US stock futures dip as Trump’s firing of Cook sparks Fed independence fears

Introduction & Market Context

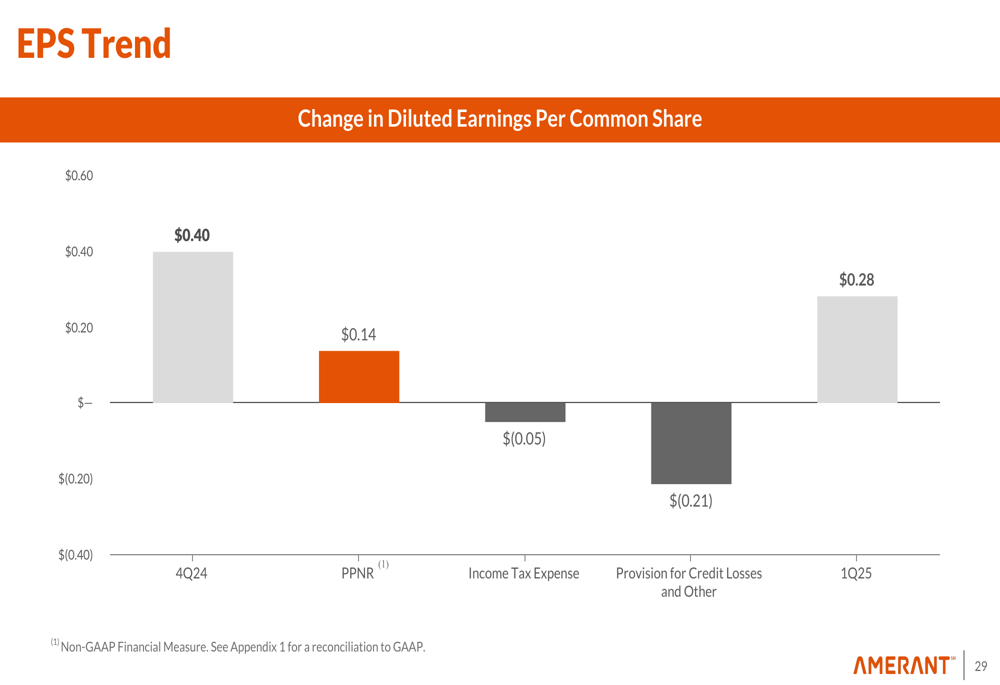

Amerant Bancorp Inc. (NASDAQ:NYSE:AMTB) presented its first quarter 2025 financial results on April 24, revealing a mixed performance marked by solid deposit growth but offset by deteriorating credit quality metrics. The Florida-focused bank reported diluted earnings per share of $0.28, down from $0.40 in the previous quarter, as increased credit provisions weighed on profitability despite operational improvements.

The bank’s stock has faced pressure in recent months, with shares trading near $19.48 at the previous close. In premarket trading following the earnings presentation, AMTB was down 3.18% to $18.86, continuing a challenging trend for the company whose shares have ranged from $16.55 to $27.00 over the past 52 weeks.

Quarterly Performance Highlights

Amerant reported net income of $12.0 million for Q1 2025, a significant decrease from $16.9 million in Q4 2024. This decline occurred despite pre-provision net revenue (PPNR) increasing to $33.9 million from $27.9 million in the previous quarter, highlighting the impact of higher credit provisions on bottom-line results.

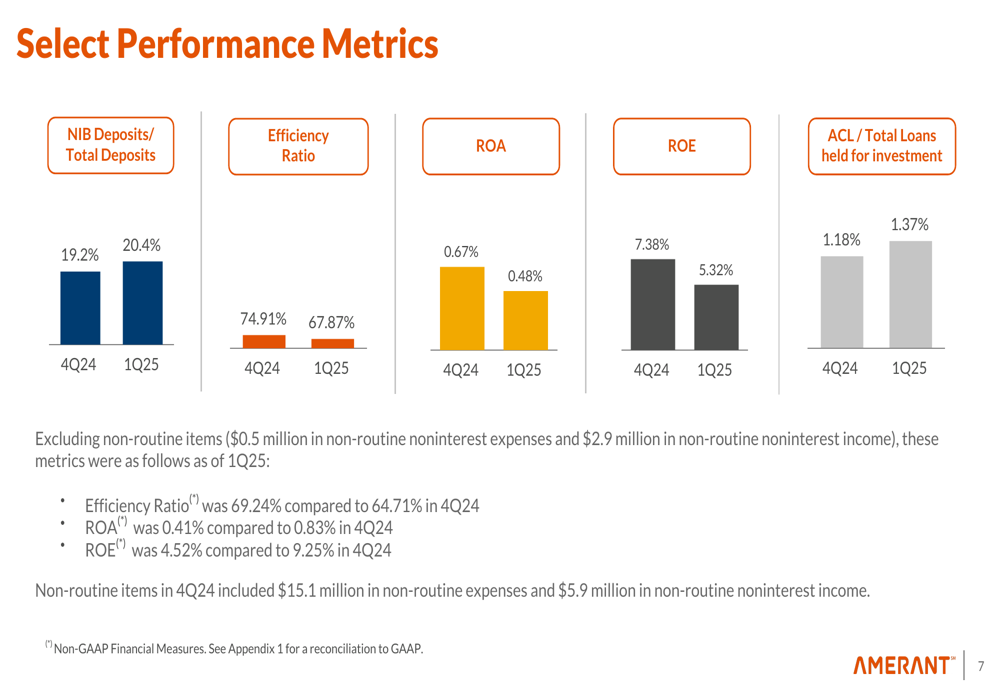

The bank’s balance sheet showed positive momentum with total assets reaching $10.2 billion, up $268 million from the previous quarter. Total (EPA:TTEF) deposits grew by $300.4 million to $8.2 billion, with core deposits increasing by $372.9 million to $6.0 billion. The proportion of non-interest bearing deposits to total deposits improved to 20.4% from 19.2% in the previous quarter.

As shown in the following chart of key performance metrics, Amerant’s efficiency ratio improved to 67.87% from 74.91%, but return on assets (ROA) and return on equity (ROE) both declined significantly:

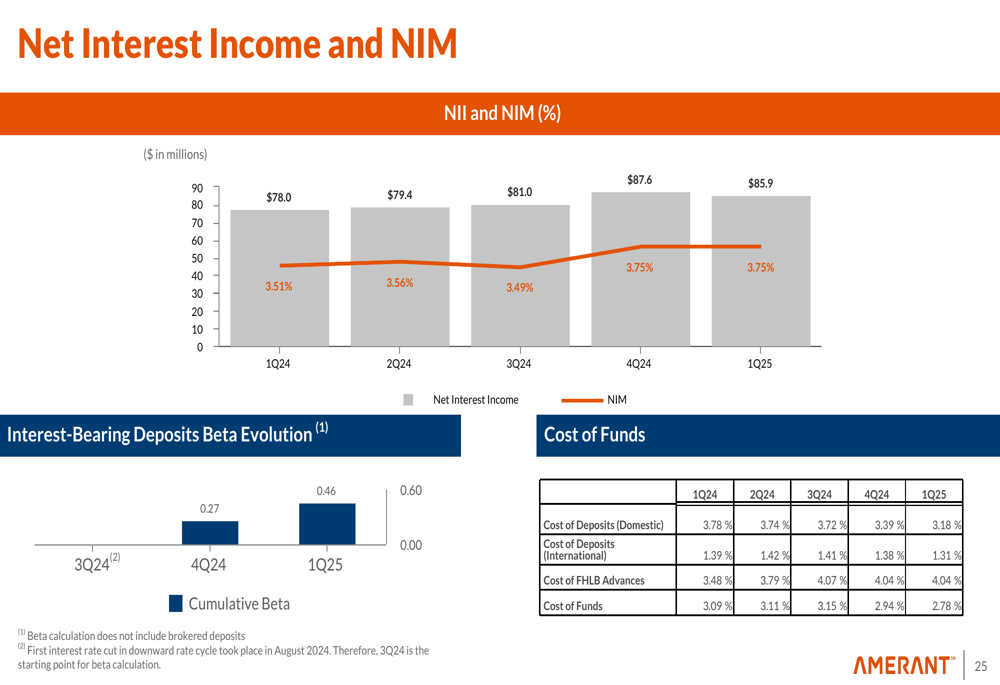

Net interest margin remained stable at 3.75%, while net interest income decreased slightly to $85.9 million from $87.6 million in Q4 2024. Non-interest income fell to $19.5 million from $23.7 million, while non-interest expense decreased substantially to $71.6 million from $83.4 million in the previous quarter.

The following chart illustrates the factors contributing to the change in earnings per share from Q4 2024 to Q1 2025:

Credit Quality Concerns

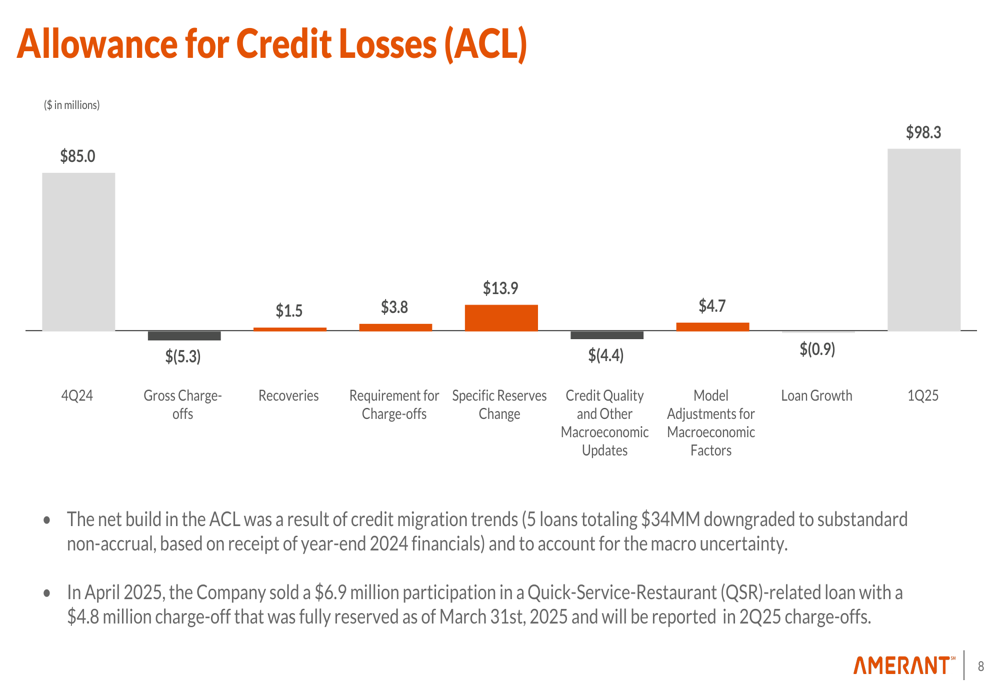

The most significant challenge facing Amerant in Q1 2025 was deteriorating credit quality across multiple metrics. The allowance for credit losses (ACL) increased substantially from $85.0 million to $98.3 million, with the ACL to total loans ratio rising to 1.37% from 1.18% in the previous quarter.

The following waterfall chart details the changes in the allowance for credit losses during the quarter:

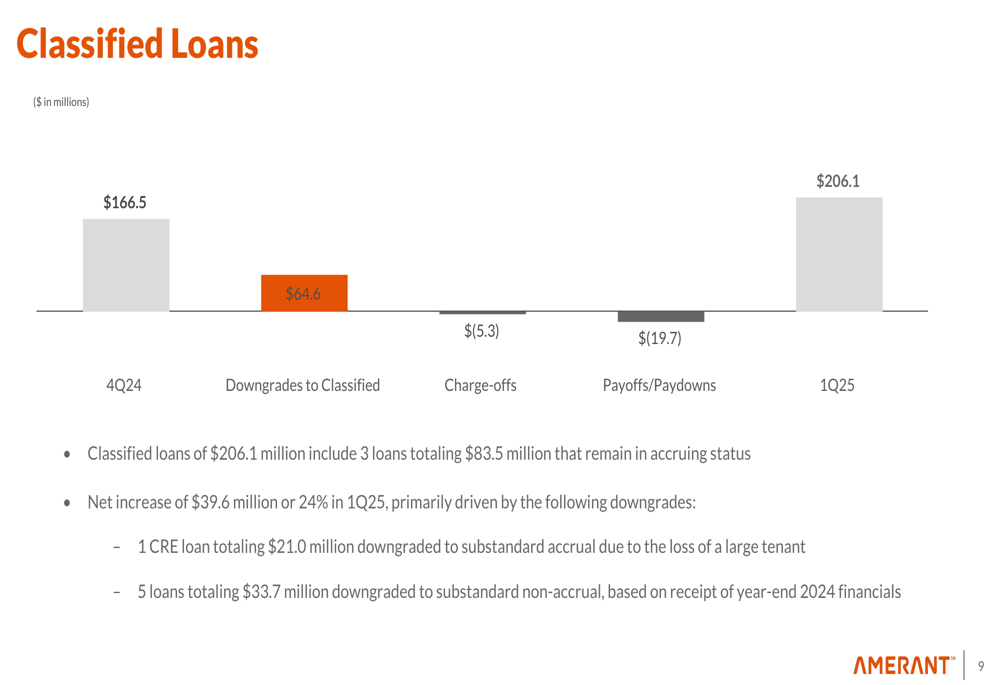

Classified loans increased by 24% to $206.1 million from $166.5 million in Q4 2024, primarily driven by downgrades based on year-end 2024 financials. The company noted that five loans totaling $33.7 million were downgraded to substandard non-accrual status.

As shown in the following chart, the increase in classified loans was primarily driven by new downgrades:

Perhaps most concerning was the dramatic increase in special mention loans, which surged from $5.4 million to $99.7 million. The company attributed this increase to eight loans totaling $97.3 million being downgraded, including three CRE loans in New York City and five commercial loans downgraded based on year-end 2024 financials.

Non-performing loans also increased from $104.1 million to $123.2 million, while non-performing assets totaled $140.9 million, including $17.5 million in other real estate owned.

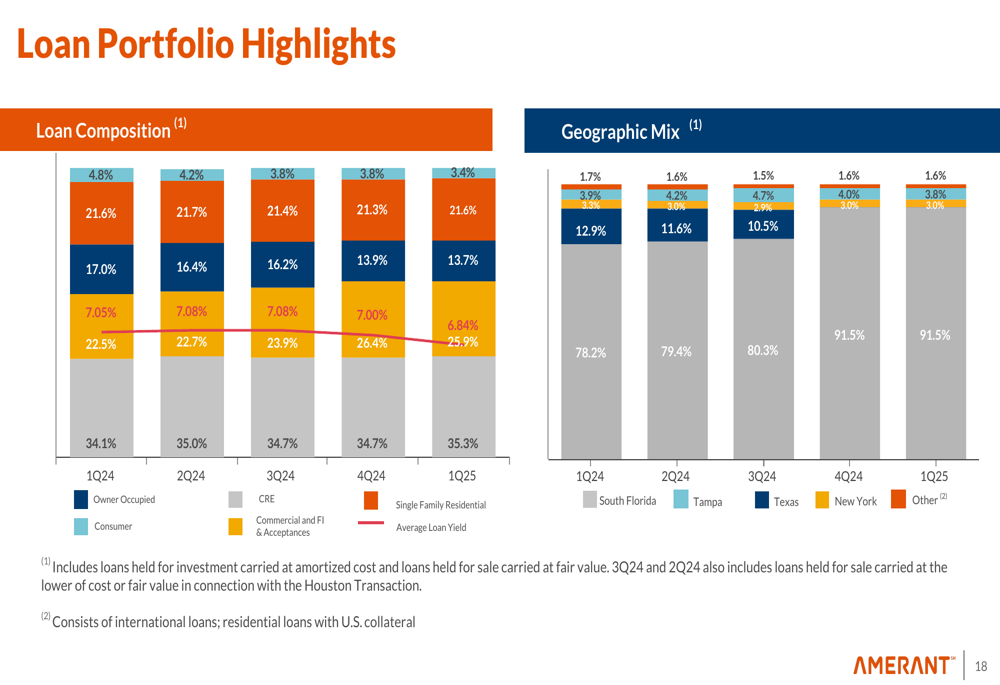

Loan Portfolio Composition

Amerant maintains a diversified loan portfolio, though heavily concentrated in real estate lending. The following chart shows the composition and geographic distribution of the loan portfolio:

The loan portfolio remains heavily concentrated in South Florida at 91.5%, with smaller exposures in Tampa (3.8%), Texas (1.6%), and New York (1.4%). By loan type, owner-occupied loans represent the largest segment at 35.3%, followed by commercial real estate at 25.9% and commercial and industrial loans at 21.6%.

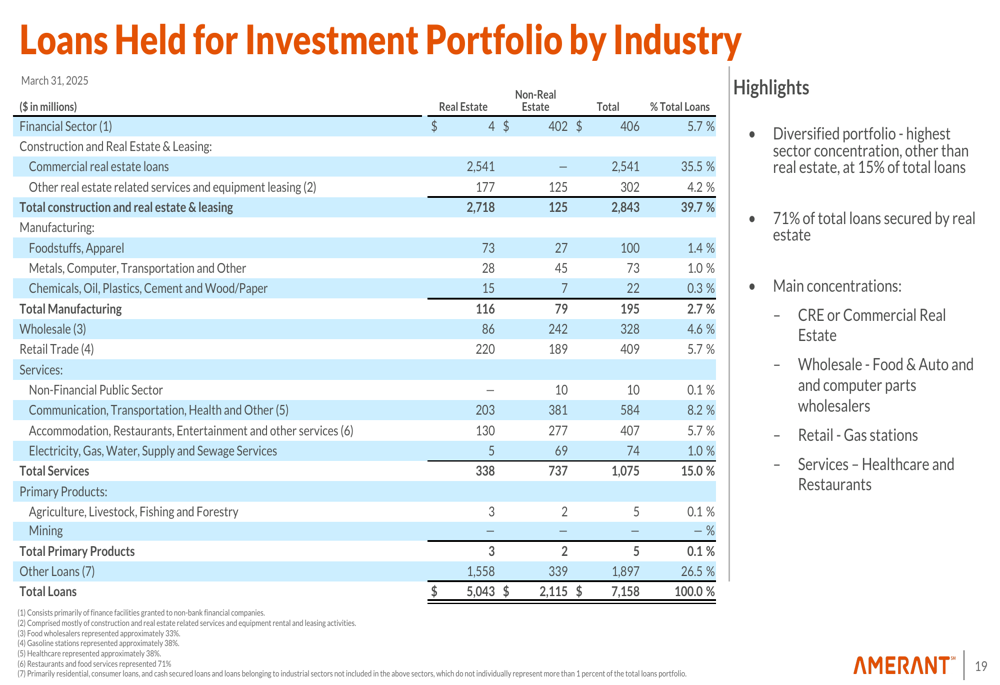

The industry distribution of the loan portfolio demonstrates Amerant’s focus on real estate, as illustrated in the following chart:

Construction and real estate lending accounts for 39.7% of the portfolio, with services at 15.0% representing the next largest concentration. Overall, 71% of total loans are secured by real estate, highlighting the bank’s exposure to property markets, particularly in Florida.

Strategic Initiatives

Amerant outlined several strategic initiatives during the presentation, most notably a significant restructuring of its mortgage business. The company is transitioning Amerant Mortgage from a national mortgage originator to focusing on in-footprint lending to support its retail and private banking customers.

This restructuring is expected to reduce non-interest expenses by approximately $2.5 million per quarter starting in Q3 2025. The company plans to reduce mortgage-related staff from 77 to approximately 20 employees over the next 120 days.

Geographic expansion remains a priority, with Amerant opening a new regional office and banking center in West Palm Beach in mid-April 2025. The bank also plans to open two new locations in Miami Beach and a second location in downtown Tampa in the coming months.

The company highlighted recent key executive hires, including Jeffrey Tischler as Chief Credit Officer, Cory Bowden as Head of Credit Review, and Kavitha Singh as Head of Enterprise Risk Management, signaling a focus on strengthening risk management capabilities amid credit quality concerns.

Forward-Looking Statements

For the second quarter of 2025, Amerant projects deposit growth in line with previous guidance of 15% annualized, with continued focus on improving the ratio of non-interest bearing to total deposits. Loan growth is expected to be in the range of 10-15% by year-end, though the company noted that temporary asset mix changes might occur if net loan growth materializes later in the year.

Net interest margin is projected to decline slightly to the mid-3.60% range in Q2 2025 from the current 3.75%. Expenses are expected to remain at similar levels to Q1 2025, with cost reductions related to the mortgage business restructuring expected to materialize in the second half of 2025.

The following chart shows the historical trend of net interest income and net interest margin:

While Amerant’s Q1 2025 results demonstrate solid deposit growth and operational improvements, the significant deterioration in credit quality metrics presents a substantial challenge. Investors will likely focus on whether the company’s strategic initiatives and strengthened risk management team can effectively address these credit concerns in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.