Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

AltaGas Ltd . (TSX:ALA) presented its second-quarter 2025 financial results on August 1, showcasing strong operational performance across its diversified infrastructure platform. The company reported significant year-over-year growth in normalized EBITDA and earnings per share, despite falling short of revenue expectations. AltaGas shares rose 0.82% to $40.91 following the announcement, reflecting investor confidence in the company’s execution strategy and growth trajectory.

The results come amid a favorable macro environment for AltaGas’s business segments, with Asian LPG demand projected to increase 30% from 2025-2030 and North American utilities facing strong demand for modernization investments. The company continues to leverage its strategic position in the Montney formation, one of North America’s most economically competitive natural gas plays.

Quarterly Performance Highlights

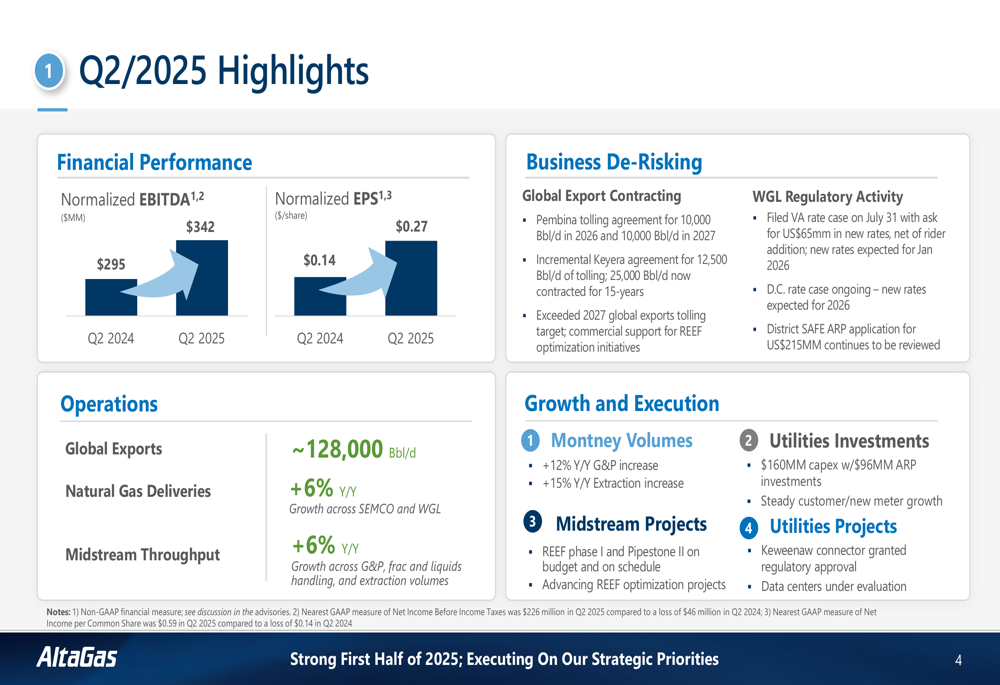

AltaGas reported normalized EBITDA of $342 million for Q2 2025, a 16% increase from $295 million in the same period last year. Normalized earnings per share nearly doubled to $0.27, up from $0.14 in Q2 2024, significantly exceeding analyst expectations of $0.24.

The strong performance was driven by growth across both business segments, with Midstream EBITDA increasing 23% year-over-year and Utilities EBITDA rising 10%. However, the company’s revenue of $2.84 billion fell short of the forecasted $2.97 billion by 4.38%.

As shown in the following quarterly highlights:

Key operational metrics showed positive momentum across the business. Global exports reached approximately 128,000 Bbl/d, while natural gas deliveries and midstream throughput both increased 6% year-over-year. Montney volumes showed particularly strong growth, up 12% for gathering and processing and 15% for extraction compared to Q2 2024.

Strategic Initiatives & Project Updates

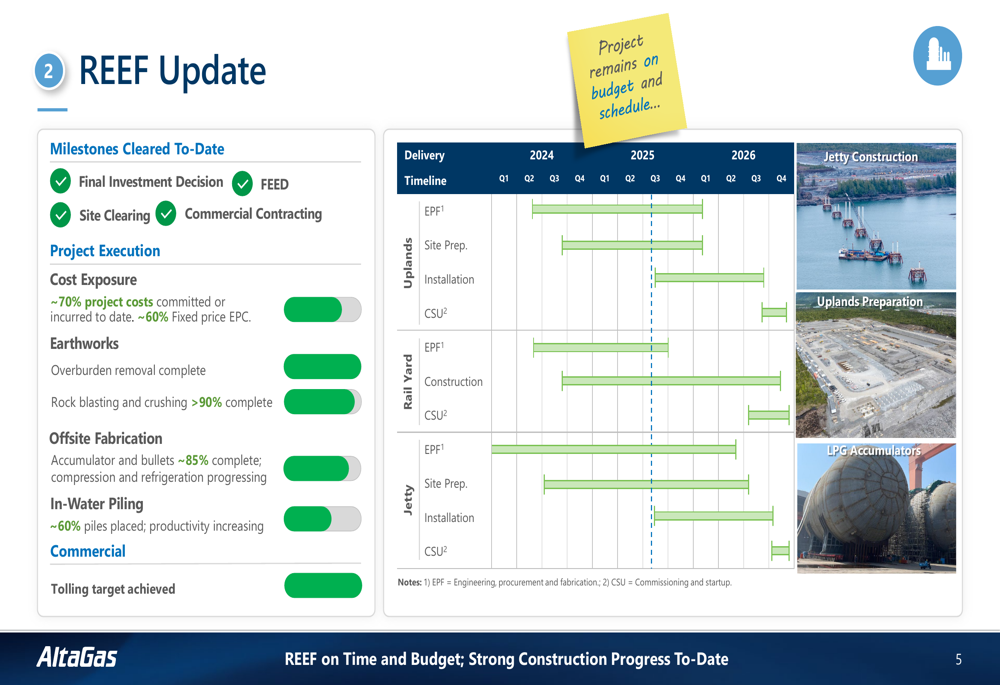

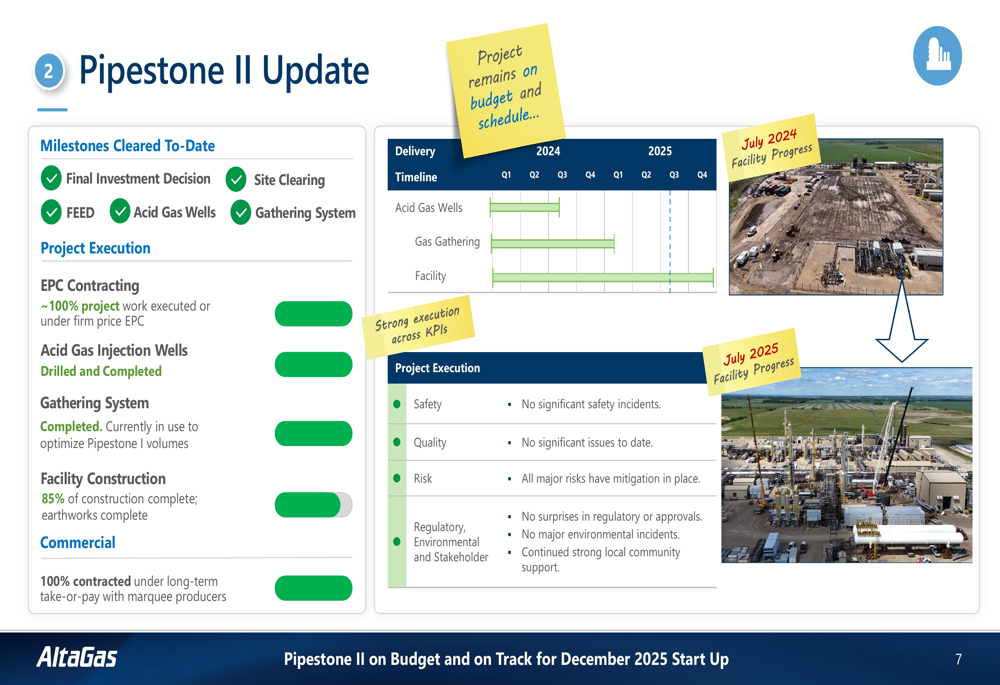

AltaGas continues to make significant progress on its two major growth projects: the Ridley Export Expansion Facility (REEF) and Pipestone II. These projects are critical components of the company’s strategy to expand its midstream capabilities and capitalize on growing global demand for LPG.

The REEF project, which will enhance AltaGas’s export capacity, is approximately 70% complete with costs committed or incurred. The company reported that about 60% of the EPC is fixed price, with earthworks, rock blasting, and crushing over 90% complete. The project remains on budget and on schedule.

The following image shows the current state of the REEF project:

The REEF facility is designed for phased growth, allowing AltaGas to add cost-effective capacity by leveraging common infrastructure. The company has already achieved its tolling target and outlined a clear path for future expansions.

Similarly, the Pipestone II project is 85% complete and remains on budget and schedule. The facility construction is well advanced, with earthworks complete and the project 100% contracted under long-term take-or-pay agreements with marquee producers.

The progress of Pipestone II is illustrated below:

These strategic investments position AltaGas to capitalize on the projected growth in global LPG demand, particularly in Asia. The company’s presentation highlighted that Asian LPG demand is expected to increase 30% from 2025-2030, providing a strong market for AltaGas’s expanded export capabilities.

Segment Performance Analysis

Midstream Segment

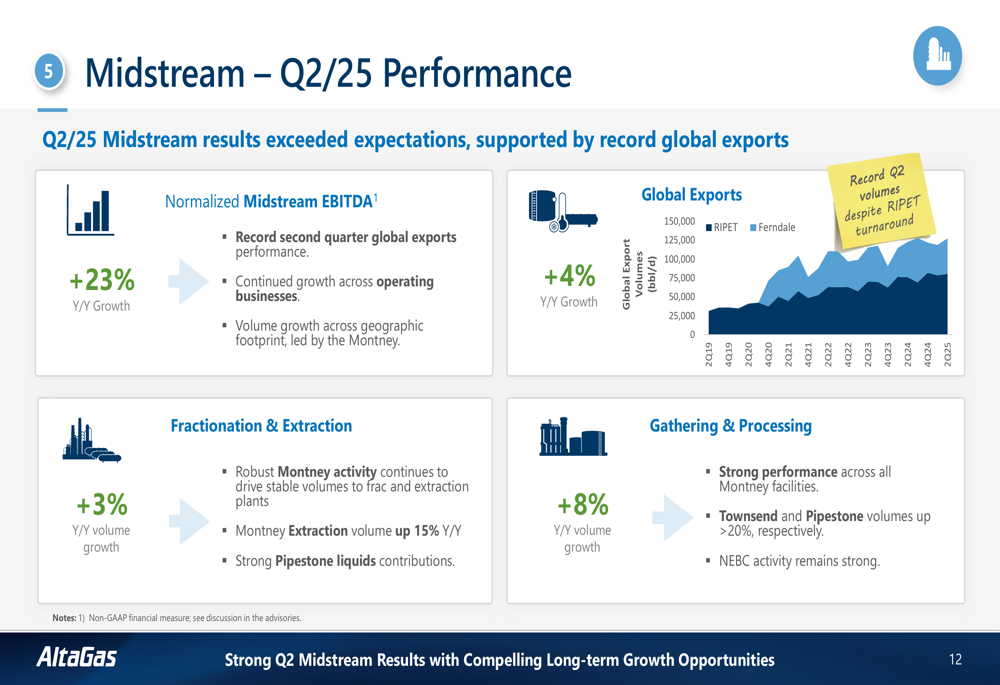

The Midstream segment delivered exceptional results in Q2 2025, with normalized EBITDA increasing 23% year-over-year. This performance was driven by record second-quarter global exports, continued growth across operating businesses, and volume growth led by the Montney formation.

The following chart illustrates the Midstream segment’s performance:

Global exports increased 4% year-over-year, while fractionation and extraction volume growth rose 3%. Gathering and processing volumes showed even stronger growth at 8% year-over-year, reflecting robust activity across all Montney facilities.

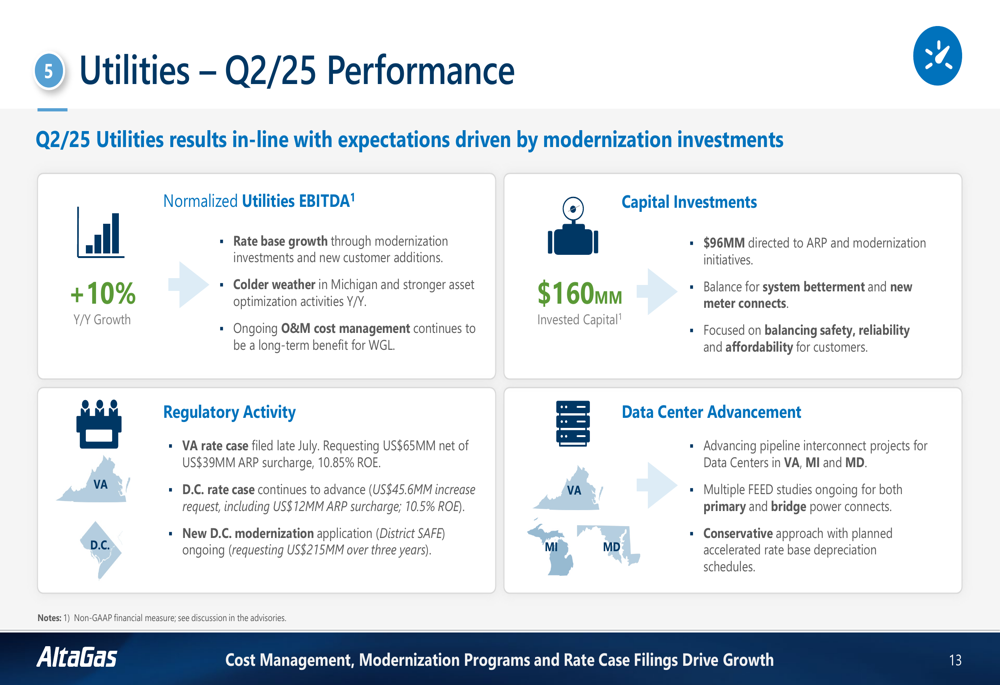

Utilities Segment

The Utilities segment also performed well, with normalized EBITDA increasing 10% year-over-year. This growth was attributed to rate base expansion, colder weather in Michigan, and ongoing operational and maintenance cost management.

Capital investments in the quarter included $160 million, with $96 million directed to accelerated replacement programs (ARP) and modernization initiatives. The segment continues to benefit from strong demand for natural gas infrastructure, particularly with the growing power needs of data centers.

As shown in the Utilities performance summary:

AltaGas highlighted that more than 30% of its utility system consists of vulnerable pipe over 50 years old, creating a substantial opportunity for continued investment in infrastructure modernization. Additionally, data center power demand is projected to more than double by 2029, further supporting the growth outlook for the Utilities segment.

Financial Outlook & Guidance

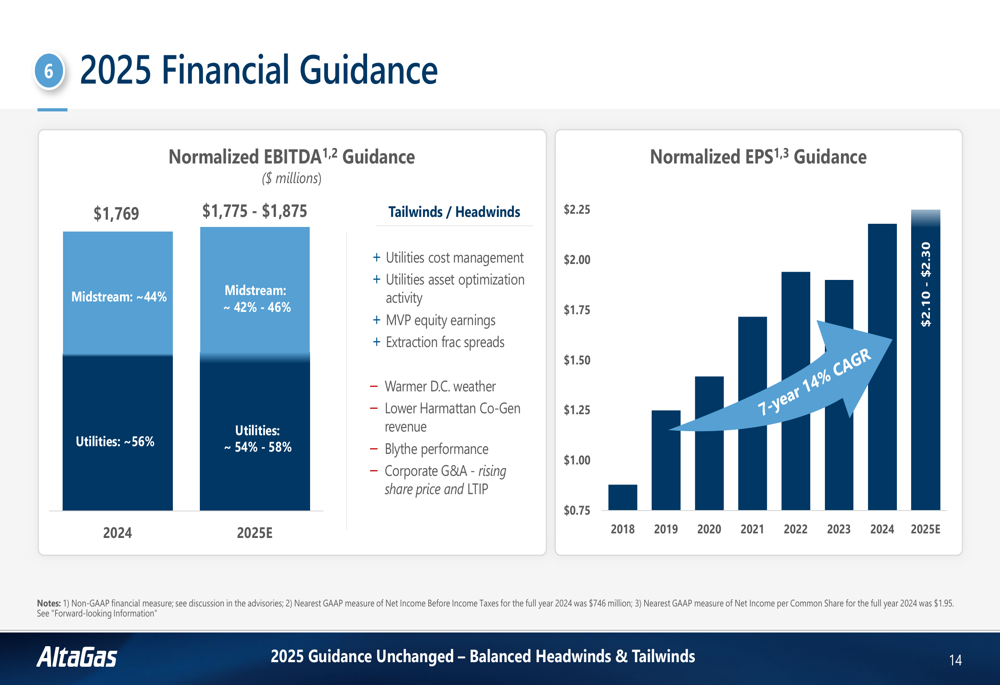

Looking ahead, AltaGas provided financial guidance for 2025, projecting normalized EBITDA of $1,775-$1,875 million and normalized EPS of $2.10-$2.30. The company expects the Midstream segment to contribute approximately 42-46% of normalized EBITDA, with Utilities accounting for 54-58%.

The financial guidance is presented in the following chart:

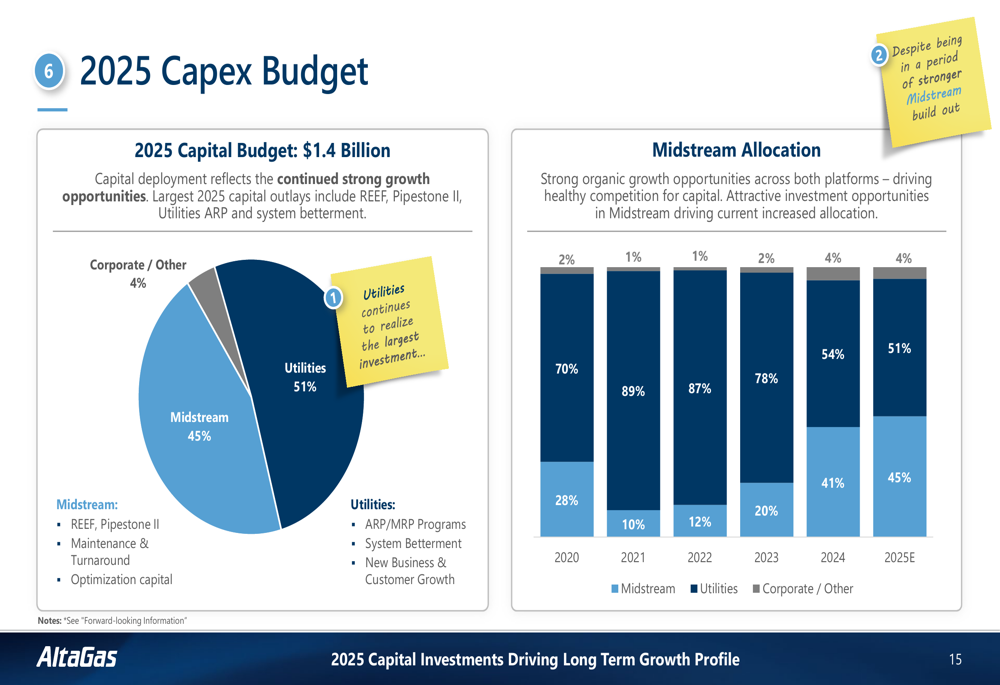

AltaGas has allocated a capital expenditure budget of $1.4 billion for 2025, with 51% directed to Midstream projects, 45% to Utilities, and 4% to Corporate/Other. This investment strategy supports the company’s focus on continued growth in both business segments.

The capital expenditure breakdown is illustrated below:

On the balance sheet front, AltaGas reported progress toward its medium to long-term leverage target of 4.65x, with a current ratio of 4.6x as of Q2 2025. The company reduced its adjusted net debt by $215 million compared to Q1 2025, demonstrating its commitment to deleveraging while investing in growth opportunities.

Forward-Looking Statements

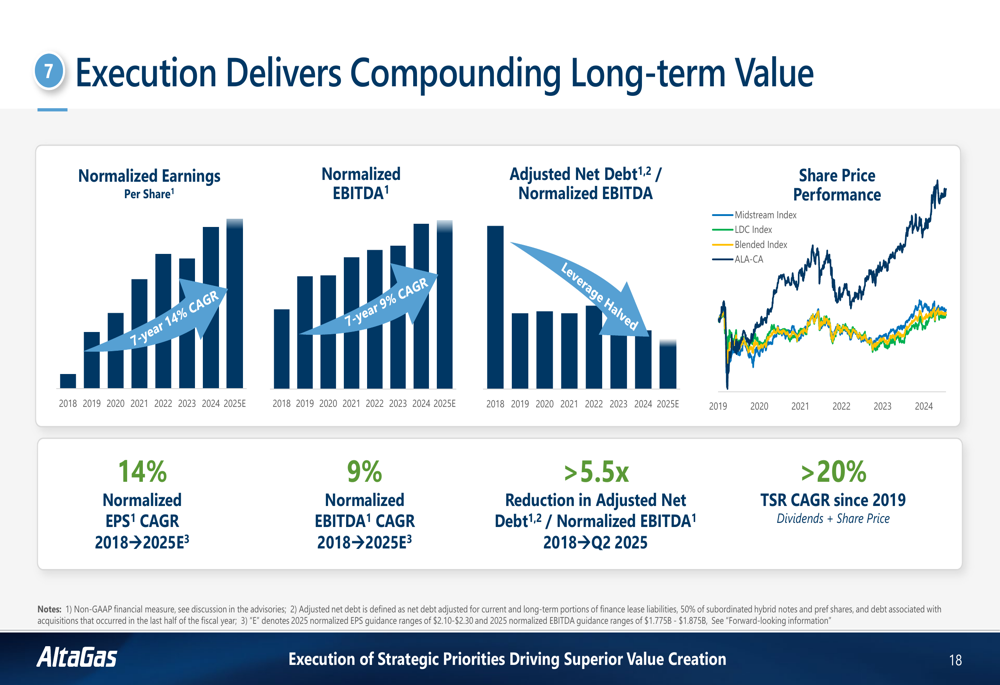

AltaGas’s long-term value proposition remains centered on its diversified, low-risk business model with visible growth opportunities and disciplined capital allocation. The company has demonstrated consistent execution, delivering compounding long-term value for shareholders.

Since 2018, AltaGas has achieved significant growth in normalized earnings per share and EBITDA while managing its debt levels. This performance has translated into strong total shareholder returns, with greater than 20% TSR growth.

The company’s execution and long-term value creation are illustrated in the following chart:

Looking forward, AltaGas is well-positioned to benefit from strong industry fundamentals in both its business segments. The growing demand for LPG in Asia provides a robust market for the company’s expanded export capabilities, while the need for utilities modernization in North America supports continued investment in its regulated business.

With its strategic projects progressing on schedule and strong operational performance across both segments, AltaGas appears well-equipped to deliver on its 2025 financial targets and continue its trajectory of long-term value creation for shareholders, despite the recent revenue shortfall.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.