Figma Shares Indicated To Open $105/$110

Anika Therapeutics Inc (NASDAQ:ANIK) presented its first quarter 2025 financial results on May 9, revealing a mixed performance characterized by strong commercial channel growth counterbalanced by significant declines in its OEM business. The company also announced a substantial downward revision to its full-year guidance, particularly for adjusted EBITDA.

Introduction & Market Context

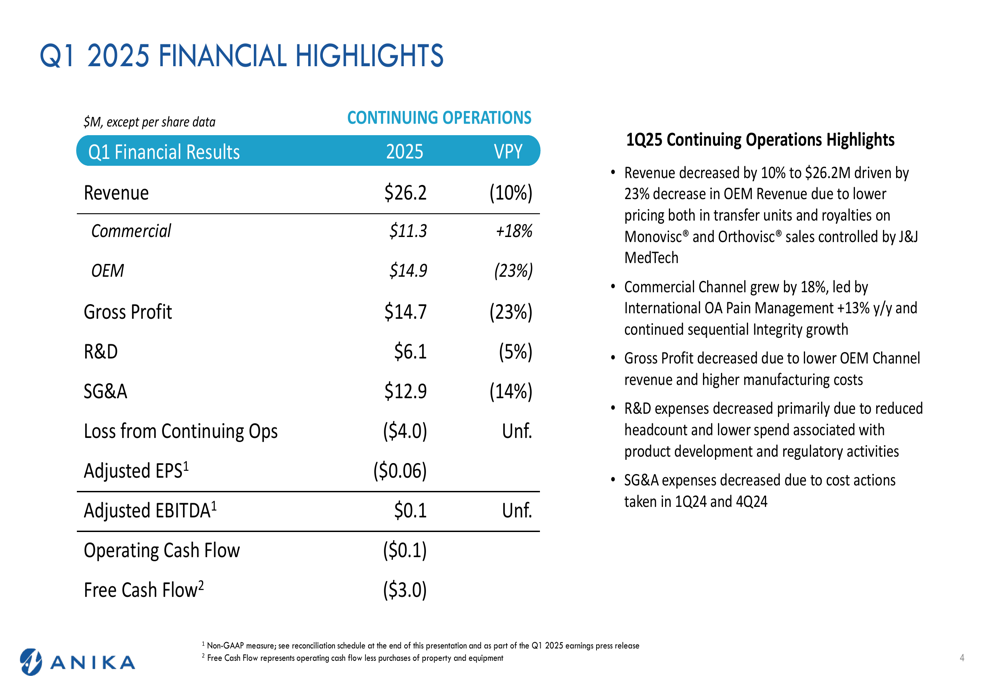

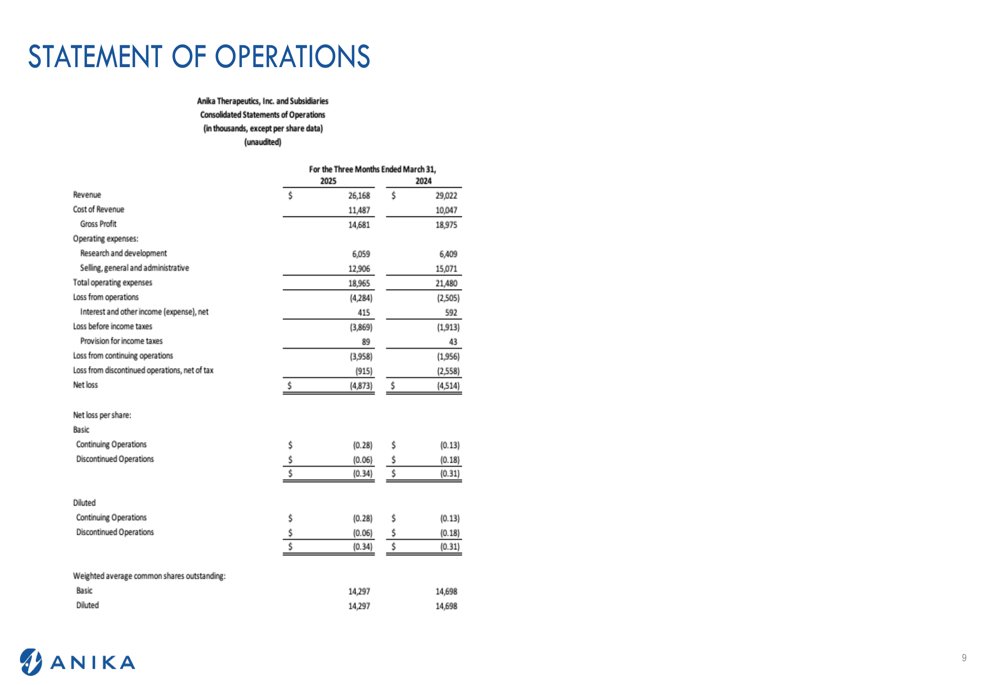

Anika’s stock fell 5.02% in premarket trading following the release of its Q1 results, reflecting investor concerns about the company’s revised outlook. The medical technology company reported total revenue of $26.2 million, down 10% year-over-year, as strong performance in its commercial segment failed to offset weakness in its OEM business.

The company is navigating a challenging environment in its US OA Pain Management business while seeing more positive trends internationally and in its Integrity™ Implant System.

Quarterly Performance Highlights

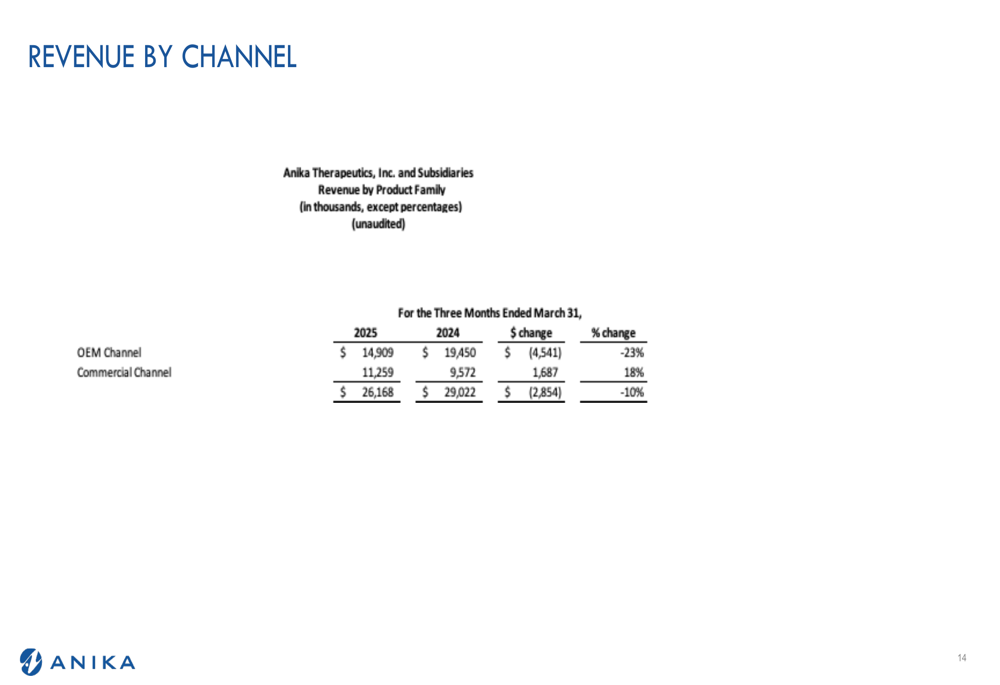

Anika’s Q1 2025 results showed a stark contrast between its two main revenue channels. The Commercial channel grew 18% year-over-year to $11.3 million, driven by strong international OA Pain Management sales and continued sequential growth of the Integrity product line. Meanwhile, the OEM channel declined 23% to $14.9 million, primarily due to lower pricing on Monovisc® and Orthovisc® sales controlled by J&J (NYSE:JNJ) MedTech.

As shown in the following financial highlights:

The company reported a gross profit of $14.7 million, down 23% year-over-year, reflecting both lower OEM revenue and higher manufacturing costs. Operating expenses showed improvement, with R&D expenses decreasing 5% to $6.1 million and SG&A expenses declining 14% to $12.9 million, reflecting cost-cutting measures implemented in previous quarters.

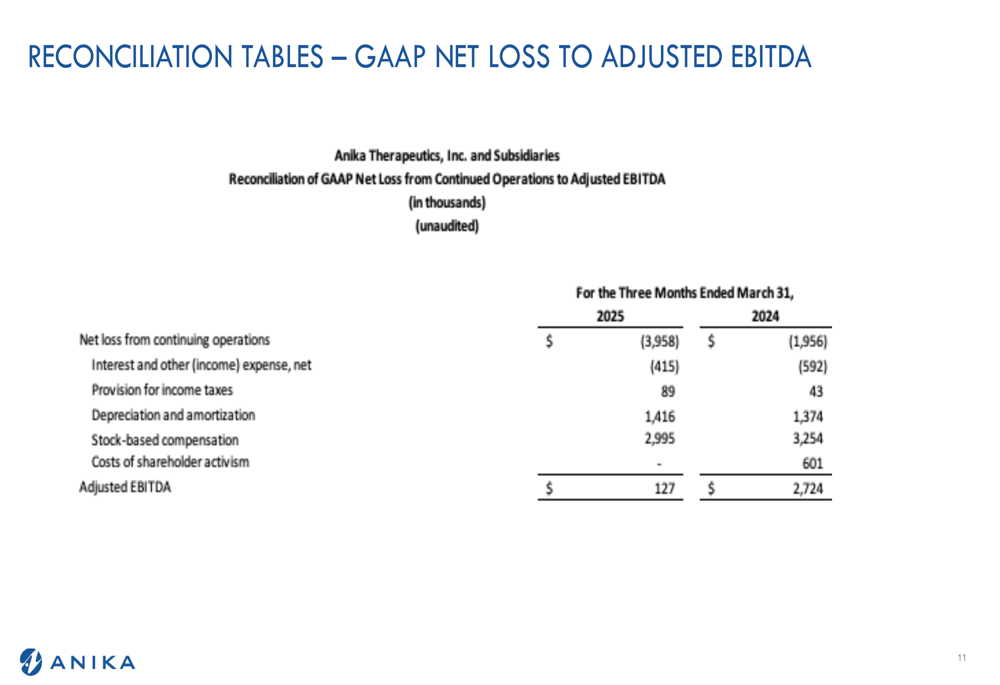

Despite these cost reductions, Anika reported a loss from continuing operations of $4.0 million and adjusted EPS of ($0.06), compared to adjusted EPS of $0.13 in Q1 2024. Adjusted EBITDA was barely positive at $0.1 million, down significantly from $2.7 million in the prior-year period.

The revenue breakdown by channel clearly illustrates the diverging performance:

Revised Guidance

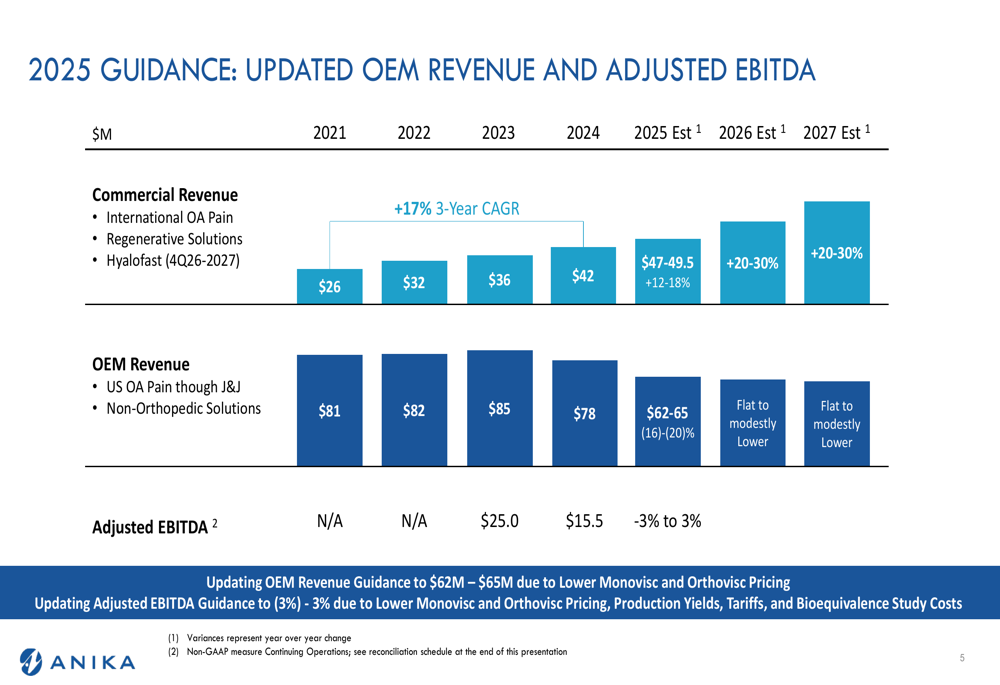

In a significant update, Anika revised its 2025 guidance downward, particularly for OEM revenue and adjusted EBITDA. The company now expects OEM revenue of $62-65 million, representing a 16-20% decline from 2024, worse than the 12-18% decline projected in its Q4 2024 earnings call.

More concerning for investors is the dramatic reduction in adjusted EBITDA guidance, now projected at -3% to 3%, down from the previous 8-10% margin guidance. The company attributed this revision to lower Monovisc and Orthovisc pricing, production yield issues, tariffs, and bioequivalence study costs.

The updated multi-year guidance shows:

Despite these challenges, Anika maintained its positive outlook for Commercial revenue, projecting 12-18% growth to $47-49.5 million in 2025, followed by 20-30% growth in both 2026 and 2027.

Strategic Initiatives

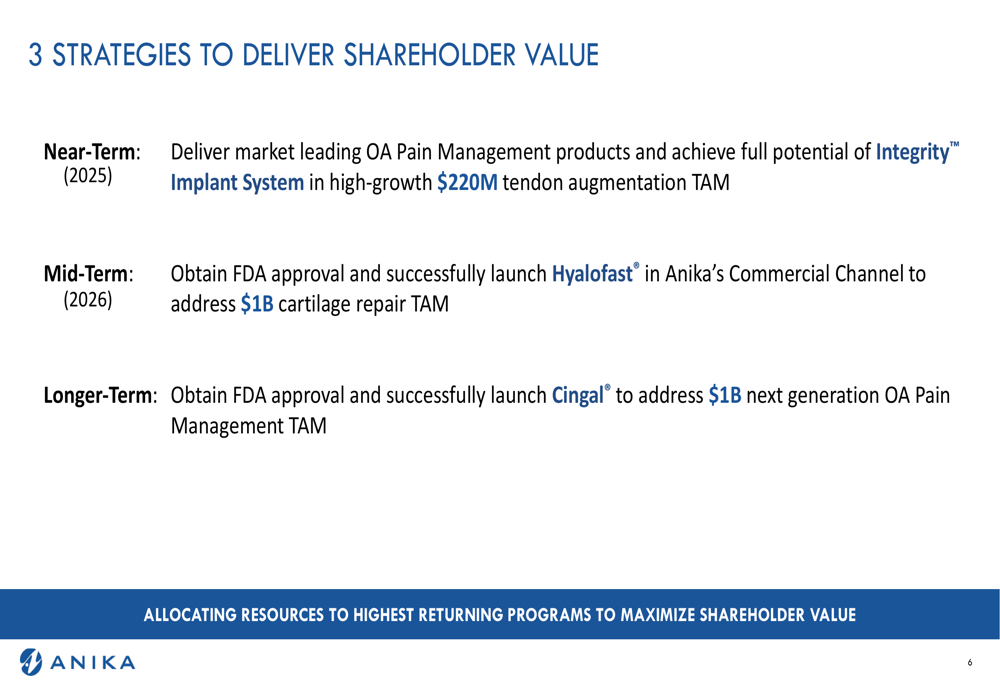

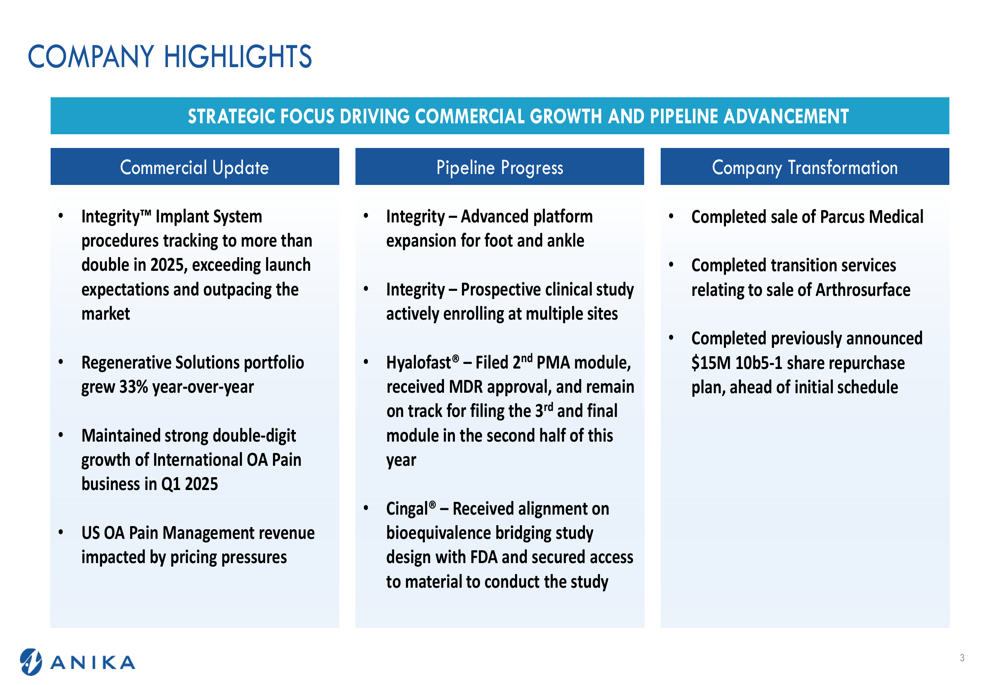

Anika outlined three strategic pillars to deliver shareholder value across different time horizons. In the near term (2025), the company is focusing on delivering market-leading OA Pain Management products and maximizing the potential of its Integrity™ Implant System in the $220 million tendon augmentation market. The company noted that Integrity procedures are tracking to more than double in 2025, exceeding launch expectations.

For the mid-term (2026), Anika aims to obtain FDA approval and successfully launch Hyalofast in its Commercial Channel to address the $1 billion cartilage repair market. The company reported filing the second PMA module and receiving MDR approval, with plans to file the third and final module in the second half of 2025.

The company’s longer-term strategy centers on obtaining FDA approval and launching Cingal to address the $1 billion next-generation OA Pain Management market. Anika reported receiving alignment on bioequivalence bridging study design with the FDA and securing access to materials to conduct the study.

These strategic priorities are illustrated in:

Company Transformation

Anika highlighted several completed transformation initiatives in Q1 2025, including the sale of Parcus Medical (TASE:BLWV), completion of transition services relating to the sale of Arthrosurface, and completion of its previously announced $15 million share repurchase plan ahead of schedule. These moves align with the company’s strategy to focus resources on its highest-returning programs.

Financial Analysis

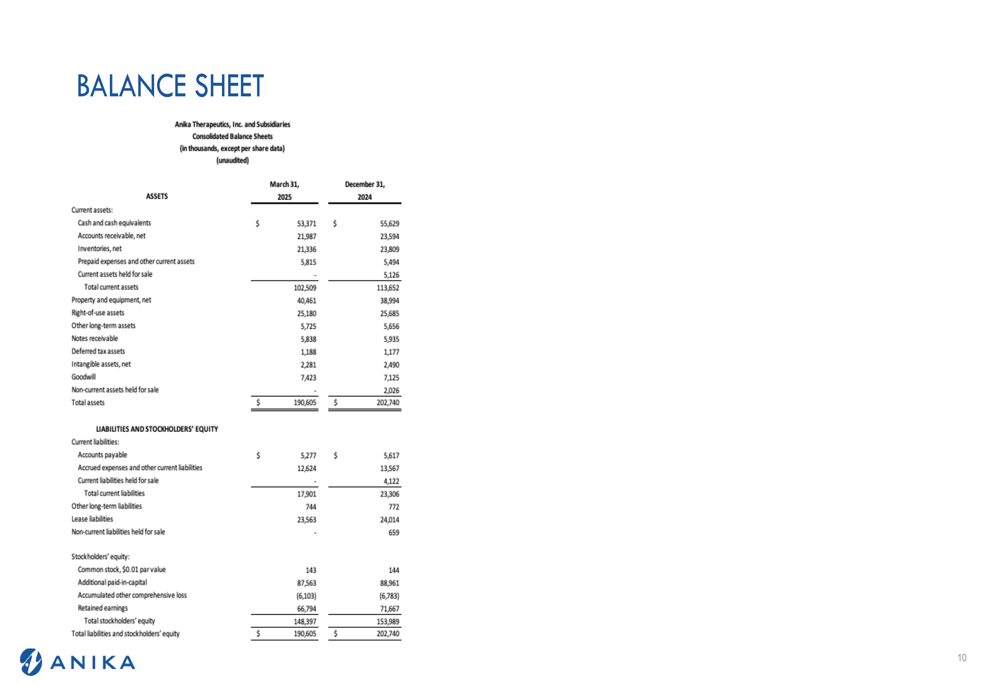

Anika’s balance sheet remains relatively stable, with $53.4 million in cash and cash equivalents as of March 31, 2025, down slightly from $55.6 million at the end of 2024. The company reported total assets of $190.6 million, down from $202.7 million at year-end 2024.

The company’s statement of operations reveals the full impact of the challenging quarter, with gross profit margin declining significantly year-over-year:

The reconciliation of GAAP net loss to adjusted EBITDA shows how the company barely maintained positive adjusted EBITDA in Q1 2025:

Forward-Looking Statements

Looking ahead, Anika faces significant challenges in its OEM business, which it expects to remain under pressure through 2025 and beyond, projecting "flat to modestly lower" performance in 2026 and 2027. The company’s strategy hinges on accelerating growth in its Commercial channel to offset these declines, with particular emphasis on international markets and new product launches.

The success of the Integrity Implant System and progress in the regulatory pathways for Hyalofast and Cingal will be critical to the company’s ability to execute its transformation strategy and return to sustainable growth and profitability. However, the significant downward revision to 2025 guidance suggests that this transformation may take longer and prove more challenging than previously anticipated.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.