Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Angel Oak Mortgage REIT, Inc. (NYSE:AOMR) released its second quarter 2025 earnings presentation on August 5, revealing mixed results that prompted a negative market reaction. The company reported a significant 35% year-over-year increase in interest income, but its earnings per share fell well short of analyst expectations. Following the earnings announcement, AOMR shares declined 6.25% to close at $8.84, reflecting investor disappointment with the bottom-line performance.

The mortgage REIT, which focuses on non-QM loans, reported GAAP earnings of $0.03 per share, significantly below the analyst consensus of $0.29, representing an 89.66% miss. Despite this shortfall, the company highlighted its continued execution of its securitization strategy and maintained its quarterly dividend.

Financial Performance Highlights

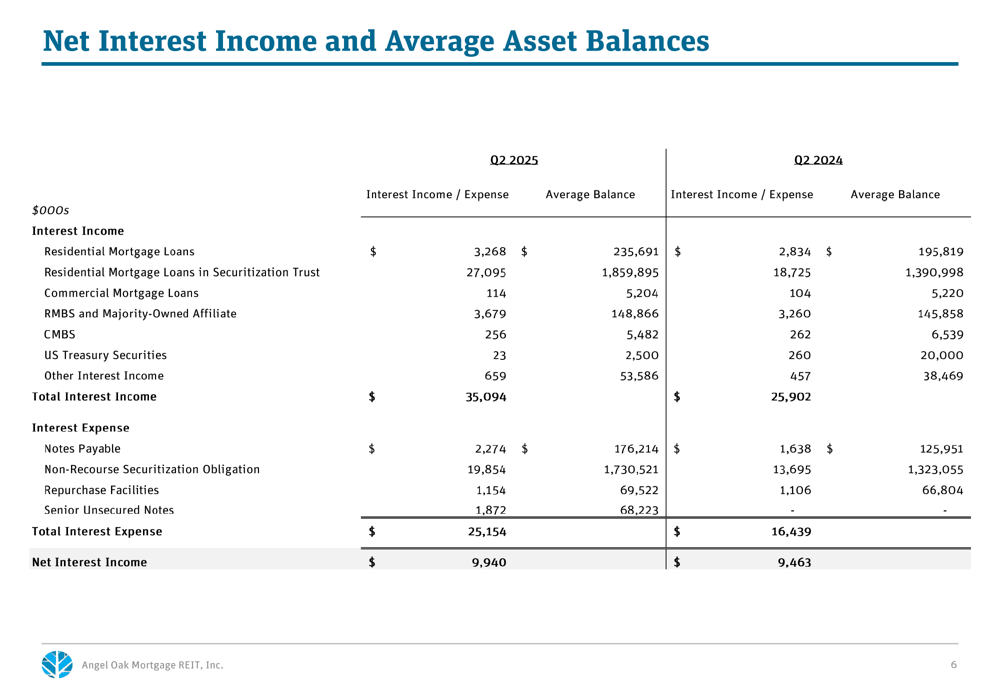

Angel Oak reported total interest income of $35.1 million for Q2 2025, a 35% increase compared to $25.9 million in Q2 2024. Net interest income grew more modestly, rising 5% year-over-year to $9.9 million. The company’s distributable earnings were $2.6 million ($0.11 per share), a marked improvement from the negative $2.3 million reported in the same period last year.

As shown in the following detailed breakdown of the company’s interest income and expenses:

The majority of interest income came from residential mortgage loans in securitization trusts, which generated $27.1 million in Q2 2025 compared to $18.7 million in Q2 2024. However, interest expenses also increased substantially to $25.2 million from $16.4 million in the prior year period, limiting the growth in net interest income.

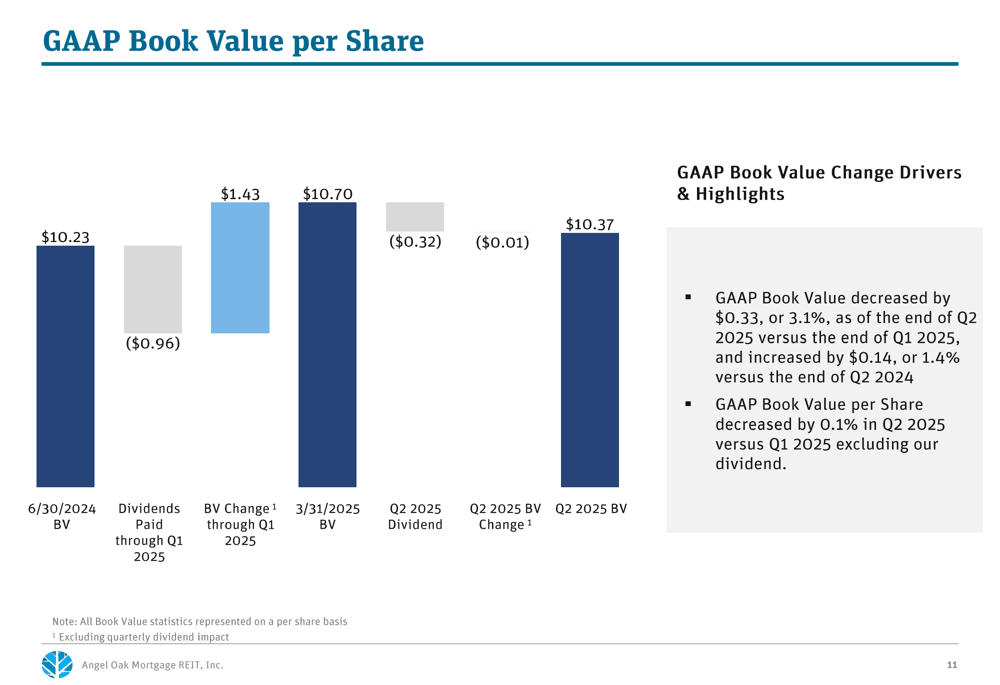

AOMR’s GAAP book value per share declined 3.1% quarter-over-quarter to $10.37, while economic book value per share decreased 3.3% to $12.97. The company attributed the book value decline primarily to dividend payments, as illustrated in the following chart:

Securitization Activity

A key component of Angel Oak’s business strategy is its securitization program, which the company continued to execute during Q2 2025. The REIT completed two securitizations during the quarter: AOMT 2025-4 and participated in AOMT 2025-6.

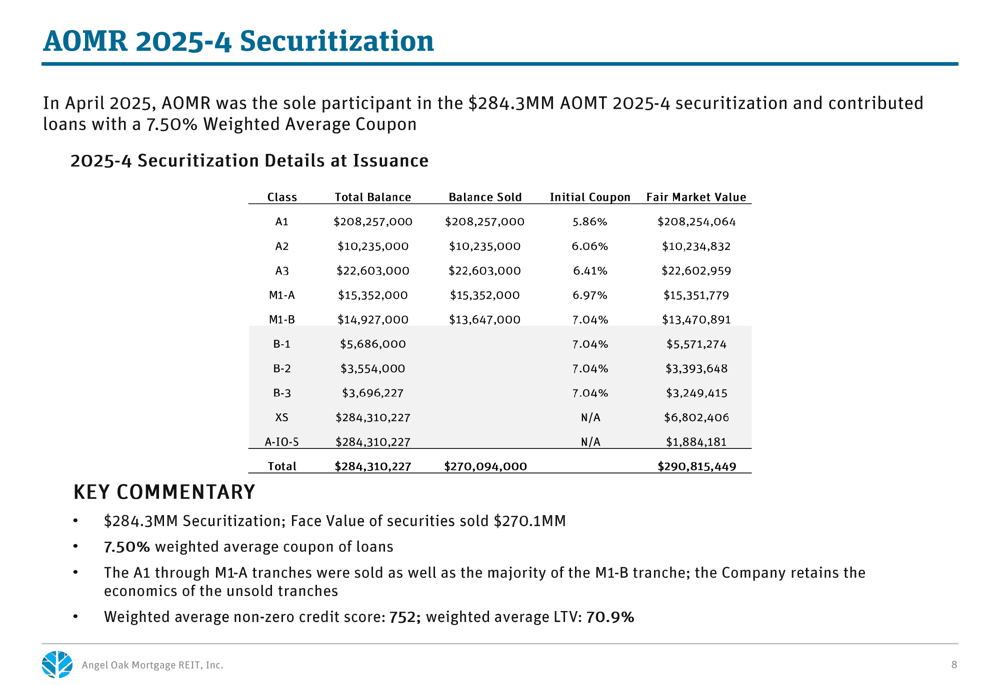

The AOMT 2025-4 securitization, completed in April 2025, had a total unpaid principal balance of $284.3 million with a weighted average coupon of 7.50%. The company sold securities with a face value of $270.1 million, retaining the economics of the unsold tranches. The following table provides detailed information about this securitization:

In May 2025, AOMR participated in the AOMT 2025-6 securitization, contributing loans with an unpaid principal balance of $87.2 million to the $349.7 million total securitization. The weighted average coupon of loans in this securitization was 7.65%.

During the earnings call, CFO Brandon Filson highlighted the strength of the securitization market, noting, "The securitization market continues to get tighter and stronger in the non-QM space." The company plans to execute another securitization in September 2025.

Portfolio Composition and Quality

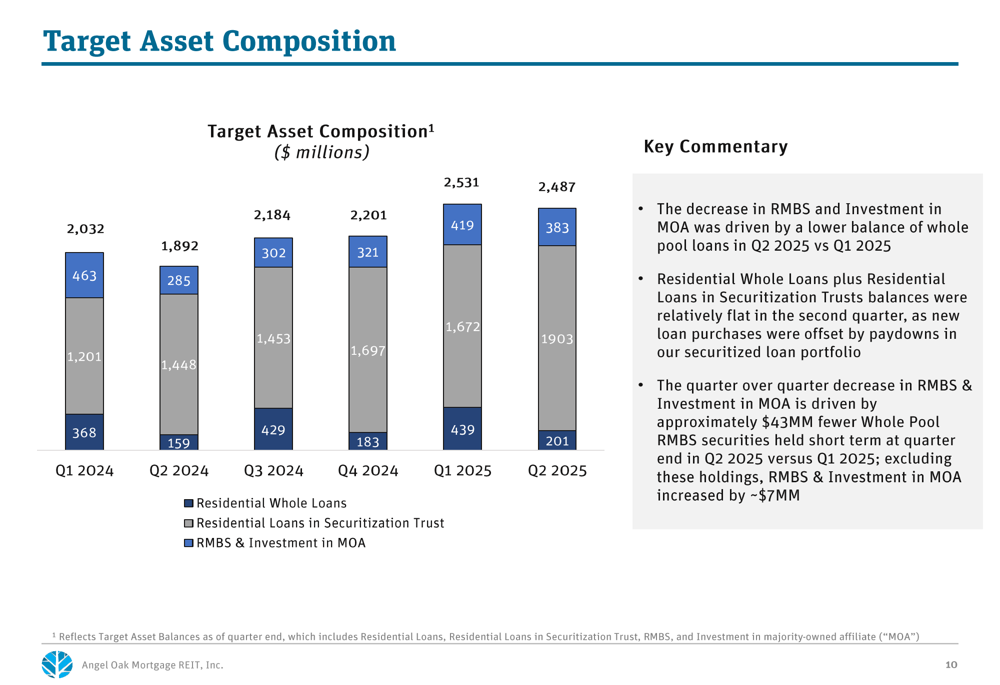

Angel Oak’s target asset composition has evolved over recent quarters, with a growing emphasis on residential loans in securitization trusts. The following chart illustrates this trend:

As of June 30, 2025, the company’s residential whole loan portfolio had a fair value of $200.7 million with a weighted average coupon of 8.37%. The portfolio remains diversified across borrower types, with bank statement borrowers representing 35%, investor loans 33%, and HELOCs & closed end seconds 27%.

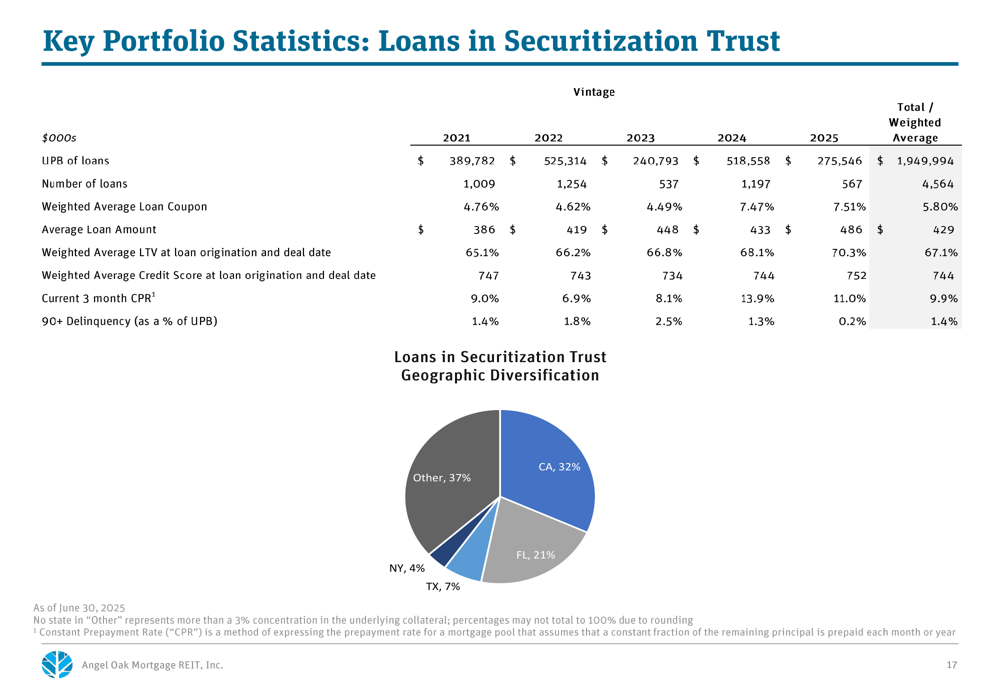

The quality of the loan portfolio remains relatively stable, with 90+ day delinquencies at 2.35% across the entire portfolio. The loans in securitization trusts, which represent the largest portion of AOMR’s assets, showed a 90+ day delinquency rate of 1.4% as detailed in the following table:

The securitized loan portfolio maintains strong credit metrics with a weighted average credit score of 744 and a weighted average loan-to-value ratio of 67.1%. The portfolio is geographically diversified, though with significant exposure to California (32%) and Florida (21%).

Balance Sheet and Leverage

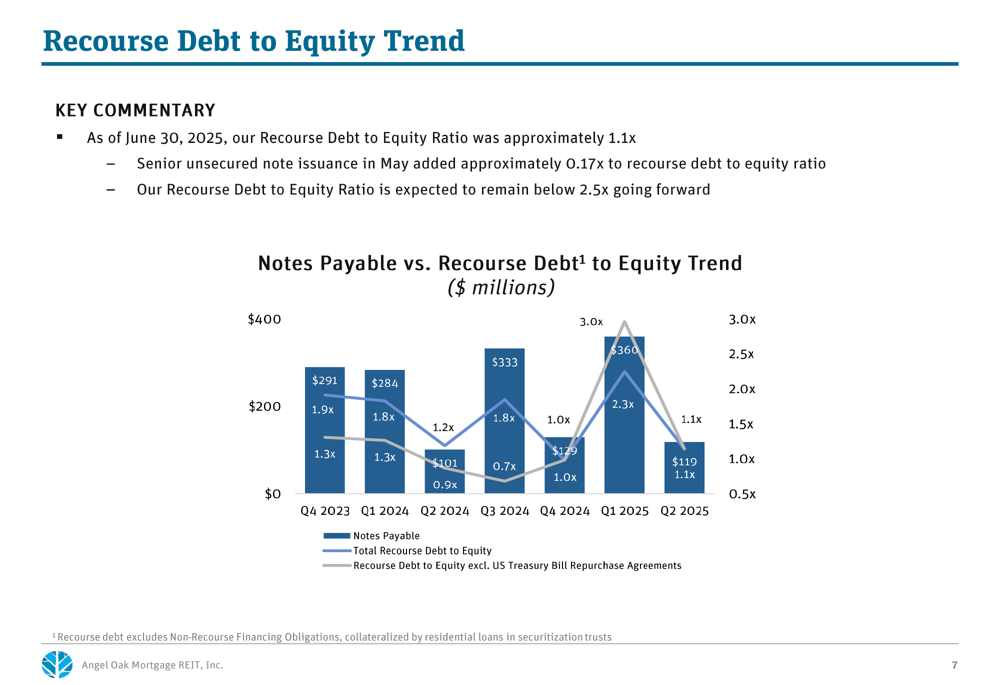

Angel Oak has maintained a conservative leverage profile, with its recourse debt to equity ratio decreasing to 1.1x as of June 30, 2025, down from 2.3x in the previous quarter. This reduction was partially offset by the issuance of $42.5 million in senior unsecured notes at 9.75% in May.

The following chart illustrates the company’s recourse debt to equity trend over recent quarters:

Management indicated that they expect the recourse debt to equity ratio to remain below 2.5x going forward, reflecting a conservative approach to balance sheet management despite the challenging interest rate environment.

Forward-Looking Statements

Looking ahead, Angel Oak plans to continue its securitization strategy with another transaction planned for September 2025. The company also indicated it would explore capital raising through preferred equity markets to support future growth.

CEO Srini Prabhu expressed optimism about the company’s future, stating, "We look forward to continuing to build long-term value for our shareholders." However, the significant EPS miss raises questions about the company’s ability to meet market expectations in the near term.

The company faces several challenges, including potential continued EPS volatility, changing market conditions affecting securitization and loan origination, and macroeconomic factors such as interest rate changes. Management is focusing on maintaining current operating expense levels while pursuing portfolio growth and net interest margin improvement.

Angel Oak’s dividend yield of approximately 13.6% (based on the $0.32 quarterly dividend declared for Q2) may continue to attract income-focused investors despite the recent earnings disappointment and stock price decline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.