IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

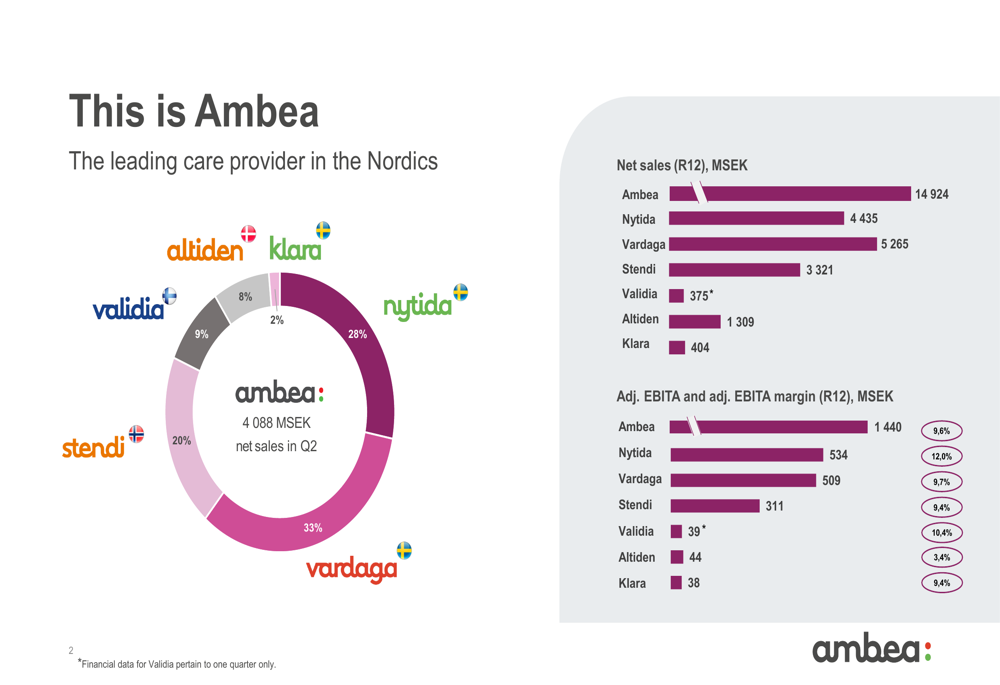

Ambea AB (STO:AMBEA), a leading Nordic care provider, presented its second quarter 2025 results on August 19, showing substantial growth primarily driven by strategic acquisitions. The company’s stock responded positively, rising 9.13% to 125.5 SEK following the presentation, continuing its impressive 75.7% gain over the past year.

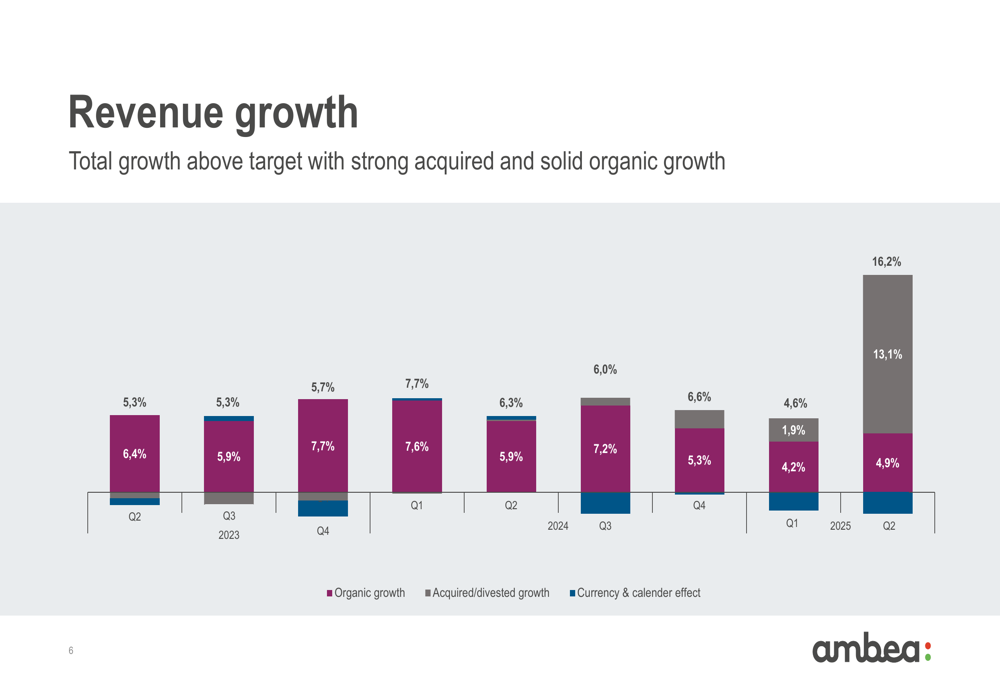

The healthcare services provider has significantly accelerated its growth trajectory compared to Q1 2025, when it reported just 5% revenue growth. This quarter’s 16% expansion demonstrates successful execution of Ambea’s acquisition strategy, particularly the completion of the Validia acquisition in Finland, which has added a substantial new revenue stream.

Quarterly Performance Highlights

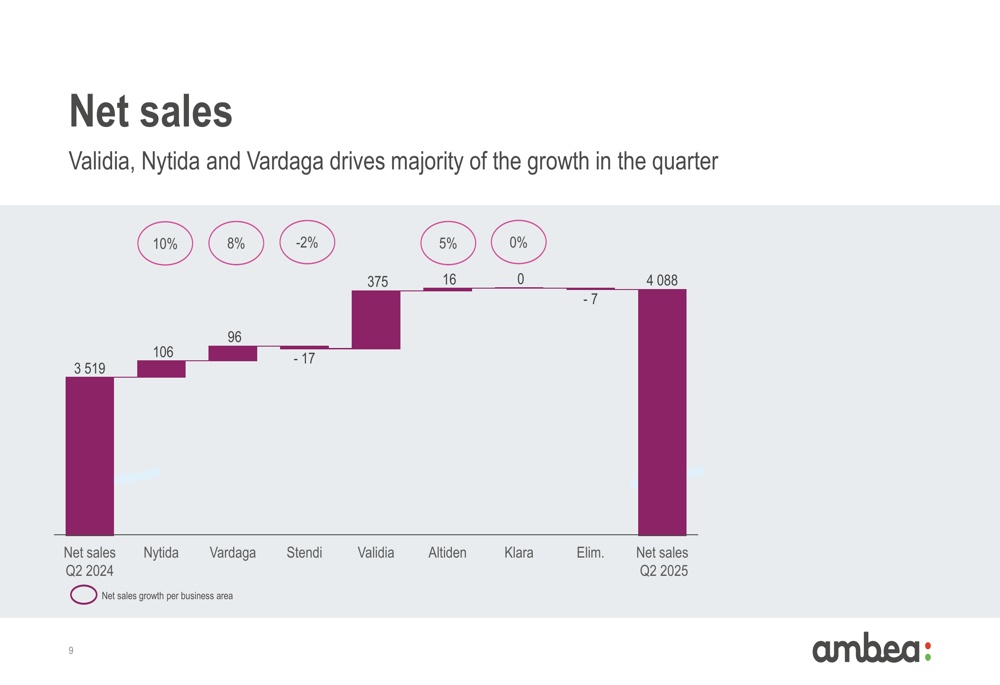

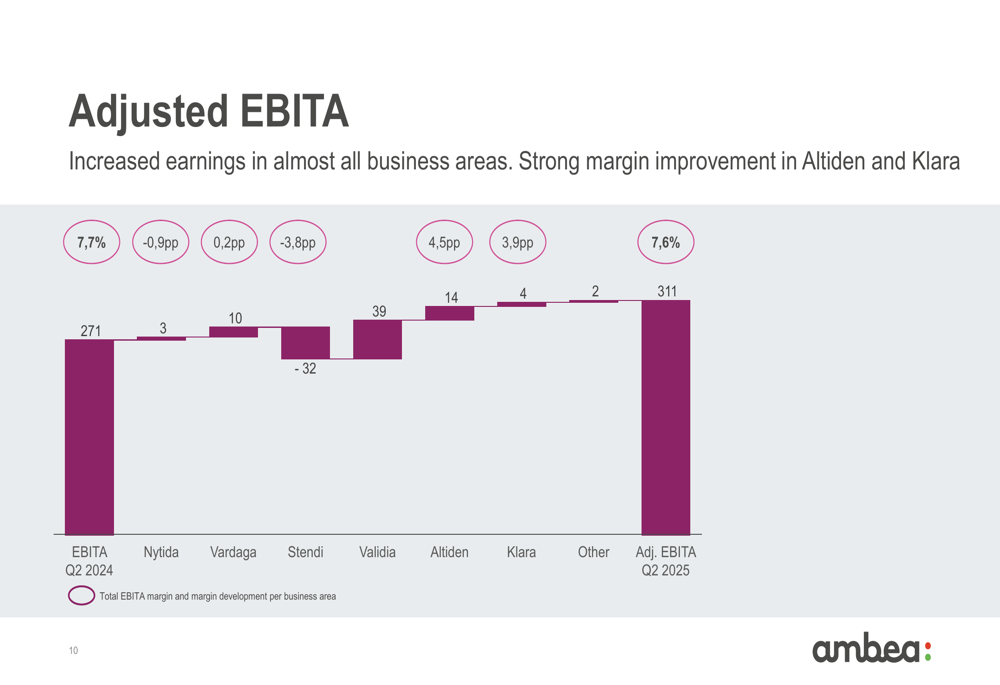

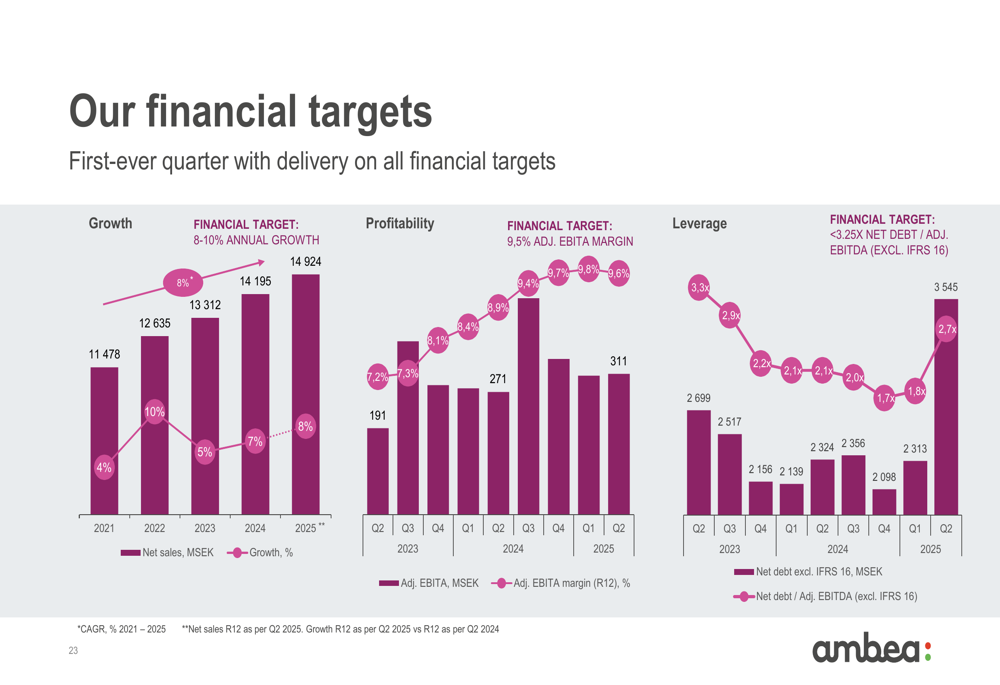

Ambea reported net sales of 4,088 MSEK for Q2 2025, representing a 16% increase compared to the same period last year. This growth was primarily driven by acquisitions (13%), with organic growth also making a solid contribution. Adjusted EBITA reached 311 MSEK, up 15% from 271 MSEK in Q2 2024, while the adjusted EBITA margin remained relatively stable at 7.6% compared to 7.7% in the previous year.

As shown in the following overview of Ambea’s business structure and financial performance:

The company’s adjusted earnings per share continued its strong upward trajectory, reaching 7.44 SEK on a trailing twelve-month basis, nearly doubling from 3.80 SEK in Q2 2023. This improvement reflects both organic growth and successful integration of acquisitions over the past two years.

The following chart illustrates this consistent growth in adjusted EPS:

Segment Analysis

Performance across Ambea’s business segments showed significant variation in Q2 2025. The newly acquired Validia business in Finland made an immediate positive impact, while established segments showed mixed results.

The following waterfall chart breaks down the net sales growth by business area:

Nytida, which provides disability care services, increased net sales by 10% to 1,154 MSEK, driven by acquisitions and new units. However, its EBITA margin declined by 0.9 percentage points to 11.0%, confirming the margin challenges mentioned in the Q1 2025 earnings call.

Vardaga, Ambea’s elderly care segment, delivered solid performance with 8% net sales growth to 1,358 MSEK and a 10% increase in EBITA to 115 MSEK. Its margin improved slightly to 8.5% from 8.3% last year, benefiting from higher occupancy rates and the AvAsta acquisition.

Stendi, operating in Norway, was the only segment to report declining sales (-2%) and experienced a significant drop in profitability, with EBITA falling to 29 MSEK from 61 MSEK and margin declining to 3.5% from 7.3%. The company attributed this to seasonal variations.

The following chart shows the changes in adjusted EBITA across all business segments:

Validia, the new Finnish business, contributed 375 MSEK in net sales with an impressive EBITA margin of 10.4%, immediately becoming a significant contributor to group profitability.

Altiden, operating in Denmark, showed continued improvement with 5% sales growth and a positive EBITA of 1 MSEK, compared to a loss of 13 MSEK in Q2 2024. This turnaround reflects the success of restructuring efforts in this previously challenging segment.

Strategic Growth Initiatives

Ambea continues to pursue growth through both acquisitions and organic expansion. The company completed two significant acquisitions in Q2 2025: Validia in Finland (April 1) and parts of AvAsta (May 5), the latter adding annual sales of 144 MSEK to Vardaga and Nytida operations.

The following chart illustrates Ambea’s consistent growth through acquisitions:

For organic growth, Ambea has a pipeline of 1,360 new places planned, with significant capacity increases across its business areas. Key developments include Nytida signing a contract for an assisted living facility with six new places, Vardaga increasing capacity by 30 beds at a nursing home in Stockholm, and Validia contracting for two assisted living facilities with 78 new beds.

Financial Position and Outlook

Ambea maintains strong cash generation, with operating cash flow increasing to 401 MSEK in Q2 2025 from 327 MSEK in Q2 2023. Cash conversion improved to 89.8% from 85.3% over the same period, providing financial flexibility for continued investments and acquisitions.

The company’s performance against its financial targets shows solid progress, as illustrated in the following chart:

Looking ahead, Ambea expects continued solid growth driven by both acquisitions and organic expansion. The company anticipates that further organic pipeline expansion will add future capacity, while adjusted operations will support margin stabilization.

CEO Mark Jensen emphasized the company’s investment case, highlighting the growing need for care services, Ambea’s strong market position across the Nordic region, high-quality services, substantial growth potential, balanced risk profile, and strong cash flow with stable dividends.

The following slide summarizes why investors should consider Ambea:

With its comprehensive Nordic platform and diversified business model, Ambea appears well-positioned to capitalize on the growing demand for care services across the region, despite some challenges in individual segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.