Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Ambea AB (STO:AMBEA), a leading Nordic care provider, presented its first quarter 2025 results on May 6, showcasing a period of strategic expansion and solid financial performance. The company’s stock closed at 114.5 SEK but fell 3.76% during the presentation day, suggesting investors had mixed reactions to the results.

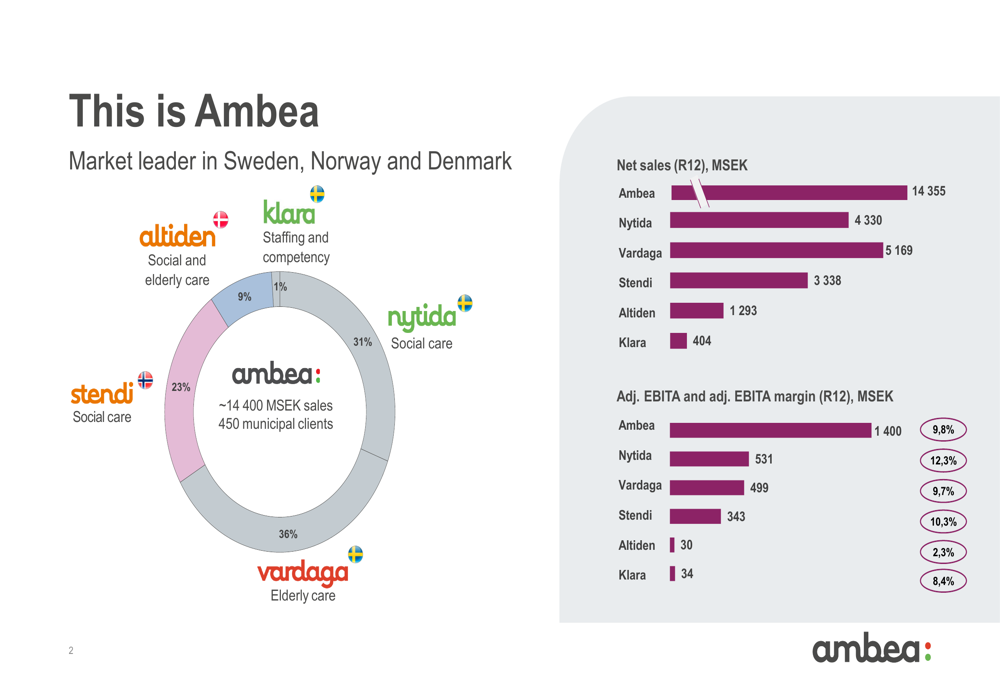

With approximately 14,400 MSEK in annual sales and 450 municipal clients across the Nordic region, Ambea maintains its position as a market leader in Sweden, Norway, and Denmark, with a fresh expansion into Finland. The company’s business is primarily divided across five segments: Vardaga (36% of sales), Nytida (31%), Stendi (23%), Altiden (9%), and Klara (1%).

As shown in the following company overview chart:

Quarterly Performance Highlights

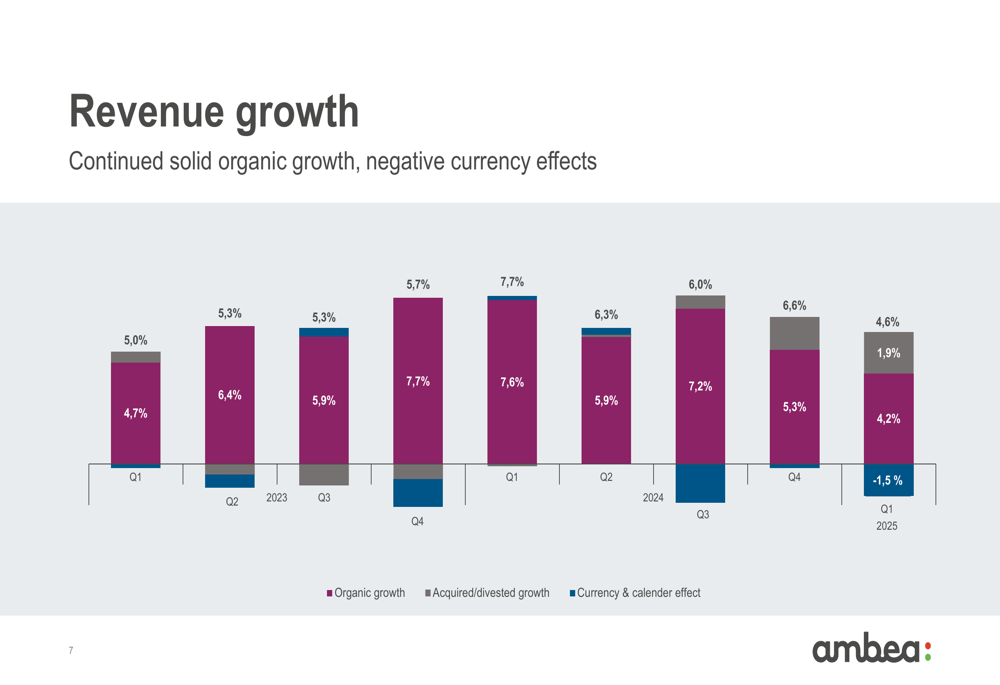

Ambea reported a 5% increase in net sales for Q1 2025, driven by 4.2% organic growth but partially offset by a 1.6% negative currency effect. The company’s adjusted EBITA increased by 10% year-over-year, with the margin improving to 8.4% from 8.0% in the same period last year.

The revenue growth trend shows consistent organic performance over the past nine quarters, though Q1 2025 saw the lowest organic growth rate since Q1 2023:

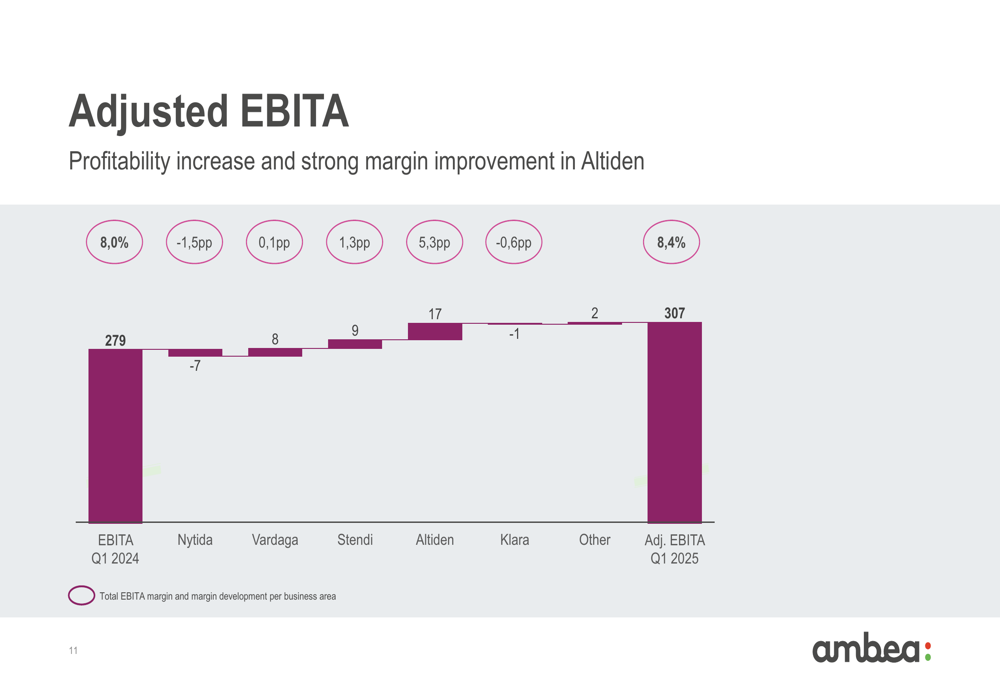

Adjusted EBITA reached 307 MSEK in Q1 2025, up from 279 MSEK in Q1 2024. This improvement was primarily driven by better performance in Stendi and a significant turnaround in Altiden, which offset weaker results in Nytida.

The following chart breaks down the EBITA contributions by business segment:

Segment Performance Analysis

Nytida, Ambea’s disability care segment in Sweden, delivered 8% sales growth to 1,122 MSEK, driven by acquisitions and newly opened units. However, EBITA decreased by 6% to 118 MSEK, with margins declining from 12.0% to 10.5%. After the quarter’s end, Nytida acquired parts of AvAsta, adding 62 MSEK in annual sales.

Vardaga, the elderly care segment in Sweden, increased sales by 7% to 1,313 MSEK with improved occupancy rates. EBITA grew by 8% to 111 MSEK, maintaining a stable margin of 8.5%. The segment also acquired parts of AvAsta after the quarter, adding 82 MSEK in annual sales.

Stendi, operating in Norway, saw a 2% decrease in net sales to 823 MSEK, though this represented a 1% increase in local currency. The segment’s EBITA improved by 15% to 68 MSEK, with margins expanding from 7.0% to 8.3%. The company noted it had terminated operations within elderly care in this segment.

Altiden, Ambea’s Danish segment, continued its impressive turnaround with a 6% increase in net sales to 333 MSEK and a shift to positive EBITA of 8 MSEK, compared to a loss of 9 MSEK in Q1 2024. This represents a significant margin improvement from -2.9% to 2.4%.

Klara, the staffing services segment, faced challenges with a 5% decline in net sales to 100 MSEK and an 11% decrease in EBITA to 8 MSEK, with margins falling from 8.6% to 8.0%. Management attributed this to a weak external market and noted that Klara has adjusted its cost base accordingly.

Strategic Expansion into Finland

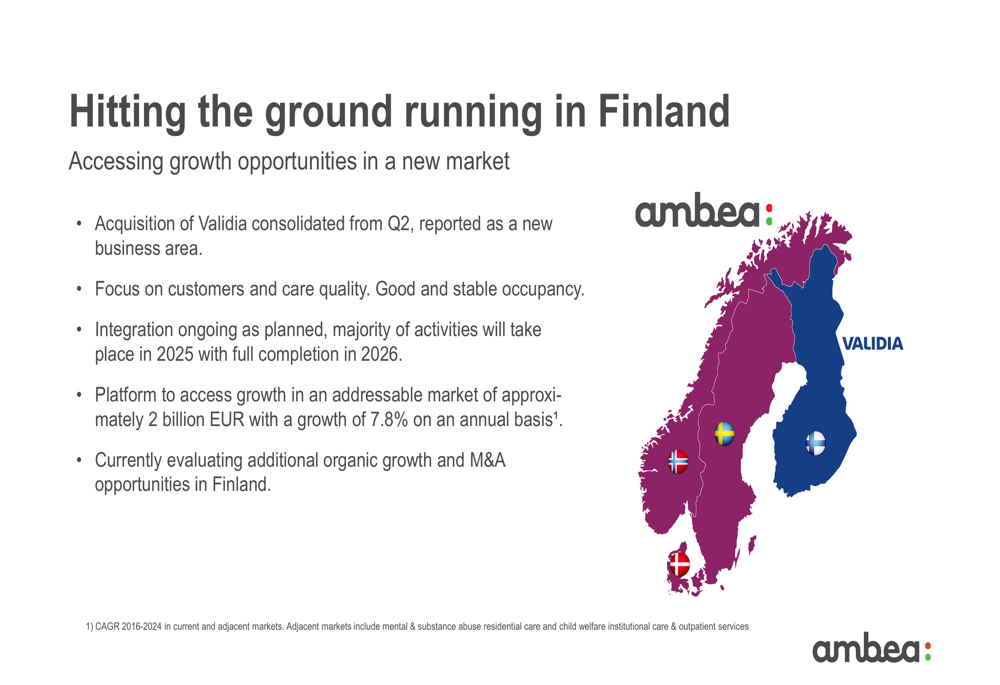

A major strategic development for Ambea is its entry into the Finnish market through the acquisition of Validia, which was completed on April 1, 2025. This expansion makes Ambea the only care provider with a strong presence in all four major Nordic countries.

The Finnish market represents approximately 2 billion EUR with a 7.8% annual growth rate (CAGR 2016-2024), offering significant opportunities for Ambea. The company plans to integrate Validia throughout 2025, with full completion expected in 2026.

As illustrated in the following geographical expansion overview:

This acquisition is part of Ambea’s broader M&A strategy, which has accelerated in 2025. The company’s acquired annual net sales have increased significantly, with 1,644 MSEK in acquisitions during 2025 compared to 267 MSEK in 2023.

Cash Flow and Capital Allocation

Ambea demonstrated strong cash flow generation, with operating cash flow of 425 MSEK in Q1 2025. While this represents a decrease from the 580 MSEK reported in Q1 2024, it shows an improvement compared to the previous two quarters.

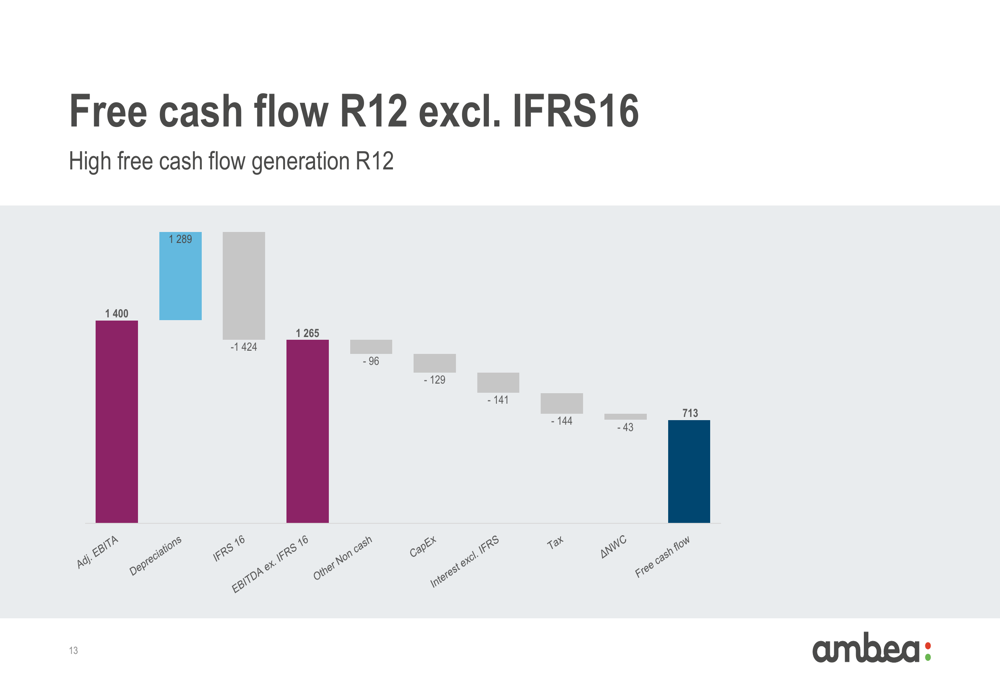

The company’s free cash flow (R12, excluding IFRS16) reached 713 MSEK, representing a 24.6% CAGR since Q1 2022. This strong cash generation is derived from various components as shown in the following breakdown:

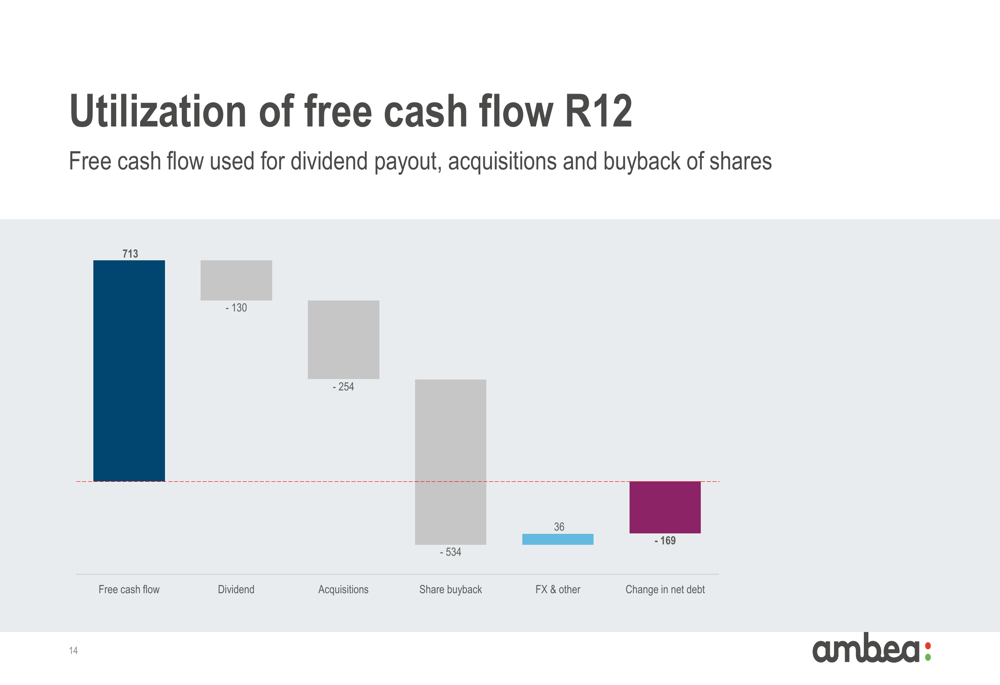

Ambea has allocated its free cash flow primarily to shareholder returns and growth initiatives. Over the trailing twelve months, the company distributed 130 MSEK in dividends, spent 254 MSEK on acquisitions, and allocated 534 MSEK to share buybacks, as illustrated below:

Forward-Looking Statements

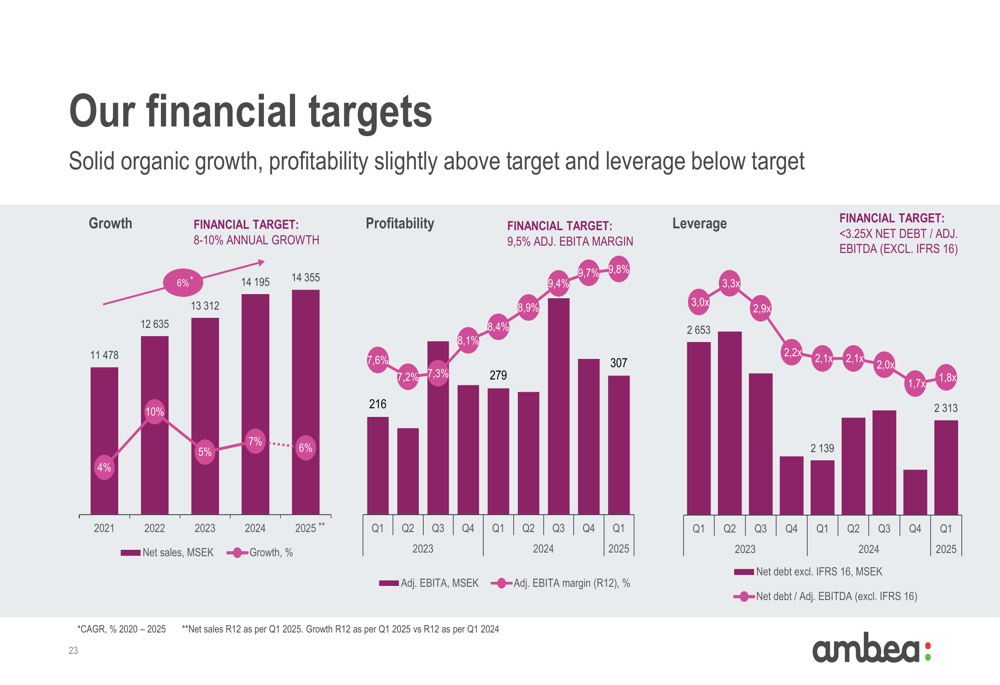

Ambea has set clear financial targets, aiming for 8-10% annual growth and a 9.5% adjusted EBITA margin in the medium term. The company also targets a leverage ratio (Net Debt/Adj. EBITDA excluding IFRS 16) of less than 3.25x.

The outlook for the remainder of 2025 includes:

- Integration of Validia in Finland

- Completion of additional acquisitions within Vardaga and Nytida (144 MSEK annual sales)

- Opening of new units across segments

- Further profitability improvements in Altiden

- Continued investments in quality and care time

As shown in the company’s financial targets overview:

CEO Mark Jensen expressed confidence in the company’s outlook, stating they remain "comfortable on both short, mid and long term outlook." However, investors should note potential challenges including margin pressure in Nytida, increased leverage following the Validia acquisition, and the impact of new Danish legislation on expansion plans.

With its expanded Nordic footprint and continued focus on both organic and acquired growth, Ambea appears well-positioned to capitalize on the increasing demand for care services driven by aging populations across the region, despite near-term market skepticism reflected in the stock’s recent performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.