ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Anika Therapeutics Inc. (NASDAQ:ANIK) presented its third-quarter 2025 earnings on November 5, revealing a tale of two business channels. The medical technology company, which specializes in joint preservation and restoration solutions, demonstrated strong commercial channel growth that partially offset significant declines in its OEM business. The stock responded positively to the results, jumping 8.83% to close at $10.48, after reaching as high as $10.60 in premarket trading.

The company delivered a surprising earnings beat with adjusted EPS of $0.04, significantly outperforming analyst expectations of a $0.18 loss. This performance comes amid challenging market conditions in the orthopedic space, where pricing pressures and shifting healthcare dynamics continue to impact industry players.

Quarterly Performance Highlights

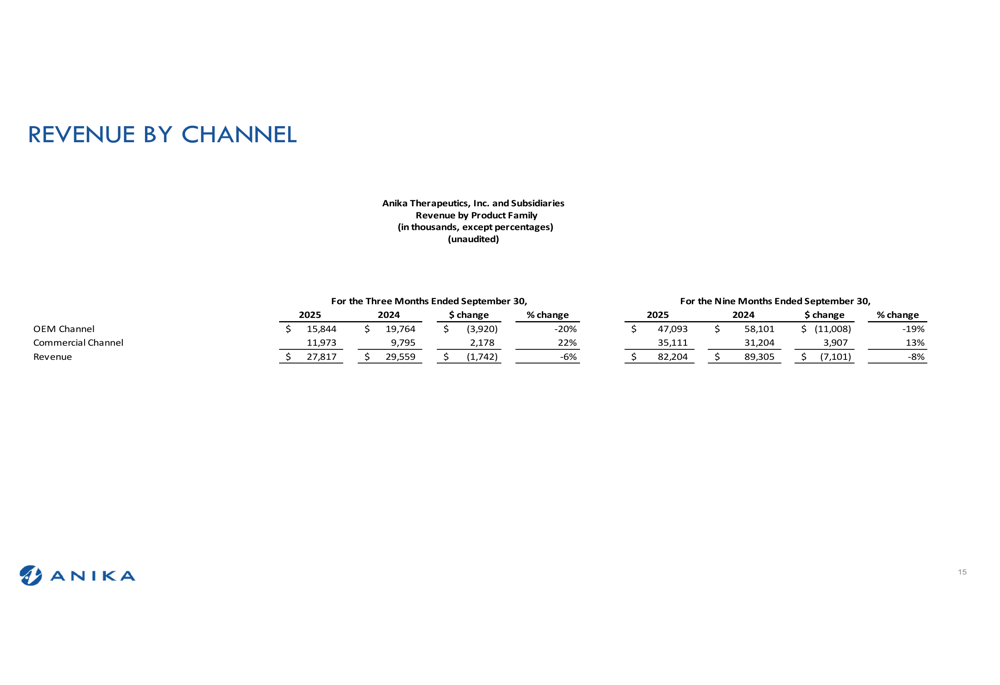

Anika's third quarter revealed contrasting performance across its business segments. The company's Commercial Channel revenue increased 22% year-over-year to $12.0 million, driven by a 25% growth in its Regenerative Solutions portfolio and 21% growth in International OA Pain business.

The Integrity Implant System, a key growth driver, continued to outpace the broader soft tissue augmentation market with approximately 500 cases performed in Q3, bringing the total number of surgeon users to nearly 300. The company noted that Integrity remains on pace to more than double procedures and revenue in 2025.

As shown in the following chart of Integrity Unit Sales since launch:

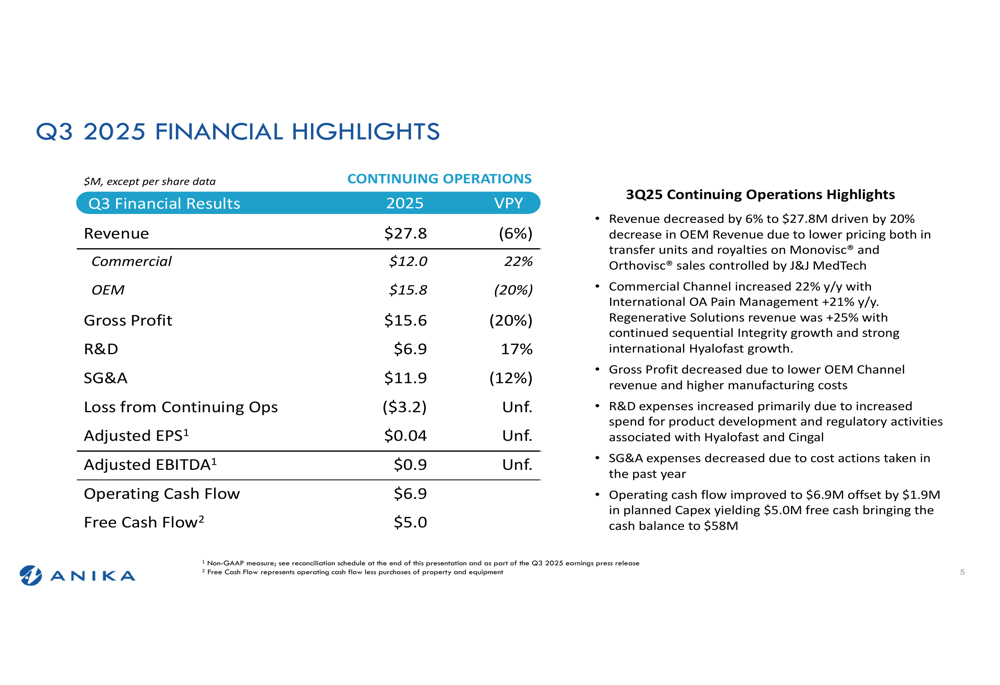

However, these gains were offset by a 20% decline in OEM Revenue, which fell to $15.8 million. The company attributed this decrease to lower pricing in both transfer units and royalties on Monovisc and Orthovisc sales controlled by J&J MedTech. As a result, total revenue decreased 6% year-over-year to $27.8 million.

The following slide provides a comprehensive overview of the company's Q3 highlights:

Detailed Financial Analysis

Anika's financial results reflect the divergent performance of its business segments. While revenue declined 6% overall, the composition of that revenue continues to shift toward the higher-growth Commercial Channel.

The company's gross profit decreased to $15.6 million, down 20% year-over-year, due to the lower OEM Channel revenue and higher manufacturing costs. Operating expenses showed mixed trends, with R&D expenses increasing 17% to $6.9 million as the company invested in product development and regulatory activities for Hyalofast and Cingal. Meanwhile, SG&A expenses decreased 12% to $11.9 million, reflecting cost discipline.

The detailed financial breakdown is illustrated in the following slide:

Despite revenue and margin pressures, Anika generated $6.9 million in operating cash flow and $5.0 million in free cash flow during the quarter, bringing its cash balance to $58 million. The company also commenced a $15 million share repurchase program, signaling confidence in its long-term prospects.

A clearer picture of the revenue split by channel is provided in this breakdown:

Strategic Initiatives

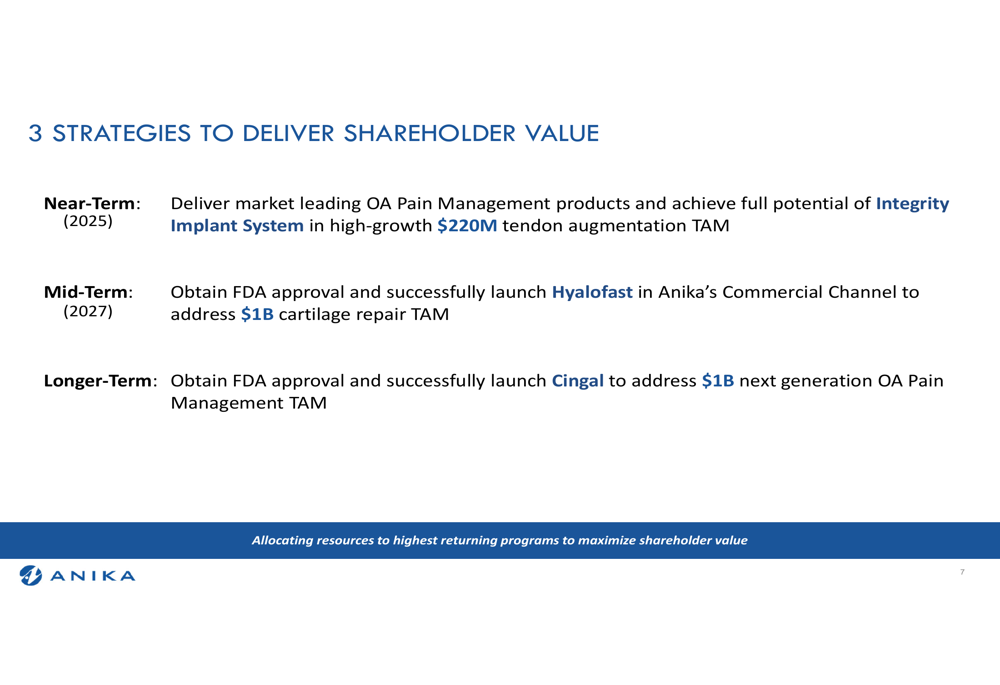

Anika outlined three strategic horizons aimed at delivering shareholder value. In the near term (2025), the company is focused on maximizing its OA Pain Management products and achieving the full potential of the Integrity Implant System in the $220 million tendon augmentation market.

For the mid-term (2027), Anika is pursuing FDA approval and launch of Hyalofast in its Commercial Channel to address the $1 billion cartilage repair market. The company submitted its Hyalofast PMA on October 31, supported by U.S. Phase III data showing statistically significant improvements in key secondary endpoints.

The long-term strategy centers on obtaining FDA approval and successfully launching Cingal to address the $1 billion next-generation OA Pain Management market. The company has completed the first of two Cingal toxicity studies and begun patient screening for the bioequivalence study.

This strategic roadmap is illustrated in the following slide:

Forward-Looking Statements

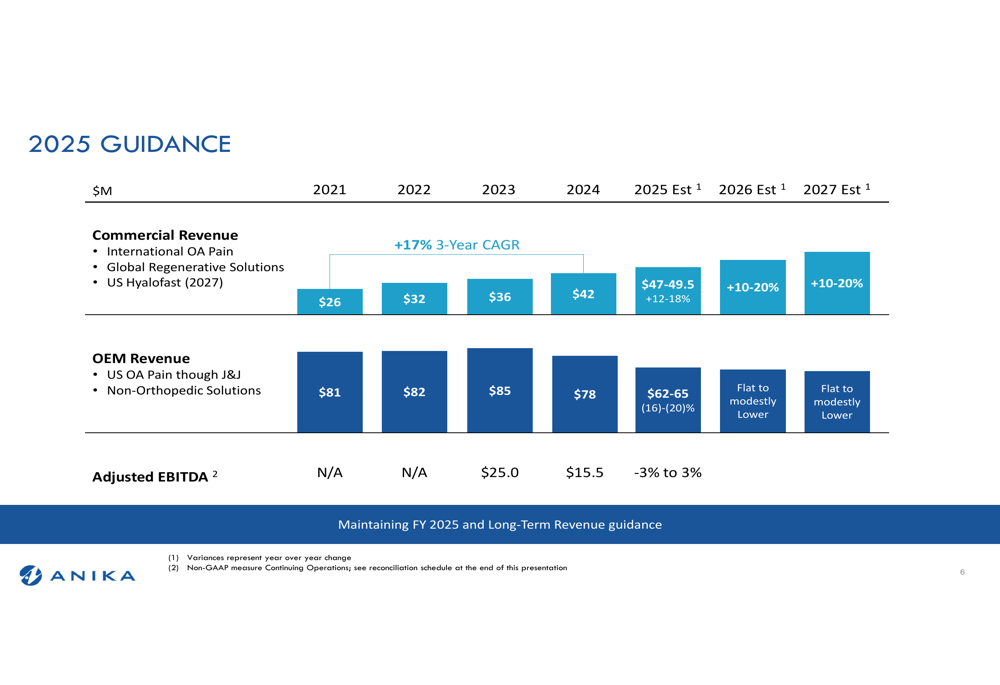

Anika maintained its full-year 2025 guidance, projecting Commercial Revenue of $47-49.5 million (representing 12-18% growth) and OEM Revenue of $62-65 million (a 16-20% decrease). The company also provided longer-term estimates, forecasting 10-20% annual growth for its Commercial Revenue through 2027, while OEM Revenue is expected to remain flat to modestly lower in the coming years.

The company's adjusted EBITDA for 2025 is projected to range from -3% to +3%, reflecting ongoing investments in growth initiatives balanced with cost discipline.

The complete guidance is presented in the following slide:

Dr. Cheryl Blanchard, CEO of Anika, expressed optimism during the earnings call, stating, "We're feeling very bullish in the U.S. market with our team coming from a position of strength." Meanwhile, CFO Steve Griffin emphasized the company's focus on expense management, noting, "We continue to be focused on improving our expense profile to deliver positive operating cash flow."

As Anika navigates the transition toward a more commercially-driven business model, investors will be watching closely for continued execution on its three-horizon strategy and the successful development of its pipeline products. The positive market reaction to the Q3 results suggests growing confidence in the company's ability to offset OEM challenges with commercial growth while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.