Chip stocks fall with Nvidia after data center rev disappointment

Introduction & Market Context

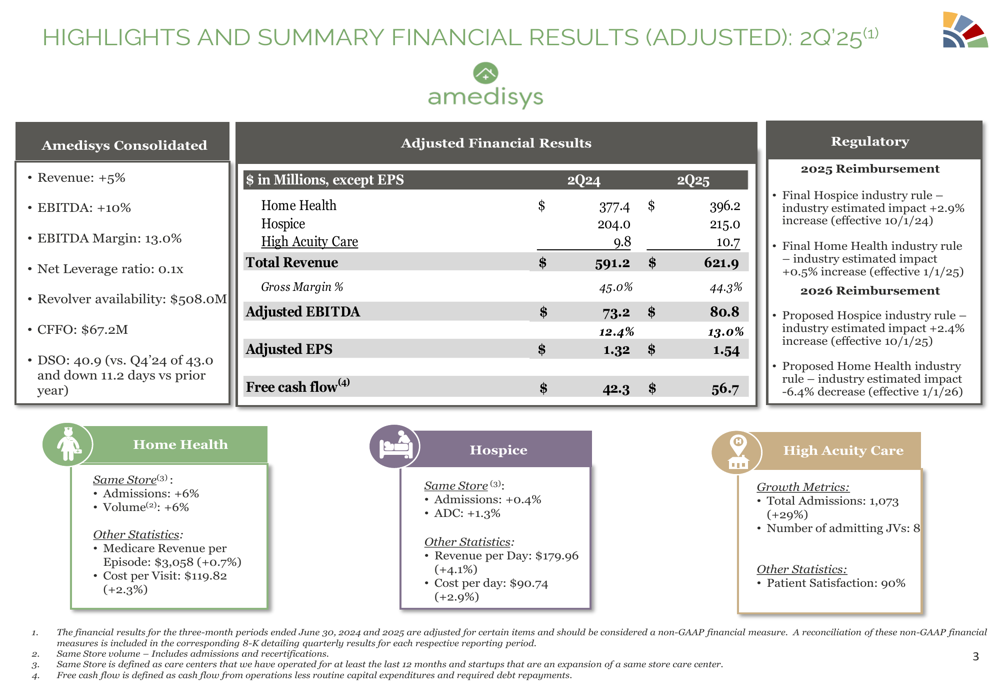

Amedisys Inc. (NASDAQ:AMED) released its second-quarter 2025 earnings presentation on July 29, highlighting solid growth across its home health, hospice, and high acuity care segments. The company, which trades near its 52-week high of $101.02, demonstrated continued operational strength with consolidated revenue growth of 5% and EBITDA growth of 10% compared to the same period last year.

The home healthcare provider continues to benefit from demographic trends favoring in-home care services, while maintaining a strong balance sheet with minimal leverage and substantial liquidity to support future growth initiatives.

Quarterly Performance Highlights

Amedisys reported total revenue of $621.9 million for Q2 2025, a 5% increase from $591.2 million in Q2 2024. Adjusted EBITDA rose 10% to $80.8 million, with EBITDA margin expanding to 13.0%. Adjusted earnings per share reached $1.54, up 16.7% from $1.32 in the prior-year period.

The company’s Home Health segment, which represents 63.7% of consolidated revenue, delivered 6% growth in both same-store admissions and overall volume. The Hospice segment, contributing 34.6% of revenue, showed more modest growth with same-store admissions up 0.4% and average daily census (ADC) increasing 1.3%.

As shown in the following chart of quarterly financial results:

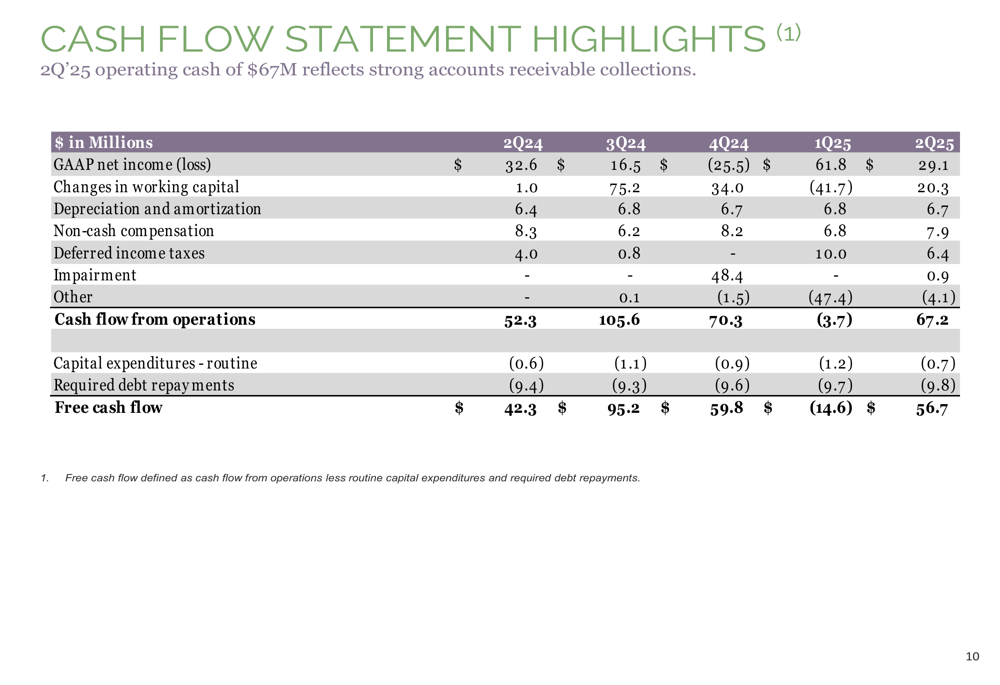

Free cash flow generation was particularly strong at $56.7 million, representing a 34% increase from $42.3 million in Q2 2024. The company maintained excellent working capital management with days sales outstanding (DSO) at 40.9 days.

Detailed Financial Analysis

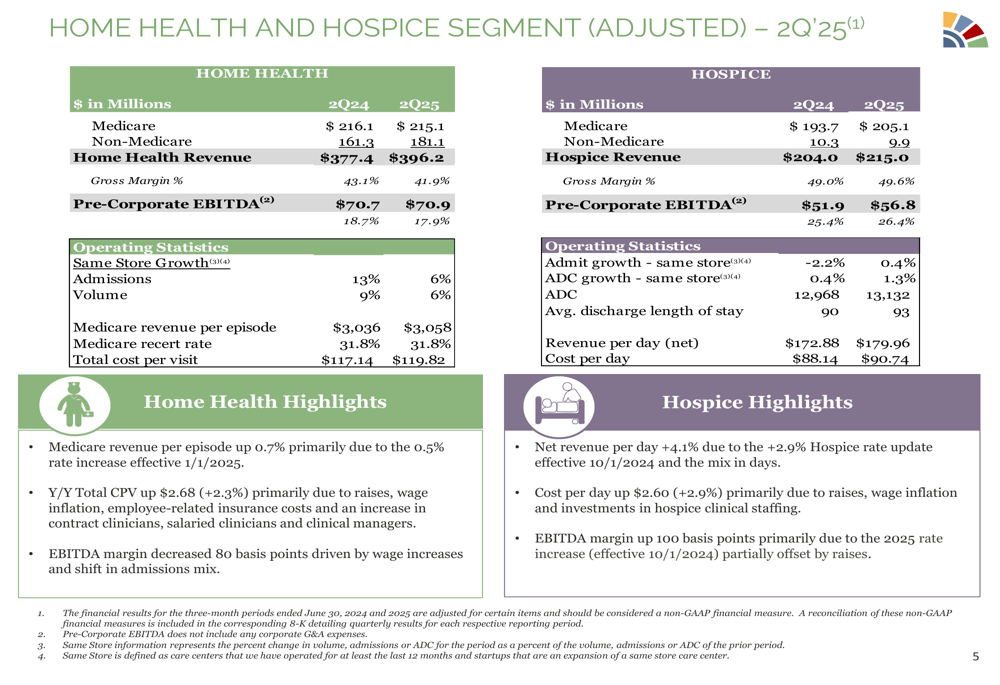

Home Health revenue increased to $396.2 million, up from $377.4 million in Q2 2024, though gross margin contracted slightly to 41.9% from 43.1%. Medicare revenue per episode improved to $3,058, while cost per visit rose to $119.82.

The Hospice segment generated $215.0 million in revenue, up from $204.0 million in the prior-year period, with gross margin expanding to 49.6% from 49.0%. Revenue per day increased to $179.96, while cost per day rose to $90.74.

The following slide details the performance of both segments:

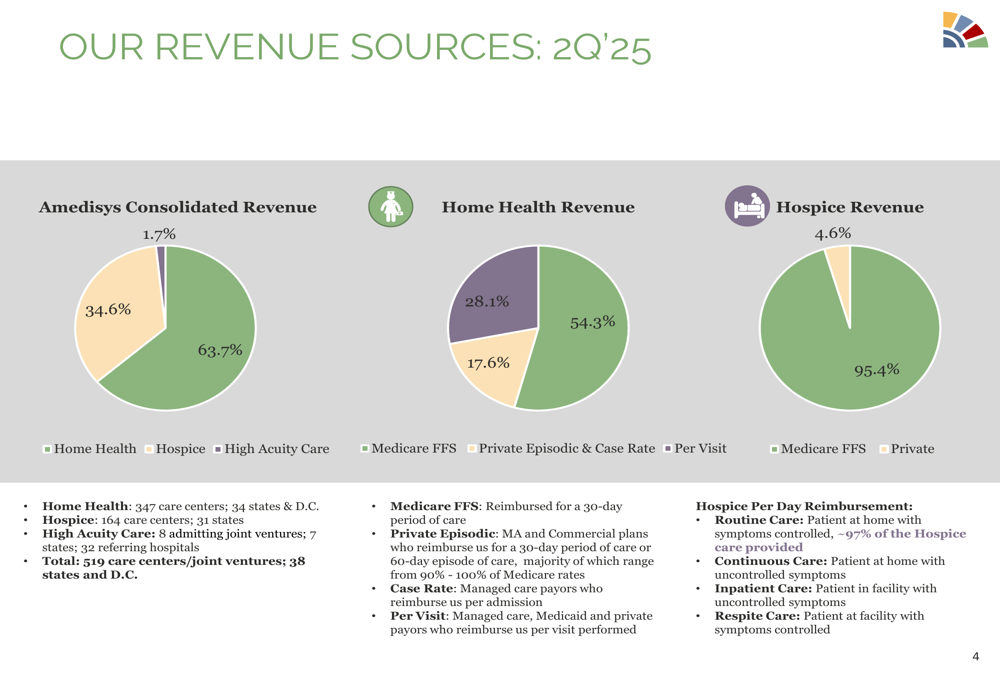

The company’s revenue mix remains heavily weighted toward Medicare fee-for-service programs, which account for 54.3% of Home Health revenue and 95.4% of Hospice revenue. The diversification of payment sources continues to evolve, with private episodic and case rate payments representing 28.1% of Home Health revenue.

The revenue breakdown by segment and payment source is illustrated here:

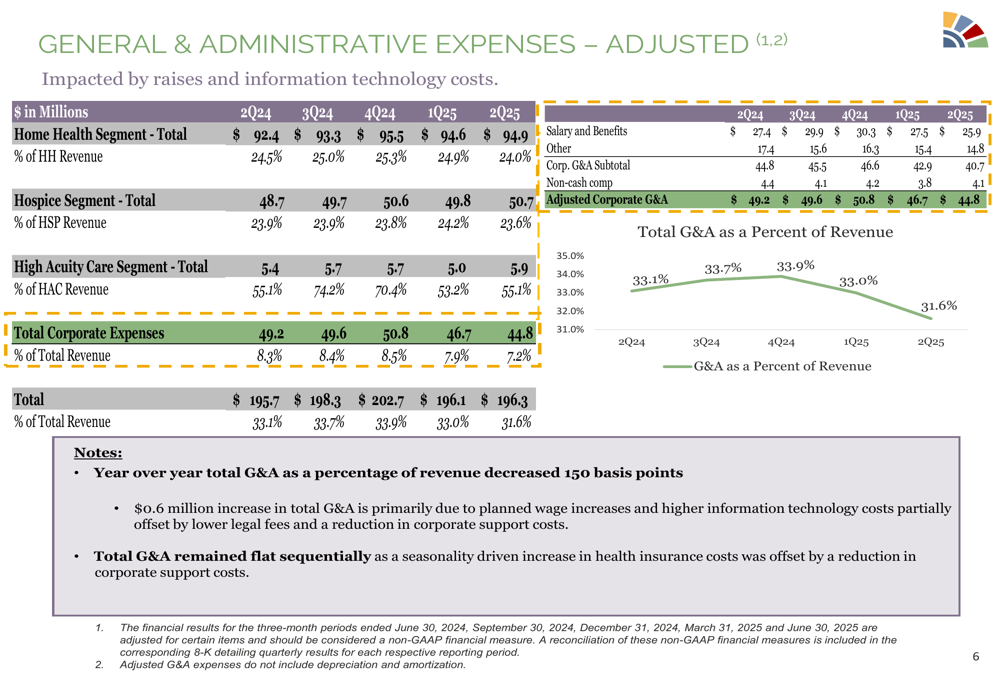

Amedisys has maintained strong cost discipline, with general and administrative expenses as a percentage of revenue decreasing by 150 basis points year-over-year. This improvement came despite planned wage increases and higher information technology costs, offset by lower legal fees and reduced corporate support costs.

Competitive Industry Position

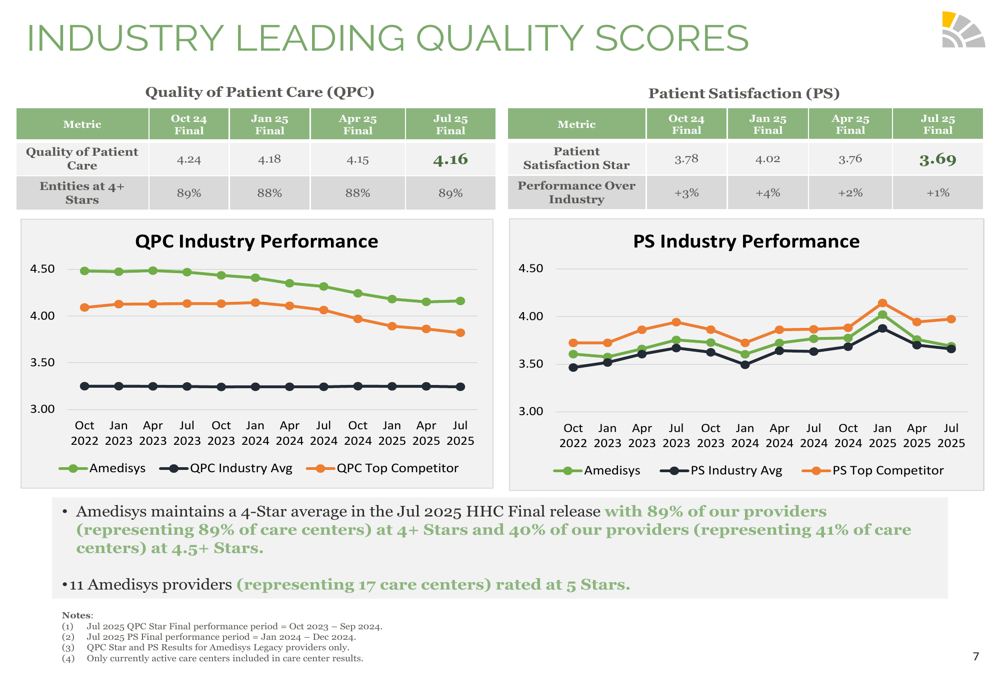

Amedisys continues to outperform industry averages in key quality metrics, which are increasingly important for reimbursement and referral relationships. The company’s Quality of Patient Care (QPC) score stands at 4.16, with 89% of entities achieving 4+ stars and 11 providers rated at 5 stars.

The Patient Satisfaction score of 3.69 exceeds the industry average by 1%, reinforcing Amedisys’ reputation for high-quality care delivery.

The following chart illustrates the company’s quality performance relative to industry benchmarks:

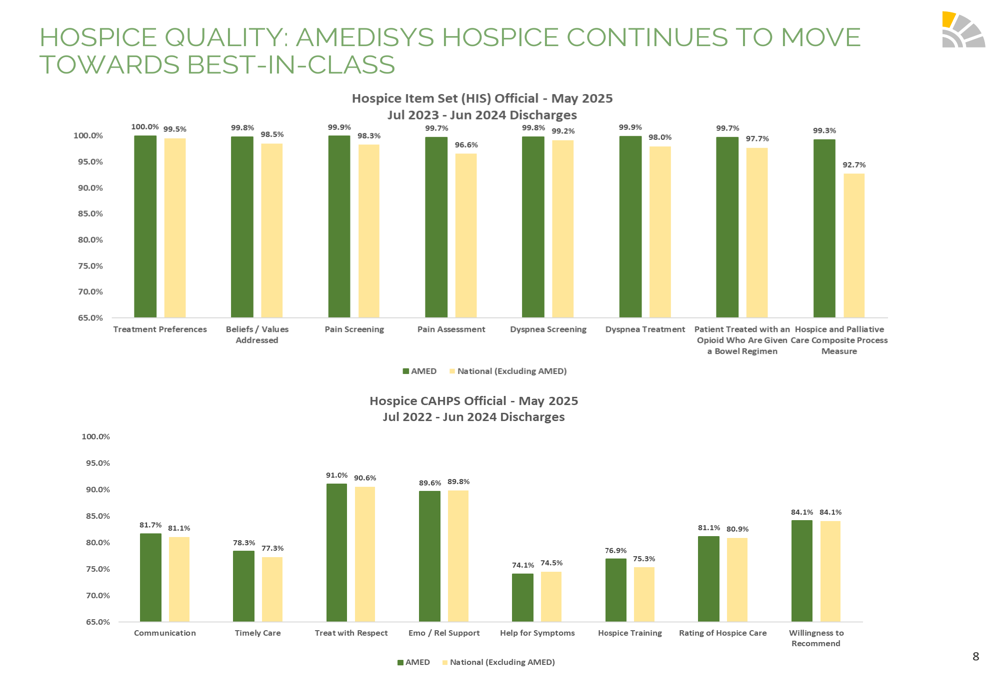

In the Hospice segment, Amedisys also demonstrated strong quality metrics compared to national averages across multiple measures, including treatment preferences, pain management, and patient satisfaction scores.

Forward-Looking Statements

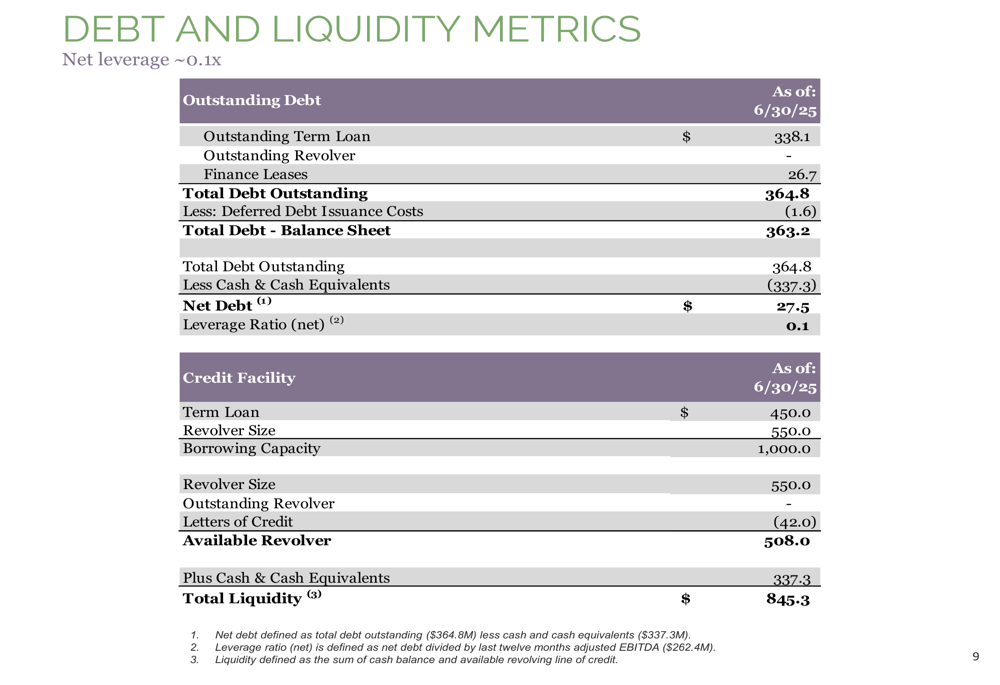

Amedisys maintains a strong financial position to support future growth initiatives, with a net leverage ratio of just 0.1x and total liquidity of $845.3 million. The company has $508.0 million available on its revolving credit facility, providing substantial flexibility for potential acquisitions or investments.

The company’s cash flow from operations reached $67.2 million in Q2 2025, with free cash flow of $56.7 million after capital expenditures. This strong cash generation supports the company’s growth strategy while maintaining financial discipline.

The financial results include adjustments related to merger expenses totaling $26.3 million, which had a $0.70 impact on earnings per share. These adjustments reflect ongoing integration activities as the company continues to optimize its operational structure.

Looking ahead, Amedisys appears well-positioned to benefit from favorable demographic trends and the ongoing shift toward home-based care services. The company’s strong quality metrics, solid financial position, and growing high acuity care segment (which saw admissions increase by 29%) provide multiple avenues for continued growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.