Bubble Wrap maker Sealed Air surges on report of buyout talks

Amdocs Ltd (NASDAQ:DOX) presented its fiscal second-quarter 2025 earnings on May 7, showcasing solid financial performance with revenue and earnings exceeding guidance. Despite the positive results, the stock declined 3.45% in after-hours trading to $86.26, reflecting potential investor concerns about future growth prospects.

Quarterly Performance Highlights

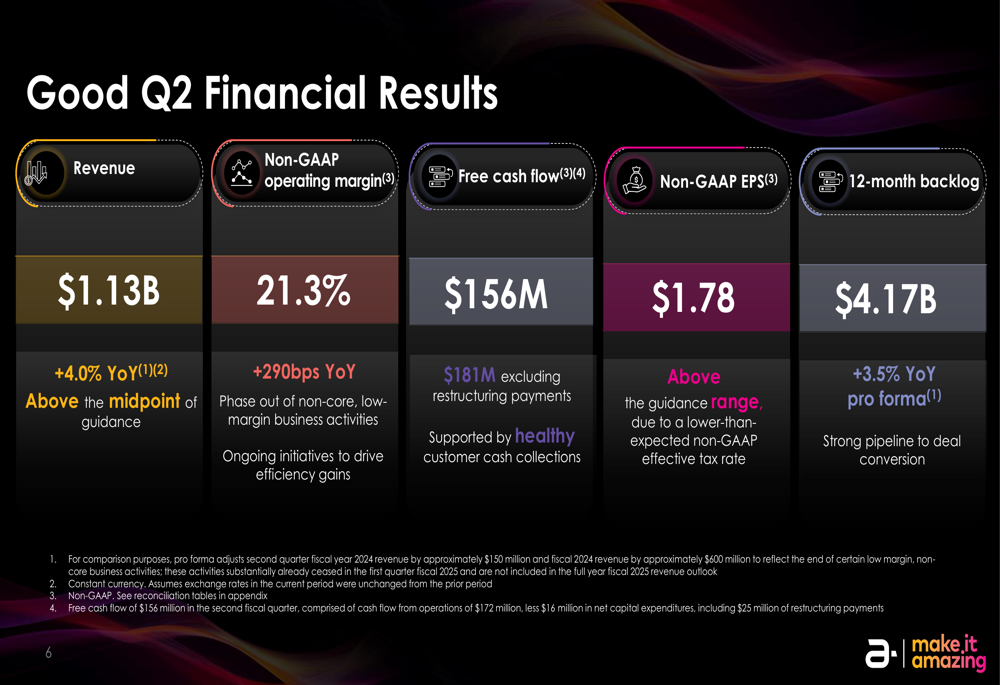

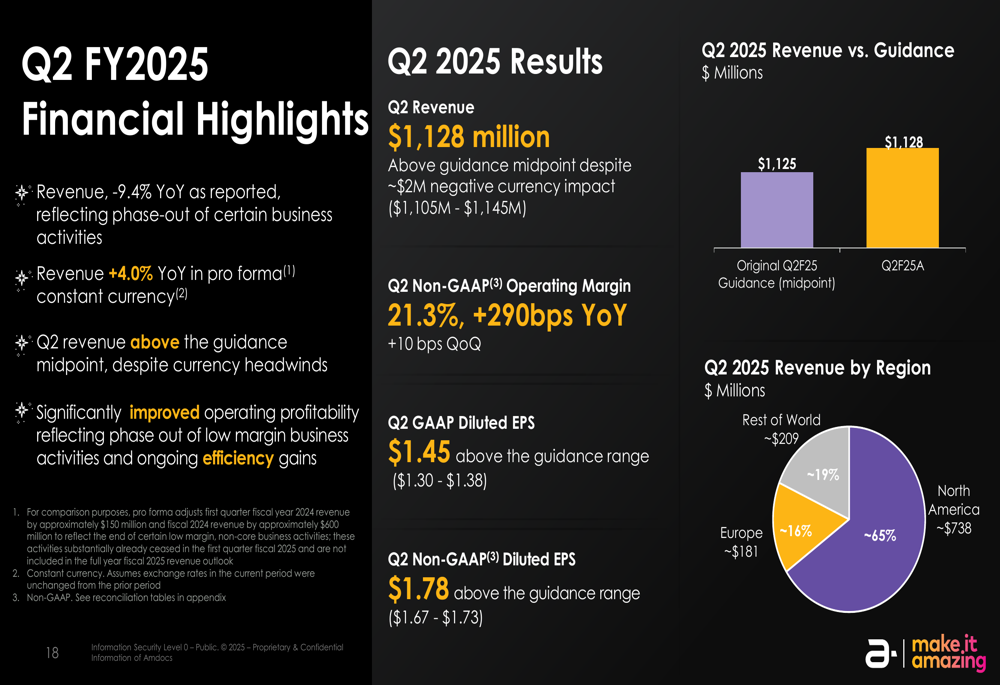

Amdocs reported Q2 revenue of $1.13 billion, representing a 4.0% year-over-year increase on a pro forma constant currency basis, exceeding the midpoint of guidance despite a $2 million negative currency impact. Non-GAAP diluted earnings per share reached $1.78, surpassing the company’s guidance range, partly due to a lower-than-expected effective tax rate.

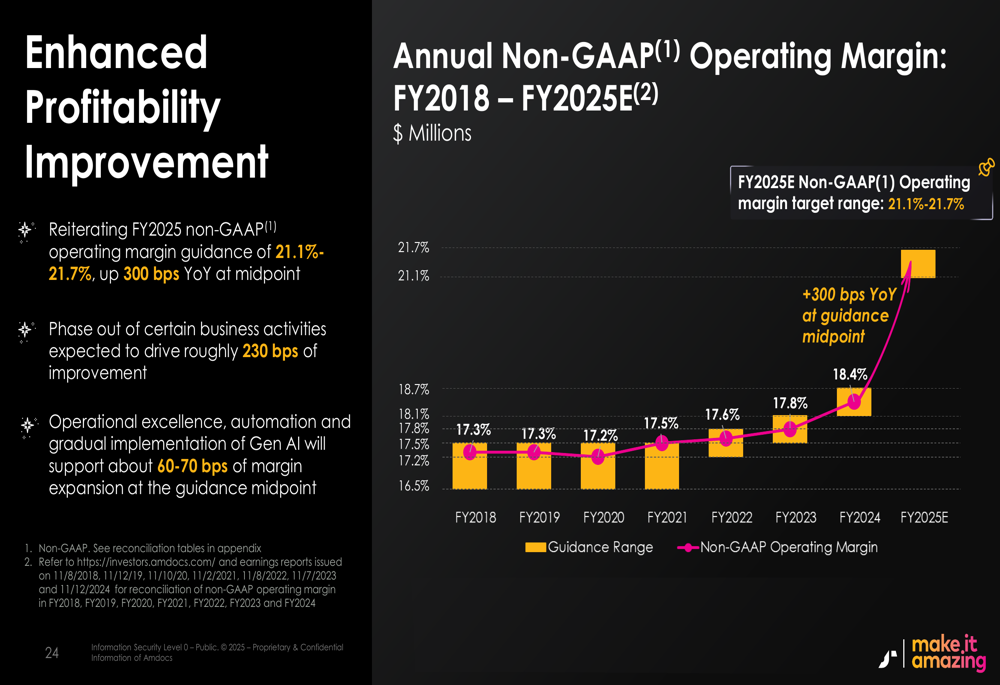

The company’s non-GAAP operating margin expanded significantly to 21.3%, an improvement of 290 basis points year-over-year and 10 basis points sequentially, driven by the phasing out of non-core, low-margin business activities and ongoing efficiency gains.

As shown in the following financial results summary:

Free cash flow was robust at $156 million, or $181 million excluding restructuring payments, supported by healthy customer cash collections. The 12-month backlog increased to $4.17 billion, representing 3.5% year-over-year growth on a pro forma basis, indicating strong pipeline-to-deal conversion and providing visibility into future revenue.

The company’s regional revenue breakdown shows North America continuing to dominate with approximately $738 million (65% of total revenue), followed by Europe at $181 million (16%) and Rest of World at $209 million (19%).

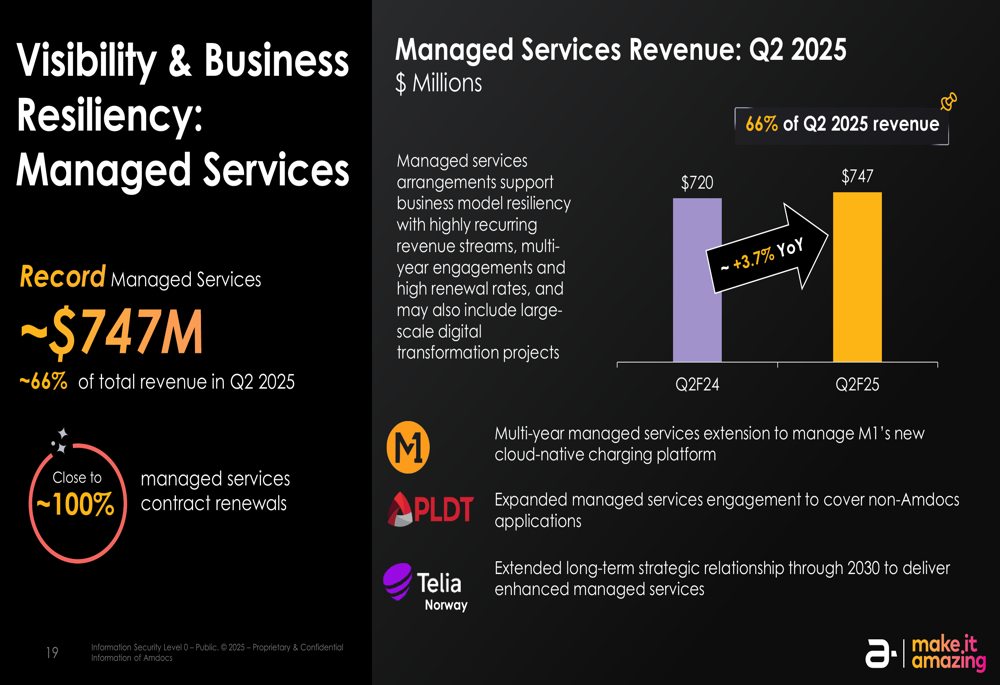

Managed services emerged as a particular strength, reaching a record $747 million and representing approximately 66% of total revenue in Q2. The company achieved close to 100% managed services contract renewals, demonstrating strong customer retention and providing enhanced business visibility and resilience.

Strategic Initiatives

Amdocs highlighted significant progress across its strategic growth framework, focusing on five key domains: cloud migration, digital modernization, monetization of next-generation networks, network automation, and generative AI.

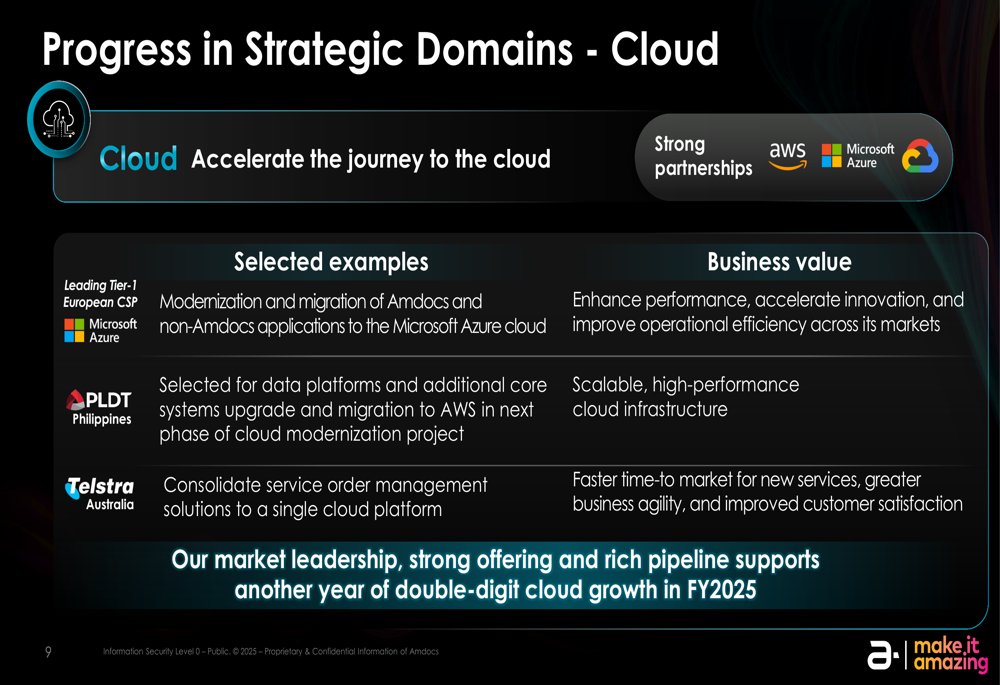

In the cloud domain, Amdocs secured several significant wins, including modernization and migration projects with a leading Tier-1 European communications service provider using Microsoft (NASDAQ:MSFT) Azure, and data platform and core systems migration to AWS for PLDT (NYSE:PHI) Philippines. Management expects another year of double-digit cloud growth in FY2025.

A notable strategic development was Amdocs’ partnership with NVIDIA (NASDAQ:NVDA) to transform AI applications in the telecommunications industry. The company was recognized at NVIDIA’s GTC conference as a key partner driving AI innovation in telecom.

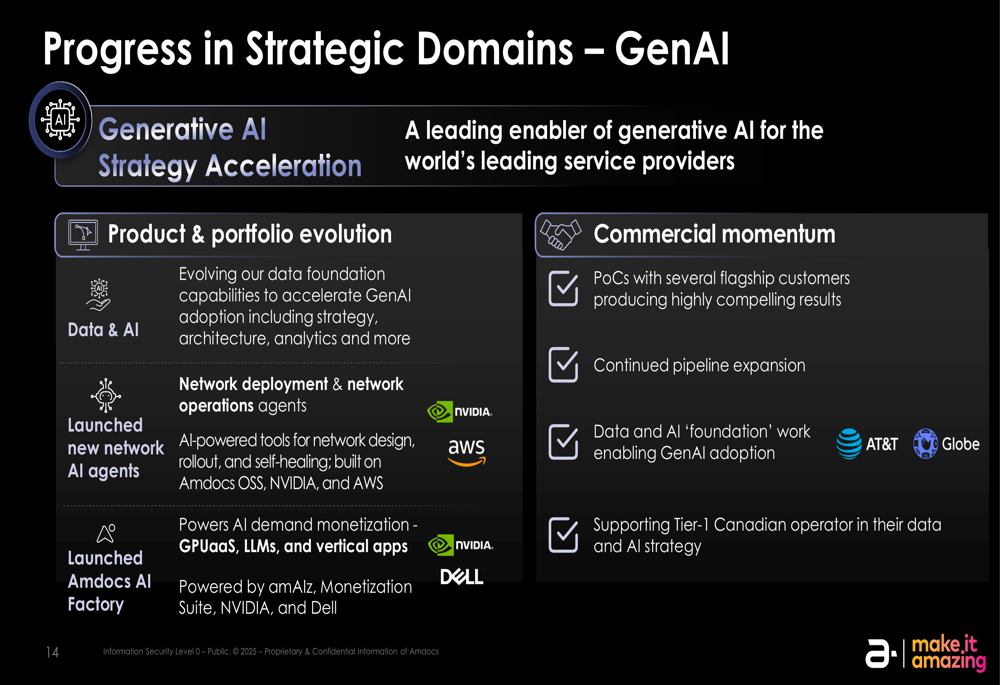

The company is also accelerating its generative AI strategy, positioning itself as a leading enabler of GenAI for major service providers. Initiatives include evolving data foundation capabilities, conducting proof of concepts with flagship customers, launching new network AI agents, and establishing the Amdocs AI Factory.

Forward-Looking Statements

For fiscal year 2025, Amdocs reiterated its revenue growth outlook of 1.7% to 3.7% year-over-year on a pro forma constant currency basis, with a midpoint of 2.7%. The company expects double-digit cloud growth to continue throughout the fiscal year.

Management maintained its non-GAAP operating margin guidance of 21.1% to 21.7%, representing a 300 basis point improvement year-over-year at the midpoint. This margin expansion is expected to be driven by the phase-out of certain business activities (approximately 230 basis points) and efficiency gains from generative AI (60-70 basis points).

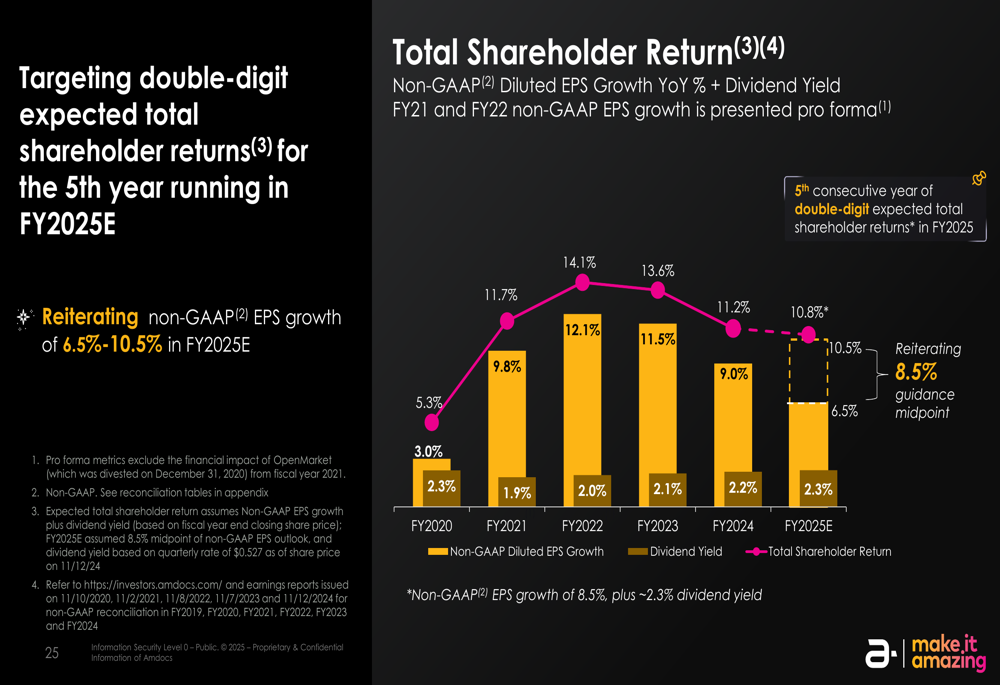

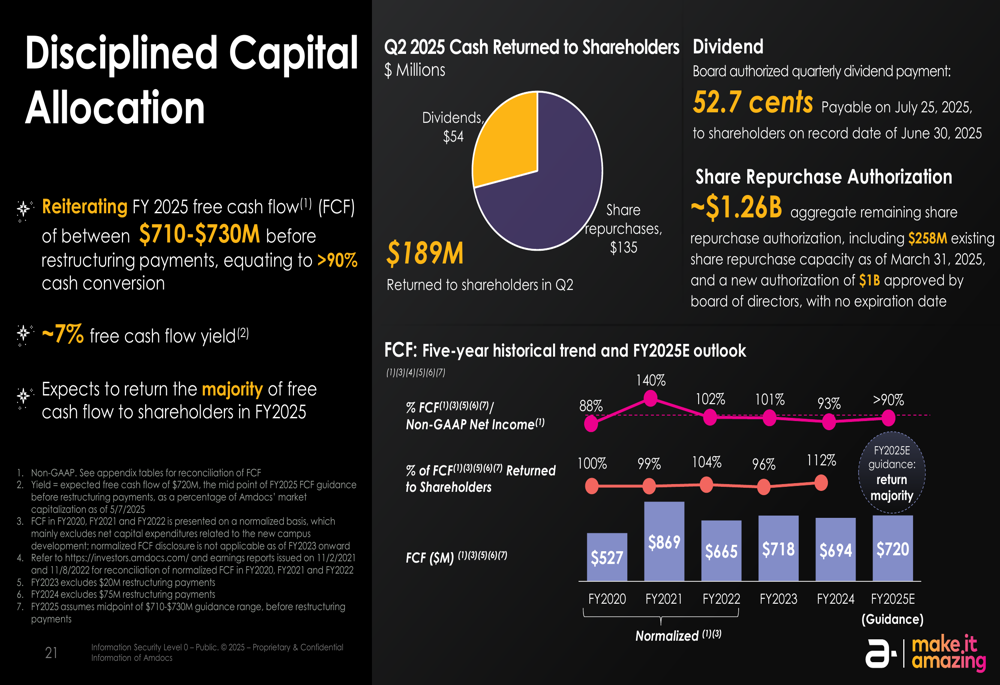

Amdocs projects free cash flow of $710-$730 million for FY2025, with more than 90% earnings-to-cash flow conversion. The company expects non-GAAP EPS growth of 6.5% to 10.5% for the fiscal year and is targeting double-digit total shareholder returns for the fifth consecutive year.

Market Context and Investor Reaction

Despite the positive financial results and outlook, Amdocs’ stock declined in after-hours trading following the earnings release. This reaction may reflect broader market concerns or investor skepticism about growth prospects in an uncertain macroeconomic environment.

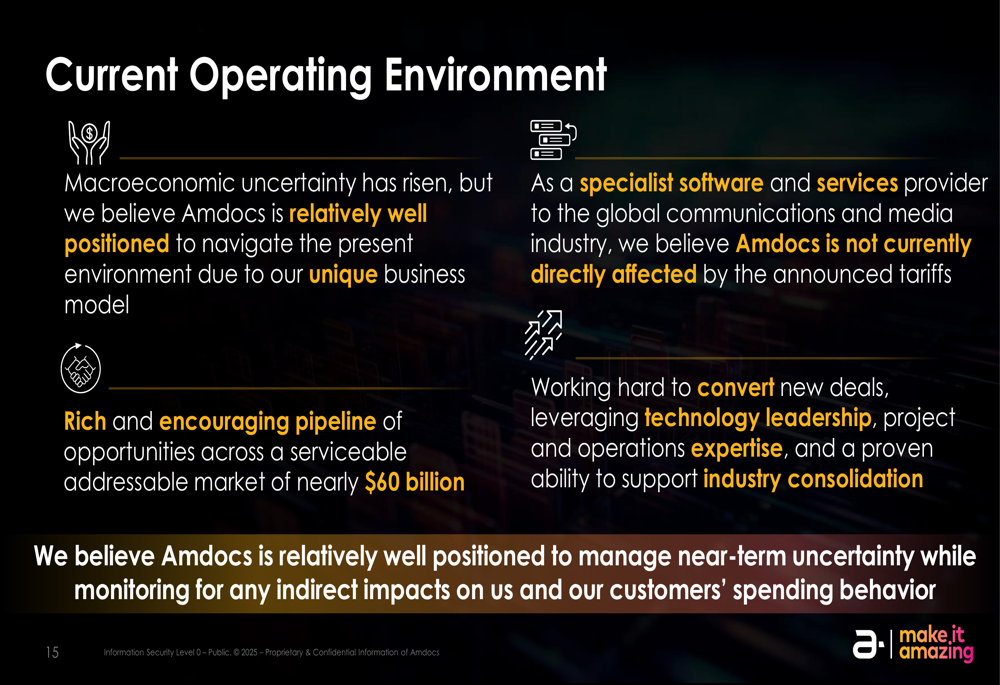

In the earnings call, CEO Shuky Sheffer addressed the current operating environment, noting that while macroeconomic uncertainty has risen, Amdocs is "relatively well positioned" due to its unique business model. The company sees a "rich and encouraging pipeline of opportunities" across a serviceable addressable market of nearly $60 billion and believes it is not directly affected by recently announced tariffs.

The company’s capital allocation strategy remains focused on returning the majority of free cash flow to shareholders through dividends and share repurchases, while maintaining investment-grade credit ratings (Baa1 from Moody’s and BBB from S&P).

Amdocs continues to navigate a competitive landscape by leveraging its technology leadership, project and operations expertise, and proven ability to support industry consolidation. The company’s focus on high-growth areas like cloud, AI, and digital transformation positions it to capitalize on evolving industry trends, though investors appear to be taking a cautious approach despite management’s confident outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.