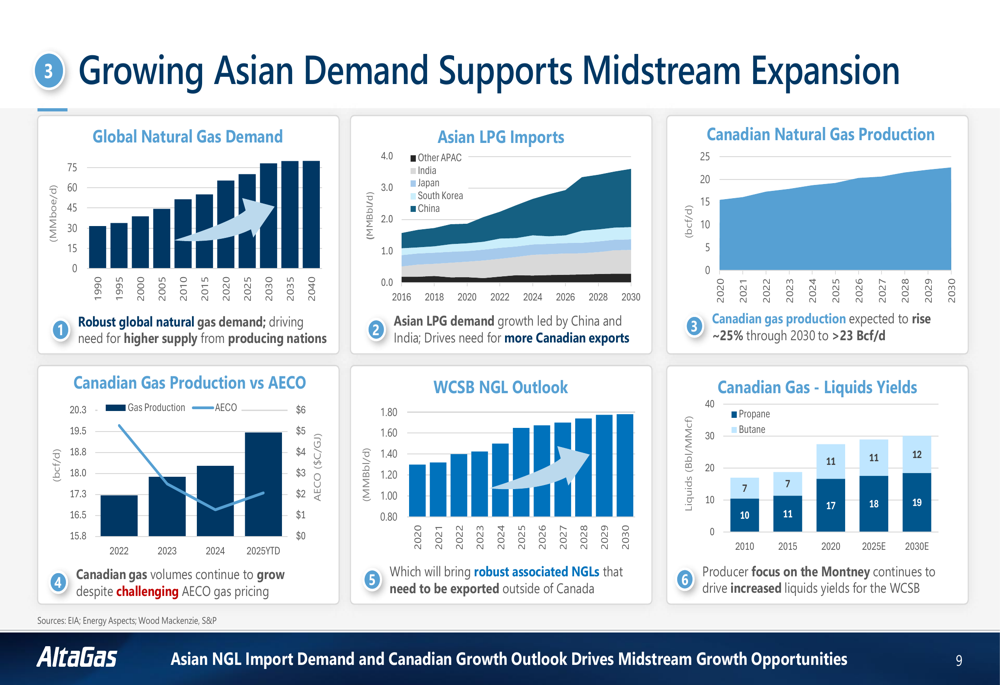

Despite these challenges, the company reported strong volume growth in its Montney gathering and processing operations, with volumes up 16% year-over-year. The company’s global exports platform and strategic infrastructure continue to drive volume growth, supported by increasing Asian demand for LPG.

The following chart illustrates the growing Asian demand that supports AltaGas’s midstream expansion:

Strategic Initiatives and Growth Projects

AltaGas continues to advance its key growth projects, including REEF and Pipestone II, both of which are reported to be on budget and on schedule. For the REEF project, approximately 60% of project costs are committed or incurred to date, with earthworks complete for overburden removal and over 70% complete for rock blasting. The company has achieved its base tolling target for the project.

The Pipestone II project is 76% complete, with facility construction progressing well. The company noted that 100% of the project is contracted under long-term take-or-pay agreements with marquee producers.

AltaGas’s 2025 business plan remains focused on five key strategic priorities:

1. Optimizing assets for maximum returns

2. Active de-risking through long-term commercial contracting and systematic hedging

3. Balance sheet deleveraging

4. Advancing key growth projects

5. Disciplined capital allocation

Financial Outlook and Guidance

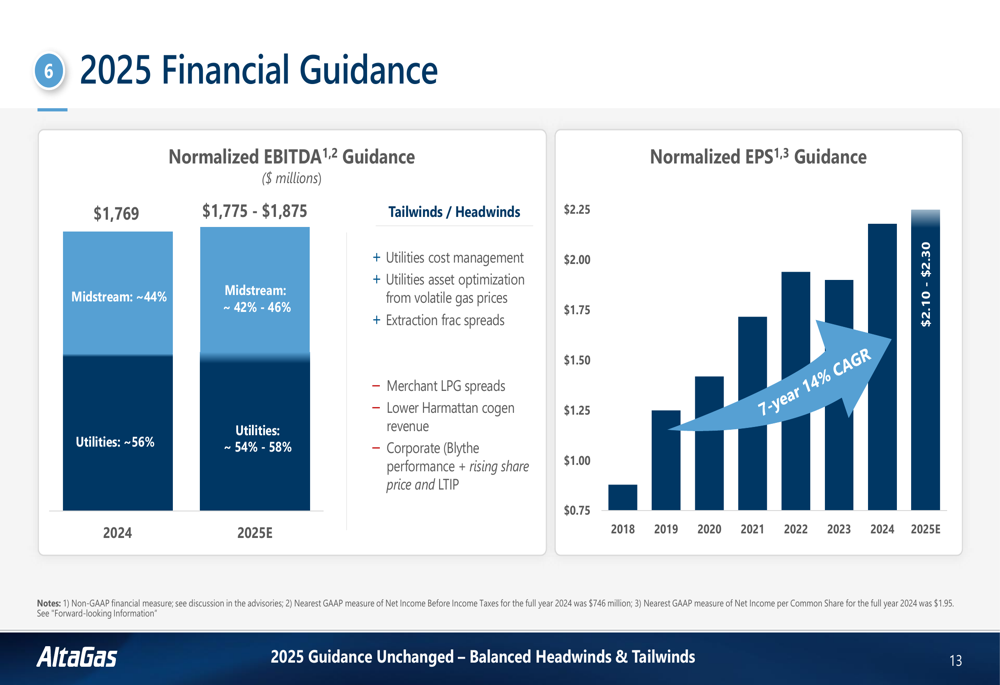

For 2025, AltaGas has provided normalized EBITDA guidance of $1,775-$1,875 million, compared to $1,769 million in 2024. Normalized EPS is expected to be in the range of $2.10-$2.30, representing a 7-year compound annual growth rate of 14% since 2018.

The following chart illustrates AltaGas’s 2025 financial guidance:

The company’s 2025 capital expenditure budget is set at $1.4 billion, with 51% allocated to Utilities, 45% to Midstream, and 4% to Corporate/Other. The largest capital outlays include REEF, Pipestone II, Utilities ARP, and system betterment.

AltaGas continues to make progress on its deleveraging objectives, reducing adjusted net debt by approximately $270 million in Q1 2025. The company’s current leverage ratio stands at 4.84x (including 50% debt treatment for preferred shares and hybrids), with a medium to long-term target of 4.65x.

Forward-Looking Statements

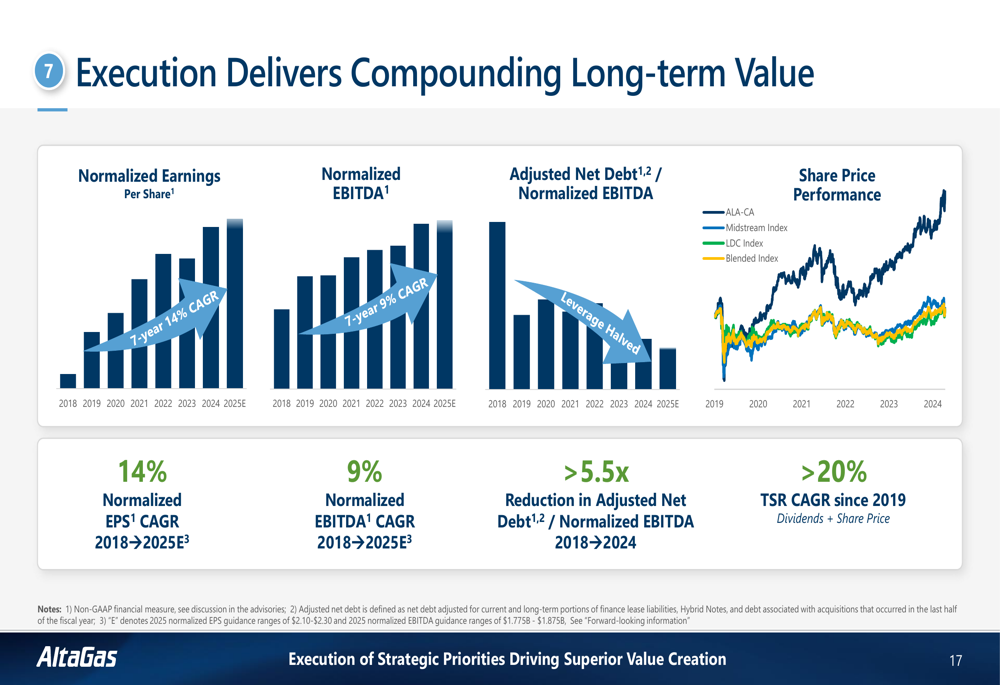

AltaGas’s long-term strategy remains focused on creating a low-risk energy infrastructure platform that provides stable and growing earnings and cash flows. The company emphasizes its diversified platform, visible growth opportunities, and disciplined capital allocation approach as key elements of its value proposition.

As shown in the following chart, AltaGas’s execution has delivered compounding long-term value for shareholders:

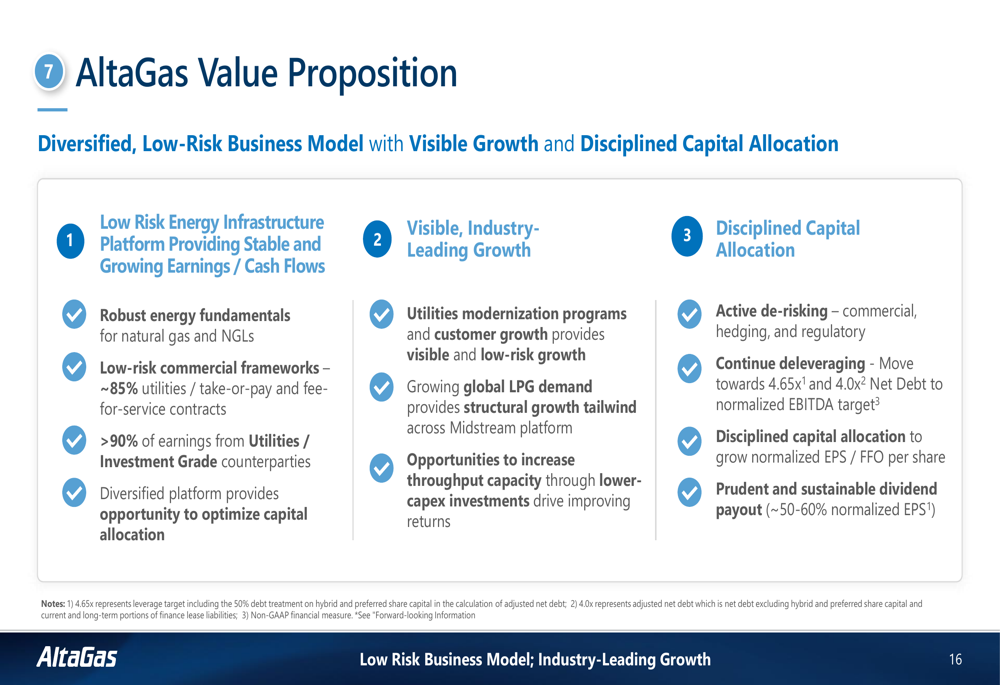

The company’s value proposition is built on three main pillars:

1. A low-risk energy infrastructure platform providing stable and growing earnings/cash flows

2. Visible, industry-leading growth

3. Disciplined capital allocation

The following slide details AltaGas’s value proposition:

Looking ahead, AltaGas is well-positioned to benefit from robust energy fundamentals for natural gas and NGLs, with approximately 85% of its earnings coming from utilities, take-or-pay, and fee-for-service contracts. The company’s continued focus on deleveraging, disciplined capital allocation, and prudent dividend policy (with a payout ratio of approximately 50-60% of normalized EPS) should support sustainable long-term value creation for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.