Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

Advanced Micro Devices (NASDAQ:AMD) reported its second quarter 2025 financial results on August 5, 2025, showcasing strong revenue growth despite significant inventory charges related to U.S. export restrictions. The chipmaker’s stock traded up 0.37% in after-hours trading to $177.43, following a 1.4% decline during regular trading hours.

AMD’s presentation highlighted the company’s continued momentum in high-performance computing markets, with particular strength in client processors and gaming products. However, the results also revealed challenges in the data center segment, where export restrictions impacted profitability.

Quarterly Performance Highlights

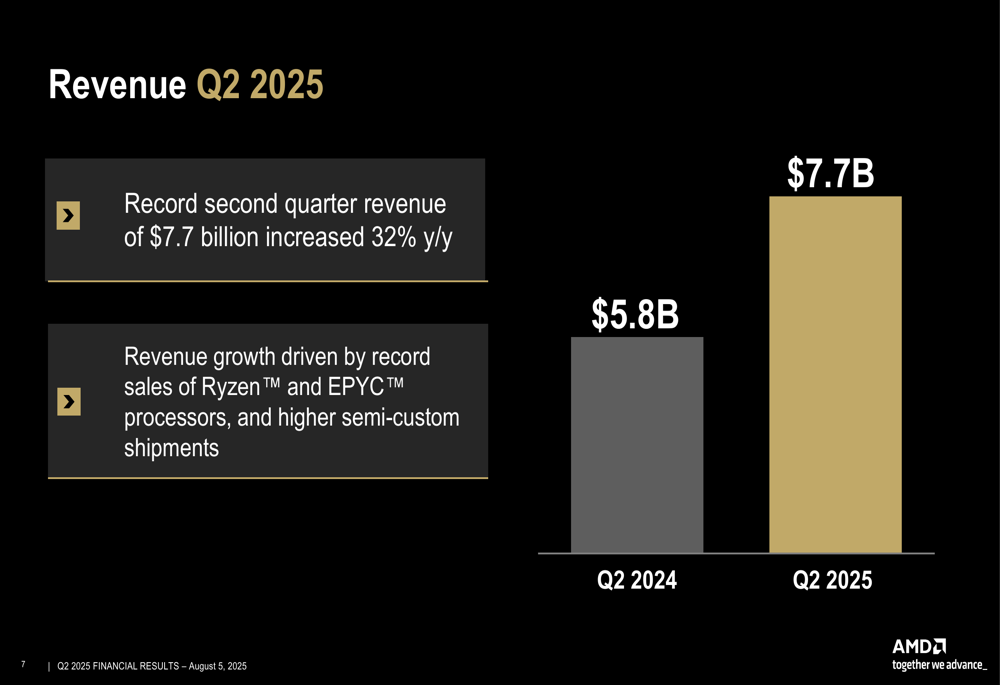

AMD reported record revenue of $7.7 billion for Q2 2025, representing a 32% year-over-year increase from $5.8 billion in Q2 2024. This growth was primarily driven by record sales of Ryzen and EPYC processors, along with higher semi-custom shipments.

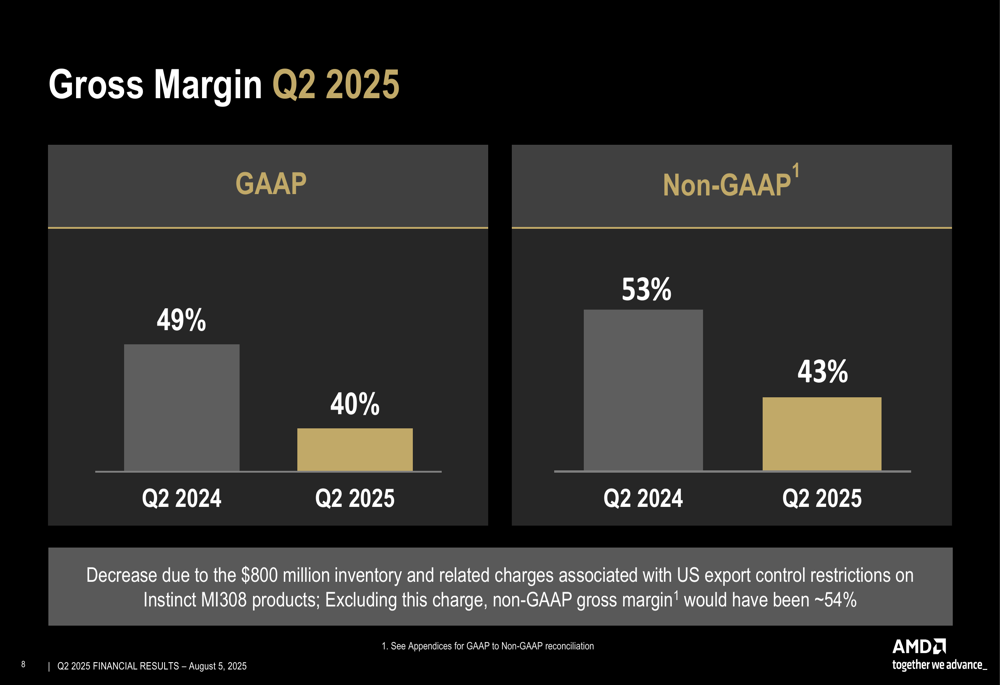

Despite the strong top-line performance, AMD’s profitability was significantly impacted by inventory charges. The company reported GAAP gross margin of 40%, down from 49% in the year-ago quarter, while non-GAAP gross margin fell to 43% from 53%. AMD attributed this decline to $800 million in inventory and related charges associated with U.S. export control restrictions. Excluding these charges, the company noted its non-GAAP gross margin would have been approximately 54%.

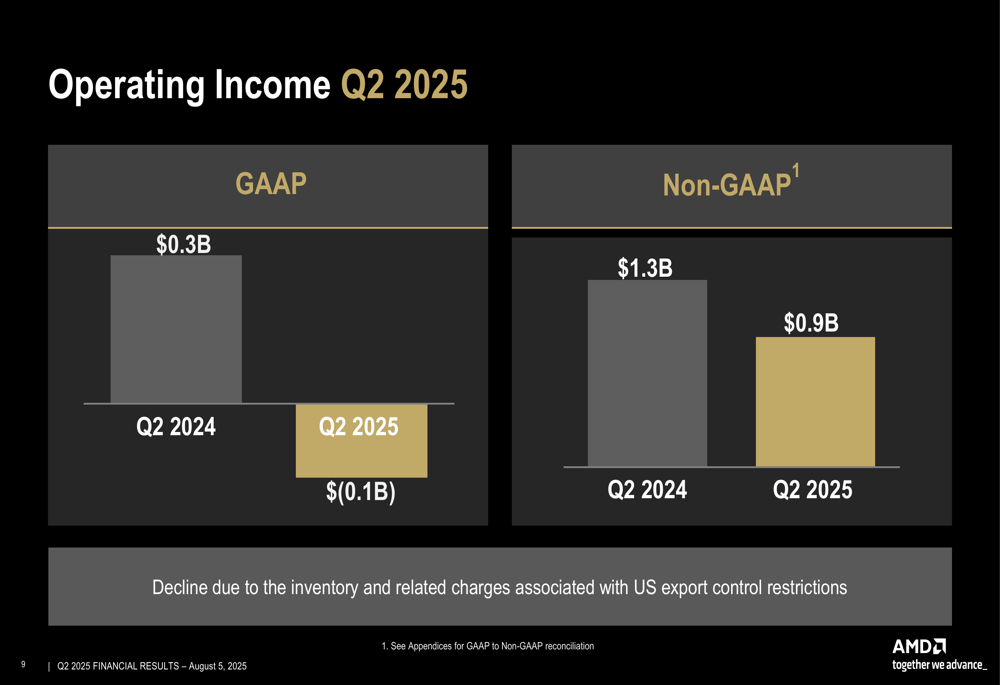

The inventory charges also affected operating income, with GAAP operating income showing a loss of $134 million compared to a profit of $265 million in Q2 2024. On a non-GAAP basis, operating income declined 29% year-over-year to $897 million.

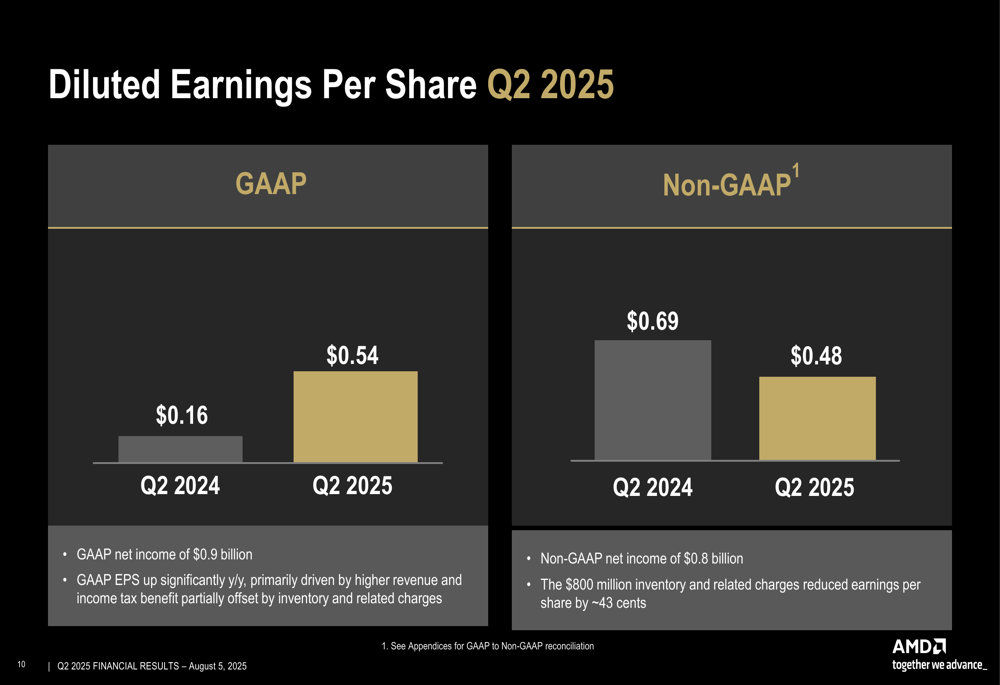

Despite these challenges, AMD reported GAAP diluted earnings per share of $0.54, up significantly from $0.16 in the year-ago period. However, non-GAAP EPS declined 30% to $0.48 from $0.69 in Q2 2024, with the inventory charge reducing non-GAAP EPS by approximately 43 cents.

Segment Analysis

AMD’s performance varied significantly across its three business segments, revealing both strengths and challenges in different markets.

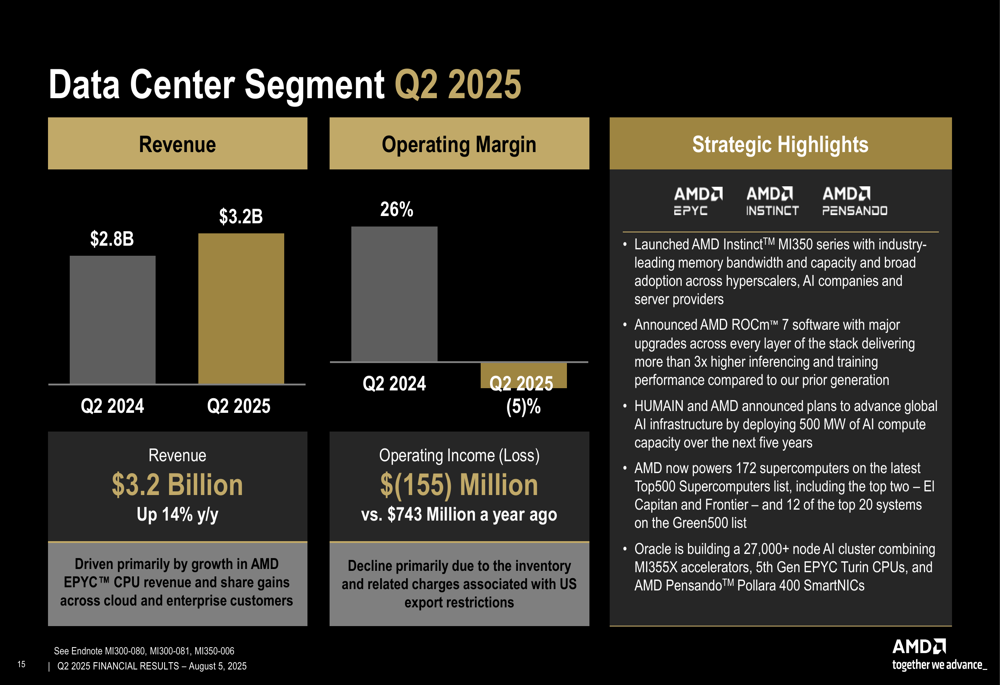

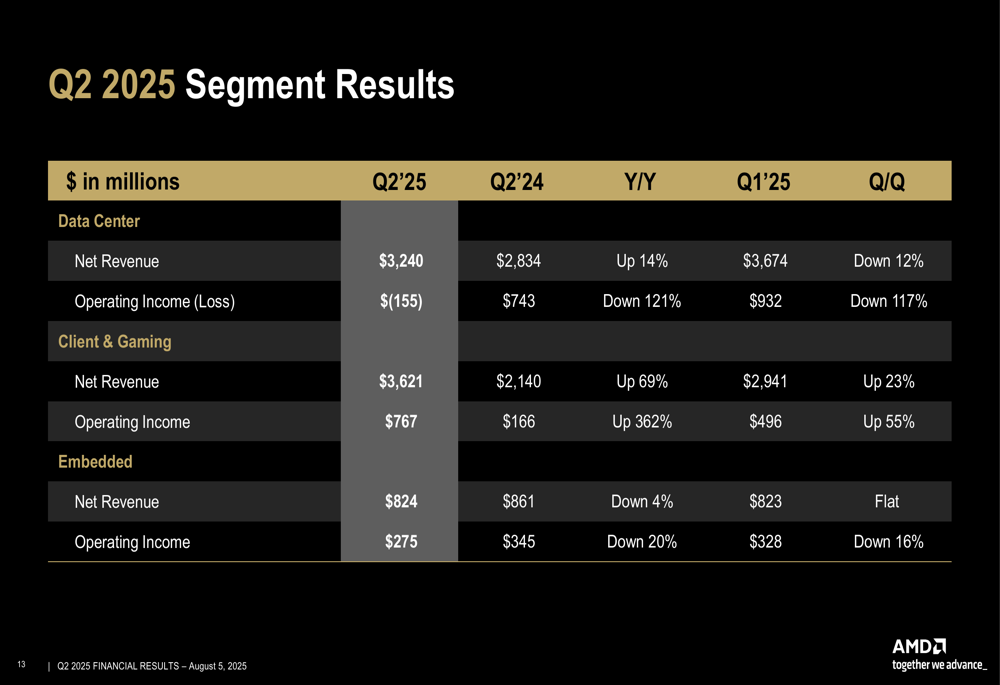

The Data Center segment generated $3.24 billion in revenue, up 14% year-over-year, but reported an operating loss of $155 million compared to an operating profit of $740 million in Q2 2024. This segment was most directly impacted by the export restrictions and inventory charges.

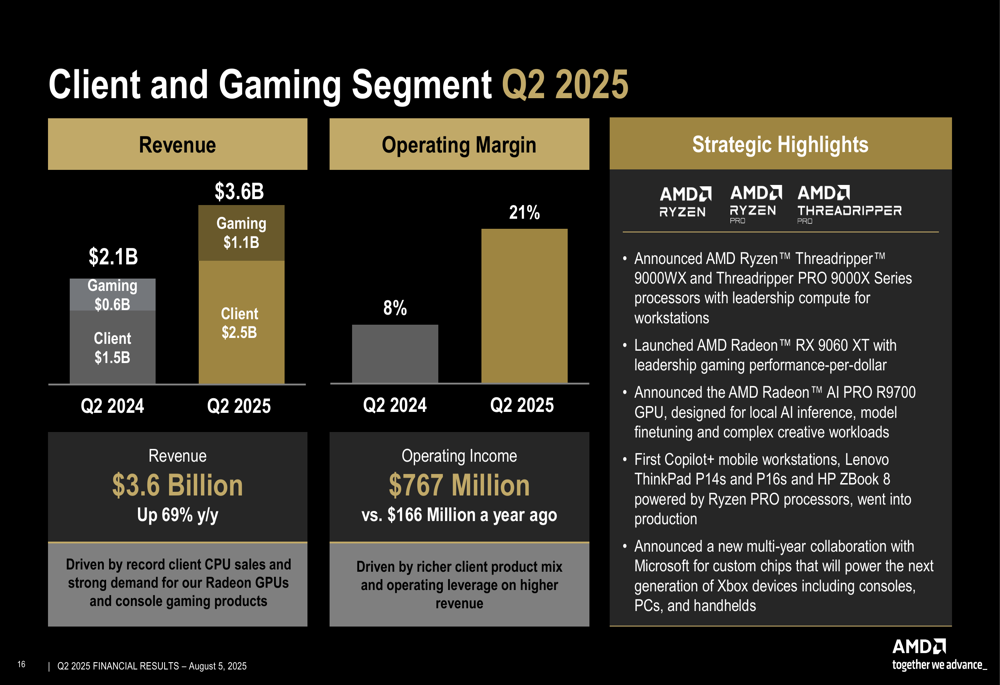

In contrast, the Client & Gaming segment delivered exceptional results with revenue of $3.62 billion, surging 69% year-over-year. Operating income for this segment increased dramatically by 362% to $767 million, driven by record client CPU sales and strong demand for Radeon GPUs.

The Embedded segment saw a modest 4% year-over-year decline in revenue to $824 million, with operating income falling 20% to $275 million. Despite this, the segment maintained a healthy 33% operating margin.

Strategic Initiatives

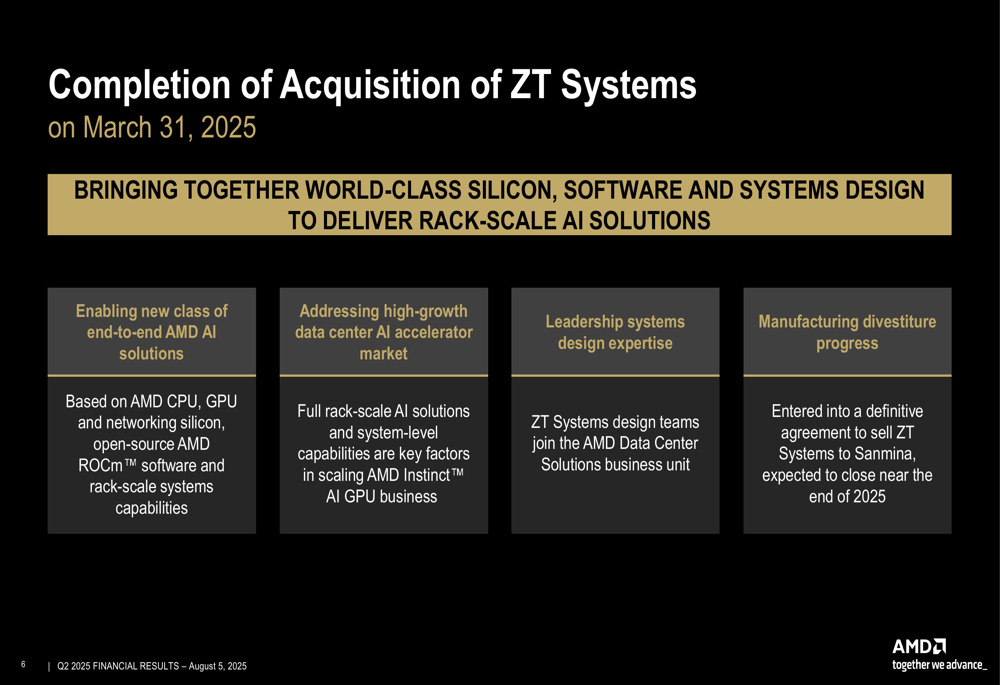

AMD highlighted several strategic developments during the quarter, including the completion of its acquisition of ZT Systems on March 31, 2025. This acquisition is expected to enable new end-to-end AI solutions and address the high-growth data center AI accelerator market while adding leadership systems design expertise to AMD’s portfolio.

In the data center space, AMD launched the Instinct MI350 series accelerators and announced AMD ROCm 7 software to strengthen its AI computing capabilities. The company also noted that Oracle (NYSE:ORCL) is building a 27,000+ node AI cluster using AMD technology, demonstrating growing adoption of its data center solutions.

For client computing, AMD introduced the Ryzen Threadripper 9000WX and Threadripper PRO 9000X series processors, along with the Radeon RX 9060 XT GPU. The company also launched its first Copilot+ mobile workstations and announced a multi-year collaboration with Microsoft (NASDAQ:MSFT).

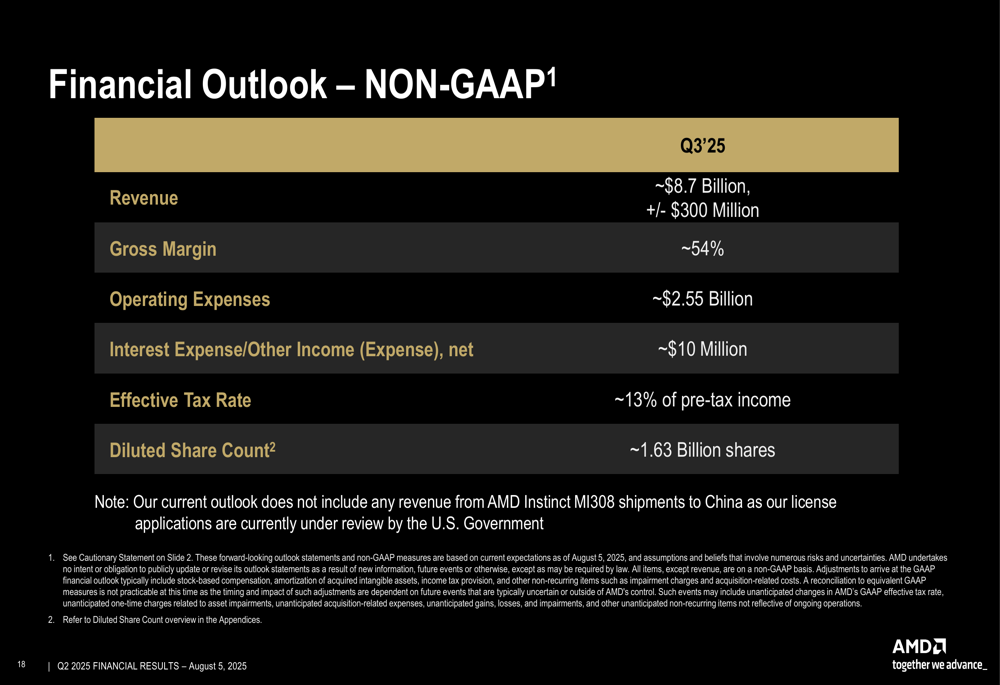

Financial Outlook

Looking ahead to the third quarter of 2025, AMD provided a positive outlook with projected revenue of approximately $8.7 billion (±$300 million), representing continued growth. The company expects non-GAAP gross margin to improve to approximately 54% and anticipates operating expenses of around $2.55 billion.

Notably, AMD’s Q3 outlook does not include any revenue from AMD Instinct MI308 shipments to China, as license applications are currently under review. This suggests potential upside if these restrictions are eased.

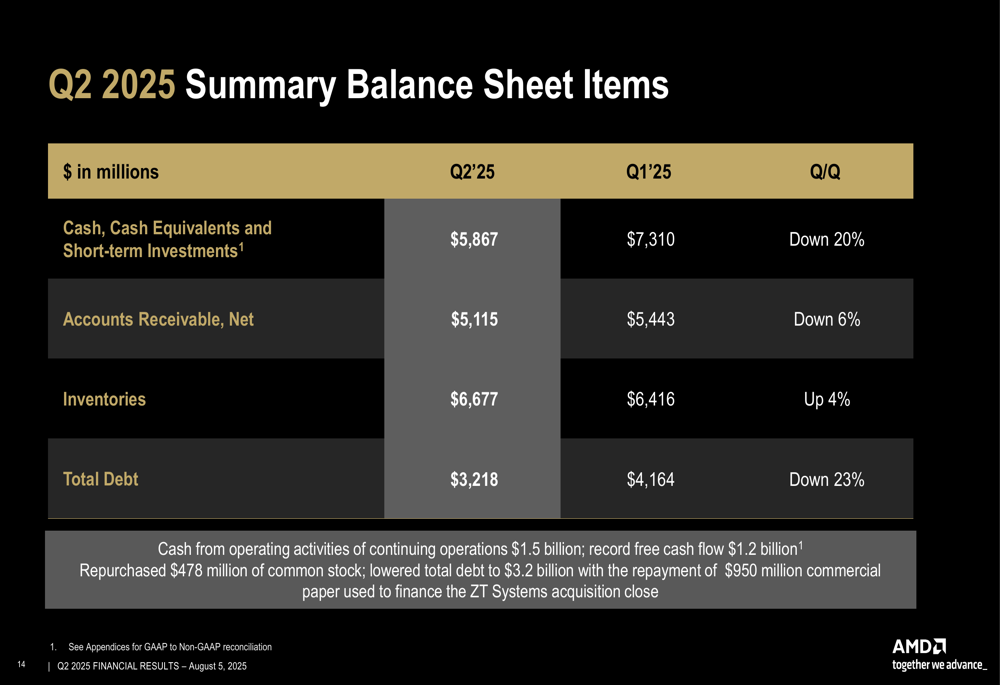

From a balance sheet perspective, AMD reported $5.87 billion in cash and short-term investments, down 20% quarter-over-quarter. The company generated $1.5 billion in operating cash flow and $1.2 billion in free cash flow during Q2, while reducing its total debt by 23% to $3.22 billion and repurchasing $478 million of common stock.

AMD’s Q2 results demonstrate the company’s ability to drive significant revenue growth even while navigating regulatory challenges. With the Client & Gaming segment showing exceptional strength and strategic investments in AI and data center technologies continuing, AMD appears positioned to maintain its growth trajectory, provided it can successfully address the challenges in its Data Center segment related to export restrictions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.